CEN - CEN: Reasonable CEF But The Private Position Could Be A Problem

2023-03-08 11:55:30 ET

Summary

- Master limited partnerships are among the best holdings for income-focused investors due to their inherent stability and high yields.

- Center Coast Brookfield MLP & Energy Infrastructure Fund invests in a portfolio of these companies in an effort to deliver a high total return and a high yield to its investors.

- The CEN closed-end fund has substantial exposure to a private entity that appears to be dragging on the portfolio's performance.

- The fund was able to easily cover its distributions over the past year, but the yield is much lower than it should be.

- The CEN CEF has a reasonably attractive valuation.

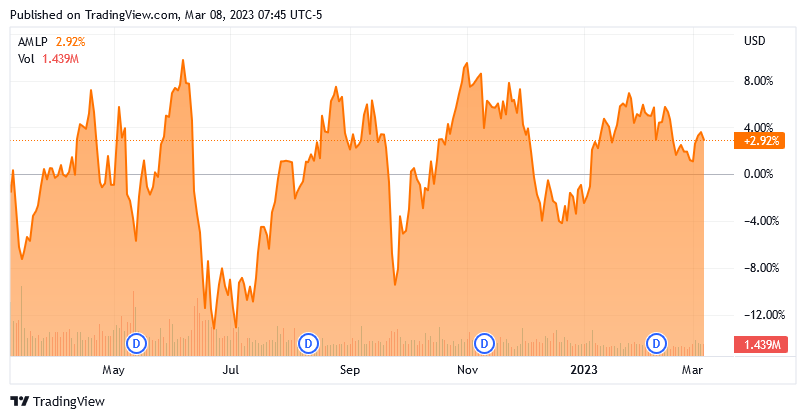

For many years now, one of the most popular investments among those that are seeking income has been midstream master limited partnerships. This makes sense since these companies are specifically structured to result in fairly large yields. After all, the distributions are subject to special tax treatment and they have relatively slow growth rates, so they typically have a low unit price compared to the distribution. That results in a high yield, which we can immediately see in the fact that the Alerian MLP Index (AMLP) currently yields 7.79% despite being one of the only indices that went up over the past twelve months:

{kind=link}

One of the big problems with these companies, though, is that it can be difficult to include them in a tax-advantaged account, such as most retirement accounts. The reason for this is their tax-advantaged nature, which results in some rather complicated tax rules. Fortunately, there is a way around that, which will also result in any investor obtaining a diversified portfolio of these companies. This solution is to purchase shares of a closed-end fund, or CEF, that specializes in investing in master limited partnerships. These funds are usually structured as corporations, which eliminates any problems that may arise regarding their inclusion in a tax-advantaged account.

In this article, we will discuss the Center Coast Brookfield MLP & Energy Infrastructure Fund ( CEN ). This fund yields 5.01% at present, which is better than many other things in the market, but it is not likely to impress anyone interested in master limited partnerships. After all, it is a lower yield than the index possesses and it is also a lot lower than most other closed-end funds. However, this alone does not disqualify it from investment since strong forward capital appreciation or a distribution increase could still give us an acceptable return, assuming the fund is capable of delivering these things. Therefore, we need to investigate its fitness. I have discussed this fund before, but a few months have passed since that time, so obviously a few things have changed. This article will thus specifically focus on those changes as well as provide an updated analysis of the fund's finances.

About The Fund

According to the fund's webpage , the Center Coast Brookfield MLP and Energy Infrastructure Fund has the stated objective of providing its investors with a high level of total return. This is hardly surprising considering that the fund is 99.49% invested in common equity:

CEF Connect

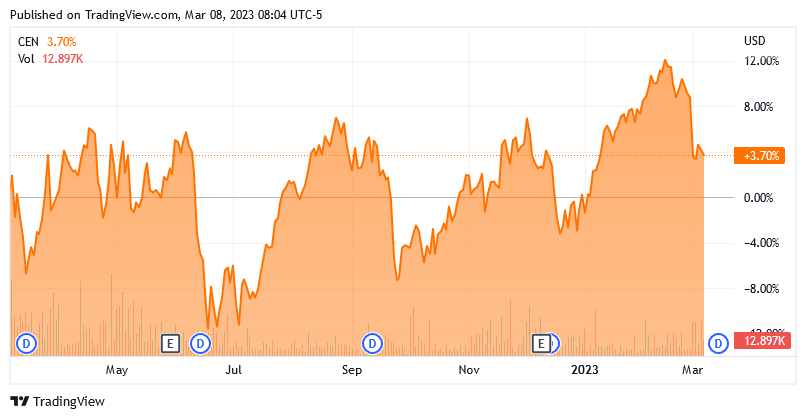

This is because common equity is by its nature a total return instrument. After all, people purchase common equity to benefit from its capital gains as well as receive an income from dividend and distribution payments. With that said, this fund does specifically state that it aims to deliver its total return primarily in the form of direct payments to its own investors. This implies that the fund will aim to keep its own net asset value and share price relatively flat over time, while it pays out its capital gains and income in the form of distributions. It was certainly successful at doing this over the past year, as the fund's share price is only up 3.70%:

{kind=link}

This may reduce the fund's appeal in the eyes of those investors that want to see the securities in their portfolios appreciate. However, there are two things to keep in mind here. First, this is the strategy used by most closed-end funds. It is quite common for these funds to simply pay out all of their gains and income to the investors as opposed to keeping them for reinvestment purposes. After all, there is nothing stopping you from simply reinvesting the distributions yourself if capital appreciation is your goal. Second, the fund can pass through the preferential tax treatment of the master limited partnerships so you will not really be exposed to the taxation that you would be normally from capital gains and dividends.

The fund specifically states that it aims to achieve its objective by investing in master limited partnerships and other energy infrastructure companies. Curiously though, it does not define an energy infrastructure company. If it is like other energy infrastructure funds, this definition would include midstream corporations like Kinder Morgan, Inc. ( KMI ) as well as electric and natural gas utilities. However, we rarely see utilities structured as master limited partnerships. In fact, the only ones that I can think of are yieldcos like NextEra Energy Partners ( NEP ) and Brookfield Renewable Partners ( BEP ). However, the fund currently does not include any utilities. In fact, the portfolio consists almost entirely of midstream companies:

Brookfield

As we can see, nearly all of the portfolio consists of gathering & processing companies and pipeline transportation firms. These are midstream companies, and they all use a similar business model. In short, these companies enter long-term (typically five- to fifteen-year) contracts under which the midstream company transports resources for the customer and the customer compensates it based on the volume of resources transported, not their value. This is something that should prove quite nice for income-focused investors because it provides a great deal of insulation against fluctuations in resource prices. This is why most of these companies are able to enjoy very stable cash flows no matter what energy prices are.

The liquefaction companies here are interesting, but they are also firms that we typically see in energy infrastructure funds. This specifically refers to companies that operate natural gas liquefaction facilities, such as Cheniere Energy ( LNG ). They also tend to operate under long-term contracts that provide a great deal of cash flow stability regardless of market conditions.

Thus, the fund consists almost entirely of companies that should have only limited exposure to any decline in energy prices. That is something that may become important in the near future as the Federal Reserve appears to be determined to push the economy into a recession, although it claims that it will only be a mild recession. One of the characteristics of a recession is that the demand for crude oil declines, which typically causes its price to decline. As I pointed out back in January though, it is unlikely that oil prices will decline much below the mid-$70s per barrel due to a few factors. The market does sometimes tend to overshoot to the downside, however. The fact that the companies in the fund should not see their cash flows impacted by such an event is something that we should appreciate, however, they probably would see their market prices decline.

As my long-time readers are no doubt well aware, I have devoted a considerable amount of time and effort over the past several years to discussing midstream and other energy infrastructure companies on this site and around the Internet. As such, most of you are likely familiar with the companies that comprise the largest positions in the fund. Here they are:

CEF Connect

I have published multiple articles on every company on this list in the past, with the notable exceptions of Western Midstream Partners ( WES ) and KKR Eagle Co-Invest. The fact that I have never discussed KKR Eagle is unsurprising, though, as this is a private company that cannot be purchased on the stock market. The fund's 2022 annual report describes this entity:

"As of September 30, 2022, the Fund's largest investment, KKR Eagle Co-Invest LP, does not permit redemptions and invests solely in Pembina Gas Infrastructure, Inc., a new joint venture entity, created by combining Veresen Midstream LP and other natural gas processing assets (the "Private Investment"), represents 33.47% of the Fund's Managed Assets. The Fund invests in the partnership through a holding company. Changes in the capital structure of the holding company may impact the equity value attributable to the Fund's interest. Accordingly, the Fund's market price and NAV will be materially impacted by the value of the Private Investment, which in turn will be affected by the business, management, results of operations, and financial condition of Pembina Gas Infrastructure, Inc."

As this is a private company, it is quite difficult to value as it does not trade on any market nor can it be easily sold by the fund. As this accounts for a sizable proportion of the fund's assets, it makes it very difficult to value the fund itself. It also makes it difficult for the fund to get out of this position should it start to perform poorly, as it did in 2022. The fund's annual report specifically states that this position lagged the benchmark index during the year, although it did deliver a positive total return. Thus, the fund would have been able to perform better than it did last year if it could have easily disposed of this position and invested the money in the public market. Brookfield has stated that it is in the process of working on potentially selling this asset to free up capital so this could be something to watch going forward.

There was only one significant change in the fund's largest positions over the past few months, which was the exchange of Plains All American Pipeline ( PAA ) for Magellan Midstream Partners ( MMP ). I cannot say that this was a bad change as Magellan Midstream Partners did hold up somewhat better than Plains All American Pipeline did during the challenging conditions back in 2020, but I can think of a few companies that would be better than either of them for that spot.

Regardless, Magellan Midstream Partners is one of the largest and most well-financed master limited partnerships in the United States and it is one of the only ones that has a core focus on refined products, so its presence enhances the fund's diversity. The fact that so few positions have changed in the past three months could be a sign that the fund has a fairly low annual turnover. This is actually the case as the Center Coast Brookfield MLP and Energy Infrastructure Fund had an annual turnover of 40.00% in 2022, which is below the midpoint for a closed-end fund. This is nice because it costs money to trade partnership units, stocks, and other assets. These costs are billed directly to the shareholders and create a drag on the fund's performance. That, of course, makes management's job more difficult because it will need to deliver sufficient returns to cover these added expenses and still have enough left over to deliver an acceptable return to the investors.

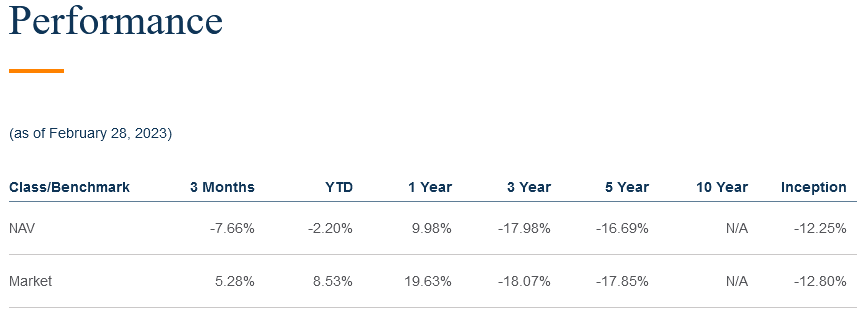

There are few management teams that consistently accomplish this over time. As we have already seen though, this fund did deliver better performance in the market than the MLP index did, although it actually underperformed it when we consider the fact that the index has a higher yield. However, the performance difference is actually starker since the fund's shares in the market actually substantially outperformed the portfolio in the past year. This can be seen here:

{kind=link}

As shown, the fund's net asset value significantly underperformed the fund's actual market return. This is something that occasionally happens with closed-end funds, and it could be a sign that the fund has become overvalued. We will discuss that in just a bit.

Leverage

Closed-end funds like the Center Coast Brookfield MLP and Energy Infrastructure Fund have the ability to use certain strategies that boost their yields beyond that of any of the underlying assets. This is something that could be rather attractive for investors in a midstream fund because most of the underlying assets tend to have remarkably high yields. One way that these funds achieve this is by borrowing money and then using those borrowed funds to purchase units of master limited partnerships. As long as the purchased assets have a higher yield than the interest rate that the fund must pay on the borrowed money, the strategy works quite well to boost the effective yield of the portfolio.

However, the use of leverage is a double-edged sword because leverage boosts both gains and losses. As such, it is important to ensure that the fund is not using too much leverage because that will expose us to too much risk. I usually like to see the fund's leverage under a third as a percentage of its assets for this reason. The Center Coast Brookfield MLP and Energy Infrastructure Fund appears to satisfy this requirement as its levered assets currently comprise 17% of its portfolio. This fund appears to be striking a reasonable balance between risk and reward.

Distribution Analysis

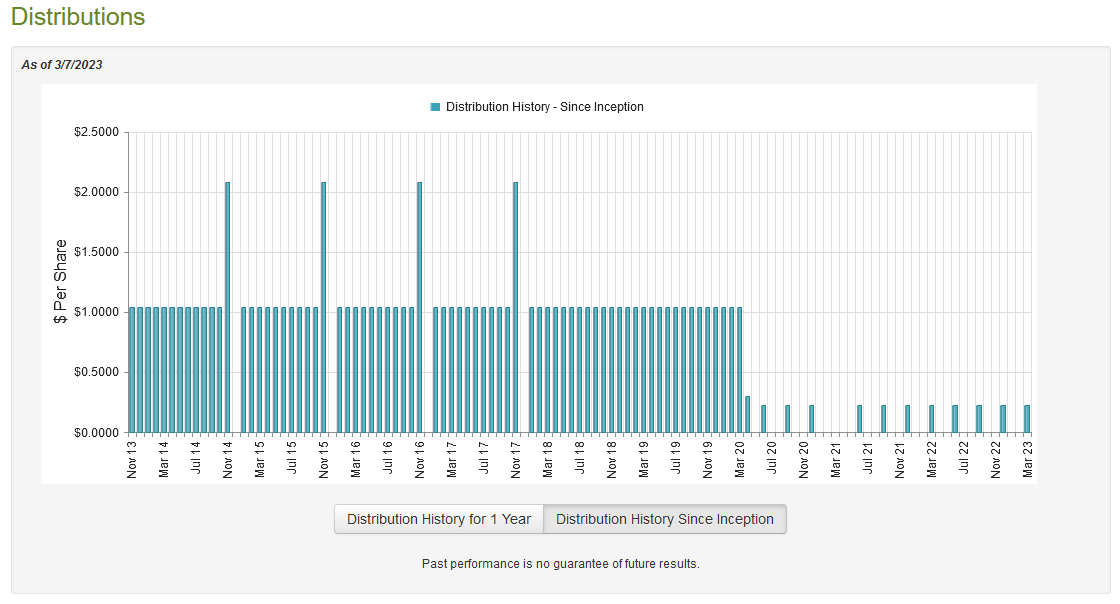

As mentioned earlier in this article, one of the primary reasons why investors purchase units of master limited partnerships is the incredibly high yields that these companies tend to possess. The Center Coast Brookfield MLP and Energy Infrastructure Fund invests in a portfolio of these entities and then applies leverage in order to boost its effective portfolio yield. Surprisingly though, the fund itself does not have an especially high yield. The fund pays a quarterly distribution of $0.2250 per share ($0.90 per share annually), which gives it a 5.01% yield at the current price. While this is better than the 1.59% current yield of the S&P 500 ( SPY ), it is not particularly impressive for anything in the midstream sector. The fund's distribution history is also not particularly impressive as it cut its payout severely back in 2020 and has yet to implement any increase:

{kind=link}

This is in stark contrast to many other midstream funds, which have been increasing their distributions over the past two years as the industry has recovered from the challenging conditions that accompanied the pandemic-related lockdowns. The fund's distribution history prior to those events was certainly attractive though and for quite some time, it had a double-digit yield. However, the fund's past is not the most important thing for anyone purchasing today. This is because anyone buying today will receive the current distribution at the current yield. As such, the most important thing is the fund's ability to maintain its current payout.

Fortunately, we have a very recent document that we can consult for that. The fund's most recent financial document is its 2022 annual report, which was linked earlier in this article. This document corresponds to the full-year period that ended on September 30, 2022. As such, we should be able to get a pretty good idea of how well the fund performed throughout most of 2022, although the energy sector did deliver a much weaker performance in the second half of the year and that will not be fully reflected here. During the full-year period, the fund received a total of $10,952,181 in dividends and distributions along with $22,532 in interest from the investments in its portfolio. Some of these distributions were from master limited partnerships and so are considered a return of capital instead of income, so the fund had a total reportable income of $7,930,088 over the course of the year. It paid its expenses out of this amount, which left it with $5,674,682 available for shareholders. This was sufficient to cover the $4,436,951 that the fund actually paid out in distributions.

This puts us in a situation where the fund substantially underpaid its distribution. During the full-year period, it achieved net realized gains of $5,869,944, although this was partially offset by $679,328 in net unrealized losses. The net unrealized losses is quite confusing since pretty much every other energy infrastructure closed-end fund reported massive realized and unrealized capital gains over the same period. This is probably due to the large allocation to the KKR Eagle Co-Invest private placement in the portfolio. The fund's assets still increased by $6,428,347 during the period even after paying out the distribution though, so this is a clear sign that it may have under-distributed.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a closed-end fund like the Center Coast Brookfield MLP and Energy Infrastructure Fund, the usual way to value it is by looking at the fund's net asset value. The net asset value of a fund is the total current market value of all the fund's assets minus any outstanding debt. This is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can acquire them at a price that is less than the net asset value. This is because such a scenario implies that we are buying the fund's assets for less than they are actually worth. This is, fortunately, the case with this fund today. As of March 7, 2023 (the most recent date for which data is currently available), the Center Coast Brookfield MLP and Energy Infrastructure Fund reported a net asset value of $20.73 per share but the shares currently trade for $17.87 per share. This gives the fund's shares a discount of 13.80% at the current price. That is much better than the 8.06% discount that the shares have traded at on average over the past month, so the price does appear reasonable today.

Conclusion

In conclusion, I want to like the Center Coast Brookfield MLP and Energy Infrastructure Fund as it does tick most of the right boxes. The fund's distribution is easily sustainable based on its net investment income, and it trades at a reasonable discount to the net asset value. In addition, the portfolio looks decent as it mostly consists of the best companies in the sector. However, the fund's yield is very low compared to comparable funds and its performance leaves a bit to be desired.

In particular, Center Coast Brookfield MLP & Energy Infrastructure Fund delivered net unrealized losses during a time when every other similar fund saw substantial gains. A reading of the fund's annual report makes me believe that this is due to that large private holding, which the fund has stated it may sell off. If that occurs, Center Coast Brookfield MLP & Energy Infrastructure Fund will definitely become a solid position, but until that time, I am indifferent to it.

For further details see:

CEN: Reasonable CEF, But The Private Position Could Be A Problem