CENTA - Central Garden & Pet: Strong Buy Maintained On Better Profit Estimates For 2024

2023-11-30 13:45:00 ET

Summary

- Central Garden & Pet Company's significant market share, paired with a growth-by-acquisition strategy, could lead to secular growth.

- The company exceeded estimates in its fourth quarter However, the market has yet to price in recent earnings results.

- A work-in-progress and raw material inventory pile-up spells higher anticipated product demand.

- Central Garden & Pet Company's key financial metrics are robust, and various valuation metrics imply the stock is grossly undervalued.

Central Garden & Pet Company ( CENT ) is a stock we've covered extensively on Seeking Alpha. The company presents a compelling, high-quality small/mid-cap opportunity with various tailwinds in store.

However, despite its potential, short-term headwinds such as waning consumer sentiment and structural setbacks have dented Central Garden & Pet's ordinary shares' recent progress.

Today's article serves as an update on our outlook for Central Garden & Pet, whereby material events that have unfolded since our latest coverage are discussed.

Without further delay, let's traverse into the main part of the analysis.

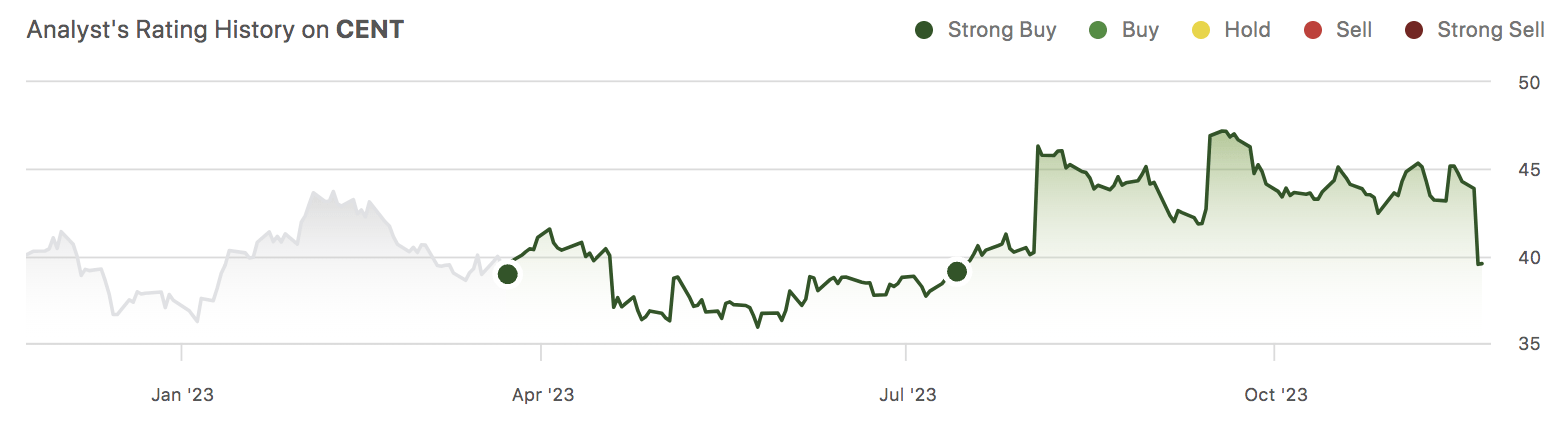

Pearl Gray Equity and Research Historical CENT Stock Ratings (Seeking Alpha)

{kind=link}

Earnings Review and Operational Updates

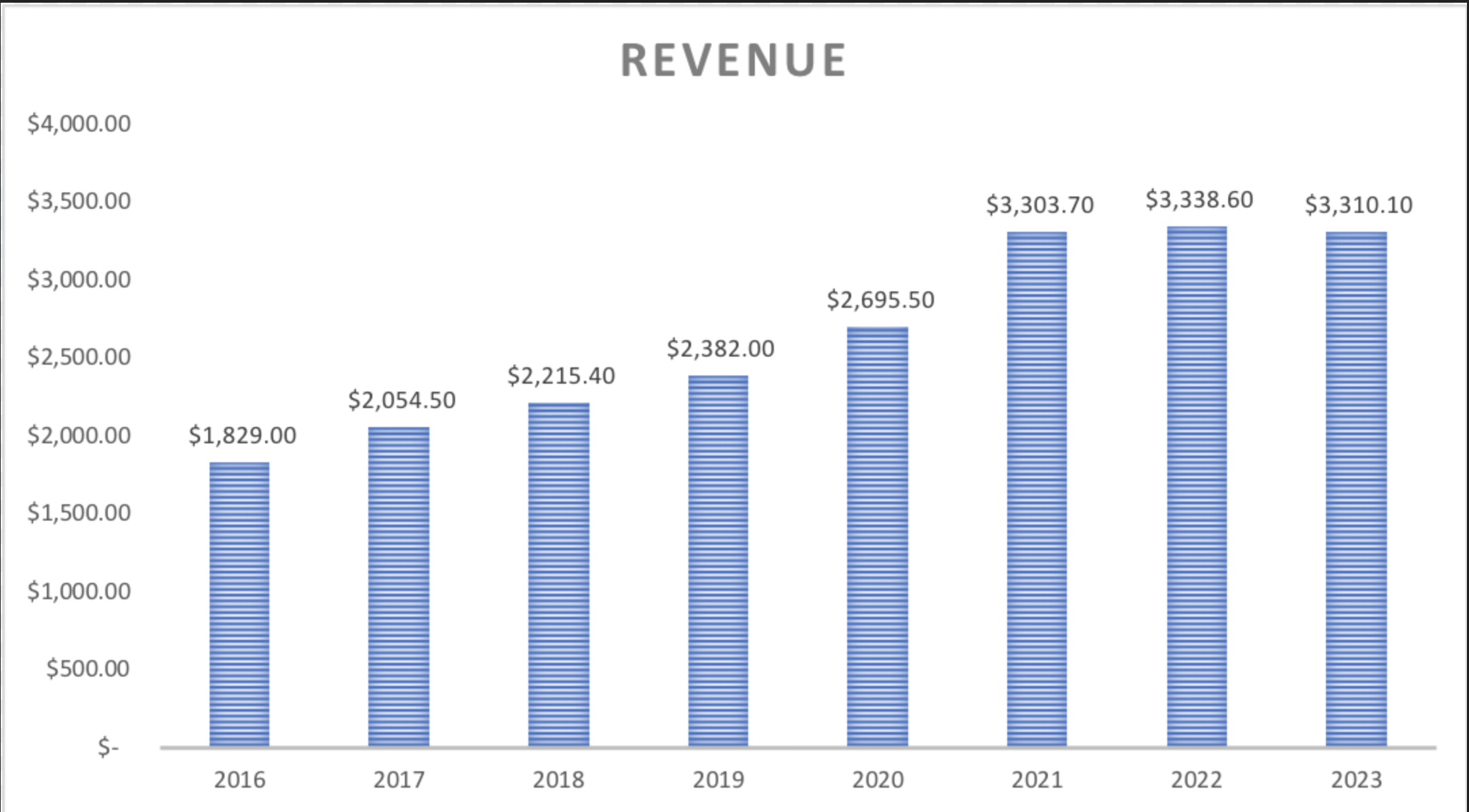

Central Garden & Pet released its fourth quarter and full-year fiscal earnings report earlier this month, revealing $750 million in quarterly revenue and $3.3 billion in full-year revenue, eclipsing estimates. Moreover, the firm achieved quarterly earnings per share of ten cents and $2.59 apiece (non-GAAP adjusted).

Central Garden & Pet's short-term growth is holding up well, which is quite impressive if you consider that many consumer product companies have waned since the interest rate cycle started peaking. Moreover, the firm is experiencing solid long-term growth. In our view, long-term growth will be sustained for as long as the U.S.'s real GDP is positive, and the firm holds down (or expands on) its approximated 35.97% market share.

($ millions) (Author's Work, Data from Seeking Alpha)

{kind=link}

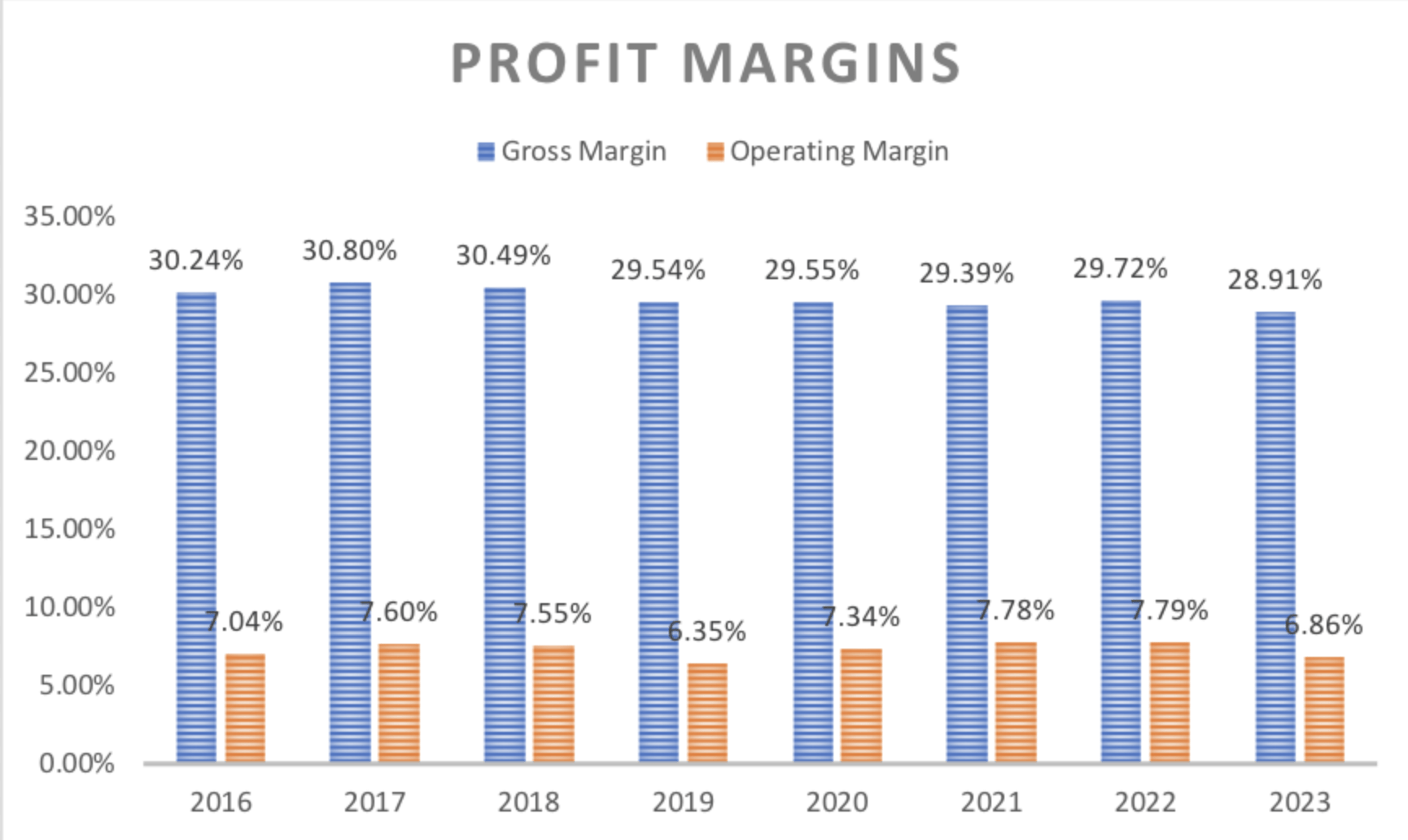

Central Garden & Pet's profit margins have decayed year over year. Systemically higher input costs definitely impacted the firm's margins in the past year. However, upstream inflation relating to wages and materials is fading, which could result in higher margins in 2024. Moreover, we believe Central Garden & Pet's long-term cost base will drop due to tech integration. Approximately 25% of the firm's sales are online, with data-driven procurement and consumer targeting playing into its technology infrastructure as well.

Author's Work, Data from Seeking Alpha

{kind=link}

Another event that occurred in Central Garden and Pet's fourth quarter was the company's acquisition of TDBBS from alternative investment firm Bregal Partners. Although comprehensive details about the deal are yet to be released, the acquisition forms part of Central Garden & Pet's growth-by-acquisition model.

The DIY garden and pet market is set to assume a compound growth of 5.4% per year until 2028 , which is very respectable. However, internal growth can be slow to achieve at times. Therefore, Central Garden & Pet's growth-by-acquisition strategy provides an accelerated approach to obtaining additional market share.

In summary, we think Central Garden & Pet's latest earnings results were within range of what most (including us) expected. And, in our opinion, input cost relief paired with sustained trend growth may lead Central Garden & Pet to new heights in 2024.

CENT's Historical Earnings Hits and Misses (Seeking Alpha)

{kind=link}

Key Metrics To Look Out For

The first key metric I want to point out is Central Garden & Pet's inventory breakdown. Although the figures need to be adjusted for inflation, it's evident that raw materials costs have climbed. Although the line items' increases can be due to numerous reasons, retailers tend to experience higher WIP and raw materials whenever they see demand rising. As such, it's definitely a factor to consider if you're a fundamentalist.

Inventory Breakdown (Central Garden and Pet)

{kind=link}

Furthermore, Central Garden & Pet's balance sheet is robust, which is critical in today's interest rate environment as high charges on liabilities are upending many retail stocks due to investors attaching excess solvency risk to them.

Let's add some data to the aforementioned. Central Garden & Pet's quick ratio of 1.79x shows that its short-term assets (less inventory) outweigh its short-term liabilities. In addition, the firm has an interest coverage ratio of 3.913x, illustrating that its accrual income succeeds contractual debt obligations with relative ease.

Finally, a look at the firm's return on equity, return on invested capital, and sustainable growth rate sets the tone for the valuation section.

Central Garden & Pet's return on invested capital of 4.72% isn't blockbuster status, but it's solid for a retailer. A good ROIC is indicative of a firm's competitive advantage as it shows that it doesn't need to overspend to achieve market share (and, in turn, profitability).

Further, Central Garden & Pet's return on equity shows that investors receive good residual value from the stock. ROE is a parsimonious indication of a sustainable growth rate for non-dividend-paying stocks , and I don't know about you, but a sustainable growth rate above 8% sounds good to me.

Valuation and Pairs Analysis

Sample data and the P/E expansion formula were used to manufacture a price target for Central Garden & Pet, which showed that the stock is undervalued by about 15%. Although the modeling technique is slightly simplified and merely an indicator, it provides a solid headline indicator to pair with the fact that most of Central Garden & Pet's salient price multiples are at five-year discounts .

Author's Work, Data from Seeking Alpha

{kind=link}

Furthermore, a peer analysis communicates technical value. A peer-based analysis shows that Central Garden & Pet stock has underperformed the consumer discretionary sub-sector this year. Perhaps more importantly, Central Garden & Pet has underperformed close peers such as Spectrum Brands Holdings, Inc. ( SPB ) and The Scotts Miracle-Gro Company ( SMG ).

To our knowledge, there have not been any structural breaks within Central Garden & Pet to suggest justified underperformance. Thus, a strong case exists that Central Garden & Pet presents a relative value arbitrage opportunity going into 2024.

Risks

I outlined a few risks within the earlier text. However, let's look at a few more to balance the argument.

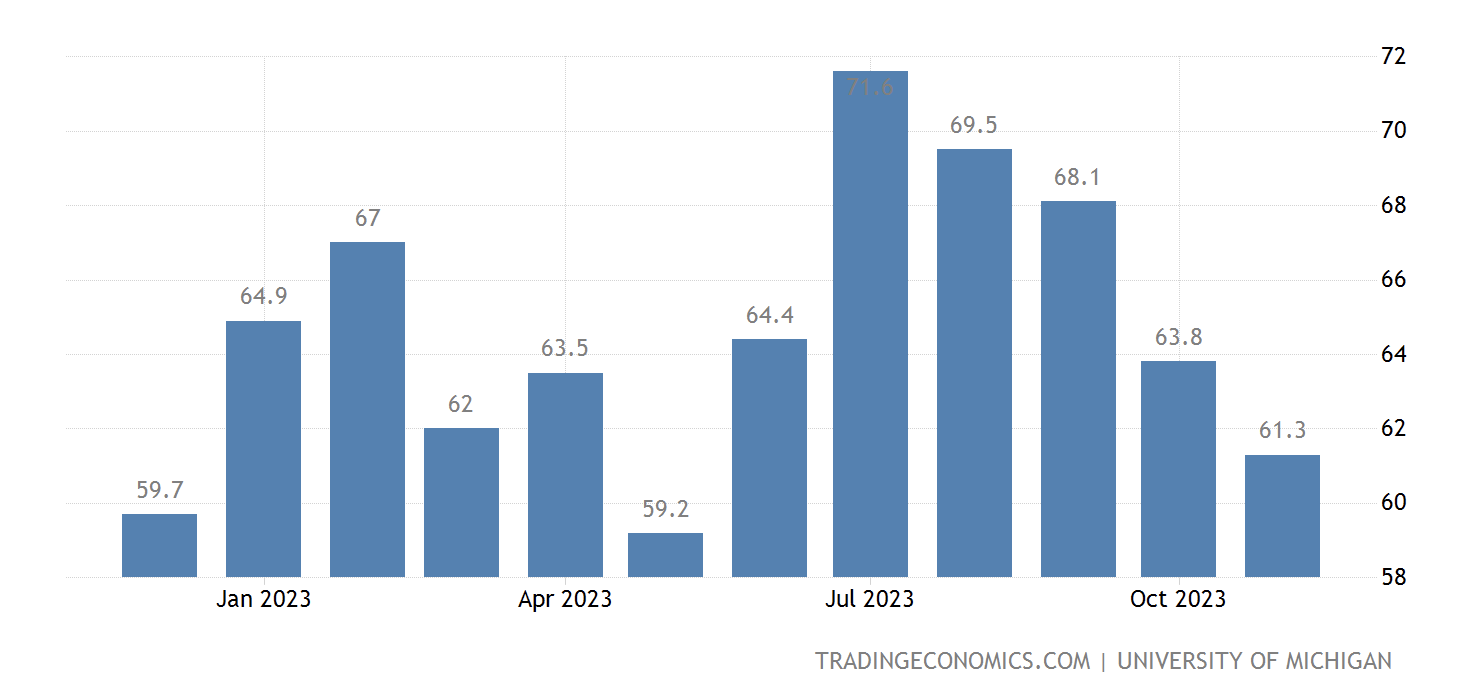

Firstly, the U.S. consumer sentiment indicator is in bad shape. Consumers have succumbed to sustained interest rate pressure and the natural softening of the economic cycle. As such, a case exists that discretionary stocks such as Central Garden & Pet may feel the heat from systemic factors in 2024.

Michigan Consumer Sentiment Index (Trading Economics, University of Michigan)

{kind=link}

Another noteworthy factor to consider is Central Garden & Pet's profit margins. As mentioned earlier in the article, we think profit margins will improve in coming years due to softer economy-wide upstream production costs paired with technological innovation. However, Central Garden & Pet's profit margins are razor-thin at times, which could upend the stock if sustained.

Side note: The following chart was inserted earlier in the article, but I added it again for readers' convenience.

Author's Work, Data from Seeking Alpha

{kind=link}

Lastly, as illustrated in the following diagram, Central Garden & Pet stock has a value-at-risk metric that's roughly 2.75x higher than the SPDR S&P 500 ETF Trust's ( SPY ), suggesting that the stock possesses significant tail risk and may hurt most portfolios in the event of a broad-based market drawdown.

{kind=link}

Final Word

Central Garden & Pet Company's stock is well positioned. The firm's cost base looks set to cool down while market share-driven sales growth will likely be sustained.

Although waning consumer sentiment is of concern, the firm's past results show that it's resilient during times of economic stress. More importantly, conscious efforts are being made to increase market participation and lower costs.

Lastly, absolute, relative, and technical pricing metrics imply Central Garden & Pet is undervalued and ready to hit new heights in 2024.

Consensus: Strong Buy Rating Maintained.

For further details see:

Central Garden & Pet: Strong Buy Maintained On Better Profit Estimates For 2024