CX - Cemex: Great Potential But Poor Finances

2023-09-12 17:49:48 ET

Summary

- Strong demographics and rising middle class in LATAM, aging homes, and overdue infrastructure renewal in the USA are driving forces behind the growing demand for new construction.

- Cemex is a cement producer perfectly positioned to benefit from those dynamics. More than 50 % of its revenue originates from the US and Mexico.

- The company has performed well in the last few quarters with rising revenue and profit margins. However, its liquidity is far from adequate.

- I give a hold rating because I believe Cemex has insufficient liquidity despite the company`s potential.

Thesis

Investing in cement producers is a bet on growing demand for construction. CEMEX ( CX ) might benefit from those processes. More than half of its revenue originates from USA and Mexico. Both countries have excellent demographics and a deficit of newly built homes.

What I do not like is the company's financials. The weakest point is its liquidity, despite the rising profit margins. In 2025 and 2026, the company has a large part of its debt due. While the revenues are adequate to cover it, more is needed to serve as a buffer in case of liquidity issues. Such a problem can become a solvency crisis, and the company must sell assets to cover its obligations.

To clarify, Cemex is not a distressed business. However, the lack of liquidity in case of unexpected events might turn into such. In the long term, if the company keeps growing profits and repays its debts, it might turn attractive to my taste. Considering the above facts and Mr. Market's fair valuation, I give a hold rating.

Big Picture

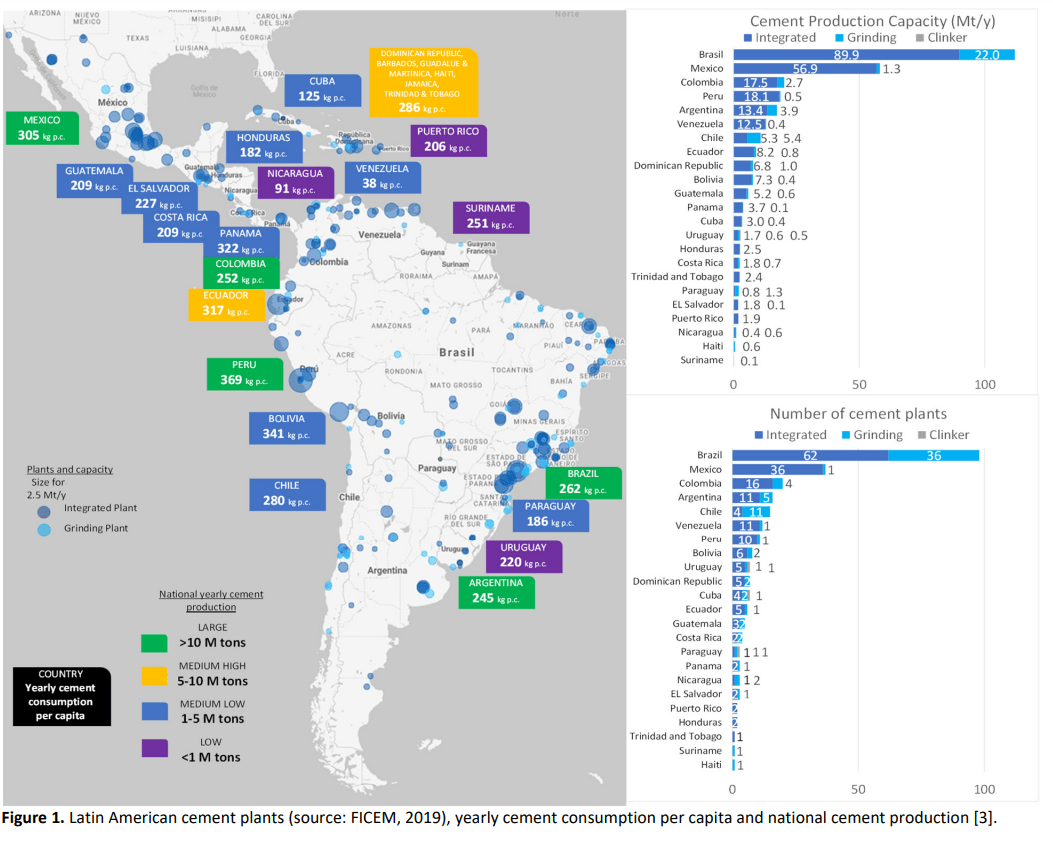

To understand the potential for growth in any business, we must examine the demand and supply. Mexico is among the major cement producers in LATAM. The image below shows the production capacity by country:

{kind=link}

Mexico is second to Brazil in production capacity and number of cement plants. The country has an advantage compared to the rest of its peers. It is part of NAFTA, and the USA and Canada are significant drivers for growing cement demand.

LATAM is passing through a transformative period. A growing number of its population is entering the middle class, thus creating demand for new homes. That translates into an increasing demand for cement. The quote from Mordor Intelligence summarizes the above:

Mexico must invest nearly 4% of its gross domestic product annually to build 800,000 housing units over the coming two decades to keep up with demand. That comes out to 3.87% of the (country’s) GDP.

Demand for houses in Mexico is rising while the number of people living together is shrinking. In 1990, there were five people per home in Mexico. By 2020, there were only 3.6 per home.

A more affluent population creates a reflexive cycle of higher spending on better basics and discretionary goods. Growth in the “old” economy (homebuilders, heavy industry, utilities) characterizes the first wave. The countries in LATAM have already passed that threshold.

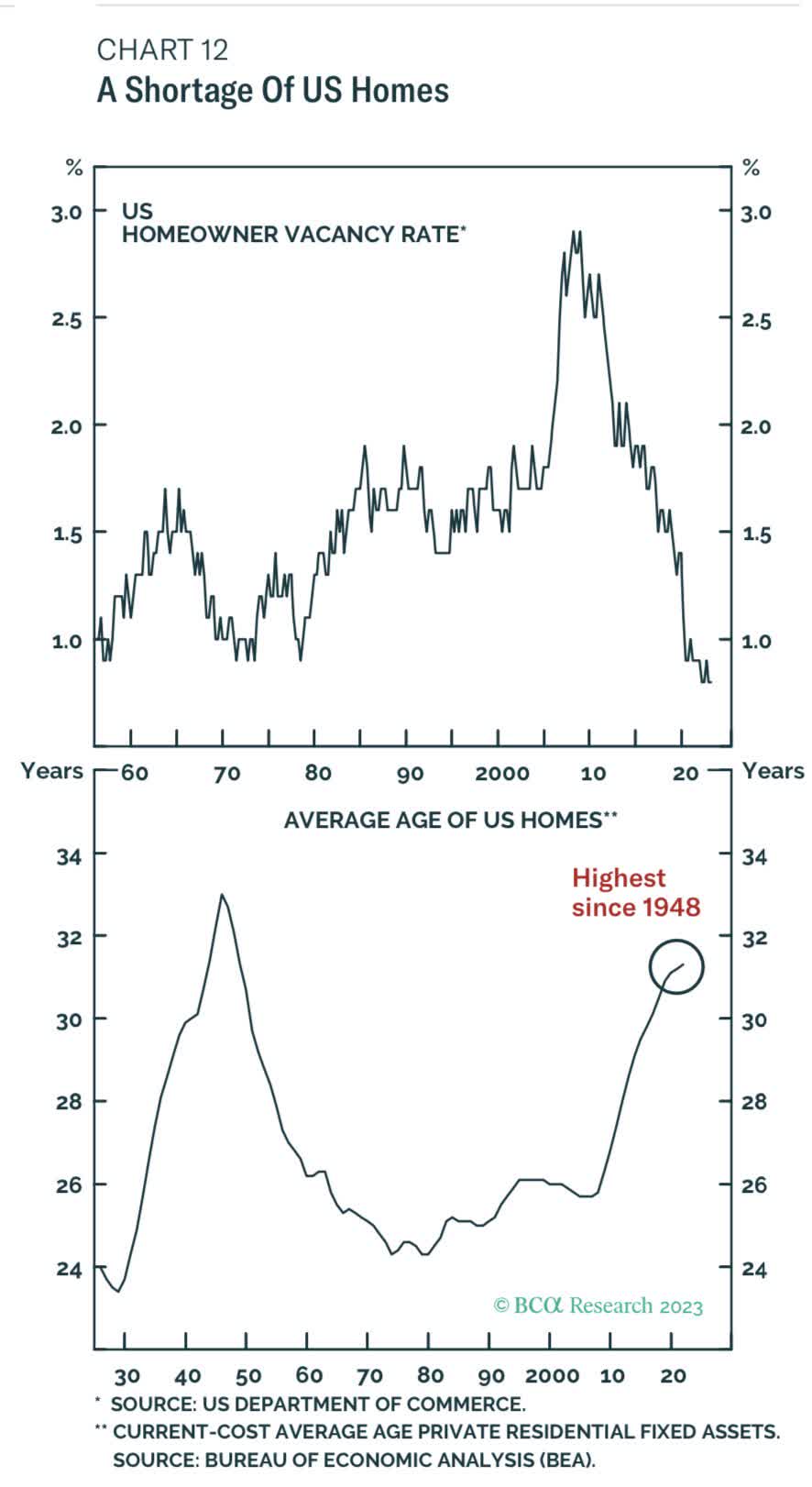

On the other hand, in the US, the demand for new homes is driven by aging homes. The chart from BCA research shows the average age of US homes and homeowner vacancy rate.

{kind=link}

Both sides of the equation will cause a growing deficit. The supply side will shrink due to the aging properties while the demand will keep rising because of healthy demography. Such imbalance creates a perfect opportunity for cement producers.

Company Overview

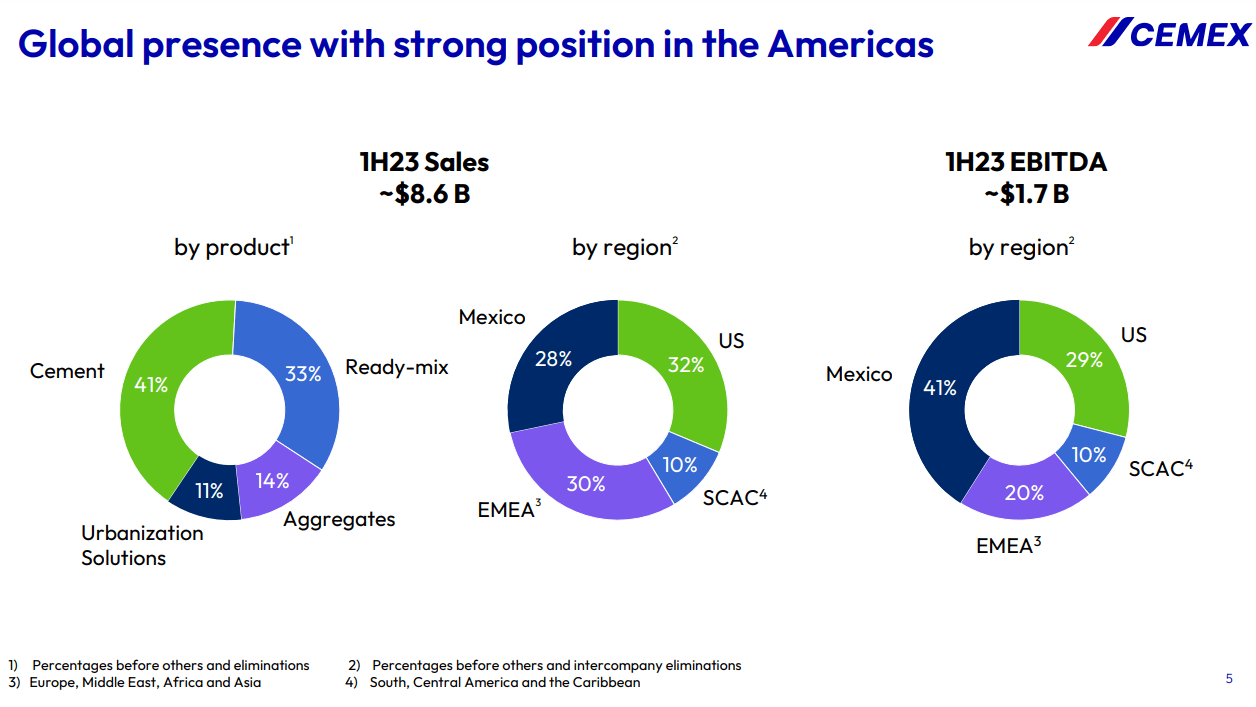

CEMEX is the fifth largest cement producer in the world. It is based in Mexico, and over 60% of its revenue originates from the Western Hemisphere. The chart below from the last company presentation illustrates the revenue distribution by geography and products:

{kind=link}

Having exposure to the Americas is a huge advantage. As mentioned earlier, the USA and LATAM are experiencing growing demand for housing. The Western Hemisphere's strong demographics are a long-term economic growth driver. The latter means more homes and better infrastructure are needed.

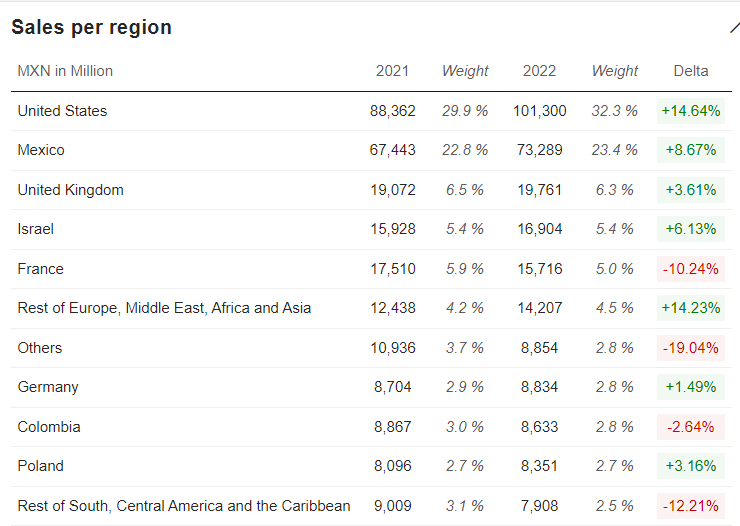

The image from Market Screener shows in detail, by country, the revenues are as follows:

{kind=link}

The largest market is the United States, and the second is Mexico.

Cemex provides a range of cement products, such as specialty cement goods, masonry cement, and Portland cement. Buildings, roads, bridges, and other infrastructure projects all use these. Cemex offers ready-mix concrete, too, ready to mix on the construction site.

The company sells a range of aggregates, including sand, gravel, and crushed stone. Totals are crucial for creating concrete, asphalt, building roads, and other projects. Lastly, Cemex provides various building materials, such as asphalt, precast concrete, architectural, cement, concrete, and aggregates.

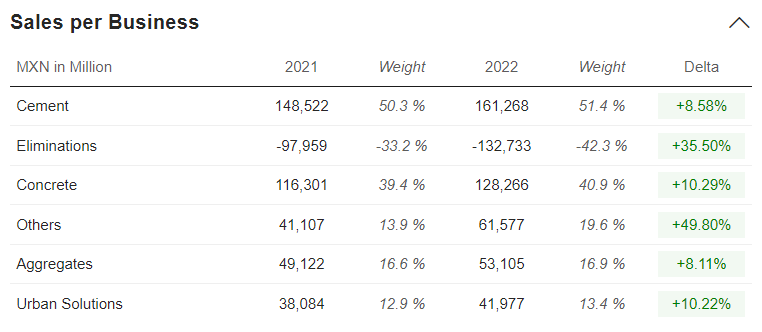

The revenue distribution by-product is shown on the chart below:

{kind=link}

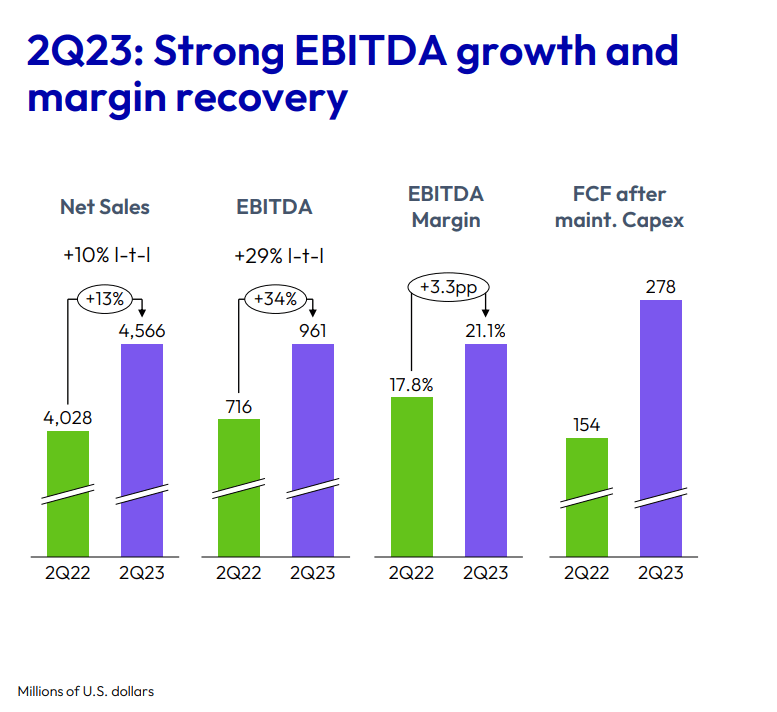

All discussed variables are fundamental catalysts for cement demand. Cemex's performance in the long term is well-positioned to benefit from that. The company's profit is in line with the discussed fundamentals. The chart below from the last presentation illustrates Q2 2023 results.

{kind=link}

The most important profitability metric for me is the free cash flow. Its simplicity makes it easy to understand and difficult to mess up. Cemex succeeded in transforming growing sales into rising cash flows.

Company Financials

Cemex has an acceptable balance sheet. The chart below presents a few metrics I use to examine balance sheet quality.

| EBITDA/Interest expense |

| 8.4 |

| EBITDA-CAPEX/Interest expense |

| 5.5 |

| Quick Ratio |

| 0.9 |

| Current Ratio |

| 0.5 |

| Net debt/EBITDA |

| 2.2 |

| Net Debt/ EBITDA - CAPEX |

| 3.4 |

| Long-term debt/Equity |

| 52.6 % |

| Total debt/Equity |

| 53.2 % |

| Total liabilities/Total assets |

| 55.4 % |

The low quick and current ratios are not adequate. They are partially compensated for by growing revenue and cash flows, thus providing liquidity. In the long term, such low values are unhealthy for a company's liquidity, especially for heavy asset businesses like cement production.

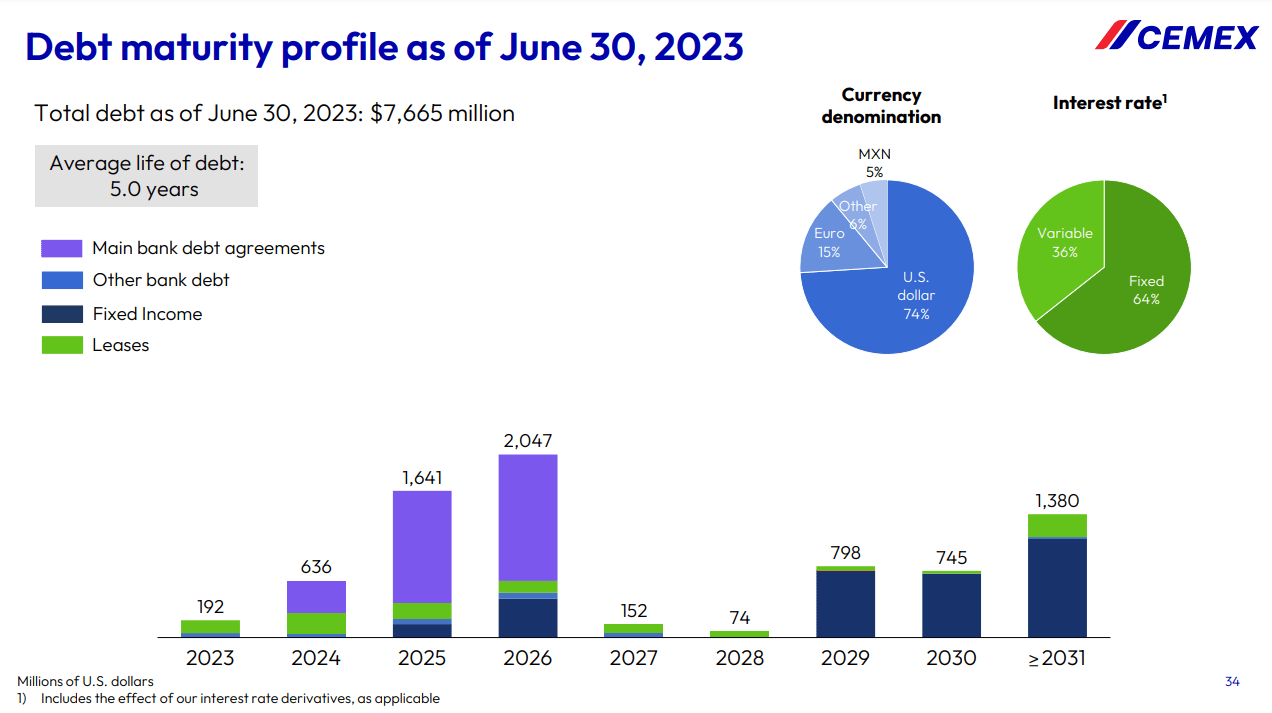

In 2025 and 2026, Cemex has a large portion of its debt maturing. The image below shows the company's debt structure:

{kind=link}

In the last few years, the company realized rising operating profits. If Cemex cannot keep the current growth rate, it might have to refinance its debts under dire terms. The troubles arise from higher interest rates. The existing debts are with much lower fixed rates.

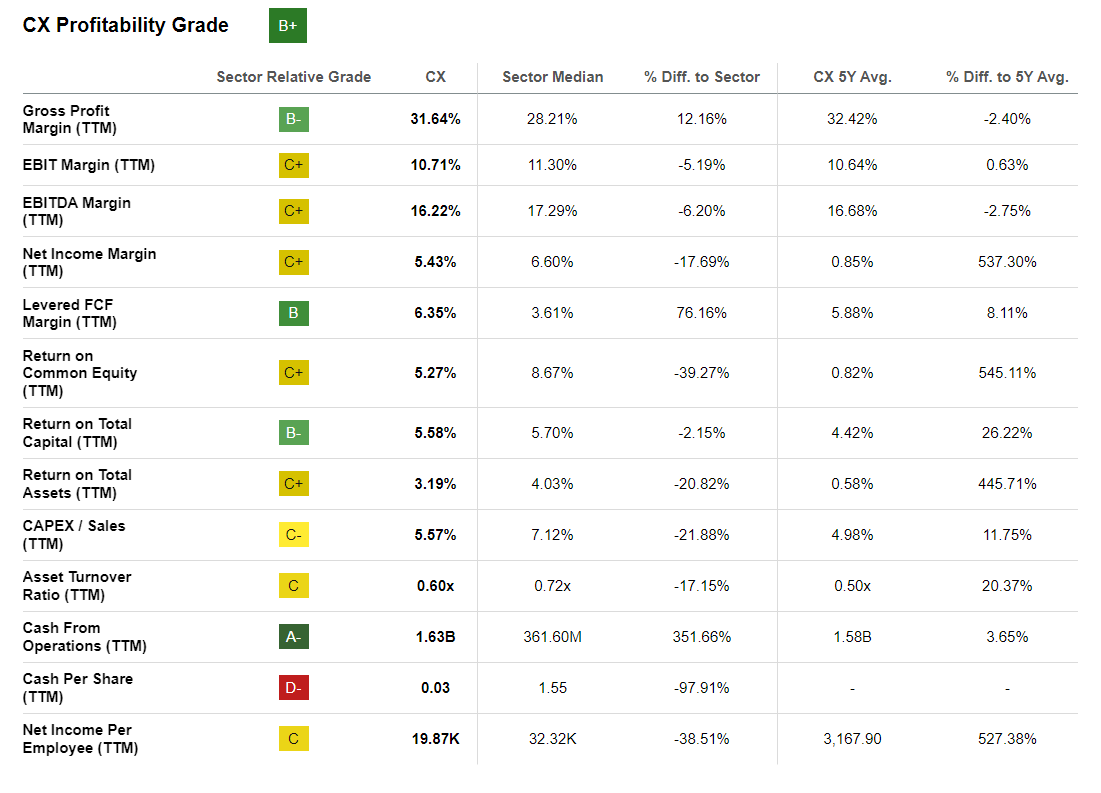

The following image compares Cemex's profitability with the industry and the company's five-year average results:

{kind=link}

The numbers are below the industry average, barely beating the company's five-year average. One positive development is ROE growth from 0.82% to 5.27% TTM. That growth is supported by rising efficiency measured by Net Income per employee. The latter has grown six times from its five-year average.

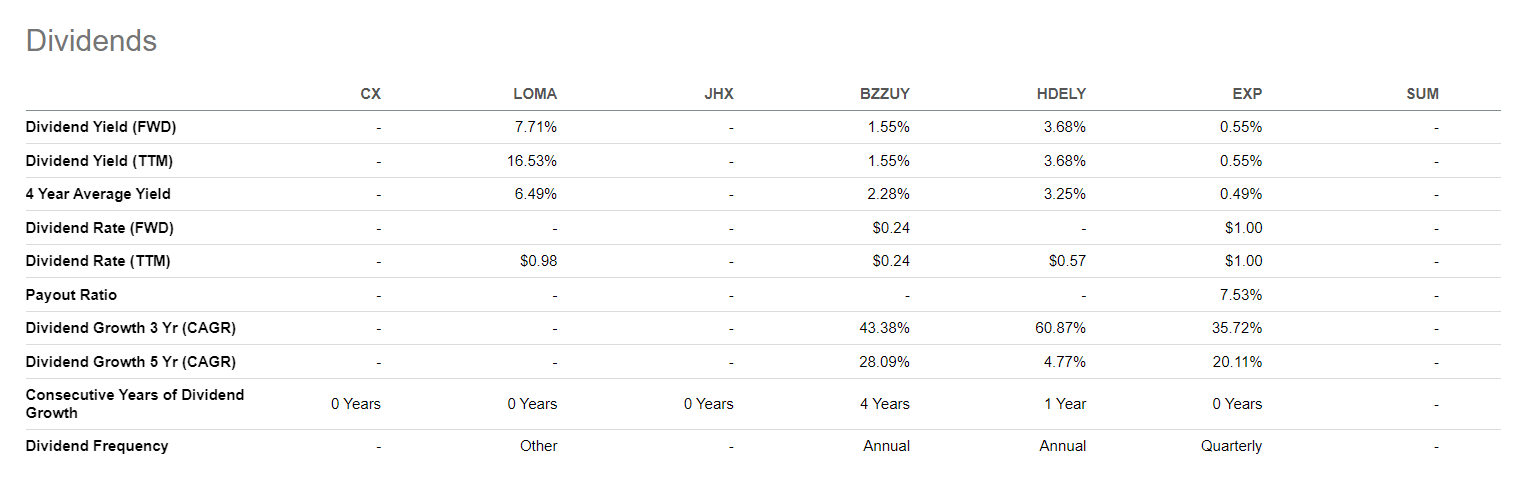

The company does not distribute dividends, as seen in the image below:

{kind=link}

Loma Negra ( LOMA ) is a primary Argentinean cement producer and has paid dividends with excellent yields for the last three years.

Valuation

I use a 2 Stage Discounted Free Cash Flow Model by Professor Damodaran to calculate Cemex's fair value. For equation inputs, I use his database and Seeking Alpha.

Assumptions and inputs:

- Risk-free rate is equal to the 5Y average of US long-term Government bond Rate - 2.2%

- Mexico's equity risk premium is 7.9 %

- Construction Supplies unlevered Beta 1.03

- Cemex Debt to Equity ratio 53%

- Cemex effective tax rate 30%

The above parameters are inputs in the following steps:

1. Calculate Levered Beta with the formula below:

Levered Beta = Unlevered Beta * (1+D*(1-T)/E)

2. Calculate the discount rate (discount rate as the cost of equity) using the resulting value for leveraged beta. The formula I use is:

Cost of Equity = Risk Free Rate + (Levered Beta * Equity Risk Premium)

3. I calculate the present value of discounted free cash flows for ten years using 2024 FCF estimates from Market Screener. I assume the FCF will grow at a stable rate of 9.7%.

Market Screener Market Screener

{kind=link}

4. I then calculate the Terminal Value of the free cash flows over ten years at stable growth into perpetuity, g, and the resulting discount rate. Then, I calculate the present value of the Terminal Value:

Terminal Value = FCF 2033 × (1 + g) ÷ (Discount Rate - g)

Present Value of Terminal Value = Terminal Value ÷ (1 + r) 10

5. Sum the final results of stage 1 and stage 2. Their sum is called the Total Equity Value (TEV);

Total Equity Value = Present value of next ten years cash flows + Terminal Value

6. Divide the TEV by the total number of company-issued shares. The result is the intrinsic value, which I compare against the current market price.

For Cemex, I get the following results:

Levered Beta = 1.08

Discount Rate = 10.09 %

Total Equity Value = $ 10,625,000,000

Total shares outstanding = 1,475,600,000

Intrinsic value per share = $ 7.19

Current market price = $ 7.19 (as of Sept 11, 2023)

The company's value based on DCF matches Mr. Market's offer. The current market price does not provide a margin of safety in my view.

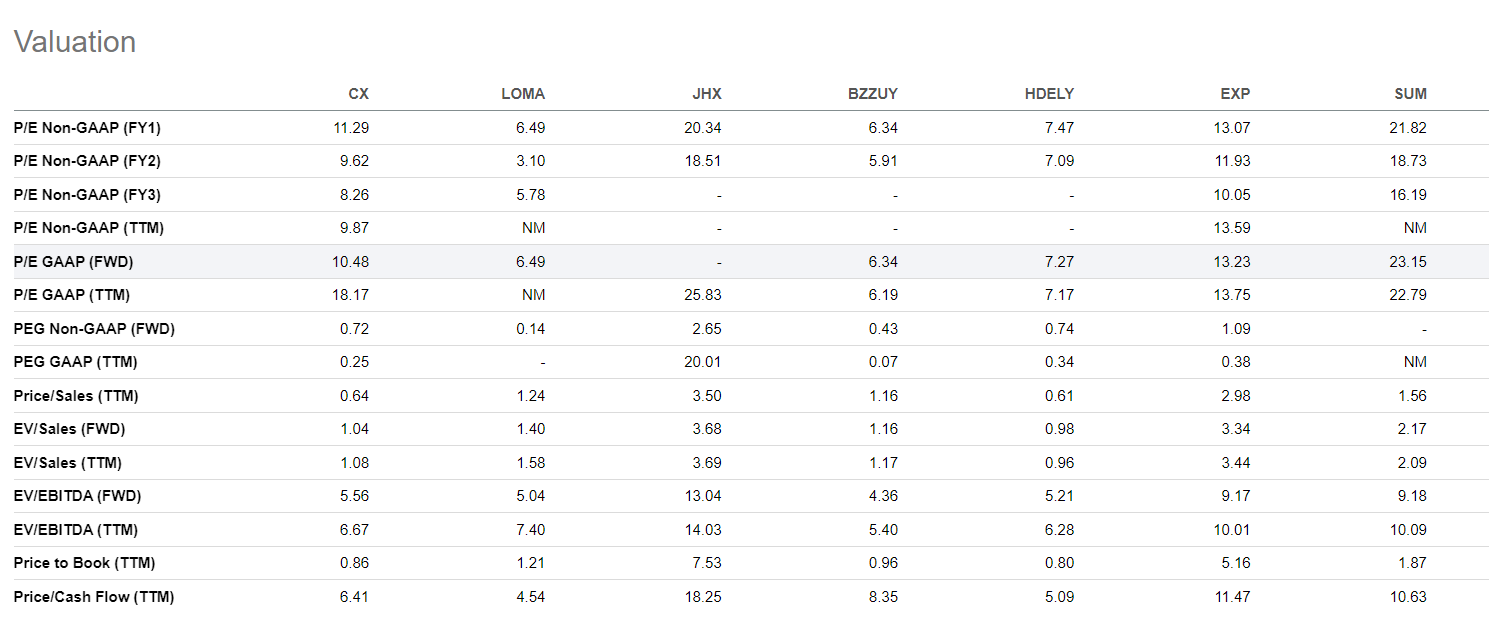

{kind=link}

Using EV/Sales and Price/Cash Flow, Cemex is cheaper than its peers. LOMA, for me, offers better value due to dividends and is cheaper based on Price/Cash Flow, however.

Risks

The most significant risk for CEMEX is declining demand for new construction. The latter depends primarily on economic conditions: inflation, interest rates, and economic growth. The cement business is complex, and operational risk is a heavy burden. Safety procedures, complex machinery, and highly qualified personnel are constant challenges. Those risks are common for all cement producers. As discussed above, insufficient liquidity is the primary risk carried by Cemex.

Conclusion

Cemex is one of the largest cement producers in the Western Hemisphere. Its primary sources of revenue are the USA and Mexico. Both countries are experiencing rising demand for new homes. The cement demand will follow in my opinion. However, Cemex's balance sheet could be more impressive. It has to repay more than 50% of its debts in three years. The liquidity ratios are below one. I believe businesses should avoid such low liquidity, particularly asset-heavy enterprises as Cemex. I will follow up later with Cemex to see if the company improves its finances. However, I give a hold rating for now due to a disappointing balance sheet.

For further details see:

Cemex: Great Potential But Poor Finances