CX - Cemex: Impressive Financial Execution Balancing Macro Uncertainties

2023-08-20 09:12:11 ET

Summary

- Cemex reported Q2 earnings highlighted by firming margins.

- The company has found success raising prices, helping to balance softer cement volumes globally.

- We are bullish on CX stock and expect the rally to continue.

Cemex, S.A.B. de C.V. ( CX ) has been a big winner with a combination of strong financial trends into the resilient global economy helping shares nearly double in value over the past year. The Mexico-based multinational cement giant just reported its latest quarterly result highlighted by firming margins and climbing profitability, continuing a trend of what has been a multi-year turnaround for the company.

We last covered the CX back in 2022 with a bullish article , while it's fair to say that the stock's performance over the period has surpassed our expectations. Even as the current setup considers a new round of macro uncertainties and potential growth headwinds, we believe Cemex's strategy execution with overall solid fundamentals supports even more upside in the stock.

{kind=link}

CX Earnings Recap

Cemex reported Q2 GAAP EPADS of $0.18 with revenue of $4.5B, up 13.4% year over year, coming in $160 million above the consensus estimate. The story here is that even as consolidated volumes are down compared to Q2 2022, higher pricing initiatives are adding to the top and bottom lines.

Indeed, the gross margin reached 34.6%, up 330 basis points compared to the period last year while operating EBITDA of $961 million increased by 34%, setting a quarterly record for the company. The EBITDA margin at 21.1% is an impressive improvement compared to a cycle low of 16.4% in Q4 2022 defined at the time by high inflationary cost pressures and weak capacity utilization.

source: company IR

A theme this quarter was that even as the pace of business globally is down compared to the exceptional post-pandemic construction boom in 2021, there were some bright spots.

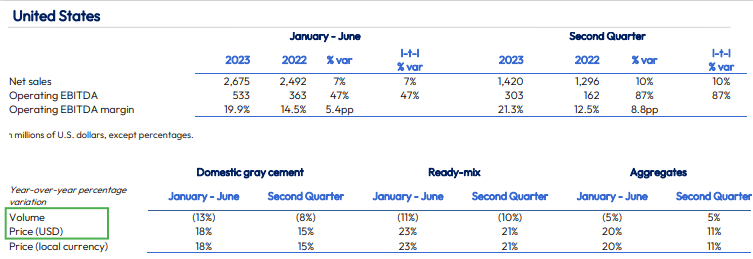

In Mexico, for example, volumes are up for the first time in two years driven by some key major infrastructure projects. The strengthening of the Mexican Peso this year has also added to the results. Sales in the U.S. have rebounded, climbing by 10% y/y while EBITDA nearly doubled, again driven by average higher pricing.

{kind=link}

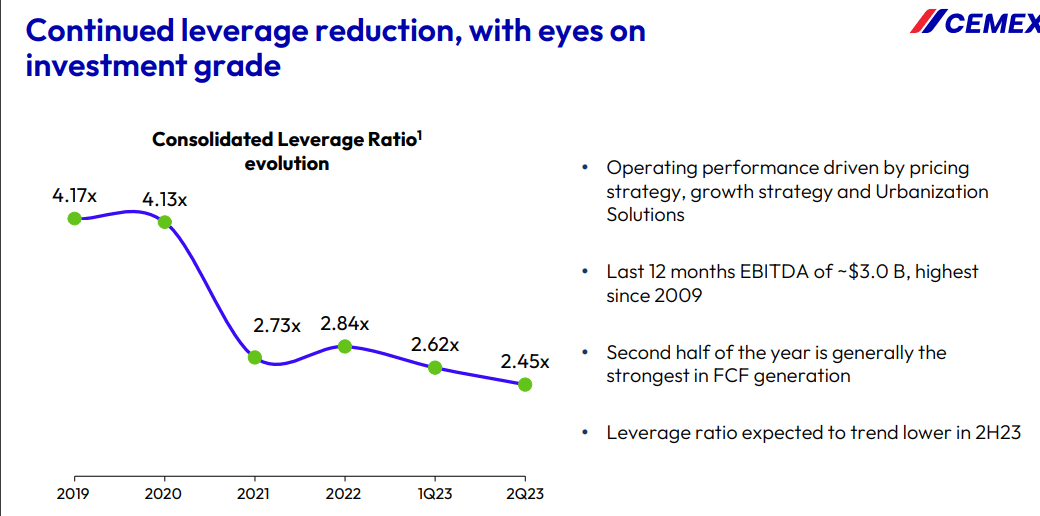

Maybe the most impressive development for Cemex, in our opinion, has been its ongoing debt reduction . Cemex ended the quarter with a net debt to EBITDA ratio of 2.45x, down from 2.62x in Q1 and levels above 4x in 2020. Management expects further deleveraging going forward backed by recurring free cash flow.

{kind=link}

What's Next for Cemex?

While economic conditions this year have thus far averted fears of a potential recession, recent headlines and otherwise mixed indicators continue to represent a layer of uncertainty. Naturally, a broader macro slowdown would undermine the operating environment for Cemex although our take is that such a scenario is far from certain.

Management is projecting confidence that the recent financial trends will continue. In the near term, the understanding is that the second half of the year is historically stronger for the business, capturing some positive cash flow seasonality.

The expectation is that further price increases in several markets add to the financial momentum. Management is hiking its EBITDA guidance to $3.3 billion, up 22% from 2022, compared to an estimate in the "low single digits" announced in Q1. From the earnings conference call :

Based on first half results, I'm quite optimistic for the rest of the year. We have additional pricing increases scale into rollout in several markets during the third quarter. We expect to see continued deceleration in key input costs, while the benefit from our growth investment portfolio should continue to scale. As a result, we are upgrading our EBITDA guidance to be in the $3.25 billion area, an approximate 21% increase year-over-year.

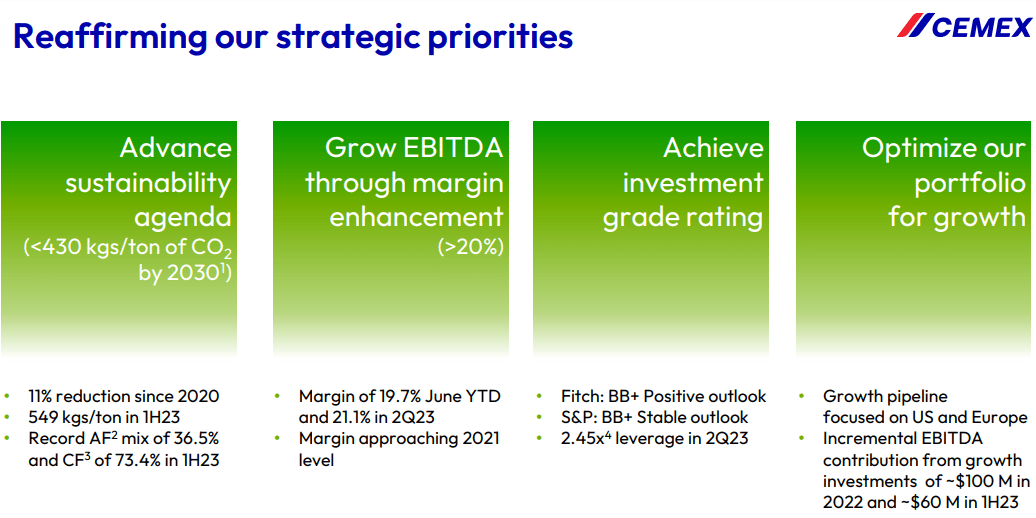

Looking ahead, Cemex's strategy centers on refining its operation to maximize efficiencies. A new facility under development in Israel is expected to add capacity in the region while also advancing the company's sustainability agenda by utilizing clean fuels and more advanced technologies to limit carbon emissions.

Beyond the push toward higher margins, management remains committed to achieving an investment-grade rating in terms of its corporate bonds. "Fitch" last rated Cemex as (BB+) with a positive outlook and we wouldn't be surprised to see an upgrade over the next year. The result should translate into a lower cost of capital as a positive on the equity side within the stock's investment profile.

{kind=link}

CX Stock Price Forecast

From the stock price chart, we notice that even with the strong rally over the past year, CX remains within a long-running down channel with a series of lower highs going back to 2014. That being said, if we consider that fundamentals and the company's outlook is stronger today than at any time over the past three to five years, there's a strong case to be made that shares have more upside.

{kind=link}

The call we make is to expect some consolidation of recent gains around the current level near $8.00 per share which can set up the next leg higher. The bullish case here is that global growth can once again find a resurgence which should lead to improved cement demand and ultimately stronger-than-expected sales and earnings growth for Cemex as a catalyst for the stock.

In terms of valuation, we note that CX is currently trading at an EV to forward EBITDA multiple of 3.5x which is below its five and seven-year average for the multiple closer to 7.5x. By this measure, we believe shares are undervalued and have room to reprice higher particularly as earnings accelerated as volumes rebound.

Final Thoughts

What we like about Cemex is that it checks off several boxes of what makes a quality stock in our opinion. This is a segment leader generating top-line growth with firming profitability alongside a strengthening balance sheet which all support a positive long-term outlook.

On the other hand, the risk here is that renewed global turbulence spoils the party. Softer-than-expected results in the upcoming quarters would open the door for a leg lower in the stock. Monitoring points here include economic indicators like industrial activity in major economies while an appreciation of the U.S. Dollar could represent a headwind for financial results.

For further details see:

Cemex: Impressive Financial Execution Balancing Macro Uncertainties