CENT - Central Garden & Pet: Undervalued With A Seasonal Uptick En Route

2023-03-23 12:16:38 ET

Summary

- Central Garden & Pet Company's stock is an overlooked cyclical pick trading at a deep discount.

- With everything else constant, historical data suggests that the company's gardening sales are set to surge.

- Factors like lower inflation, streamlined stock-keeping units, and an enhanced omnichannel retail model are all set to contribute.

- Although dividends remain astray, the stock's price multiples reveal that it is at a deep discount relative to its cyclical average. Moreover, a peer-based analysis implies that the stock is undervalued.

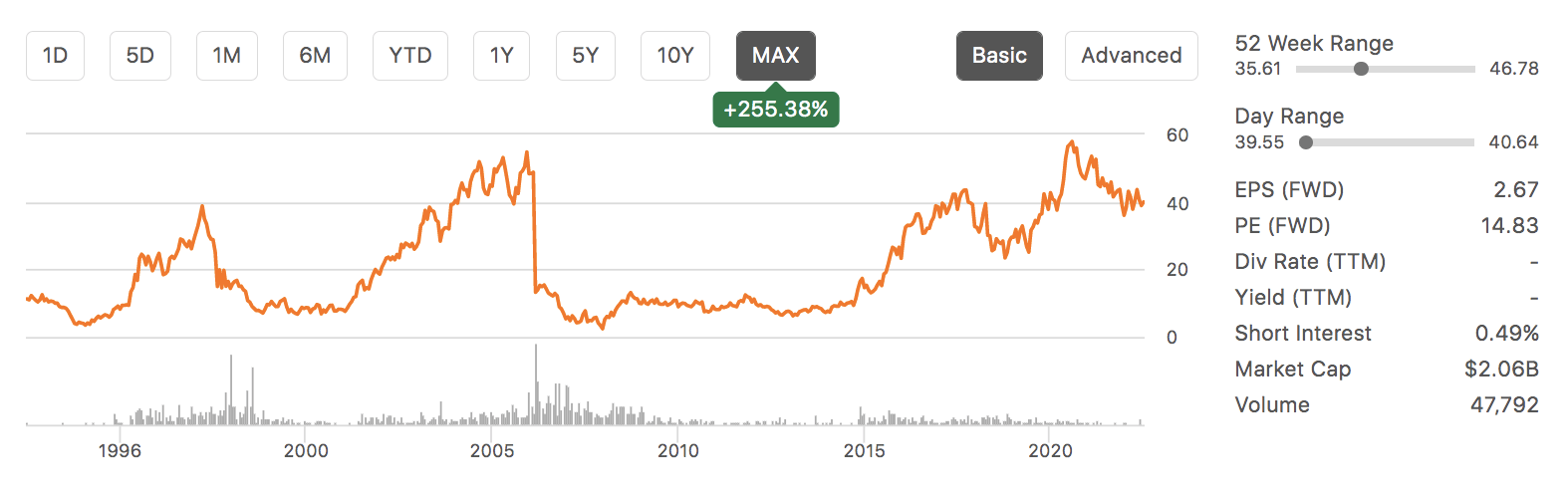

In our view, Central Garden & Pet Company ( CENT ) falls into the same bracket as ACCO Brands Corporation ( ACCO ) , which we recently covered on Seeking Alpha. As with ACCO Brands, Central Garden & Pet has suffered a staggering year-over-year drawdown as its business has succumbed to a cyclical downturn. Moreover, Central Garden & Pet's stock has shed nearly 15% in the past year as investors refrained from betting on cyclical stocks during 2022's bear market.

CENT's Realized Returns (Seeking Alpha)

{kind=link}

Despite Central Garden & Pet's recent misfortunes, we believe its stock provides investors with an excellent cyclical value opportunity that should not be overlooked; here is why.

A Cyclical Inflection Point?

Central Garden & Pet Company's latest earnings report communicates its sensitivity to the economic cycle. In addition, the company sells seasonal products, which tends to result in slower winter sales.

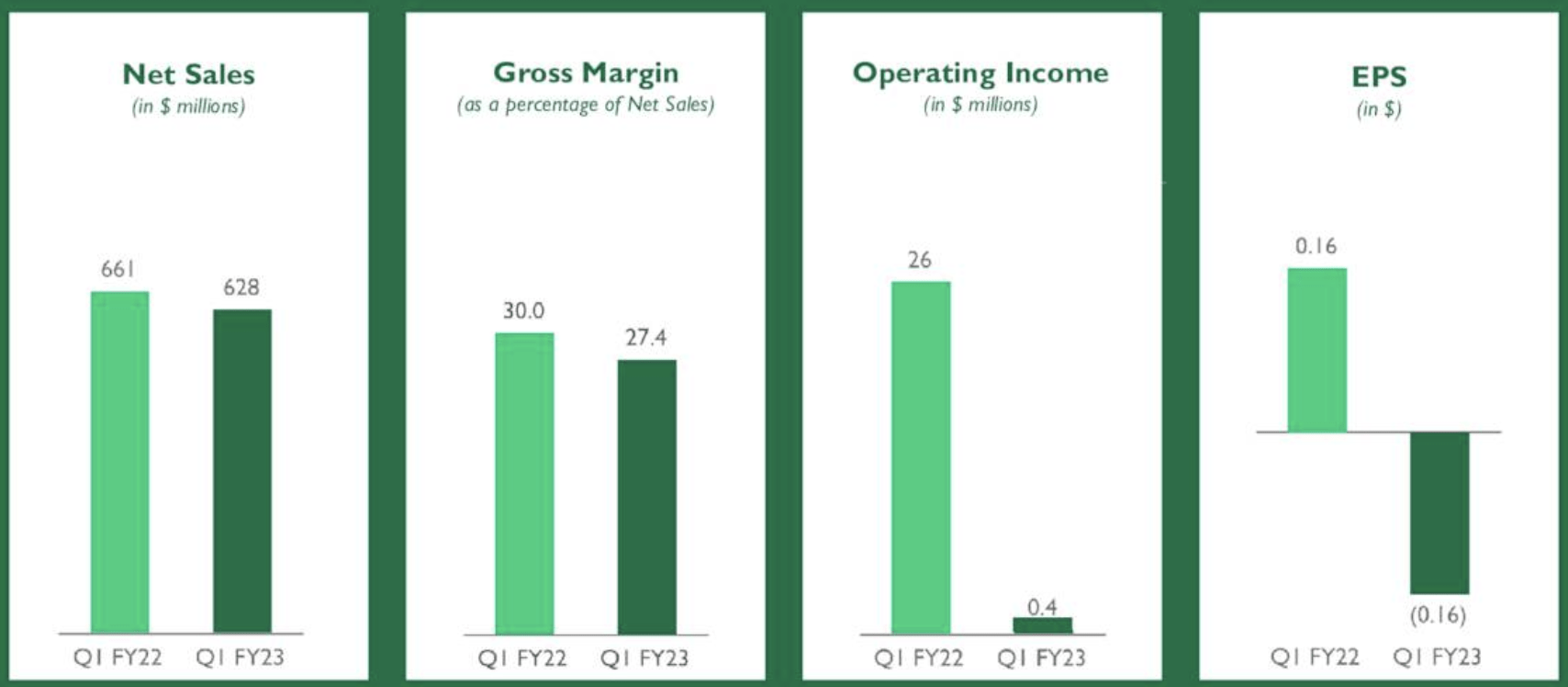

The firm's quarterly net sales decreased year-over-year, which its management attributes to a softening economy and business restructurings.

{kind=link}

As embodied by its name, Central Garden & Pet operates two segments: Pet and Garden.

Pet Segment

Starting with the Pet segment. The firm suffered from a 5% year-over-year top-line drawdown as post Covid new pet ownership has continued to decline. Moreover, the company is phasing out various private-label products in an attempt to improve its future profit margins.

Furthermore, the segment's costs rose dramatically during 2022 and early 2023, which was a uniform phenomenon among businesses amid multiyear high inflation. In our view, the firm's elevated costs will taper due to the gradual easing of inflation in the U.S. coupled with Central Garden & Pet's streamlining of stock-keeping units and continued digitalization of supply lines. Additionally, a softer labor market might stagnate wage demands.

Lastly, a noteworthy mention is that the segment's sales mix continues to shift online, with eCommerce now spanning 23% of the business unit's revenue mix. This provides two benefits: 1) An omnichannel business model, which allows for a personalized consumer experience, and 2) Less reliance on sporadic retailer purchases, which is likely to smoothen the company's gross margins.

Garden Segment

The enterprise's garden segment provides an interesting topic of discussion as it hosts a seasonality effect. For example, historically speaking, Central Garden & Pet's first-quarter garden sales usually constitute 15% of the business unit's annual revenue.

The Northern Hemisphere's gardening season usually starts in mid-March , meaning a cyclical increase in sales for Central Garden & Pet is probably en route. Nevertheless, it must be considered that consumers are growing increasingly worried about the global economic outlook, meaning that non-essential goods such as garden supplies might suffer from softer demand than usual. However, we anticipate a net increase in sales in the firm's second quarter.

A key consideration regarding the company's long-term garden sales is its emphasis on its point-of-sale strategy, which has proliferated by 30% in the past year. Leveraging modern retail techniques like POS and leaner stock-keeping units might do the trick for Central Garden & Pet, consequently allowing it to pass down residual value to its stockholders.

Efficiency Metrics

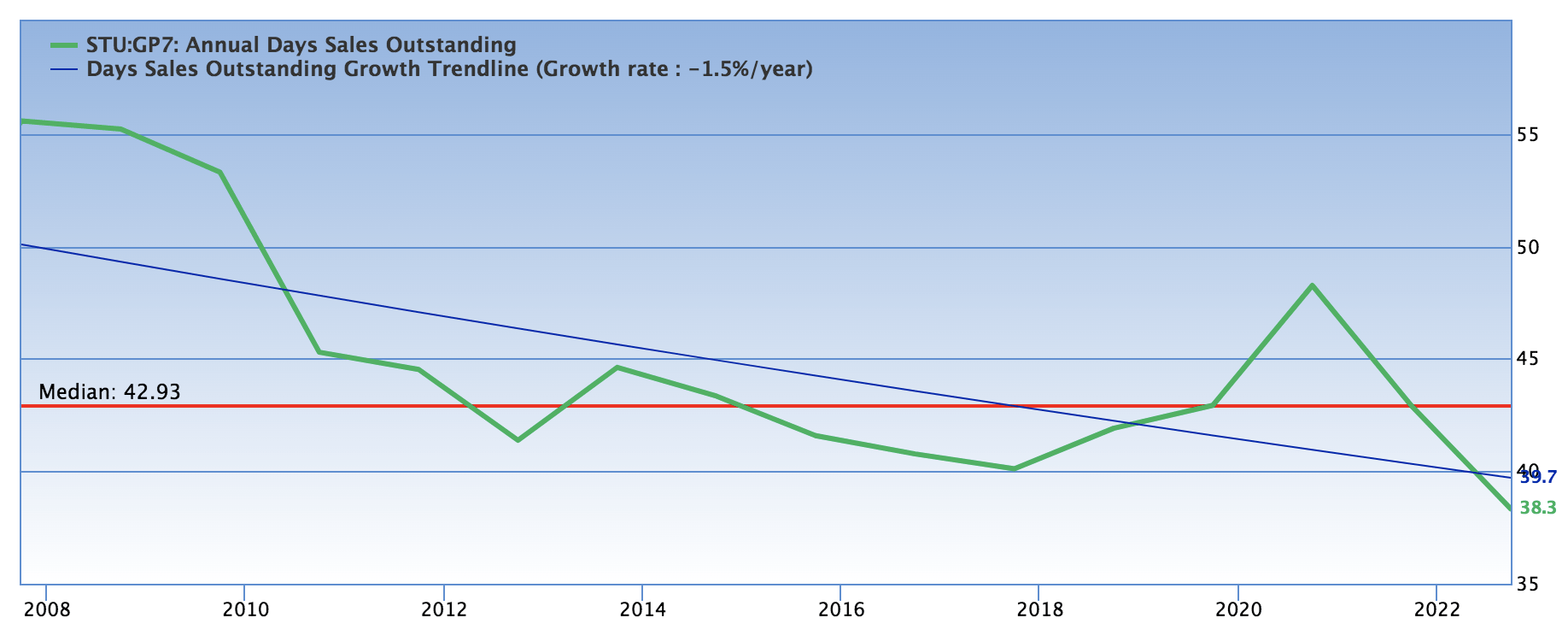

The past few years have been a bumpy ride for inventory-heavy businesses like Central Garden & Pet because of congested supply chains and elevated inflation. Nonetheless, the long-term trendlines of Central Garden & Pet's efficiency ratios should provide a sense of encouragement to us analysts and the firm's investors alike.

Firstly, Central Garden & Pet's days of sales outstanding ratio's trendline is downward sloping, meaning its capital efficiency and risk of uncollectible payments are both improving. This doesn't only provide a better credit outlook but also enhances the firm's working capital efficiency.

{kind=link}

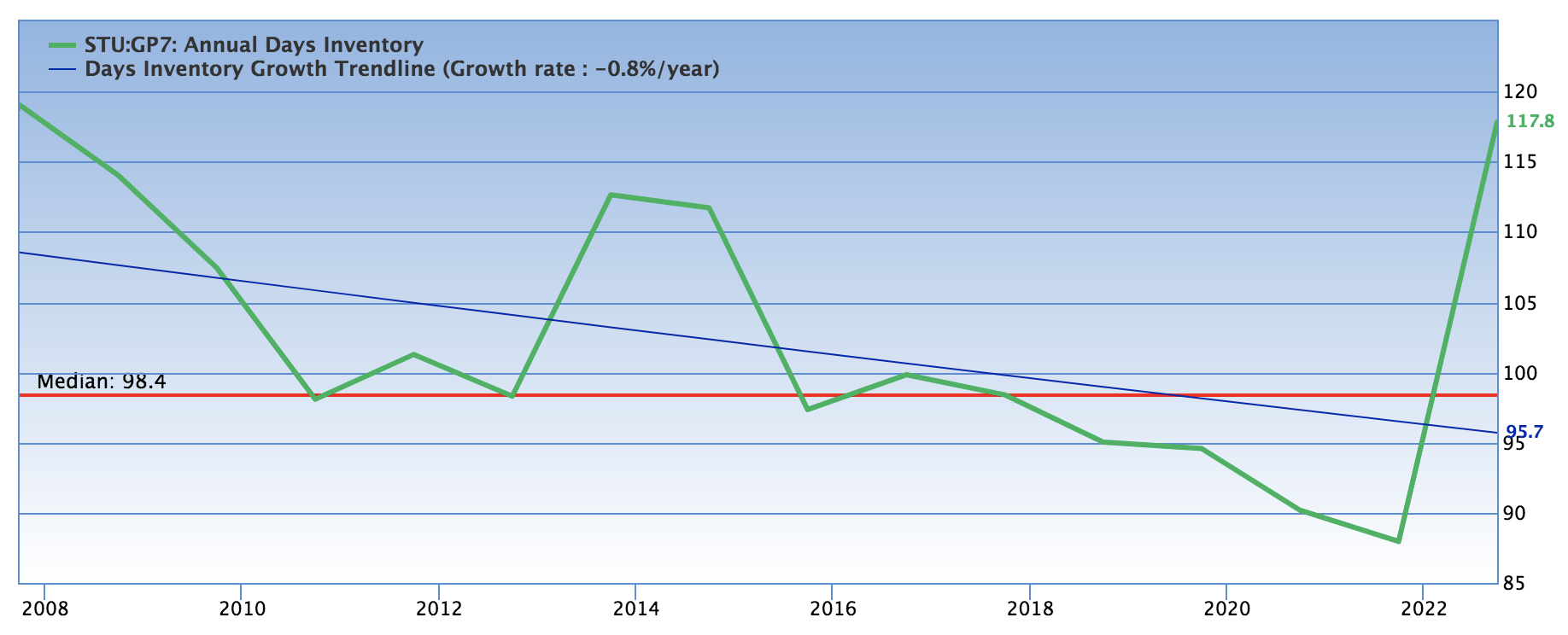

Another area worth considering is the company's improving days of inventory on hand, communicating the success that its omnichannel and streamlined SKU strategy is yielding. Even though Central Garden & Pet experienced an uptick in 2022, the effects were systemic, and we anticipate a reversion to its downward-sloping simple moving average as supply lines normalize.

{kind=link}

Valuation

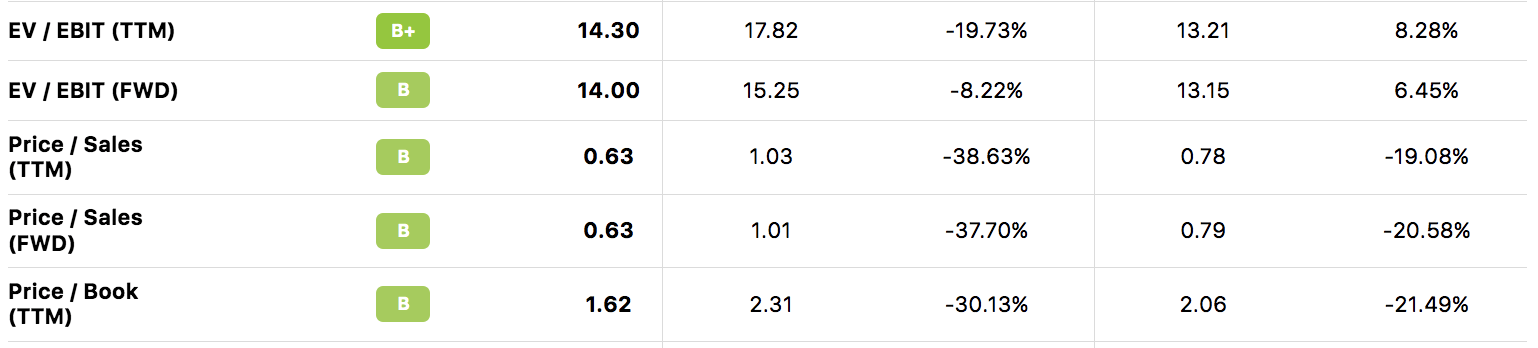

In light of the fact that our argument centers on cyclicality, we decided that Central Garden & Pet should be valued on a relative basis. As displayed in the diagram below, and as can be corroborated via this link , most of the firm's price multiples are discounts to their 5-year cyclical averages. Additionally, most of the stock's ratios are at a discount relative to Central Garden & Pet's sector peers. Thus, we deem Central Garden & Pet's stock relatively undervalued.

{kind=link}

Noteworthy Risks

We believe that the primary identifiable risk pertaining to Central Garden & Pet is related to economic tail risk. Based on recent events such as the SVB Financial Group's ( SIVB ) collapse and Credit Suisse's ( CS ) credit event , fears of a pending banking crisis cannot be overlooked. If such an event had to occur, cyclical stocks, including Central Garden & Pet, would likely shed value.

Furthermore, despite its relatively mature status and average cash from operations exceeding $161 million , Central Garden & Pet's stock does not pay a dividend. In our opinion, this company should be paying a dividend, and a failure to do so might cause agent-principle conflict.

Final Word

Our analysis shows that Central Garden & Pet Company's stock is at a cyclical discount. Our premise is that an operational inflection point is near amid smoothening supply chains and a pending gardening season. In addition, the firm is cutting costs via its leaner stock-keeping units and well-implemented omnichannel model.

Furthermore, key metrics suggest the stock is at a cyclical discount relative to its own historical price and its sector peers. Thus, we have decided to assign a strong buy rating to Central Garden & Pet Company.

For further details see:

Central Garden & Pet: Undervalued With A Seasonal Uptick En Route