CSR - Centerspace: Weighed Down By A Higher Interest Burden

Summary

- Centerspace owns a portfolio of multifamily apartment communities, located primarily in the Midwestern and Mountain regions of the U.S.

- The company ended 2022 with occupancy gains, strong same-store performance, and earnings growth.

- But a higher debt load and an elevated degree of variable rate exposure is creating headwinds on forward guidance.

- Shares trade at an attractive forward multiple, but the lower valuation is justified, given fundamental dynamics.

Centerspace ( CSR ) owns a portfolio of multifamily apartment communities, located primarily in the Mountain and Mid-Western regions of the U.S. In recent years, their Minneapolis market has represented a growing share of operating income, as does Denver, Colorado.

November 2022 Investor Presentation - Share Of NOI By Market (September 2022 Vs 2017)

The company’s operating regions continue to benefit from favorable macroeconomic tailwinds, such as low unemployment rates and a low degree of new incoming supply, compared to national averages. This provides CSR with the continued ability to drive rent growth, while maintaining current occupancy levels.

Since two prior updates on the stock, shares have continued to decline. Since the most recent update, the stock is down just over 2%, which compares unfavorably to an increase of over 5.5% in the broader markets.

Seeking Alpha - Summary Of Prior Ratings History On CSR

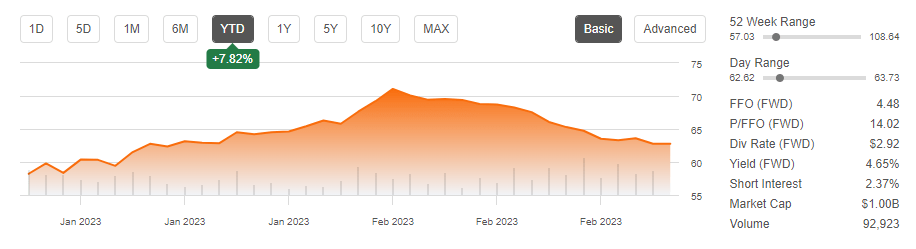

Though shares are up almost 8% YTD, they are still down over 30% over the past one year.

Seeking Alpha - Basic Trading Data Of CSR

{kind=link}

Fresh off their most recent earnings release, CSR is trading at an attractive forward multiple of 14x, and their dividend currently offers a yield of over 4.5%. Despite these draws, the company is likely to face headwinds in 2023 due to their higher debt load. Their dividend is also less secure than how it appears at the surface. For investors, it remains best to maintain a sideline position.

Recent Performance and Current Portfolio Metrics

At the end of 2022 , total portfolio occupancy stood at 94.6%. In the same-store portfolio, which represents the primary share of operations, it stood at 94.5%. This is up 20 basis points (“bps”) from 2021.

For the year, same-store net operating income (“NOI”) grew 9%, led by strong overall revenue growth of 10%. And for the quarter, same-store revenues were up 9.3%. This was due in part to blended rental growth of 4.2%, driven primarily by a 7.2% increase in renewal spreads.

On an overall basis, their same-store portfolio locked in spreads of 8% and 8.4% for new lease signings and renewals, respectively. While renewals remain strong in the new year, the company is experiencing a return to a more normalized pricing environment. Renewals in January 2023, for example, were up 6.5%, while new leases were up 1.4%.

Likewise, traffic and inquiries to their properties have also returned to pre-COVID levels but were still up YOY through the day of their earnings release. The continuing demand was reflected in their Q4 weighted average occupancy levels, which increased 40bps to 94.9%. And this came on near-full collections of 99.8%.

Strength in their same-store portfolio contributed to an overall increase in full year funds from operations (“FFO”) of 11%.

Looking ahead to 2023, management is expecting same-store NOI growth of 8% in 2023 at the midpoint. Key drivers for this include estimated earn-in of 4% and projected blended rate growth of 4.5%.

Additionally, total expense is expected to be significantly lower, up 5.5% at the midpoint as compared to 11.6% in 2022. This is due to an expected fall back in utilities and repairs and maintenance costs to flattish levels in relation to 2022.

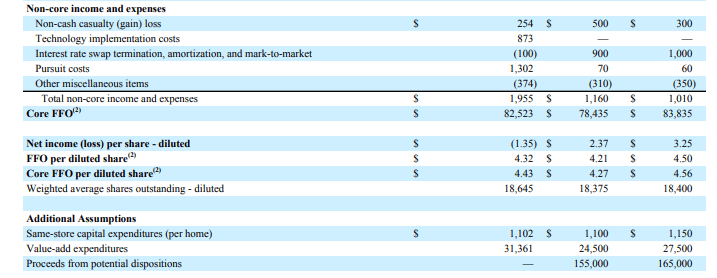

While same-store NOI is expected to be up, core FFO is expected to be flat compared to 2022, due to higher interest expense and the effects of planned dispositions.

Liquidity and Debt Profile

In 2022, total interest expense increased 12.6%, primarily due to their larger debt burden compared to the 2021 fiscal year, relating to their acquisition activity and the addition of a +$100M term loan in November.

Furthermore, approximately 21% of their debt load is variable rate, which exposes them to greater risks pertaining to volatile interest rates. This is one reason why core FFO growth is expected to be muted in 2023.

The higher variable rate exposure is also a result of the company delaying their financing plan to wait out a settling in the market rate environment. And this came just as they were becoming more active in the second half of the year, which included new acquisitions as well as additional share buybacks.

On an overall basis, their total debt to market capitalization stood at 46.3% at year end. This is up 460bps sequentially, due primarily to a lower share price. But it’s also up significantly from the end of 2021, where it stood at 28.9%. The YOY increase is due to a combination of a lower share price and higher total debt balances.

As a multiple of EBITDA, net debt stood at 8.25x for the year. This compares unfavorably to other peers within the sector.

Q4FY22 Investor Supplement - Debt Summary Metrics By Quarter

{kind=link}

Looking ahead, the company has about +$182M in commitments within the next 12 months. Additionally, they also expect to spend between +$24.5M and +$27.5M on value-add expenditures in 2023.

FY2022 Form 10-K - Summary Of Contractual Obligations

{kind=link}

At present, CSR has total liquidity of approximately +$153M. This includes availability on their revolving lines as well as existing cash on hand. In addition, they are expecting between +$155M to +$165M in disposition proceeds in 2023. The combination of the two should be sufficient to hold them over through the next 12 months.

Furthermore, they are generating between +$85M to +$90M in operating cash flows. And they have about +$127M available on their at-the-market (“ATM”) program. All considered, CSR remains in an adequate position to address their reoccurring obligations, though the effects of higher interest rates will weigh on results, given their naturally higher operating leverage.

Dividend Safety

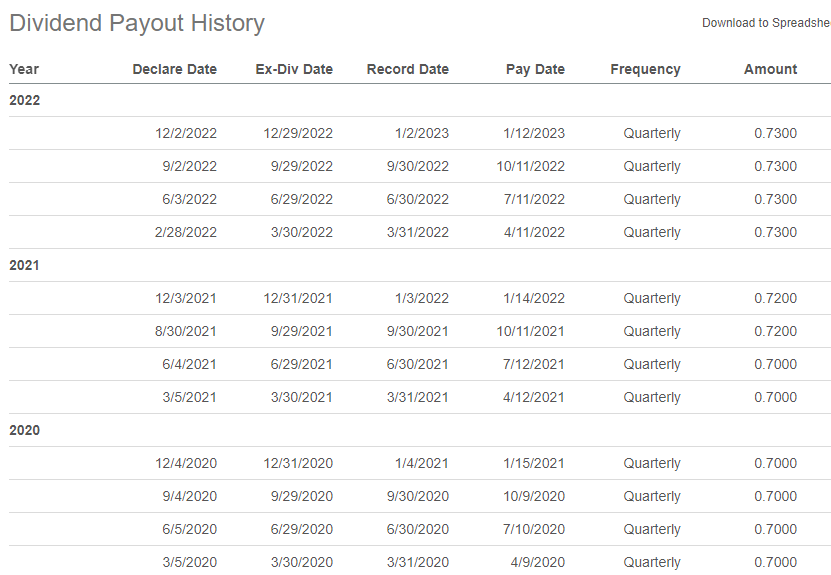

CSR currently provides a quarterly payout of $0.73/share. This is up from the $0.70/share that they were paying through the first half of 2021, after which it was increased two times to its present state.

Seeking Alpha - Recent Dividend Payout History

{kind=link}

In its current form, the payout yields about 4.65%. This is competitive to in-line with other peers within the sector. It does, however, run high in relation to their earnings potential.

On their supplemental, the payout ratio is disclosed as being in the mid-60s of core FFO. At the surface level, this appears safe and in-line with sector averages . Management also confirmed on their earnings release that the dividend is not at risk of a cut.

However, it’s worth noting that the disclosed payout levels do not account for their value-add expenditures. If one were to reduce the high-end forecast of core FFO by their expected value-add activities, then their core would come in at about $3.06/share on the high-end of estimates. On an annual payout of $2.92/share, that would bring their payout ratio to the upper 90s.

Q4FY22 Investor Supplement - Partial Summary Of FY23 Guidance

{kind=link}

Given their higher debt levels, investors should not view CSR’s dividend as sacrosanct.

Final Thoughts

CSR managed to grow FFO by 11% in 2022 on the back of strong same-store performance. And in 2023, momentum in their same-store portfolio is expected to continue. In fact, guidance of 7% to 9% NOI growth comes with expectations of 6% to 8% growth in revenues, which is notably higher than the range provided by many of their peers.

Yet, core FFO is expected to come in flat compared to 2022. Negating their strong same-store performance is higher interest expense on their high debt load. Delays in implementing their financing plan in 2022 resulted in greater variable rate dependence to fund their capital priorities. And now CSR must face the near-term costs associated with that.

Furthermore, though their dividend is fully covered at the surface level, the payout is on shakier ground when considering their value-add expenditures. Sure, these expenditures are discretionary and can always be paired back. But any scaling back on these value-add activities could, too, negatively affect earnings, which would ultimately affect coverage levels.

At 14x forward FFO, shares do offer a higher value proposition than in prior periods. And this view is reinforced via the company’s increased repurchasing activities. However, the lower multiple is justified, given their higher debt load, weak FFO growth expectations, and elevated uncertainties on the dividend. For investors seeking new initiation, CSR is one stock worth keeping on the sidelines.

For further details see:

Centerspace: Weighed Down By A Higher Interest Burden