IMO - Cenovus: What To Expect From Oil Sands Producer's Q4

Summary

- Cenovus is scheduled to release its Q4 and full-year 2022 results on Thursday. Expect a meaningful reduction in the company's year-over-year debt load.

- That's because, as of Q3, debt had already dropped from C$12.4 billion at year-end 2022 to C$8.8 billion (-29%). I expect further progress was made in Q4.

- While Cenovus has struggled with its Toledo and Lima refineries, the WRB JV with Phillips 66 had a very strong Q4.

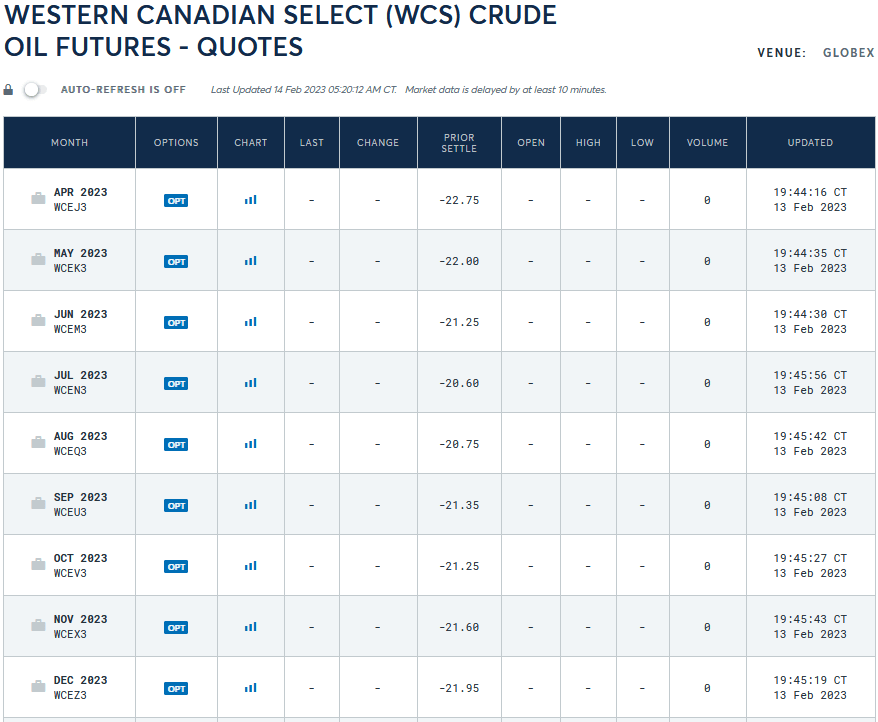

- Going forward, the CME crude oil futures shows the WCS discount to WTI is solidly over $20/bbl for the remainder of 2023.

In my last Seeking Alpha article on Cenovus ( CVE ), I reported that the TransMountain Pipeline expansion project will likely be a bullish development for the company. However, that project - which will increase the pipeline's capacity by 300,000 bpd to 890,000 bpd - is not expected to be completed until the back half of this year. Today I will take a look at what to expect when CVE reports its Q4 results on Thursday and for the rest of FY23. One thing is certain: The large debt load that has been hanging over Cenovus like a black cloud since the big oil sands deal with ConocoPhillips ( COP ) back in 2017 has been significantly reduced. Indeed, the company previously reported its intention to reduce debt by ~$4 billion by year-end 2022. We'll find out Thursday if that goal was reached. Regardless of the exact amount, the significant reduction in Cenovus' debt is good news shareholders because lower debt-servicing costs means more cash flow is left over for increased shareholder returns.

WCS

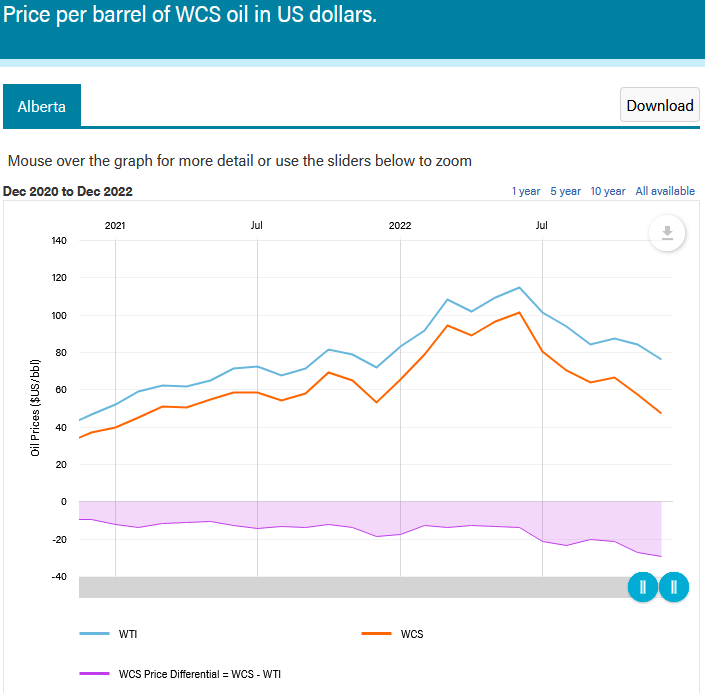

As usual, CVE's results will be significantly impacted by the price it was able to realize for its Canadian Oil Sands production - which is typically represented by the price of WCS, or Western Canadian Select. Oil prices in general weakened in Q4 as compared to Q3:

{kind=link}

Economicdashboard.Alberta.ca

More importantly, and as you can see from the right-hand side of the graphic above, the WCS discount to WTI blew-out once again in December. This time it was because TC Energy's ( TRP ) Keystone Pipeline sprung a leak in Kansas. That forced closure of the 622,000 bpd pipeline on Dec. 7 and caused a backup in WCS supply all the way back to Edmonton. As a result, WCS ended 2022 at $47.14/bbl - a whopping $29.30/bbl discount to WTI . The Keystone pipeline returned to full service on Dec. 29 after a 21-day outage.

Going forward, the CME futures show the WCS discount to WTI remaining solidly above $20/bbl for the remainder of 2023:

{kind=link}

CME Futures

Refining

The good news is that Cenovus has been taking steps to pick up the lost margin on heavily discounted WCS crude by increasing its refining footprint. The company wholly owns two refineries in the L48 - Lima and Superior. CVE also jointly owns the ill-fated (shut-down due to a fire) Toledo Refinery with BP ( BP ), while the star of the show is arguably the Wood-River Borger (or so-called "WRB") JV with Phillips 66 ( PSX ).

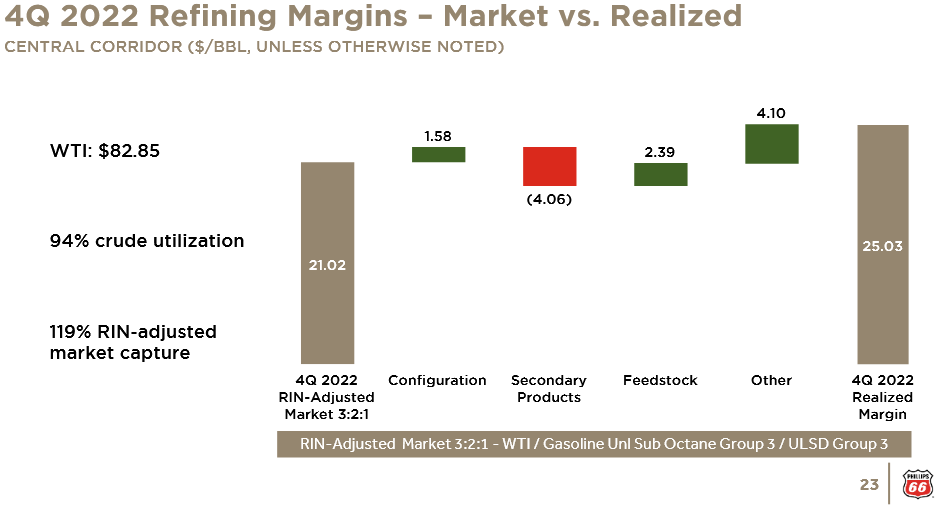

PSX reported its Q4 results on Jan. 31 and its mid-continent refineries (which are primarily WRB) had an excellent quarter:

{kind=link}

Phillips 66

As can be seen in the graphic, PSX achieved a (RIN-adjusted) market capture of 119% as compared to the 3:2:1 market crack spread (i.e. $25.03/bbl vs. $21.02/bbl) while running at a 94% capacity utilization rate. As I have been reporting on Seeking Alpha for some time now, PSX has just been killing it on diesel margin due to strong demand and relatively low global diesel refining capacity. Of course heavy Canadian oil feedstock (i.e. WCS) is perfect for refining into diesel. That's the main reason that PSX - which has a higher distillate yield as compared to its refining peers - is the largest importer of WCS.

Indeed, after earnings a massive $23.27/share in 2022, PSX's outlook for FY2023 is so bright the company recently boosted its quarterly dividend by 8% to $1.05/share. Indeed, as I have advised for many years on Seeking Alpha, the best way to play the tar sands is through the refiners - not the producers:

Q4 Earnings Estimates

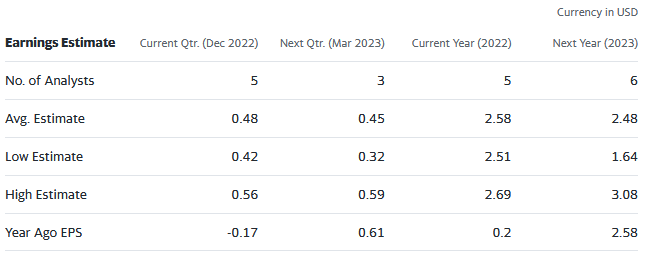

Current consensus Q4 EPS estimates for Cenovus are for US$0.48/share, which would put full-year 2022 earnings at US$2.58:

{kind=link}

Yahoo Finance

With the stock trading at US$19.89, that puts the P/E = 7.7x. And while that arguably points to a low valuation level considering peer Suncor ( SU ) trades at 8.3x, note that Cenovus' earnings are expected to drop by $0.10/share in FY2023.

The Dividend

However, things are looking up for shareholders. Instead of the big dividend cuts suffered in 2015, 2016, and 2021, with the big debt-reduction accomplish in 2022, Cenovus shareholders should see meaningful dividend increases going forward. Indeed, the June quarterly payment was $0.1050/share - which was up significantly from the piddly $0.0175/share in Q2 of 2021. In addition, CVE has instituted a variable dividend policy and paid out a US$0.1140 variable dividend in December. I would expect another significant variable dividend declaration in Q1.

Going forward, the key to CVE's dividend growth will depend on the allocation split between the dividend and share buybacks. Note that, as of Q3, Cenovus had spent $2.1 billion on buybacks. As we have seen many times over the years in the energy sector, these companies tend to dramatically increase share buybacks during up-cycles when the stock price is high, while suspending buybacks during down-cycles when the stock price is low and actually a much better value. Don't be surprised if Cenovus follows its L-48 peers like ConocoPhillips ( COP ), Exxon ( XOM ), and Chevron ( CVX ), and begins to significantly over-emphasize share buybacks over the dividend. In addition, and as we have also seen many times in the past, don't be surprised if Cenovus ends up reissuing the majority of those bought-back shares onto the market in order to fund a significant acquisition. As I have pointed out in my many articles on Seeking Alpha, those massive share buybacks are effectively forcing shareholders to double-down on oil just as the transition to clean-energy and EVs is quickly accelerating.

Summary and Conclusion

I maintain my Hold on Cenovus as the earnings growth outlook going forward in FY23 isn't all that exciting to me. While it should improve in 2024 due to the significantly addition to oil sands exit capacity due to the TransMountain pipeline expansion project, that bump could be short lived. I say that because, as we saw with big increase in Enbridge's ( ENB ) Line-3 expansion, that addition capacity was relatively quickly and easily filled by a handful of big oil sands producers that have been effectively bottled up for many years and who were dying to grow production.

That said, the potential for Cenovus shareholders to, finally, see some significant dividend growth is good-to-excellent. The stock currently trades with a (base dividend) yield of $0.42/$19.89, or 2.1%. Assuming FY23 variable dividends of at least as much as the base (i.e. $42 cents), the (base+variable) dividend yield would be 4.2%. That's certainly attractive. However, as I pointed out earlier, I continue to favor the higher-margin refiners over the Canadian tar sands producers. From that standpoint, note that PSX is currently trading with a P/E of only 4.65x while yielding 3.9%.

I'll end with a 10-year chart of some of the Canadian oil sands producers, including Imperial Oil ( IMO ), as compared to COP and the S&P500 as represented by the Vanguard S&P 500 ETF ( VOO ):

As can be seen in the graphic, the opportunity costs of investing in the leading Canadian oil sands producers have been hugely negative.

For further details see:

Cenovus: What To Expect From Oil Sands Producer's Q4