CENTA - Central Garden & Pet Company: The Balance Sheet Is Robust

2023-03-20 04:23:59 ET

Summary

- Net sales are stagnant as Central Garden & Pet Company is too leveraged to keep on the aggressive M&A strategy.

- Profit margins, although healthy, are beginning to notice inflationary pressures.

- Very high inventory levels will allow for strong cash from operations in the coming quarters.

- The company is performing share buybacks regularly.

- The current share price decline represents a good opportunity to start averaging down.

Investment thesis

General Garden & Pet Company ( CENT ) is starting to truly feel inflationary pressures on its operations. If we add to this a reduction in volumes as a result of lower pet adoption rates after the coronavirus pandemic boost and weaker sales in the Garden business segment, we have as a result a significant drop in profit margins in the past quarter, which is starting to worry investors.

Even so, the current profit margins are still at quite healthy levels despite said headwinds, which I believe are of a temporary nature due to their direct link to the current macroeconomic context. Furthermore, very high inventories are allowing new hirings to be paused, which will certainly help stabilize profit margins and reduce inventories in order to generate strong cash from operations in the short and medium term. In addition, these inventories are similar in size to the company's long-term debt, which significantly reduces the company's risk profile.

For these reasons, I believe the current decline in the share price of ~ 38% represents a good opportunity for long-term investors with enough patience to wait for more optimistic prospects for the company as the macroeconomic context improve. But still, I think dollar cost averaging is the right approach given current headwinds and recession risks.

A brief overview of the company

General Garden & Pet Company is a major manufacturer of products for the garden and pet industries. The company was founded in 1955 and its market cap currently stands at $2 billion, employing over 6,000 workers.

Central Garden & Pet Company (Central.com)

{kind=link}

The company operates under two main business segments: Pet and Garden. Under the Pet segment, which provided 56% of the company's overall net sales in fiscal 2022, the company supplies dog and cat products, dog treats and chews, toys, pet beds and grooming products, waste management and training pads, pet containment; supplies for aquatics, small animals, reptiles and pet birds including toys, cages and habitats, bedding, food and supplements; products for equine and livestock, animal and household health and insect control products; live fish and small animals as well as outdoor cushions. All these products are sold under the Aqueon, Cadet, Comfort Zone, Farnam, Four Paws, K&H Pet Products, Kaytee, Nylabone, and Zilla brands. And under the Garden segment, which provided 44% of the company's overall net sales in fiscal 2022, the company supplies lawn and garden consumables such as grass seed, vegetable, flower and herb packet seed; wild bird feed, bird houses and other birding accessories; weed, grass, and other herbicides, insecticide and pesticide products; fertilizers and live plants. These products are sold under the Amdro, Ferry-Morse, Pennington, and Sevin brands.

The company also supplies private-label brands and third-party brands in both business segments.

Currently, shares are trading at $38.84, which represents a 38.26% decline from all-time highs of $62.91 on March 31, 2021. Personally, I consider that said drop represents a good opportunity to start averaging down as current headwinds (increased production costs, lower pet adoption rates, and growing recessionary concerns) are, in my opinion, of a temporary nature due to its direct link to the current macroeconomic context. Furthermore, the company has significantly increased its business size since 2021 thanks to one major and some minor acquisitions while accumulating inventories of a size similar to that of all its long-term debt. For this reason, and as the company has successfully operated since 1955, I consider Central Garden & Pet a company for long-term focused investors with enough patience to wait for a more positive macroeconomic context.

Recent acquisitions

Central Garden & Pet performed over 60 acquisitions since 1992, which has allowed it to increase the size of its business to become the company we know today. Next, I will make a summary of the acquisitions carried out during the past few years.

In April 2017, the company acquired K&H Manufacturing, a producer of premium pet supplies and the largest marketer of heated pet products in the country. K&H operates under the K&H and K&H Pets brands and manufactures pet products for a wide range of animals, including dogs and cats, small animals, and farm and ranch animals.

In March 2018, the company acquired Bell Nursery, the largest commercial grower of flowers and plants in the mid-Atlantic, for around $61 million. During the same year, in April 2018, it acquired General Pet Supply, a leading Midwestern U.S. supplier of pet food and supplies, for ~$24 million.

In February 2019, the company acquired the remaining 55% ownership interest in Arden Companies, a manufacturer of outdoor cushions and pillows, for $13.4 million, and used $36 million to pay the acquired company's long-term debt. Later, in May 2019, it acquired C&S Products, a manufacturer of suet and other wild bird feed products, for ~$30 million.

In January 2021, the company acquired DoMyOwn.com, a leading and fast-growing online retailer of professional-grade control products in the United States. During the same month, the company also acquired Hopewell Nursery, a leading live goods grower serving retail nurseries, landscape contractors, wholesalers, and garden centers across the Northeast. A month later, in February 2021, it acquired Green Garden, a leading provider of vegetable, herb, and flower seed packets, seed starters, and plant nutrients in North America, shipping over 250 million seed packets annually to a network of over 70,000 retail locations, for $532 million.

And the latest acquisition took place in June 2021 when the company acquired D&D Commodities, a developer, manufacturer, and provider of high-quality, premium bird feed operating under the 3D, Wild Delight, Better Bird, and L'Avian Plus brands.

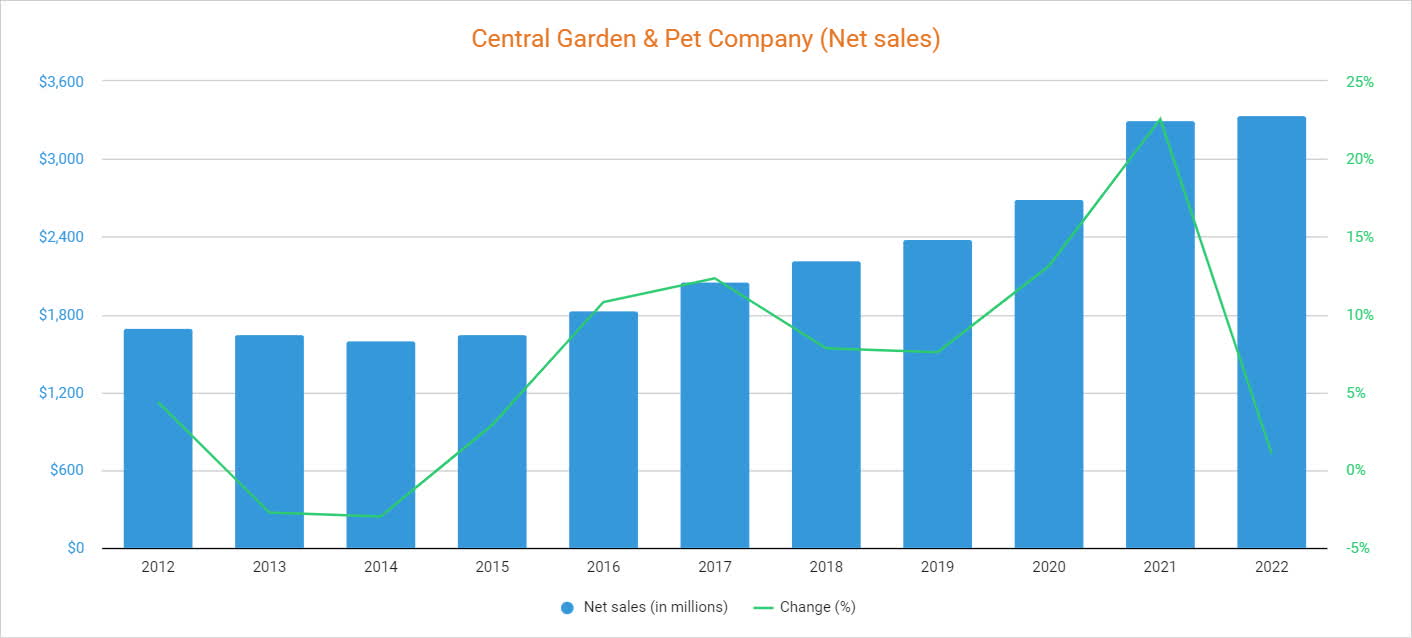

Net sales are showing signs of stagnation

Thanks to an aggressive M&A strategy, the company has managed to increase its net sales over the past few years at a relatively fast pace. Indeed, net sales increased by 22.56% in fiscal 2021, boosted by the Green Garden acquisition, after a positive fiscal 2020 thanks to higher pet adoption rates during the early stages of the coronavirus pandemic outbreak. Nevertheless, the trend has recently stabilized as declining pet adoption rates are causing a decline in demand for pet durables and the company's long-term debt is already too high to keep pace with acquisitions.

Central Garden & Pet Company net sales (10-K filings)

{kind=link}

In this regard, net sales increased by 1.06% during fiscal 2022 and declined by 5.10% year over year during the first quarter of fiscal 2023 as the company exited some low-profit private-label product lines and customer inventory levels remained high. The recent slowdown in net sales growth comes at a time when the company's ability to continue acquiring other companies has been hampered by a high debt load, with which investors should not expect growth rates similar to that of the past few years, but rather a strengthening of the balance sheet through a more conservative use of cash. In other words, the company has moved, in my opinion, from a growth stage to a deleveraging (or more moderate growth through smaller acquisitions) stage.

Due to expectations of slower growth (and even the possibility of lower net sales in a potential recessionary scenario), the share price has fallen significantly, driving the P/S ratio to the lowest range since 2016 at 0.634.

This ratio is 2.01% lower than the average of 0.647 during the past decade (due to much lower share prices prior to 2016), and 44.39% lower than the peak of 1.140 reached in the first half of 2021. But despite the weaker capacity for new acquisitions, the company keeps launching new products on a regular basis, which should help maintain the market share achieved in recent years. For example, in February 2023, it launched 40 different Plantlings Garden Starter Kits and a variety of chew toys and treats for dogs . But in addition to a debt load that must now be reduced, the company is also showing a deterioration in its profit margins as a consequence of the current inflationary pressures, which is having quite a role in the current fall in the share price.

Inflationary pressures are impacting company operations

The company has enjoyed fairly high profit margins in recent years. In this regard, gross profit margins usually danced around 30% while EBITDA margins have been close to 10%.

Inflationary pressures and lighter volumes have caused a recent decline in the trailing twelve months' gross profit and EBITDA margins to 29.22% and 9.57%, respectively, despite recent pricing actions. Actually, those profit margins are not bad at all, especially if we take into account the recent increase in costs derived from a macroeconomic context marked by strong inflationary pressures.

Nevertheless, during the past quarter, the gross profit margin of 27.4% was down 260 basis points year over year mainly due to higher production costs and lower volumes in the Garden business segment, which seems to be setting off alarm bells for the upcoming high season.

The management is currently undertaking short-term cost cuts in order to keep margins healthy while improving the company's cost structure in the long term. In fact, some of this is already taking place in light of recent investments in process automation and the pause in hiring new staff. Still, margins are expected to be lower than usual for as long as current inflationary pressures remain part of the macroeconomic context. Furthermore, a potential recession would likely affect volumes negatively, which would certainly have a direct impact on profit margins due to unabsorbed workforce.

A new deleveraging phase has just begun

Long-term debt has increased significantly from fiscal 2017 to fiscal 2022 as a consequence of a pace of acquisitions that seems unsustainable in the long term. During this period, long-term debt has tripled to $1.19 billion.

Recent inflationary pressures, along with a sharp increase in inventories, caused the trailing twelve months' cash from operations to plunge into negative territory at $-4.87 million. Specifically, that fall in cash generation is because inventories increased by $179.5 million during the past twelve months, and accounts payable declined by $50.6 million while accounts receivable only declined by $14.6 million. This has caused a decline in cash and equivalents from $296 million a year ago to $88 million during the past quarter as the company has accumulated inventories to record-high levels.

But now, the need to use these resources to reduce the company's debt pile becomes clear when looking at the rising trailing twelve months' interest expense, which has more than doubled since 2018 to $57 million per year.

Furthermore, capital expenditures have increased by 86.31% in fiscal 2021 to $80.3 million, and by another 43.46% in fiscal 2022 to $115.2 million as the management invested cash for capacity expansion and automation, but are stabilizing as they declined by 27% year over year during the first quarter of fiscal 2023. It's important to point out that capital expenditures are expected to remain higher than in the past few years due to the increase in the size of the company's business after the major acquisition of Green Garden in early 2021.

During the Q1 2023 earnings call conference, the management stated that converting part of the inventory levels of $1.02 billion into cash is one of the current priorities to maintain strong cash from operations, for which a pause on hiring is currently being adopted. Considering that the long-term debt is at similar levels at $1.18 billion, it does not pose too significant a risk thanks to current inventories. Still, low cash and equivalents of $87.80 million carry the risk that if inflationary pressures last longer than expected or recessionary risks materialize, the company may have to draw on such inventories to offset a potential drop in profit margins, rather than using them to pay off debt or acquire new companies to make it more manageable.

Share buybacks are increasing the position of investors passively

The management has performed share buybacks (more or less) steadily since fiscal 2019, and thanks to that, the number of shares outstanding has decreased by 6.57% since then. The latest announcement took place in August 2021 when the company announced a share repurchase program of up to $100 million and authorized supplemental purchases. As for the past quarter, the company repurchased $9 million worth of shares, so the share buyback efforts remain in effect to this day.

This means that investor positions represent an ever-increasing portion of the company as fewer shares are outstanding, leading to improved per-share metrics. Since the company does not pay dividends, it appears that the management is currently opting to reward shareholders through this more flexible type of payout .

Risks worth mentioning

Although it is true that the company's risk profile is, in my opinion, low thanks to very high inventories and profit margins that remain sufficiently stable considering the complexity of the current macroeconomic context marked by high inflationary pressures, there are certain risks that I would like to highlight.

- Profit margins could continue to be negatively affected if inflationary pressures continue to be part of the current macroeconomic context for much longer, which would lead to difficulties in generating enough cash from operations to sustain interest expenses and capital expenditures through operations themselves in the short to medium term, having the company to make use of inventories to offset the impact.

- High customer inventories also pose a risk to the company, which also has unusually high inventory levels. This could cause difficulties in the short and medium term to empty inventories, with which it could be forced to do so at lower product prices, leading to weakening profit margins.

- Faced with growing fears of a potential recession due to recent interest rate hikes in order to mitigate high inflation rates, consumers could opt for private labels over branded products, which could produce a reduction in the company's profit margins. Also, the increased cost of living is causing a decrease in the purchasing power of consumers.

- If a recession does finally materialize, the company could see its volumes drop significantly, leading to lower profit margins as a result of unabsorbed workforce.

Conclusion

If we take into account the complexity of the current macroeconomic context, which is marked by strong inflationary pressures, we could say that Central Garden & Pet is performing quite well today despite current headwinds. The company's profit margins, although below normal, remain at quite healthy levels, which is allowing the company to remain profitable (despite the recent cash from operations drop due to increasing inventories and declining accounts payable). Furthermore, I believe that the current pause in the hiring of new workers will allow a successful reduction in the currently inflated inventories, as well as pave the way for a possible recession in the medium term, where the company could face a significant reduction in volumes.

For these reasons, in addition to inventories of a size similar to the company's total long-term debt, I believe that this is a good time to acquire Central Garden & Pet shares and take advantage of the recent share price decline. But despite that, current risks (especially the risk of further inflationary pressures or a recession materializing) suggest that a wise approach would be to average down from current share prices.

For further details see:

Central Garden & Pet Company: The Balance Sheet Is Robust