CSR - Centerspace: Active Market Participants At The Wrong Time

Summary

- Centerspace is a multifamily REIT that has an interest in a portfolio of apartment communities located in the Midwest and Mountain West regions of the U.S.

- The company has benefitted from a record year in the rental housing business. Growth, however, appears to be moderating.

- Rising interest rates and capital-related costs are also creating an uncertain market environment.

- Despite the uncertainties, CSR remains an active participant. While this may pay off over the long term, the timing doesn't appear right in the current macroeconomic environment.

Centerspace ( CSR ) owns a geographically differentiated portfolio of multifamily apartment communities across the Midwest and Mountain West United States, with a significant footprint in Minnesota and Colorado.

June 2022 Investor Presentation - Map Of Geographic Concentration By NOI

Over the past two years, their operating markets benefitted from increased inbound migration from tenants seeking more space and recreational opportunities. This enabled continued rental rate growth that remained supported by favorable supply dynamics.

Following a solid stretch of elevated growth rates, the market now appears to be moderating. Rising interest rates and capital-related costs are also creating an uncertain operating environment. But instead of stepping to the sidelines in the face of uncertainty, CSR remains active market participants, as net purchasers of additional property and of their own stock. The timing, however, doesn't seem right, especially when considering their elevated debt load and liquidity position.

An Ill-Timed Portfolio Acquisition In A Period Of Slowing Rental Growth

As of September 30, 2022, CSR owned an interest in 84 apartment communities comprising approximately 15K apartment homes. This is up one community from last quarter due to their recent acquisition of Lyra Apartments , a 215-home apartment community located in Colorado.

This community was acquired at a going-in cap rate of about 4.25% via a drawdown on their credit facility. At the time of purchase, the property was also stabilized and over 90% occupied. Given current interest rates, however, the acquisition created an instance of negative leverage that ultimately contributed towards a $0.02/share reduction in the midpoint of their guidance for core funds from operations ("FFO").

Though management believes the asset is well positioned in the Denver submarket, it appears the purchase was made at or around the top of the market. And management acknowledged as much by noting they weren't underwriting particularly strong growth in a market that is broadly cooling.

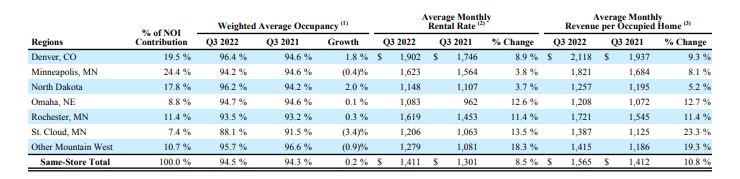

In Q3 , for example, the average monthly rental rate ("AMRR") on their same-store portfolio in their Denver region grew 8.9% YOY. While this is a healthy rate of growth, it's lower than the 9.6% YOY growth reported in Q2 . It's also shy of the double-digit rates posted in their other top markets.

Q3FY22 Investor Supplement - Portfolio Metrics Of Key Operating Markets

{kind=link}

In defense of the higher purchase price, it was noted that the property was bought at less than what it would cost to build it. And over the long term, the acquisition is expected to be a net contributor to earnings growth. But that aside, the company is taking a near-term hit to earnings due to the higher interest costs associated with the purchase.

Higher Interest Costs On An Already Elevated Debt Load

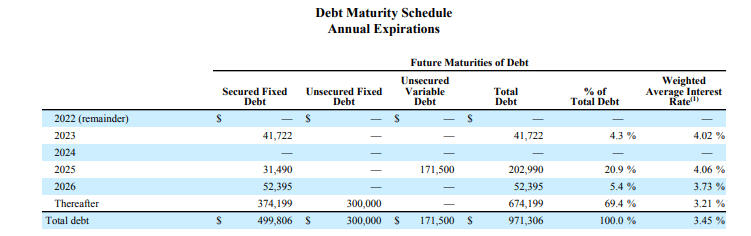

As it is, leverage is on the high end. At the end of the quarter, net debt as a multiple of adjusted EBITDA stood at 7.7x. This is consistent with prior quarters in the current fiscal year and down from the 8.7x level last year, but it's elevated, nevertheless.

{kind=link}

CSR does benefit from a favorable debt ladder, with over 90% of their total stack due in 2025 or thereafter. Additionally, the debt load is mostly fixed-rate, which insulates them from the worst effects of interest rate volatility.

{kind=link}

The revolver, however, carries a variable rate. The +$98.5M drawn for the purchase, therefore, exposes the company to higher rate risks during a period marked with more stringent lending conditions. Granted, the balance on the line can likely be termed out, but the terms may not be favorable enough to clear the elevated hurdles created by the bloated purchase price.

Lower Total Liquidity Reduces Financial Flexibility

The acquisition also further constrained total liquidity to about +$100M at period end, which is over +$110M lower than the end of 2021. Though the company consistently generates positive cash from operations, the reduced flexibility is noteworthy, considering the company is also engaging in share repurchases, which itself is curious, given widely cited challenges in price discovery among active market participants. Even with these uncertainties in mind, however, management evidently believes their stock price is overly disconnected with current fundamentals.

Another constraining commitment is rising capital expenditures ("CAPEX") on their same-store portfolio. In the current period, for example, total non-value-adding CAPEX increased by 87%. And as properties from their previously completed KMS acquisition transition into the same-store population, that is likely to increase further due to increased CAPEX requirements relating to the age of the properties.

Rising Expenses In Addition To Greater CAPEX Requirements

In addition to rising CAPEX requirements, repairs and maintenance ("R&M") costs in the same-store portfolio were also up significantly during the period due to factors such as increased portfolio turnover, availability of labor, and rising security needs, particularly in their urban assets.

In Q3, just over 5% of their YOY move-outs were related to the lifting of eviction moratoriums in certain key markets. In Minnesota, for example, a state representing 50% of total NOI, all aid has now tapered off, which is allowing CSR to turn impacted tenants, though that is coming at a higher R&M cost, as the space is typically not in ideal condition upon possession. Compounding the issue is greater difficulty securing available labor, especially in an operating region of the country that is generally more sparsely populated.

As the weather gets colder, utilities are another cost that can weigh on earnings in future periods, given an expected hike in heating-related costs. Similar to labor availability, CSR's geographic footprint presents a disadvantage due to colder-than-average winters experienced in their operating regions. While many of these costs can be passed through rates or hedged, regulations may impede cost recovery efforts in certain markets.

Revenue And Earnings Growth Still Positive Despite The Challenging Environment

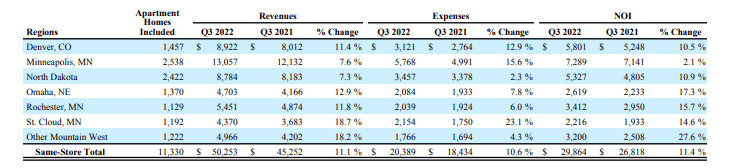

Despite higher overall costs, CSR still benefitted from strong revenue growth, which ultimately resulted in core FFO that was up 17% for the quarter and 11% YTD, driven by double-digit same-store NOI growth of 11.4% from the same period last year.

In individual markets, same-store revenues were up double-digits in all markets except Minneapolis and North Dakota due to higher average rates and slightly stronger overall occupancy of 94.5%. NOI also remained robust everywhere except Minneapolis, a region that was significantly pressured from higher expense burdens.

Q3FY22 Investor Supplement - YOY Comparison Of Revenues, Expenses, And NOI

{kind=link}

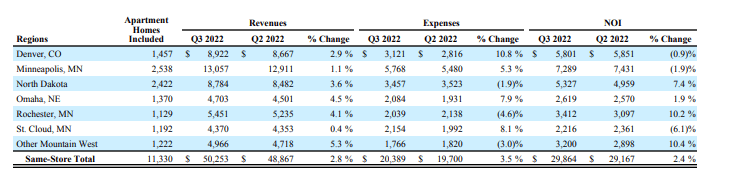

Sequentially, the impact of rising expenses was more pronounced, with growth outpacing revenues by 70 basis points ("bps") overall, with a notable divergence in the Denver and St. Cloud markets that ultimately resulted in a 90 and 610bps decline in NOI, respectively.

Q3FY22 Investor Supplement - Sequential Comparison Of Revenues, Expenses, And NOI

{kind=link}

Given the higher expense burdens across their portfolio, in addition to the dilutive effects of their Lyra acquisition, core FFO guidance was revised downwards by $0.07/share at the midpoint to $4.46/share. This is despite a 25bps increase to the midpoint of expected same-store revenue growth.

Not Enough Upside Potential To Overcome Return Hurdles

CSR continues to report positive earnings growth against a backdrop of a record year in the rental housing business, with 2022 likely being their fourth straight year of same-store NOI and core FFO growth.

A differentiated market focused on the Midwest and Mountain West states provide key benefits, such as lower unemployment rates and a favorable supply dynamic characterized by the lowest percentage of construction among their multifamily peers.

June 2022 Investor Presentation - Supply Outlook In CSR's Markets Compared To Peers

This has enabled the company to drive rents, especially over the past two years. But even with the increases, the average monthly rate across the portfolio remains affordable relative to other markets across the country, which are commanding over $2K a month in certain markets compared to $1,400/month in CSR's operating regions. And with a loss-to-lease of approximately 6.5%-7%, the company still has some room to drive rents further in the periods ahead.

Despite the opportunity, growth rates appear to be moderating. And this moderation is occurring simultaneously with rising expense burdens associated with higher interest costs and other controllable expenses, such as R&M. Negative leverage tied to the current period Lyra acquisition only amplified these pressures.

At a forward multiple of 15.2x, CSR is currently trading on par with NexPoint Residential Trust ( NXRT ), which is another multifamily peer that is of similar size. This is down from the 19x multiple commanded earlier in the year.

While a return to former trading levels can't be ruled out, it's unlikely to be swift due to the slowing market environment. For existing shareholders, holding may be the better alternative than recycling into a peer with a comparatively similar macroeconomic outlook. Prospective investors, on the other hand, would be better off stepping aside altogether.

For further details see:

Centerspace: Active Market Participants At The Wrong Time