CENTA - Central Garden & Pet: A Smart Money Stage Investment

2023-07-13 18:48:07 ET

Summary

- Its past returns, coupled with fundamental data, suggest Central Garden & Pet Company is an overlooked stock gem.

- The company's growth by acquisition strategy has provided it with a substantial market share, concurrently increasing its cost structure.

- Although Central Garden has a cyclical business model, its long-term trend growth is stellar.

- An absolute valuation model implies Central Garden & Pet Company stock is undervalued.

If you are in search of an underfollowed "value investing" opportunity, then you're in the right place, as today's analysis covers Central Garden & Pet Company ( CENT ) , which is a North American discretionary stock with immense potential. In fact, it is quite astonishing that the stock is underfollowed, as its realized returns have by far outpaced the discretionary sector as well as the broader stock market.

We last covered CENT in March, claiming it was undervalued with a seasonal uptick waiting in the wings. Although the stock has underperformed the market since our rating, we have decided to affirm our strong buy rating, as headline features suggest that Central Garden & Pet Company stock is primed for gains.

Seeking Alpha

Let's head into a deeper discussion about our most recent findings on Central Garden & Pet Company.

Operational Update

Latest Earnings

Since our latest coverage of Central Garden and Pet Company, the firm beat its second-quarter earnings estimates, delivering a quarterly revenue number of $909 million and an earnings-per-share figure of 90 cents per share. Although Central Garden and Pet's numbers were slightly softer than in the previous year's Q2 results, we have reason to believe that there's much to be optimistic about.

The basis for our positive outlook is multifactorial and is discussed throughout the article.

Firstly, investors must consider that the firm is in/approaching its peak sales season for Garden products. However, worse-than-anticipated weather in North America somewhat delayed the firm's sales numbers, which is a non-core influencing variable that might abate soon.

On the other end of the playing field, the firm's pet company performed as planned, reaching an operating profit margin of 11.6% , which is not bad if the current inflationary environment is factored into the equation.

{kind=link}

Efficiency

As illustrated in the panel data below, Central Garden & Pet Company has been on a cost-cutting spree since listing as a public company. The firm has achieved its favorable cost structure through smart acquisitions, which allow for synergies. Looking ahead, we think features such as a direct-to-consumer approach, AI integration, and strong growth from the firm's existing brand will stem further cost reduction, concurrently delivering more residual value to its consumers.

Furthermore, Central Garden's efficiency ratios improved once again during its second quarter. The firm's receivables and inventory turnover ratios both compressed, illustrating fewer delayed payments and lower inventory stockpiles. Keep in mind that global supply chains have gradually smoothened in past quarters as the initial impact of Covid-19 and the Russia-Ukraine war has diminished. Therefore, a combination of systemic influence and company-specific prowess has resulted in a more efficient operating cycle for Central Garden & Pet Company.

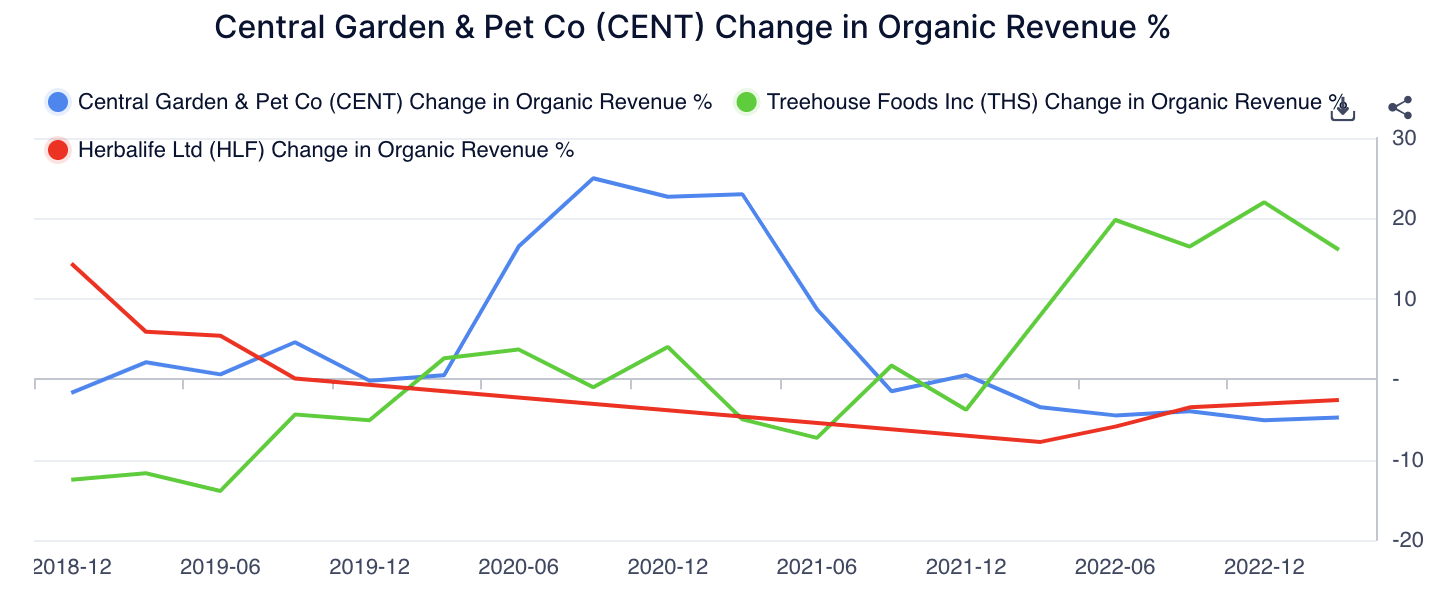

Seasonal Trends and Growing Market Share

As displayed by the revenue numbers in the diagram below, Central Garden & Pet, like its peers, is a cyclical company. Its cyclicality primarily stems from its Garden segment, which is a seasonal business that spans approximately 47.6% of the firm's revenue mix. Whether you determine this a risk or not depends on your investment horizon; in our view, long-term investors will benefit from a market that might realize long-term trend growth of 6% , whereas cyclical market timers probably need to enter a position in the stock prior to the North American summer season.

{kind=link}

Another factor worth considering is Central Garden & Pet Company's market share and how its market share might increase in the next few years. Firstly, it is worth noting that the company holds down an aggregated market share of approximately 39.15% across its two segments, suggesting that it possesses significant pricing power over its end market and bargaining power over its suppliers. Moreover, since its inception, the firm has acquired numerous entities, with recent acquisitions of Green Garden , bird feed company D&D Commodities , and garden accessory supplier Gulfstream , lending it the necessary latitude to drift away from its previous white private business model and into a synchronized branded retail model to realize additional market share and synergies.

CENT Market Shares (CSI Markets)

Valuation

Absolute Valuation

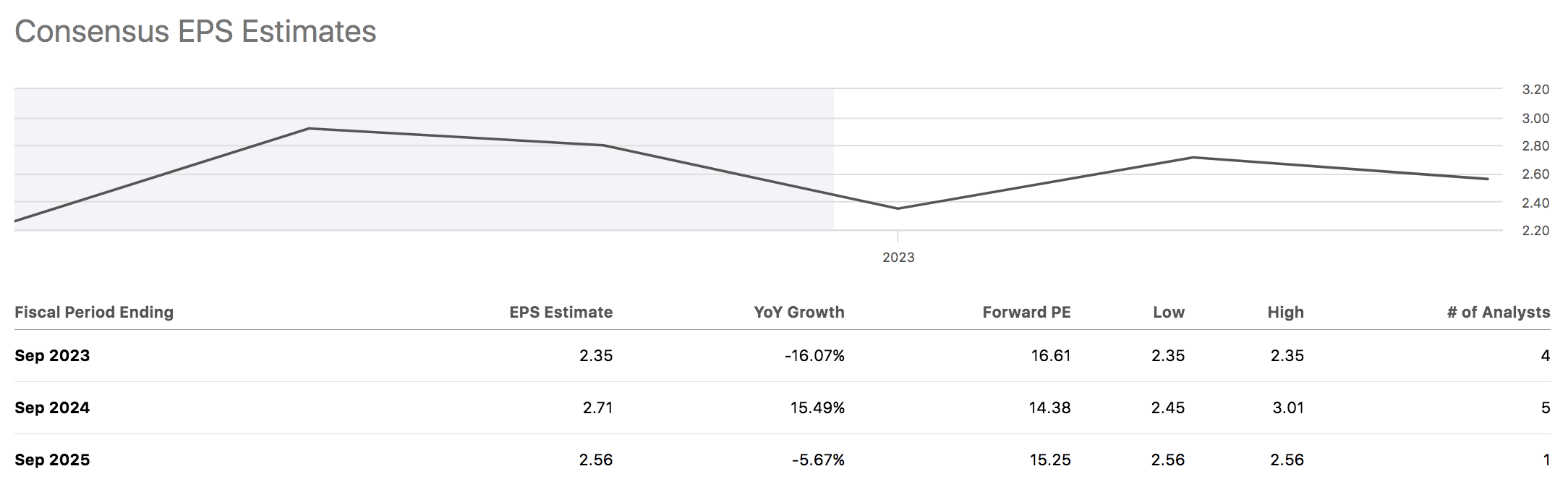

An absolute valuation of Central Garden & Pet Company stock suggests there is value in store. For example, the price-to-earnings expansion formula coupled with Seeking Alpha's databank suggests the stock has a September 2024 price target of $47.43, implying an upside potential of approximately 22%.

Although additional variables need to be looked at, the P/E expansion formula is highly touted by financial analysts and is a solid indicator of a stock's absolute valuation; below is the formula I utilized.

Formula = 5-Y average P/E multiple x Estimated EPS for September 2024 = 17.50 x $2.71 = $47.43

{kind=link}

Noteworthy Risks

As mentioned a few times during this article, Central Garden & Pet Company has a cyclical business model, meaning that, unlike long-term trend investors, short-term investors will likely be subject to systemic and idiosyncratic business cycles.

The idiosyncratic risk mentioned pertains to the company's seasonal effect, relating to its garden products, which tend to sell more comprehensively during the summer season. In addition, systemic risk is rife, as durable goods, such as the company's garden and pet accessories, remain subject to extreme volatility. Although we believe durable and consumer goods sales will improve, volatility is a risk factor that should not be neglected.

{kind=link}

Final Word

Our analysis shows that Central Garden & Pet Company stock is well-aligned with the prerequisites needed for growth. The company's continuous increases in cost-efficiency and its substantial market share can be attributed to smart acquisitions, while its stock's theoretically undervalued status is a sign of it being overlooked.

We remain positive on this stock and expect great things for the remainder of the year.

For further details see:

Central Garden & Pet: A Smart Money Stage Investment