CX - CEMEX: An Undervalued Leader In Sustainable Cement

2023-05-28 03:22:17 ET

Summary

- CEMEX is taking proactive steps to address climate change—a must for any cement manufacturer.

- CEMEX has a strong balance sheet, generates consistent EBITDA and cash flow, and is building equity.

- A discounted free cash flow model indicates CX stock is undervalued, and results are only mildly sensitive to demand.

CEMEX, S.A.B. de C.V. (CX) is a large cap, publicly traded company that produces and distributes cement and derivatives. On par with the cement industry, CEMEX has prioritized its climate action goals and is making good progress toward its 2030 carbon reduction goals. CEMEX approaches carbon reduction mainly through applying its hydrogen injection technologies to increase the efficiency of its alternative fuels, and CEMEX also uses significant amounts of biomass waste to fuel their kilns. The company’s commitment to sustainability initiatives along with their relatively healthy balance sheet with falling debt to equity ratio make the stock appealing. A discounted free cash flow model suggests that the stock is undervalued as well, with an intrinsic value of about $13.

The High Carbon Intensity of Cement Manufacturing

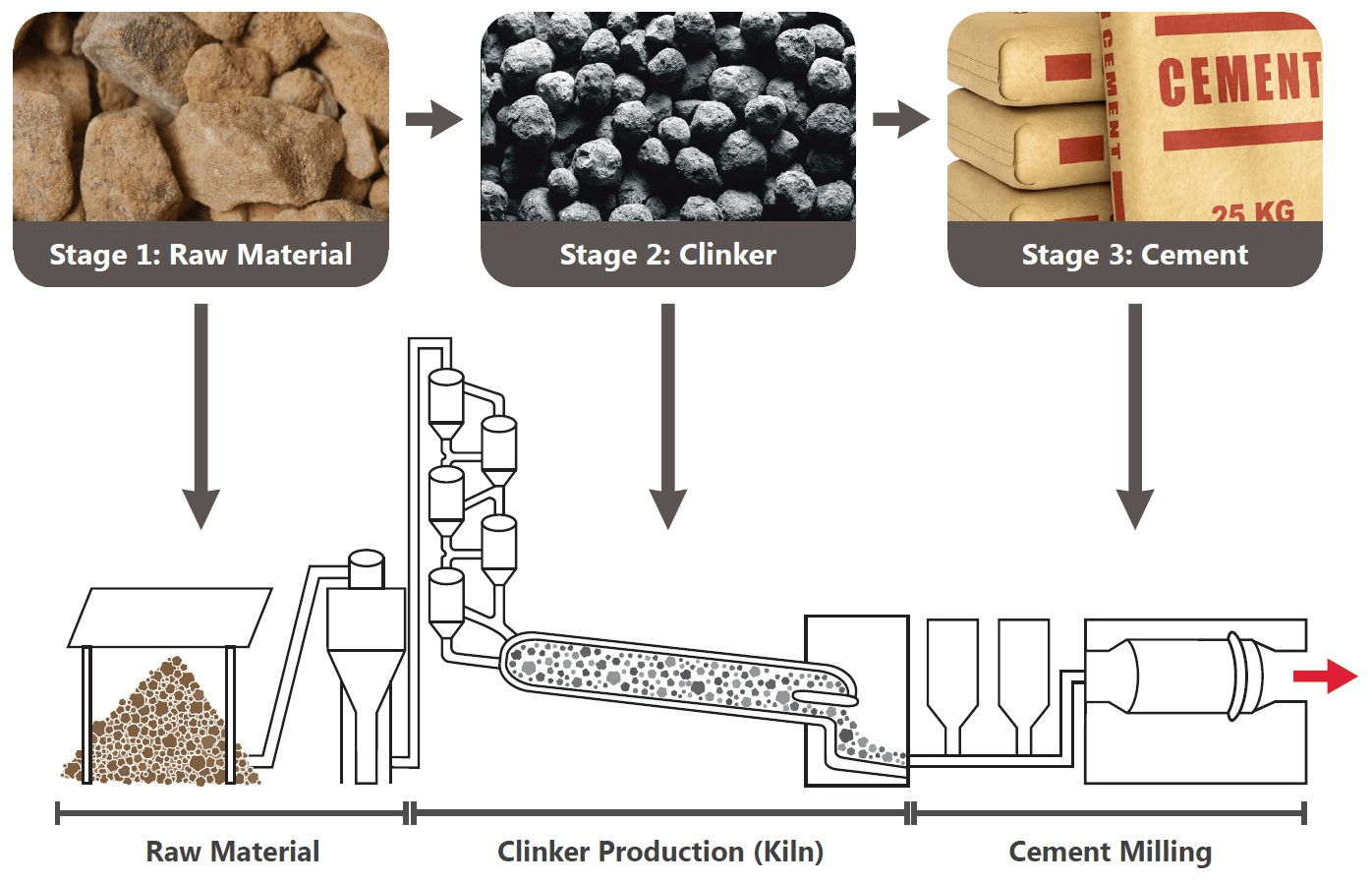

Cement production has a staggering carbon footprint that accounts for about 7% of global CO 2 emissions. As shown in Figure 1, the main stages of cement manufacturing are: (i) excavation and milling of limestone; (ii) heating raw materials to high temperatures in a kiln to form clinker, and (iii) grinding clinker and mixing with other ingredients to produce cement. Cement is the second-most consumed material on earth—second only to water—and cement demand is projected to grow a CAGR of 4-5%. Reducing CO 2 emissions in view of concrete’s increasing demand is a serious global predicament to be solved.

Figure 1. Schematic showing key steps of cement manufacturing. (Cement Industry Federation)

{kind=link}

Most CO 2 emissions from cement production occur in the kiln. There, calcium carbonate (CaCO 3 , limestone) is converted to calcium oxide CaO, and CO 2 is released as a side-product, i.e.

CaCO 3 -> CaO + CO 2.

However this reaction, alone, is an oversimplified generalization; many other reactions occur involving clays, magnesium compounds, alumina, and iron oxide that all liberate CO 2 . Generation of CO 2 from these reactions accounts for about ~480 kg of CO 2 per ton of cement product. However, the kiln must also be heated to 1450 °C, and these conditions require combustion of fossil fuels, generating another 300 kg of CO 2 per ton of cement produced. The total CO 2 generated during cement manufacture can exceed 800 kg of CO 2 per ton of cement.

The industry has collectively realized the need to achieve net-zero carbon emissions by 2050. Future legislation will likely reward cement firms who succeed in hitting climate milestones and will punish those who fail. Therefore, investors should avoid any cement-producing company who is not taking the industry’s sustainability initiative to heart.

CEMEX's Climate Action Priorities

As of 2021, CEMEX has reduced their specific CO 2 emissions by 26% compared to their 1990 baseline, and they are on-track for a 40% reduction by 2030. CEMEX reduces their carbon footprint mainly through: (i) utilization of fly-ash, and (ii) utilization of alternative fuels, including injection of hydrogen into raw material mixture.

CEMEX uses fly ash, a byproduct of coal-burning electric power plants, or blast furnace slag as a clinker substitute, decreasing the amount of cement needed by 20-30%. Further, fly ash improves cement workability, and it improves the strength of the cured concrete. The main issue facing fly ash is its availability: as coal phases out, fly ash is becoming scarcer.

CEMEX uses alternative fuels to fuel their kilns for clinker production. In their 2022 annual report, they claim that their fuel mix comprises of 35% alternative fuels. In Europe, CEMEX is using hydrogen to maximize fuel efficiency in all of their cement plants, and they are entering partnerships to access new hydrogen injections technologies. One question about hydrogen injection, is where the hydrogen comes from because if it is natural gas derived, it should not necessarily count as a ‘green’ energy source. However, CEMEX is also using biomass waste and non-recyclable materials to fuel their kilns. This reduces landfill waste streams and represents an alternative to more expensive fossil fuels. With these strategies at play, three of CEMEX’s cement plants are already producing cement at less than 430 kg of CO 2 per ton of product, which is nearly half of the baseline level described above explained earlier.

CEMEX’s Capital Structure

The evolution of CEMEX’s capital structure is shown in Figure 2. The company has built up over $10B of equity (dark blue in the figure) and has effectively managed debt over the past couple of years. Careful debt management continues to be an important part of their strategic plan. Their accumulated equity now exceeds their market cap. With significant intangible assets (orange in Figure 2), CEMEX is appealing from a valuation standpoint and has a relatively low price-to-book ratio of 0.8. Currently, one dollar invested in CEMEX corresponds to about $1.00 of equity with another $1.50 of liabilities and with an annual EBITDA yield of about $0.25.

Figure 2. Evolution of CX’s capital structure from 2019 to 2022. (Data provided by Financial Modeling Prep, and figure created by Absolute Valuation)

CEMEX’s Valuation

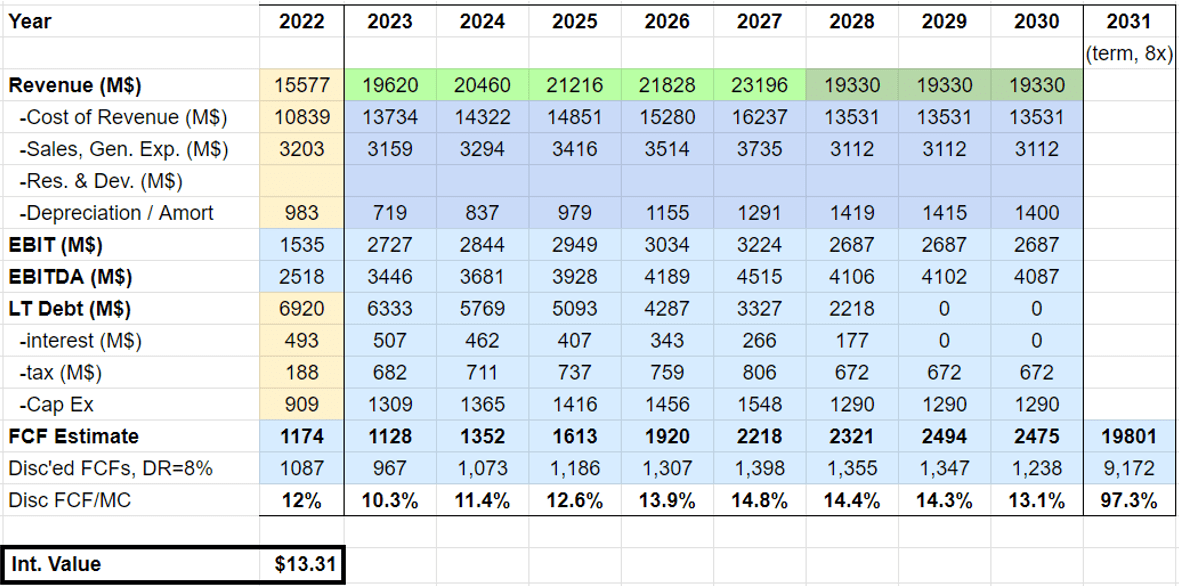

CEMEX’s healthy balance sheet and steady earnings make a discounted free cash flow analysis straightforward. The analysis is summarized in the table below. The light green cells show revenue predictions and are taken directly from analysts (Seeking Alpha's website), and revenue is conservatively frozen at just over $19B for 2028 and beyond. The cost of revenue is taken to be 70% of each year’s revenue, which is at the upper end of the range for the past five years. Similarly, sales and general expenses, including depreciation, is conservatively taken to be 23% of each year’s revenue figure projection. Depreciation is estimated to be 1/5 of the prior five years of cap ex investment. EBIT is calculated as the remaining revenue, and EBITDA is calculated by adding back depreciation to EBIT. Interest is assumed to be 8% of long-term debt, compounded annually, and tax is 25% of EBIT. The resulting free cash flow is calculated by subtracting interest, tax, and cap ex investment from EBITDA. Free cash flow is used to reduce long term debt, and, under this scenario, all debt is paid by 2029. Any remaining cash flow could count as retained earnings to build equity, or it could be dispersed to shareholders. Discounting future cash flow streams at a discount rate of 8%, the model projects CX’s intrinsic value of about $13, suggesting the stock is currently undervalued.

Figure 3. Table showing discounted free cash flow model (Figure created by Absolute Valuation)

{kind=link}

Risks and Demand Uncertainty

Probably the greatest risk to CEMEX stock performance is the uncertainty in demand. Economic conditions, the war in Ukraine, or another pandemic could all impact demand. Low demand can lead to decrease in sales / price and revenue. To estimate the impact of low demand, the revenue numbers in the DFCF model discussed previously were reduced by 10% and 30%, and the model’s predicted intrinsic value decreased to $11.29 and $9.95, respectively, which are still well above today’s stock price.

Take-home Message

In a nutshell, CEMEX is taking appropriate steps toward reducing carbon. However, all cement producers including CEMEX need to be held accountable to achieving carbon reduction milestones by both governmental agencies and by their customers. I rate the stock CEMEX as a long-term buy because I believe: (i) they will continue to lead in carbon reduction, (ii) they have a fairly strong balance sheet, good access to capital, and the company is consistently generating EBITDA and building equity; (iii) a discounted free cash flow model suggests CEMEX is currently undervalued, and (iv) while cement demand may be difficult to predict, the company is globally diversified, and the free cash result is only mildly sensitive to variations in revenue.

For further details see:

CEMEX: An Undervalued Leader In Sustainable Cement