CSR - Centerspace: The Mountains Are Calling This Multifamily REIT

- Centerspace is a multifamily-focused REIT that has a strong operating presence in the Midwestern and Mountain regions of the United States.

- Their operating markets have benefited from the relative affordability of their properties and the employment trends of their tenant base.

- While growth has held up strongly over the past several quarters, moderation is likely in the coming periods.

- Earnings and dividend growth are likely to be further inhibited by rising debt servicing costs resulting from their fairly high debt load.

- While upside potential exists, better opportunities are available elsewhere.

Centerspace ( CSR ) is a real estate investment trust ("REIT") operating in the multifamily residential sector with an interest in 83 apartment communities consisting of over 14K apartment homes.

With a market cap of just over +$1B, they are on the smaller size compared to larger peers, such as AvalonBay Communities ( AVB ), Equity Residential ( EQR ), and Mid-America Apartment Communities ( MAA ), who each have a market cap in excess of +$20B, or +$30B in the case of EQR.

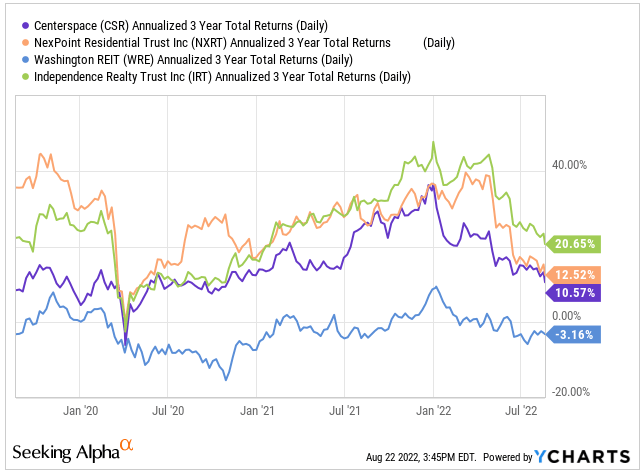

Similar-sized competitors include NexPoint Residential Trust ( NXRT ), Washington REIT ( WRE ), and Independence Realty Trust ( IRT ). Over the past three years, CSR has underperformed both NXRT and IRT, with a narrower gap of 195 basis points ("bps") compared to NXRT.

YCharts - Comparison of Annualized 3-YR Returns of CSR Compared to Competitors

{kind=link}

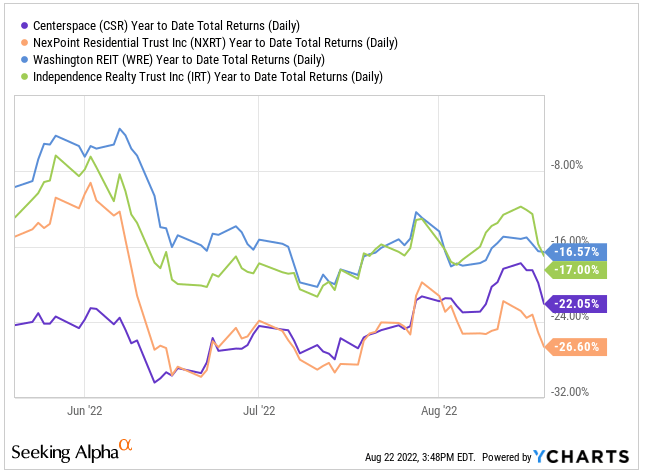

YTD, CSR is down over 20%. This is better than the nearly 27% decline suffered by NXRT. CSR is, however, currently priced at a lower multiple, at 18.9x forward funds from operations ("FFO") versus 20x for NXRT.

YCharts - Comparison of YTD Returns of CSR Compared to Competitors

{kind=link}

CSR reported solid quarterly results that showcased strengths displayed by other peers in the sector, namely rising rental growth that continues to be supported by limited supply and heightened demand due to the relative affordability of renting a multifamily unit versus outright ownership.

While shares are currently trading at the lower end of their 52-week range, a moderation in rental growth moving forward is likely to limit the upside potential. Appreciation to a 20x multiple is certainly possible, but that is still unappealing, given current risk premiums. While a solid portfolio holding, there are better opportunities elsewhere for those seeking new additions to their long-term portfolio.

Strong Operating Presence In The Midwestern and Mountain Regions Of The U.S.

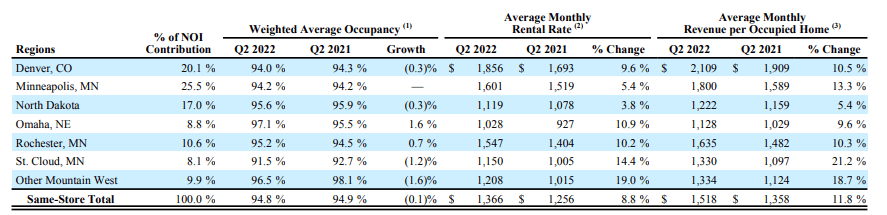

CSR's multifamily-focused portfolio is concentrated in the Midwest and Mountain regions of the United States, with Minnesota representing the majority of annual net operating income ("NOI"), at 50%, followed by Colorado, at 22%.

Their current exposure to Minnesota is up from just over 10% in 2017, a period in CSR's history where they had just begun to focus exclusively on multifamily housing. Additionally, CSR had no presence in Denver in earlier years. The current expansion into the competitive region, therefore, is impressive from an external growth perspective.

June 2022 Investor Presentation - Map of Geographic Concentration

Overall, CSR's portfolio includes nearly 15K homes. While approximately 40% of these homes are in Minneapolis, Denver produces the most revenue per occupied home, at around +$2K, which is up 10.5% from Q2FY2021. Weighted average occupancy of 94% does lag other markets, however. And occupancy did decline 30bps from last year following nearly 10% growth in average monthly rental rates. Nevertheless, given the region's share of total NOI and current occupancy levels, Denver is likely to be one continuing driver of growth for CSR.

Q2FY22 Investor Supplement - Portfolio Metrics of CSR's Key Markets

{kind=link}

Though total weighted average occupancy in Q2 remained strong at 94.8%, it is a slight decline from the same period last year, weighed down not only by Denver but by St. Cloud, Minnesota, which experienced a 120bps decline, and other non-reportable mountain regions, which collectively lost 160bps of occupancy.

The declines are partly due to the average rent-to-income ratios in the affected areas. In Denver and St. Cloud, for example, the ratios stood at about 20.5%, the only two markets where the burden was 20% or greater. Granted, this is lower than the 30% seen in non-CSR markets. But it is noteworthy that the renters in two of CSR's largest markets are more sensitive to rental rates.

Another potential factor driving occupancy declines in certain areas is the return-to-work initiatives being implemented by many companies based out of the coastal locations. During the height of the COVID-19 pandemic, drawn by the open spaces and vast recreational opportunities, many migrated to the mountain states to conduct fully remote operations. But since then, many employers have begun calling employees back for more hybrid working arrangements. This is forcing many to relocate back to their original locations. Moving forward, this may become more pronounced in certain CSR markets, creating a drag on occupancy gains.

The occupancy declines in certain regions are offset by strength elsewhere, however, particularly in Minneapolis, where occupancy has remained fixed despite a 5% increase in average rates and a 13% increase in revenue per occupied home. In addition, though there was a slight YOY decrease in occupancy levels, occupancy was still up 90bps sequentially.

Benefiting From Below Average Unemployment Rates And Construction Activities

CSR's markets also benefit from an unemployment rate that is well below both their competitors and the U.S. average, which stood at 3.9% at the end of March 2022 compared to 2.7% for CSR. This is one contributing factor to the generally low rent burden in most of their markets and is one strength that should support the portfolio from rising delinquencies and/or material vacancies.

June 2022 Investor Presentation - Comparison of Average Unemployment Figures in CSR's Markets Compared to Competitors

A limited supply of homes with a lower degree of construction activity in their markets is another competitive strength that sets CSR apart from their competitors. This will enable CSR to continue driving rents higher for as long as their tenants' employment and income prospects allow. With housing starts continuing to decline , the supply outlook is unlikely to change in the near-medium term, providing further tailwinds to their leasing activities.

June 2022 Investor Presentation - Comparison of Housing Supply Growth in CSR's Markets Compared to Competitors

A Strong Leasing Environment With One Major Exception

In the current period, total revenues grew 11.7%, due primarily to blended rental rate growth of 10.5% and a 90bps overall occupancy gain from the first quarter. While property-related expenses did track higher during the period, same-store NOI is still up nearly 10% YTD. And that is expected to accelerate further into the double-digits for the full year. In addition, core FFO was up nearly 14%, driven by strong same-store results, with quarterly same-store NOI up 11.5% from last year.

Results also continue to be favorably impacted by recent acquisitions, such as the +$324M acquisition in 2021 of 17 communities formerly owned by KMS Management, which have increased revenues by approximately 25% on an annualized basis.

In the current quarter, however, a major deal fell through after the company had already spent over +$1M conducting due diligence on the pursuit. Had it been successful, it would have increased CSR's portfolio by +$2B and given them scale in several new markets. According to management , their counterpart in the deal had second thoughts after reassessing current market conditions. Initially, the deal included the counterpart's entire portfolio. But after the reassessment, the counterparty felt compelled to piecemeal the portfolio, which was not acceptable to CSR. While this was somewhat downplayed by management on the earnings call, this fallout is concerning, especially considering YOY internal growth is expected to moderate in the coming periods.

An Undesirable Debt Load Will Weigh On Future Earnings And Dividend Growth

A further obstacle for future growth is CSR's high debt load. While their total debt as a percentage of their market cap was just 35% at period end, their net debt as a multiple of adjusted EBITDA was 7.1x. Though this is lower than the 7.7x reported last year, it is still on the high end. Additionally, their coverage ratios on both interest costs and total debt service don't provide the highest degree of cushion, at just 3.4x and 2.8x, respectively.

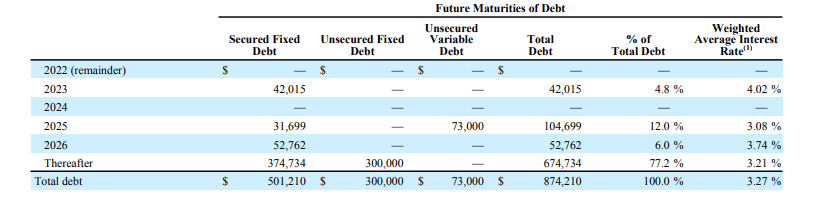

Alleviating these concerns is their favorable debt ladder , which is skewed significantly to later years, with nearly 80% due after 2026. Furthermore, their limited exposure to variable-rate debt should insulate them from the worst effects of a rising rate environment. As such, despite the higher debt load, there are no repayment risks at present.

Q2FY22 Investor Supplement - Debt Maturity Schedule

{kind=link}

Still, rising interest costs on their existing debt will weigh on earnings and inhibit their ability to take on new debt, resulting in a greater likelihood of further equity raises to fund future acquisitions. This, too, will weigh on future earnings. For income investors, the effects are likely to be felt through minimal dividend growth.

At present, the quarterly payout yields 3.5%, which is more than many of their peers. Coverage also is adequate, at approximately 65% of both AFFO and operating cash flows. Though safe in its current form, further increases, if any, are unlikely to be impressive, given their current debt exposure in current market conditions.

A Solid Portfolio Holding For Existing Shareholders But Better Opportunities Elsewhere For New Investors

CSR is a smaller multifamily-focused REIT with a strong operating presence in the Midwest and Mountain regions of the U.S. An abundance of outdoor recreational activities and the relatively lower cost of living in these locations has been a draw for many, especially in the current market environment.

The company has continued to report strong results that include rising occupancy levels, steadily growing rents, and full cash collections. A low rent-to-income ratio, despite rising rents, also provides confidence regarding the credit quality of their tenants. Favorable macro-related trends in the region, such as low unemployment and limited housing supply, should continue to support revenues in future periods.

With shares down over 20% YTD and trading at the bottom end of their 52-week range, some may find it of benefit to initiate a new position. The upside potential, however, is limited. Though rents are expected to rise further, growth is projected to moderate. Rising interest rates on their elevated debt load, which stood at 7.1x at the end of Q2, will further pressure earnings growth.

Additionally, at its current multiple of nearly 19x, shares aren't significantly discounted to the peer set, with NXRT trading at 20.6x. While appreciation to a 20x multiple is certainly possible, the gains are insufficient to cover the estimated CAPM-derived cost of equity of 8.5%. Though a solid portfolio holding for existing shareholders, new investors will be better off seeking opportunities elsewhere.

For further details see:

Centerspace: The Mountains Are Calling This Multifamily REIT