CELTF - Centamin: Growth At A Reasonable Price

2023-12-25 07:45:00 ET

Summary

- Centamin had a tough Q3 due to choosing to do preventative maintenance especially when combined with lapping tough comps from Q3 2022.

- However, Centamin is on track to report a better Q4 with maintenance complete, has delivered a robust new Sukari LOMP & could grow into a 700,000 ounce producer by 2027.

- In this update we'll dig into the Q3 results, recent developments, and where the stock's updated buy zone lies:

Just over four months ago, I wrote on Centamin ( CELTF ), noting that while the company has just come off a solid Q2 report, the ideal buy zone for the stock was at US$1.01 or lower instead of paying up for the stock above US$1.17. This is because we were heading into a weaker seasonal period for the sector and the company was coming up against difficult comparisons after lapping a massive quarter in Q3 2022 (~127,500 ounces produced). Since reaching this buy zone, Centamin has bounced 30% to hit new multi-month highs, helped by an impressive new LOMP at Sukari, continued reserve growth, and an outlook for a much better 2024/2025. In this update we'll dig into the Q3 results, recent developments, and where the stock's updated buy zone lies:

Sukari Mineralization - Company Website

{kind=link}

Q3 Results

Centamin released its Q3 results in October, reporting quarterly production of ~101,400 ounces, a 20% decline from the year-ago period. The significant decline in quarterly output was related to lower open-pit and underground grades, in addition to preventative maintenance completed late in the quarter after the company identified a potential issue on SAG mill 1 following a routine mill relining. However, it's important to note that the magnitude of the decline in year-over-year production was largely attributed to lapping tough year-over-year comparisons, with Q3 2022 being one of the best quarters in years with production just shy of 130,000 ounces. Plus, while the impact to production in the quarter was unfortunate, the work was fully completed to start Q4 and Centamin is still on track to deliver into its FY2023 guidance of 450,000 to 480,000 ounces of gold, albeit at the lower end with just ~321,900 ounces produced year-to-date (71.5% of low end of guidance).

Centamin - Quarterly Gold Production - Company Filings, Author's Chart

{kind=link}

Digging into the results a little closer, the company's Sukari Mine processed ~2.79 million tonnes at an average grade of 1.25 grams per tonne of gold, down from ~3.23 million tonnes at 1.37 grams per tonne of gold in the year-ago period. As noted above, the lower throughput was related to the temporary setback related to preventative maintenance. The company noted that lower open-pit grades were related to a higher conversion of waste to ore from Stage 7, leading to higher than planned low grade ore mined. Meanwhile, although underground tonnes mined were up 34% year-over-year to ~359,000 tonnes, and underground ore mined increased 16% to ~245,000 tonnes, grades were lower with (4.6 grams per tonne of gold vs. 6.2 grams per tonne of gold) with over 50% of ore being lower-grade development ore at a grade of 3.24 grams per tonne of gold.

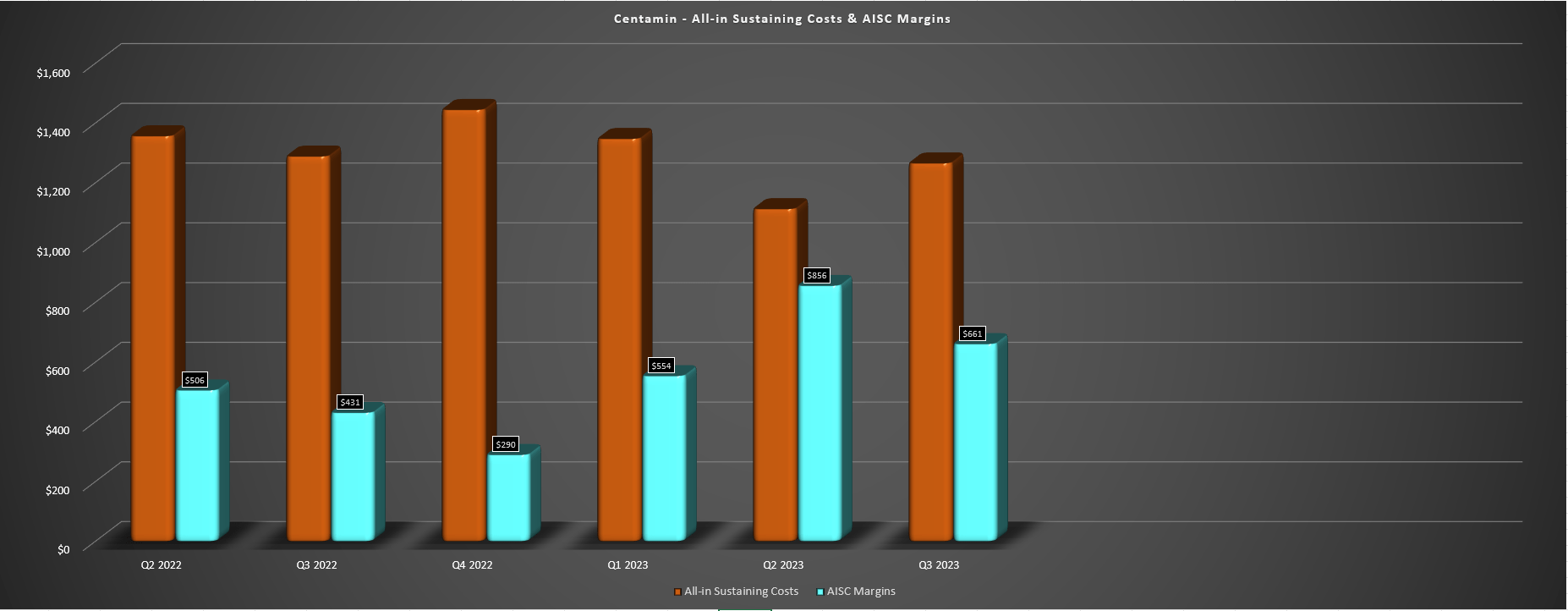

Centamin - All-in Sustaining Costs & AISC Margins - Company Filings, Author's Chart

{kind=link}

On a positive note, Centamin expects a stronger Q4 with high-grade inventory on its ROM pad, and we should see production closer to 500,000 ounces next year. In addition, while production was down sharply due to the lower sales, all-in sustaining costs [AISC] fell 2% year-over-year to $1,266/oz, with AISC margins improving to $661/oz (Q3 20222: $431/oz) on the back of a higher average realized gold price. These lower all-in sustaining costs were driven by lower sustaining capital spend, lower fuel/consumables costs, offset by fewer ounces sold. Finally, from a financial standpoint, the company generated $200.4 million in revenue on sales of ~103,800 ounces, and free cash flow of $12.4 million despite the difficult quarter. Free cash flow benefited from lower capital expenditures year-over-year, and Centamin finished the quarter with ~$126 million in cash and ~$276 million in liquidity with its undrawn $150 million senior secured RCF.

Centamin - Quarterly Free Cash Flow & Average Realized Gold Price - Company Filings, Author's Chart

{kind=link}

Recent Developments

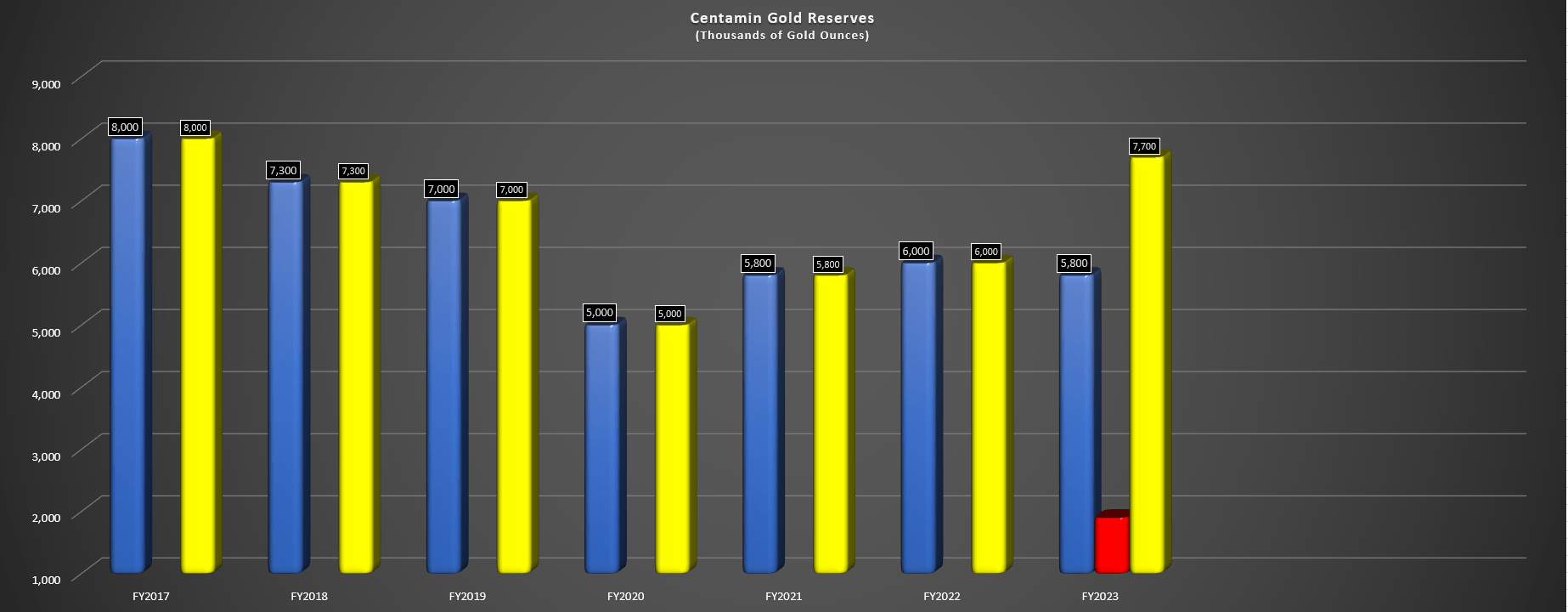

Moving over to recent developments, it's been a busy H2 for the company. Not only did Centamin released a new and more robust updated life of mine plan [LOMP] for its flagship Sukari Mine, but it also declared maiden reserves at its Doropo Project, and released a new updated resource/reserve estimate at Sukari. Starting with the resource/reserve estimate, Sukari's reserves increased to ~5.8 million ounces at a relatively conservative $1,450/oz gold price assumption, while mineral resources landed at ~11.3 million ounces, with ~91% of resources in the M&I category. Within the reserve base, open-pit ounces stood at ~4.4 million at 1.1 grams per tonne of gold while underground reserves (2.2 gram per tonne cut-off) came in at ~1.1 million ounces at 4.0 grams per tonne of gold. This solid underground reserve base supports the company's plan to increase underground mining rates to ~1.4 million tonnes per annum, with just shy of 9.0 million tonnes in underground reserve inventory.

Centamin - Annual Gold Reserves - Company Filings, Author's Chart

{kind=link}

As for the company's total reserve base, Centamin's reserve ounces increased to ~7.7 million ounces with the addition of Doropo, and the company believes that it can increase production to ~700,000 ounces from 2027-2032 company-wide, giving it a similar production profile to intermediate producer Evolution Mining ( CAHPF ) which continues to see above-average share dilution due to an aggressive M&A strategy with multiple acquistions since 2020. However, perhaps the most positive takeaway from Centamin's H2 news flow is that its Sukari Mine's updated LOMP is projecting ~506,000 ounces over the next nine years at industry-leading all-in sustaining costs of $922/oz. Meanwhile, the company has pulled forward capex from 2024 with spending planned on its grid power connection and new open-pit truck purchases, with the former expected to lead to ~$40 million in annual savings on sub $50 million investment to reduce reliance on higher-cost diesel power.

Even assuming just $25 million in annual savings over twelve years to be conservative, the grid connection will offer a 500% return on investment, while the planned gravity circuit will improve LOM recovery rates for a paltry ~$20 million investment based on the current design plans.

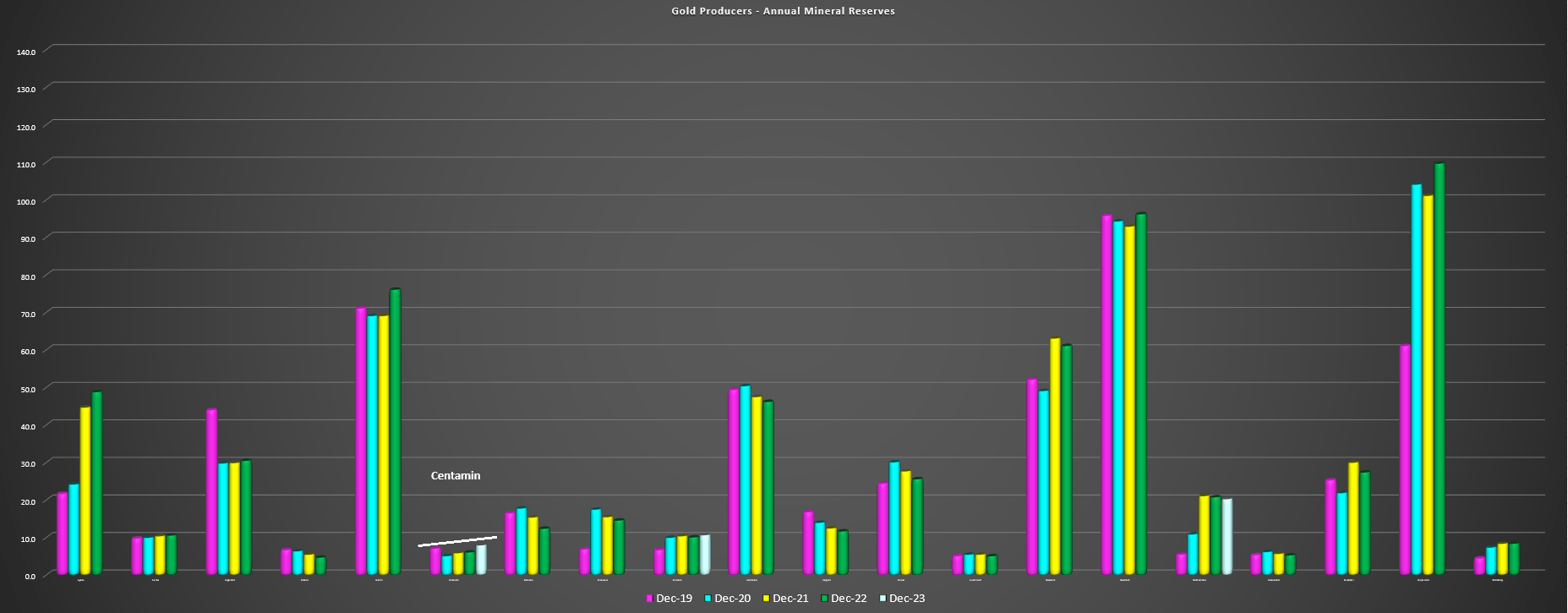

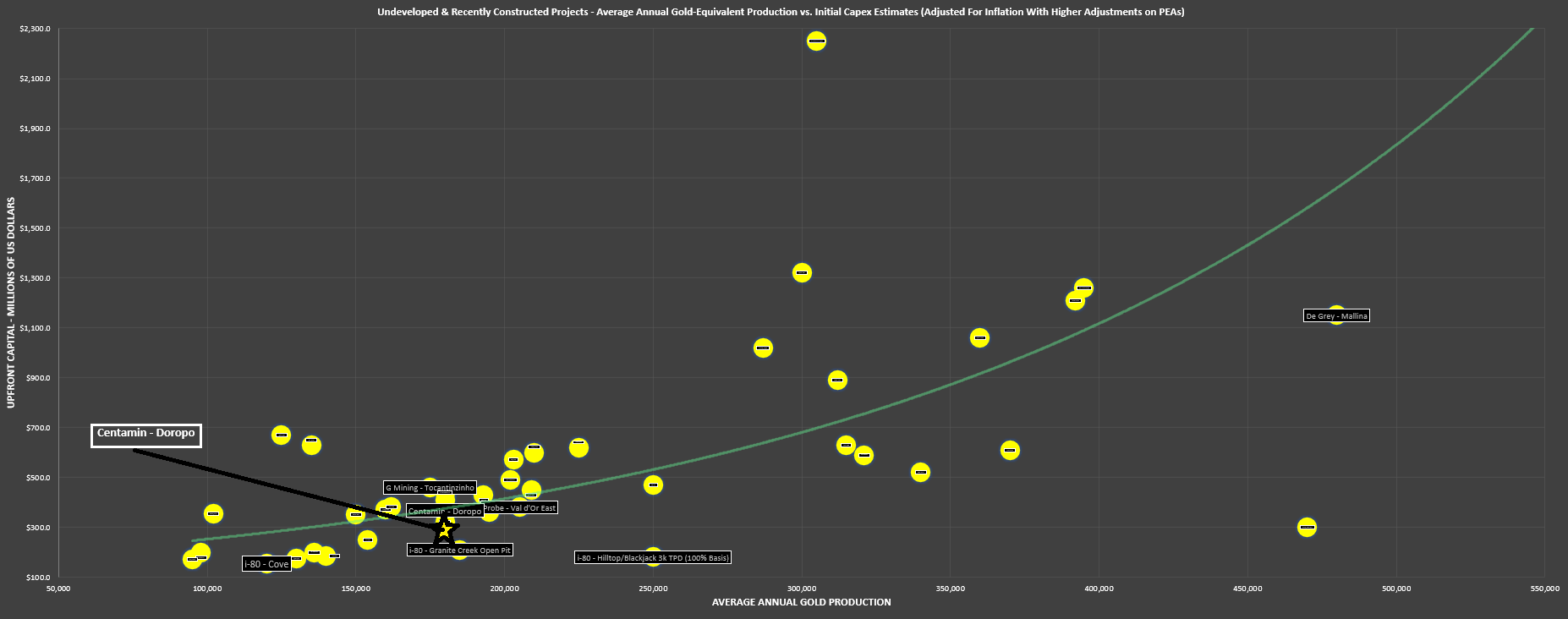

Finally, looking at how Centamin's reserves stack up against peers, we can see that Centamin now has one of the better track records of reserve per share growth. This is because unlike producers such as Evolution and Ramelius Resources ( RMLRF ) that have been busy with share deals, Centamin has continued to grow resources/reserves organically without any share dilution. In fact, it's one of the few producers that has grown reserves by nearly 20% without relying on M&A or share issuance, as highlighted by the below chart. Just as importantly, this reserve growth is not coming from marginal projects, with Doropo being one of the better undeveloped assets sector-wide with the potential for production of ~210,000 ounces in the first five years at sub $950/oz all-in sustaining costs when adjusting for inflationary pressures.

Major Gold Producers - Annual Reserves Progression - Company Filings, Author's Chart Undeveloped & Recently Constructed Gold Projects - Company Filings, Author's Chart & Estimates

{kind=link}

{kind=link}

Let's take a look at Centamin's valuation and see whether this improved production and cost profile (~700,000 ounces in 2027 at sub $950/oz AISC or ~460,000 attributable ounces when adjusting for 50% profit-share) looks priced into the stock:

Valuation

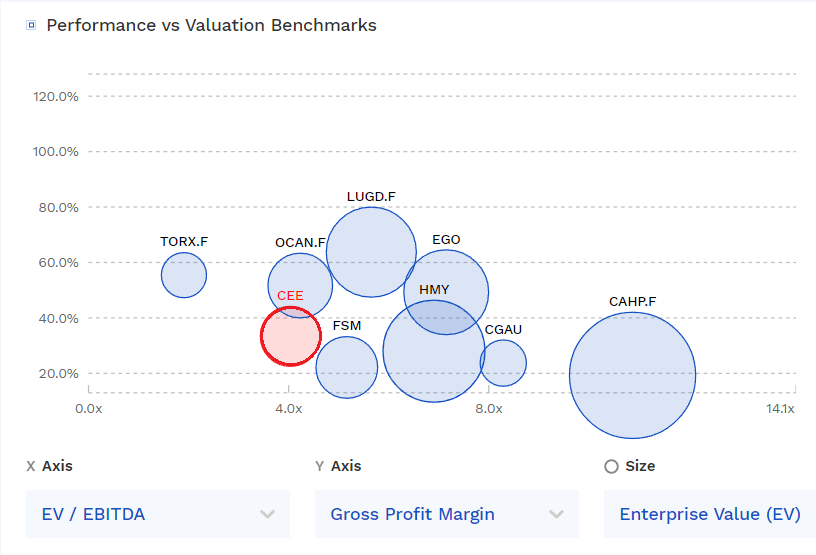

Based on ~1.16 billion shares and a share price of US$1.24, Centamin trades at a market cap of ~$1.45 billion and an enterprise value of ~$1.39 billion. This makes it one of the lower capitalization names in the sector (especially among peers with Tier-1 scale operations of 400,000+ ounces), though this is partially attributed to its profit-sharing with EMRA on a 50/50 basis at Sukari vs. peers with near full ownership of their assets. That said, Centamin continues to screen well from a P/NAV standpoint relative to peers following its updated LOMP at Sukari, and certainly when we factor in its growth to a similar scale to Evolution Mining (if Centamin green-lights its Doropo Project in Cote d'Ivoire). In fact, Centamin's P/NAV multiple currently sits at 0.78x based on an estimated net asset value of ~$1.87 billion (includes $300 million in exploration upside at Sukari & its Eastern Desert Exploration Blocks).

Valuations Peer Group vs. Centamin - FinBox

{kind=link}

Using what I believe to be a fair multiple of 1.0x P/NAV and ~1.16 billion shares outstanding, I see a fair value for Centamin of US$1.60. This points to a 29% upside from current levels and a near 32% total return when including Centamin's industry-leading dividend yield. That said, I am looking for a minimum 35% discount to fair value to justify buying small-cap producers to ensure a margin of safety, pointing to a low-risk buy zone of US$1.06 or lower. In summary, while I think Centamin could easily hit the US$1.62 level over the next year if the company continues to execute successfully, I think there are more attractive bets elsewhere in the sector currently.

Summary

Centamin had a tough Q3 while simultaneously lapping difficult comps, but the company is still on track to deliver into its full-year guidance, has a bright future ahead. The latter is evidenced by a more robust LOMP at Sukari, catalysts that include green-lighting Doropo and exploration results from regional exploration, and ultimately graduating to dual-asset producer status by 2028 with a ~700,000 ounce production profile. That said, I continue to a better reward/risk ratio for names like K92 Mining ( KNTNF ) that have 100% ownership of furture Tier-1 scale assets with higher margins yet at a lower enterprise value (~$1.0 billion), trading at barely 3x FY2026 EV/FCF. Hence, while I see Centamin as a solid buy-the-dip candidate, I would need a dip below US$1.06 to become more interested.

For further details see:

Centamin: Growth At A Reasonable Price