CEN - CEN: Some Uncertainty About Upcoming Merger And Disappointing Yield

2023-07-24 12:15:09 ET

Summary

- The midstream sector has been a popular way to earn income from a portfolio for many years.

- Center Coast Brookfield MLP & NRG Inf Fd invests in a portfolio of midstream corporations and partnerships in an attempt to provide a high total return to its investors.

- The CEN closed-end fund might soon be merged into one of Brookfield's other funds and is probably best avoided until that is resolved.

- The fund has a very low yield for a midstream company, but its distribution is fully covered, and the fund probably could increase it.

- The fund is currently trading at a smaller discount to intrinsic value than normal.

For many years now, midstream corporations and master limited partnerships, or MLPs, have been among the favorite investments for anyone seeking to earn a high level of income from their portfolios. This is unsurprising, as these companies are ideal for income-seeking investors. For example, their business models result in midstream companies having remarkably stable cash flows through any economic environment. They also pay out a substantial percentage of their cash flows to the investors because they tend to be capital-intensive businesses with low growth compared to other sectors. In the case of midstream master limited partnerships, their distributions also receive some tax benefits, which are invaluable to those in a high tax bracket.

Unfortunately, the fact that midstream partnerships come with tax benefits causes a problem for anyone that wants to include them in a retirement account. In particular, these companies can actually expose your individual retirement account to tax liability. Midstream corporations do not have this problem and can be included in a retirement account just like any other security. In addition to potential tax problems, it can be difficult to put together a diversified portfolio of midstream companies without having access to a considerable amount of capital. That is hardly a problem unique to this sector, though.

Fortunately, there is a way around both of these problems. This is to purchase shares of a closed-end fund, or CEF, that specializes in midstream investments. These funds are normally structured as corporations, which eliminates all of the potential tax problems of including a master limited partnership in a tax-advantaged retirement account. In addition, these funds basically consist of a diversified portfolio of midstream and other energy infrastructure companies, making it easy to acquire a professionally-managed portfolio simply by purchasing the fund itself. In addition to this, these funds are able to use certain strategies that allow them to boost their effective yields well beyond that of the underlying assets. When we consider that the Alerian MLP Index ( AMLP ) yields 8.40% as of the time of writing, this is something that can be very appealing to anyone seeking a very high level of income.

In this article, we will discuss the Center Coast Brookfield MLP & NRG Inf Fd ( CEN ), which currently yields 4.42%. This is admittedly a very disappointing yield, and many of the other funds in the sector yield substantially more. However, many infrastructure investors have a great deal of respect for the Brookfield name, and indeed this fund is managed by Brookfield's Public Securities Group, so we are getting the benefit of that company's research and expertise with this fund. I have discussed this fund before, but a few months have passed since that time so naturally several things have changed. This article will focus specifically on these changes as well as provide an updated analysis of the fund's financial condition.

About The Fund

According to the fund's webpage , the Center Coast Brookfield MLP & Energy Infrastructure Fund has the objective of providing its investors with a high level of total return. This is not surprising considering that this is an equity closed-end fund. As we can see here, the fund's portfolio consists entirely of equity, along with a fairly small cash position:

Morningstar

The reason that the fund's objective is not surprising is that equity is by its very nature a total return vehicle. After all, investors purchase common equity in order to receive capital gains as the issuing company grows and prospers over time. In addition, investors want to receive a cut of the company's profits in the form of dividends and distributions, which function as a source of income. The fund aims to deliver both of these things, although it has an emphasis on providing its total return in the form of distributions. The fund's fact sheet describes the fund's objective and strategy as follows:

Center Coast Brookfield & Energy Infrastructure Fund's investment objective is to provide a high level of total return with an emphasis on distributions to shareholders. The "total return" sought by the fund includes appreciation in the net asset value of the fund's common shares and all distributions made by the fund to its common shareholders, regardless of the tax characterization of such distributions, including distributions characterized as return of capital.

Energy infrastructure funds such as this one tend to have substantial return of capital distributions. This comes from the simple fact that the distributions of master limited partnerships are considered a return of capital that reduces the cost basis of the partnership units. It is not until the cost basis reaches zero that the distributions become classified as capital gains for tax purposes. The fund will pass money collected in this way through to its shareholders as a return of capital. This could make the fund a rather attractive position for someone in a high tax bracket, just like master limited partnerships.

As my long-time readers are no doubt well aware, I have devoted a considerable amount of time and effort over the years to discussing midstream partnerships and corporations here at Energy Profits in Dividends as well as on Seeking Alpha. As such, the largest positions in the fund are certain to be familiar to most regular readers. Here they are:

Brookfield Oaktree

Unlike most other closed-end funds, the Center Coast Brookfield only provides its five largest holdings on the webpage. This is probably because this fund only has 21 total positions and the five largest alone account for 47.1% of the fund's total portfolio. This is therefore a highly concentrated portfolio, but that is not unusual for a midstream fund. The Alerian MLP Index itself only has sixteen positions due to the simple fact that there are not a very large number of midstream companies. After all, unless you live in Texas, you do not see natural gas and crude oil pipelines everywhere. Due to the capital-intensive nature of the business, there has also been a substantial amount of industry consolidation over the years. This has resulted in there only being a handful of companies in the midstream sector and not all of them are great investments. Thus, almost any midstream fund will have highly concentrated positions to only a small number of companies.

As my regular readers on the topic of closed-end funds are likely well aware, I do not like to see any individual position in a fund account for more than 5% of the fund's total assets. This is because that is approximately the point at which the asset begins to expose the fund to idiosyncratic risk. Idiosyncratic, or company-specific, risk is that risk that any asset possesses that is independent of the market as a whole. This is the risk that we aim to eliminate through diversification, but if the asset accounts for too much of the fund then this risk will not be completely diversified away. Thus, the concern is that some event may occur that causes the price of a specified asset to decline when the market as a whole does not. If that asset accounts for too much of the portfolio, then it may end up dragging the entire fund down with it in such an event. As we can clearly see, there are several companies here that each account for significantly more than 5% of the fund's portfolio. As such, investors in the fund should ensure that they are willing to be exposed to the risks of these companies individually before taking a position in this fund. With that said, the five companies that comprise the largest positions are five of the six or seven best companies in this sector right now so pretty much anyone that wants midstream exposure will want to be exposed to these firms. As such, I am not really as concerned about the concentration here as I would be with a broad-market fund.

All five of the companies listed above were among the fund's ten largest positions the last time that we discussed it. The fund has substantially decreased its exposure to Cheniere Energy ( LNG ) since the last time that we discussed it. By far the biggest change here though is that the fund divested its enormous stake in KKR Eagle Co-Invest, which was a private company that previously accounted for the largest position in the fund. The company discussed the sale of this position in a press release that announced a proposal to reorganize the fund. From the press release:

As stated in a press release issued on August 1, 2022, PSG, in collaboration with the Board, has evaluated various strategic options for CEN seeking to advance and maximize shareholder value, including, without limitation, reorganization opportunities with third parties, and strategic portfolio repositioning, including a potential sale of all or part of CEN's holding in KKR Eagle Co-Invest LP ("KKR Eagle"). Following an extensive process with a strategic advisor regarding potential sale opportunities for KKR Eagle, PSG has signed a purchase and sale agreement to sell CEN's interests in KKR Eagle. The sale of CEN's interests in KKR Eagle is expected to close tomorrow, March 31, 2023.

This is nice from an analyst's perspective as it is much easier to analyze the performance of the public companies in the fund's portfolio than it is a private company. After all, public companies make their financial information easily accessible and we can see at a glance how a public security performs in terms of price. In addition, KKR Eagle has proven to be something of a negative influence on the fund's performance over time so disposing of it has secondary benefits as it should allow the fund to improve its performance.

Proposed Merger

One major wildcard with this fund is a proposed merger with the Center Coast Brookfield Midstream Focus Fund, which is an open-ended fund. I will admit that I am not particularly in favor of this merger. The open-ended fund does not have the same flexibility to use leverage, for example. It is nice for investors to have the ability to choose between the options of purchasing a levered closed-end fund or an ordinary midstream open-ended mutual fund. The closed-end fund also has the ability to purchase stakes in private corporations, but the open-ended fund does not, which can be advantageous. With that said though, the open-ended fund has managed to outperform the closed-end fund over time.

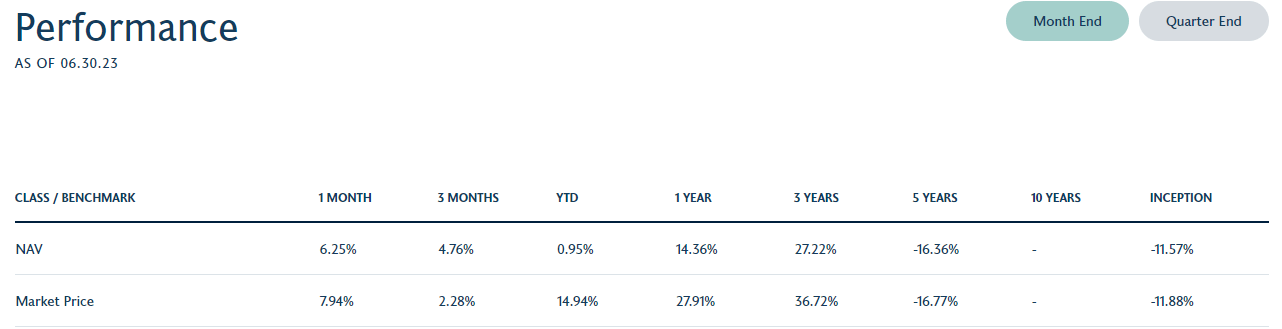

Here is the performance data for the Center Coast Brookfield MLP & Energy Infrastructure Fund:

{kind=link}

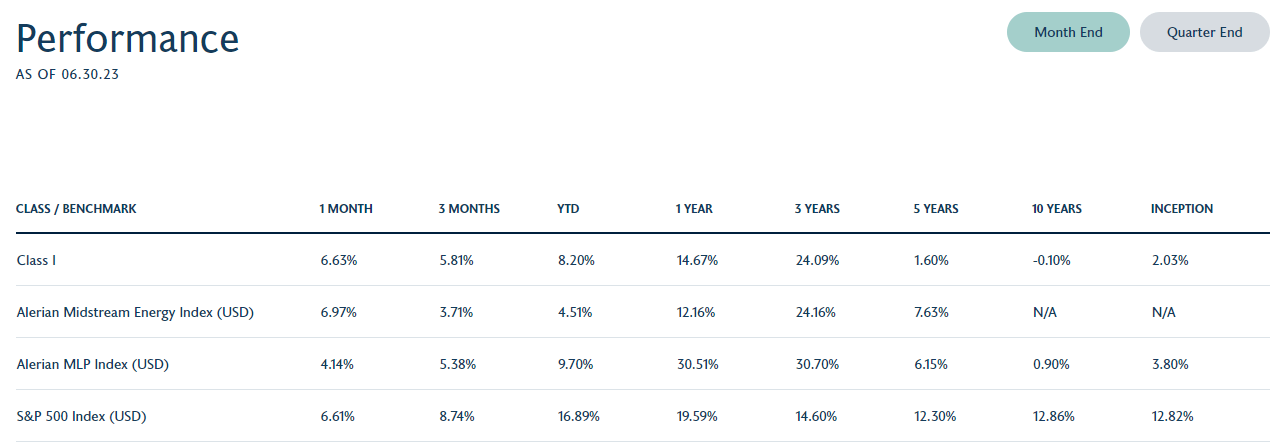

Here is the performance data for the Center Coast Brookfield Midstream Focus Fund:

{kind=link}

As we can see, the open-ended fund has usually outperformed the closed-end fund. The closed-end fund did manage to outperform both the Midstream Focus Fund and the Alerian Midstream Energy Index over the three-year period, though. This is due to the use of leverage in what was a pretty strong bull market for midstream companies. Unfortunately, both funds have substantially underperformed the two Alerian indices that cover the sector.

I am not a fan of combining the two funds mostly because it is nice for investors to have the option to use leverage when they desire it. There are other closed-end funds available that cover the midstream sector though that could be used to get the benefit of leverage during a midstream bull market and many of them have outperformed both of these funds. It therefore may not be the end of the world if this merger does get consummated.

As of right now, the two Brookfield funds remain separate. I am not a shareholder of either of them and I will not consider buying until it is known how this scenario plays out. It is my recommendation that you avoid both funds until it is known what will happen here, but if you do happen to be a shareholder you may want to vote against the merger.

Leverage

In the introduction to this article, I stated that closed-end funds like the Center Coast Brookfield MLP & Energy Infrastructure Fund have the ability to use certain strategies that let them boost total returns and yields beyond that of any of the underlying assets in the fund. One of these strategies is the use of leverage. In short, the fund borrows money and then uses that borrowed money to purchase common equity of midstream partnerships and corporations. As long as the purchased assets deliver a higher total return than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, that will normally be the case. With that said though, this strategy is much less effective today than it was a year ago due to the higher costs of the borrowed money.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. That is probably why this fund managed to outperform a very similar open-ended fund over the trailing three-year period. As such, we want to ensure that the fund is not using too much leverage because that would expose us to too much risk. I do not usually like to see a fund's leverage exceed a third as a percentage of its assets for this reason. Fortunately, this fund meets that requirement as its levered assets are 16.41% of the portfolio as of the time of writing. Thus, this fund appears to be striking a reasonable balance between risk and reward. We should not have to worry too much here.

Distribution Analysis

One of the biggest reasons that investors purchase shares of midstream corporations and master limited partnerships is the incredibly high yields that these entities typically possess. This comes from the fact that midstream companies usually have remarkably stable cash flows over time along with fairly low growth rates, so they pay out a substantial percentage of their cash flow in order to provide the investors with a reasonable rate of return. The market does not normally assign high multiples to most of these companies due to their slow growth, so the distribution ends up being a substantial percentage of the unit market price. The Center Coast Brookfield MLP & Energy Infrastructure Fund invests in a portfolio of these companies and then adds a layer of leverage to boost the effective yield of the portfolio. The fund then aims to pay out all of its received payments and investment returns to the shareholders. We might therefore expect that this fund would have a very high yield. However, that is not the case as the fund currently pays out a quarterly distribution of $0.2250 per share ($0.90 per share annually), which gives the fund a 4.42% yield at the current price. This is one of the lowest yields of any midstream closed-end fund, and this is one of the only funds that has not increased its distribution since the fund cut it back in 2020. That is very disappointing and will undoubtedly make this fund a second drawer choice for an investor that is seeking a high level of sustainable income.

As is always the case though, it is important that we investigate the fund's ability to sustain its current payout. After all, we do not want to be the victims of another distribution cut since that would almost certainly reduce our incomes and cause the fund's share price to decline. Let us investigate this in order to determine how well covered the fund's current distribution is and how well it may be able to increase the distribution in the future.

Fortunately, we do have a very recent document that we can consult for the purposes of our analysis. The fund's most recent financial report corresponds to the six-month period that ended on March 31, 2023. This is a much newer report than the one that we had available the last time that we discussed this fund, which is very nice as it will give us six more months of data. The period in question was an interesting one as energy prices generally declined but the stock market switched to a bullish stance due to investors' belief that the Federal Reserve's rate-tightening cycle may be about to come to a close. During the six-month period, the Center Coast Brookfield MLP & Energy Infrastructure Fund received $2,518,714 in dividends and distributions along with $25,121 in interest from the assets in its portfolio. However, some of this money came from master limited partnerships so it is not considered to be income for tax purposes. The fund, therefore, reported a total investment income of $1,000,274 during the period. It paid its expenses out of this amount, which left it with a negative $1,480,381 available for shareholders.

Obviously, this is not enough to pay any distributions, but the fund still paid out $2,218,476 during the period. At first glance, this might be concerning as this fund is clearly not covering its distributions out of net investment income.

However, a fund like this has other methods that can be employed in order to obtain the money that it needs to cover the distributions. As already mentioned, the fund receives a significant amount of money from the master limited partnerships in its portfolio that can be distributed but is not considered to be income for tax purposes. The fund might also have capital gains that can be paid out. It was, fortunately, quite successful at this task during the period. Over the six-month period, the fund had net realized gains of $1,558,724 and had another $6,654,312 in net unrealized gains. Overall, the fund's net assets went up by $4,514,179 after accounting for all inflows and outflows in the period.

Thus, the fund not only covered all of its distributions but theoretically could have paid out more than it did. The current distribution is probably safe as long as a market decline does not wipe out the gains that the fund managed to get over the period.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a closed-end fund like the Center Coast Brookfield MLP & NRG Inf Fd, the usual way to value it is by looking at the fund's net asset value. The net asset value of a fund is the total current market value of all the fund's assets minus any outstanding debt. This is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can obtain them at a price that is less than the net asset value. This is because such a scenario implies that we are acquiring the fund's assets for less than they are actually worth. This is, fortunately, the case with this fund today. As of July 20, 2023 (the most recent date for which data is currently available), the fund had a net asset value of $21.21 per share but the shares currently trade for $20.35 each. This gives the fund's shares a 4.05% discount to the net asset value at the current price. This is not as good as the 5.85% discount that the shares traded at on average over the past month. Thus, it might make some sense to wait until the fund declines a bit before buying its shares.

Conclusion

In conclusion, the Center Coast Brookfield MLP & Energy Infrastructure Fund is one way for income-focused investors to use their retirement accounts to invest in the high-yielding midstream sector. Unfortunately, the fund itself does not pass those high yields through to its shareholders as its own yield is quite a bit lower than most companies in the sector and much lower than other closed-end funds that cover the sector. The fund also might not exist much longer depending on whether or not the shareholders approve the merger. The distribution is sustainable, though, and is unlikely to be cut if the merger does fail. The fund's shares also trade at an acceptable price right now.

For further details see:

CEN: Some Uncertainty About Upcoming Merger And Disappointing Yield