CNP - CenterPoint Energy: Well-Positioned For Ongoing Dividend Growth

2023-11-30 06:00:00 ET

Summary

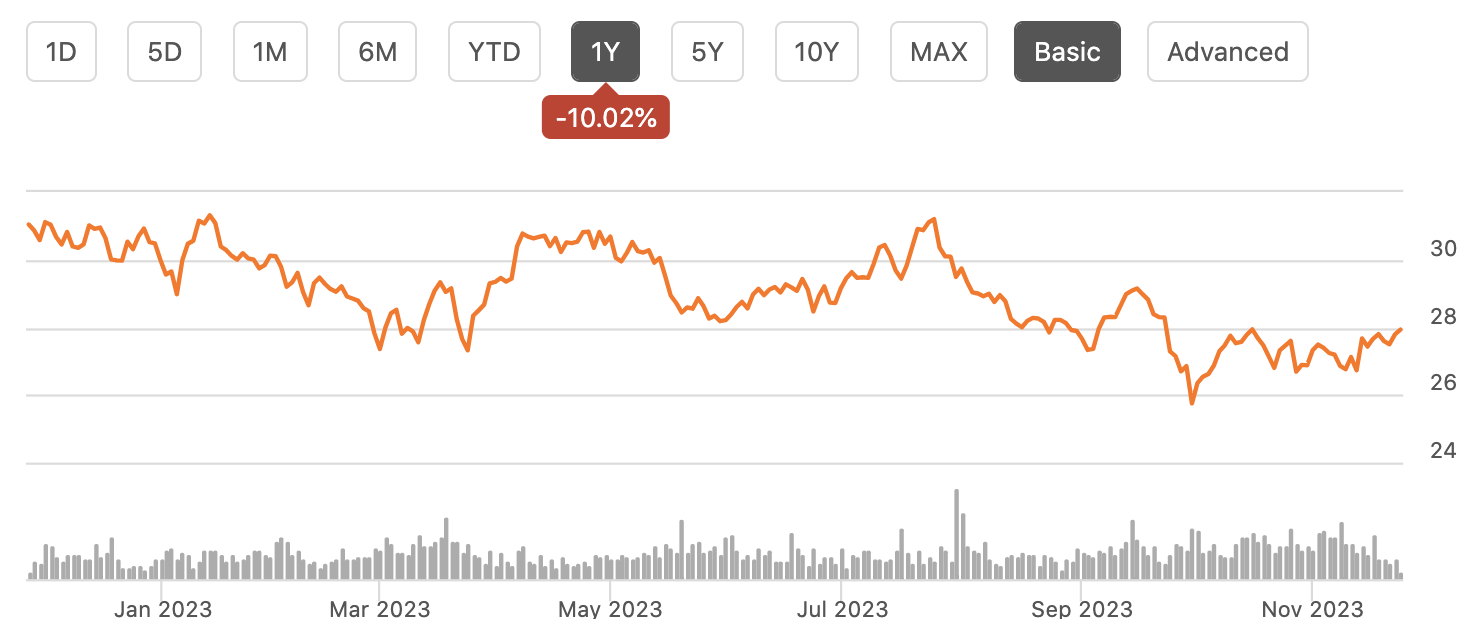

- CenterPoint Energy's shares have underperformed, losing about 10% of their value due to higher interest rates and concerns about cap-ex programs.

- The company reported adjusted EPS of $0.40, up from $0.32 last year, and expects to earn $1.49-$1.51 for the full year.

- CenterPoint has simplified its operations around its core Houston utility, which is attractive with its go-forward dividend growth potential.

Shares of CenterPoint Energy (CNP) have been a poor performer over the past year, losing about 10% of their value. Higher interest rates have been a significant contributor to this, with higher-rates making dividend-oriented stocks less attractive as well as leading investors to worry about the feasibility of cap-ex programs. While CNP's long-term dividend track record is unimpressive, the company has greatly simplified its operations around its core Houston utility, which should make go-forward dividend growth more attractive for investors.

{kind=link}

In the company's third quarter , CenterPoint earned $0.40 in adjusted EPS, which was up from $0.32 last year. For the full year, it now expects to earn $1.49-$1.51. It also initiated 2024 earnings guidance at $1.61-$1.63, representing 8% growth. From 2025-2020, it is targeting 6-8% growth, putting 2024's target at the top-end of this longer-term goal.

Rate recovery was the primary driver of the earnings growth as it was a $0.08 tailwind from last year as CenterPoint recouped past capital expenditures. Results were flattered with weather a further $0.06 benefit. Absent this, earnings growth would have been about 6%--a more realistic view of the company's run-rate growth potential. Weather can be volatile on a quarter-by-quarter basis, impacting utility usage. Interest expense was an $0.08 headwind-this is a headwind that should moderate going forward.

Interest expense was up to $176 million from $116 million last year. Higher rates have been a meaningful headwind, though they have not been enough to eliminate earnings growth. At the start of the year, CNP had $4.5 billion in floating rate debt, about 25% of its $18 billion total. It has reduced this down to $1.8 billion, so higher rates are largely now factored into results. It has $1.2 billion of maturities next year, at under 4% on average, so there will be a modest increase in interest expense likely from this refinancing. After 2024, CenterPoint has just $51 million in 2025, and a more substantial $2.3 billion in 2026, by which point rates may be lower. Ultimately, we are likely to see interest expense stay at this new level rather than go back down, but it should rise much more slowly than it has the past twelve months.

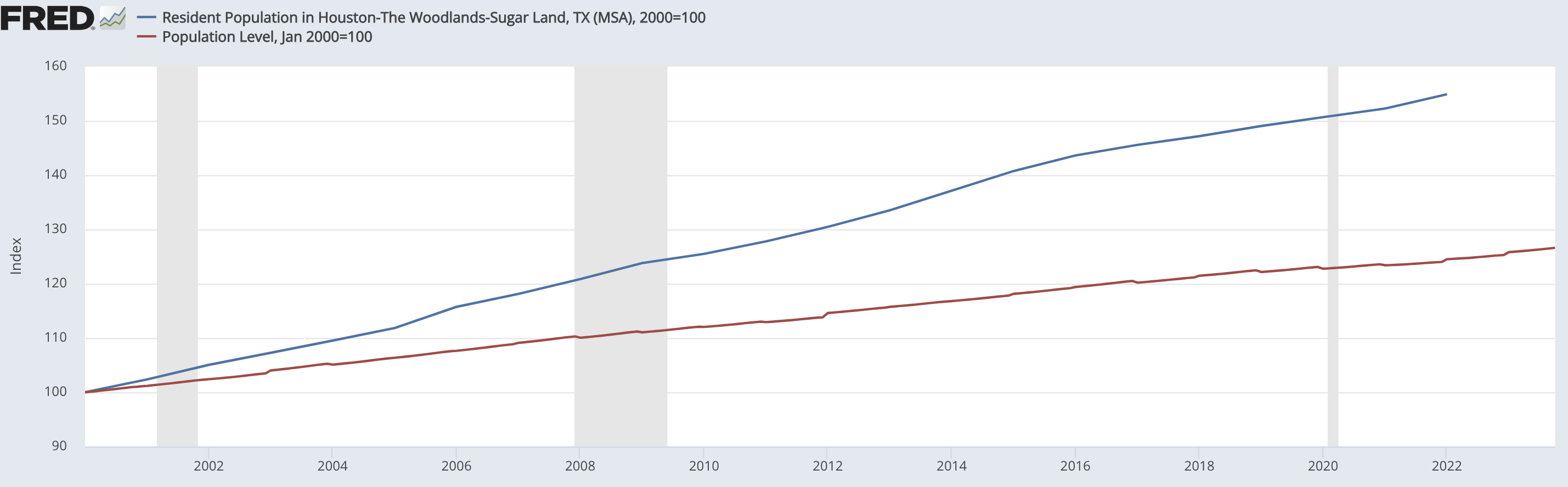

Over the medium term, utilities can grow earnings and cash flow, and thereby dividend capacity through two ways: customer growth and by investing in the expanding the rate base on which they earn a regulator-approved returned on equity. On the first, CNP is extremely well positioned. While it operates across multiple states, Houston Electric drives about 60% of revenue . Revenue rose 15% from last year thanks to the blistering growth in the Houston area. Since 2000, Houston's population has risen by more than 50%, growing twice as quickly as the national average. CNP continues to plan on 1-2% customer growth, even as recent results suggest that could be conservative.

{kind=link}

Increased customer counts also help maintain good relations with regulators and the public. An increasing customer base helps to spread the rate base across more people, helping to reduce the per-customer bill. The less customer bills rise, the happier the public and the regular are. Impressively, a Houston Electric customer pays $49/1,000KWH, which is the same they paid in 2014. In. world of meaningful inflation, holding rates flat over the past decade is an impressive performance.

Beyond benefitting from a growing customer base, CNP has proven to be an austere operator. Its Houston Electric operation and maintenance (O&M) expenses were up just 3.5% from a year ago, rising 10% more slowly than revenue. This takes further pressure off of customer bills. When the company seeks to recoup investments or raise rates, it is helpful to have customer bill growth being relatively low. When bills are rising quickly, there is likely to be less appetite to increasing a utility's revenue.

This budget-conscious philosophy is evident across the company's operations. Total operation and maintenance expense of $648 million was down over 4% from last year. Since 2021, O&M has fallen by 12%. Moreover, in the wake of a bad Texas winter storm last year that caused surging prices, utilities like CNP were able to recoup excess energy costs through securitizations. The end of this surcharge will be next year, which will reduce bills for customers by 4%. This should give it even further leeway to gradually raise rates as this essentially will pay for several years of the 1-2% bill grow it is targeting in its medium-term capital plan.

Outside of Houston Electric, energy resources revenue was down by $89 million to $583 million, but natural gas expenses were down by $135 million. This unit is simply passing along natural gas prices to customers, not taking actual commodity risk itself, though there can be slight quarterly timing mismatches. This can cause revenue and margins to move in ways that do not impact CNP economically over time. Overall, we see the company growing revenue, enjoying customer growth, and maintaining cost discipline.

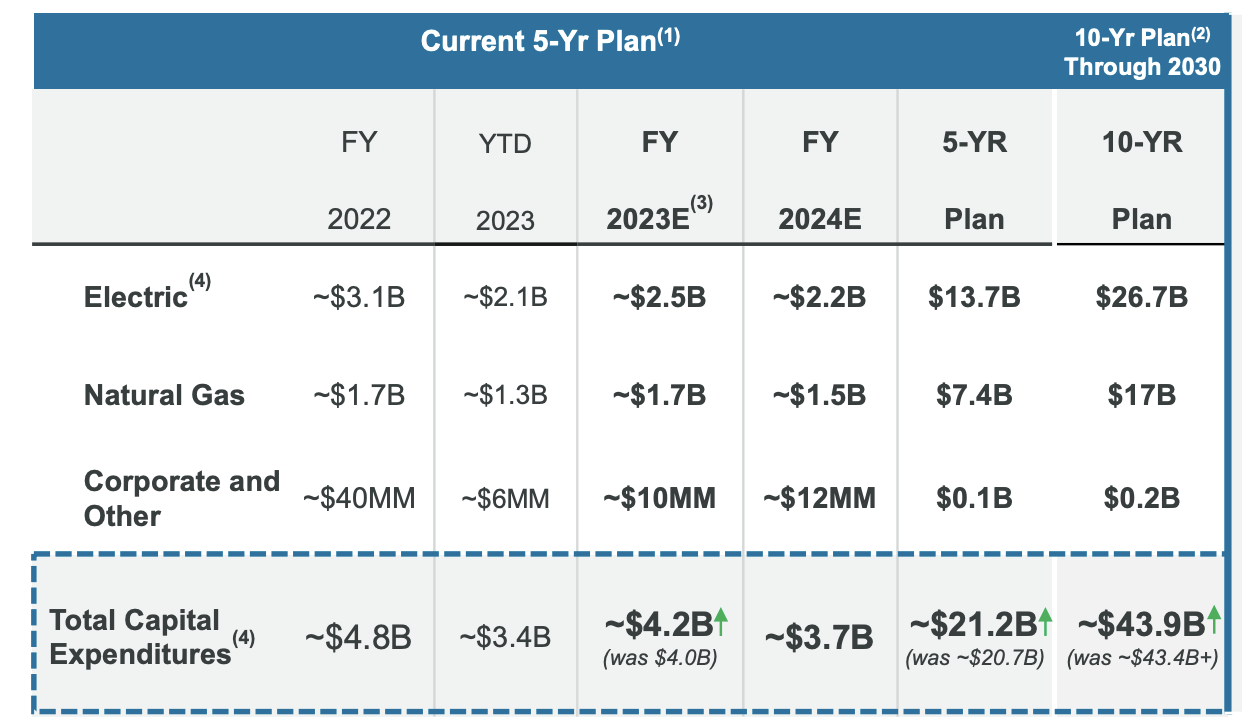

Alongside these results, CenterPoint increased its 2020-2030 capital plan by $500 million to $43.9 billion. $200 million of this is coming in 2023 with the balance in 2024-2025. As a result, it plans on issuing $250 million in stock through an "at-the-market" (ATM) program. CNP can fund the first $43.4 billion via retained cash flow and incremental debt issuance, but beyond that, it needs additional equity to maintain a sufficiently strong balance sheet. As part of this capital plan, it is targeting an FFO (funds from operations)/Debt ratio of 14-15%, and it sits at 14.3% today. This is a fairly modest equity issuance program, at about 1.5% of its market capitalization. Importantly, management committed to its 6-8% long-term earnings growth target, including the impact of dilution from equity issuance.

As you can see below, capital spending sill slow a bit in 2024 from this year. It has spent more than $3.3 billion in cap-ex so far this year with $3.1 billion of operating cash flow, though this included about $1 billion of favorable working capital movement. Including about $408 million in dividends, about half of its cap-ex program is funded via retained cash flow and half via debt, a prudent allocation breakdown. This capital program should significantly increase the company's rate base, which sits at $22.3 billion, though four pending cases will increase that total somewhat.

{kind=link}

It is off of that base that it earns its regulator-approved return on equity. By being able to aggressively grow the rate base, it can support its medium-term earnings targets. Critically, 80% of rate actions will be earned through interim mechanism with just 15% having to go through formal rate cases. This makes increases to the rate base quite likely, especially as most of its work is aimed at improving the resiliency and reliability of the grid.

Following crippling winter storms, reliability is a significant public policy goal in Texas, which is planning a $10 billion fund to enhance its utility grid. With public buy-in and state resources going to this goal, investors should feel fairly confident in CNP's ability to grow its rate base, especially considering its ability to manage customer bills. In fact, management sees more than $2.6 billion in opportunities beyond its $43.9 billion capital plan. However, with incremental spending requiring equity issuance, there is a higher hurdle rate to future predicts, to ensure that they are accretive. The current program is sufficiently ambitious to grow earnings meaningfully, and there is no pressing need to expand it further. Instead, this points to growth potential beyond 2030.

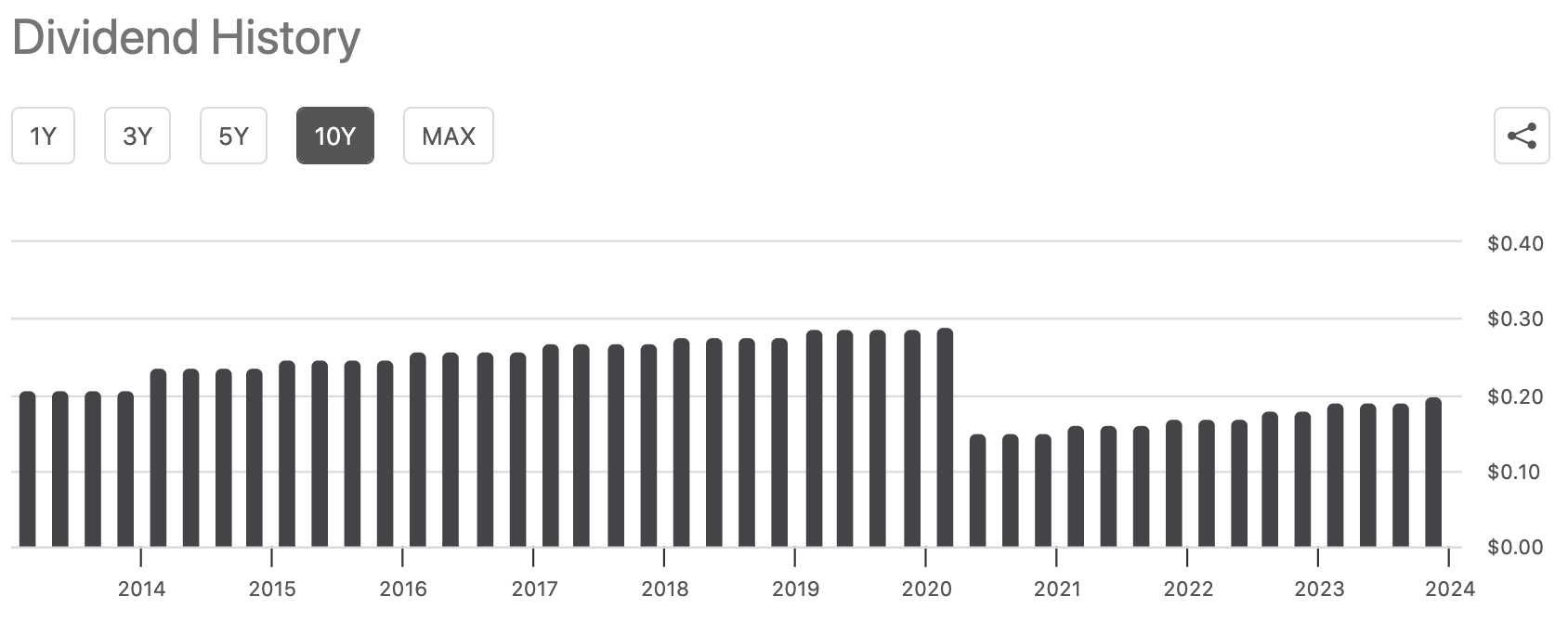

Over the next few years, CNP aims to grow its dividend alongside earnings. During the quarter, CenterPoint increased the dividend to $0.20, now 10% higher than last year, and shares now yield 2.9%. In 2020 , CenterPoint had to cut its dividend by nearly 50% after its MLP, Enable cut its distribution, thereby reducing cash flow to CNP. Last year, CNP completed its exit from the midstream business after Enable merged with Energy Transfer (ET), and CNP sold its equity in ET for about $2 billion . Ultimately, dividends are lower because they are solely supported by the utility and no longer what proved to be a volatile set of midstream cash flows.

{kind=link}

I would emphasize this dividend cut did not have to do with problems at the utility business, but in the midstream business. This unit is now gone, and the dividend is solely support by a highly-regulated utility business. This is a simpler company with more predictable cash flows. As such, the next ten years should not look like the past ten.

With a starting yield near 3%, and a credible 6-8% growth target, CNP should be able to generate ~10% medium-term returns in a fairly low-risk fashion. While not a stock that will "double your money" in a short period of time, for investors seeking a steady source of income growth, this simplified CNP should benefit from Texas's growth and focus on electric reliability. I view shares as attractive.

For further details see:

CenterPoint Energy: Well-Positioned For Ongoing Dividend Growth