CENT - Central Garden & Pet: Underwhelming Financials Lack Of Growth Not Appealing

2023-10-06 16:42:19 ET

Summary

- Central Garden & Pet Company's financials show steady performance, but lack of growth and margin improvements are underwhelming.

- The company has a decent amount of debt, but its historical interest coverage ratio suggests no risk of insolvency.

- The company's current ratio is strong but not efficient, possibly indicating underutilization of assets. Many financials are stable but could be improved.

Investment Thesis

I wanted to take a look at Central Garden & Pet Company's ( CENT ) financials before the company reports its full-year results in November. The company seems to be chugging along steadily, which is not a bad sign, but also a little underwhelming. Because of the lack of growth estimated and no improvements in margins, I give the company a hold rating until we see an uptrend develop.

Briefly on the Company

CENT is a company that produces and sells many different products relating to the garden and lawn areas. It also sells products relating to pets. The pet segment sells cat and dog supplies such as treats and chews, pet beds, and grooming products, while the garden segment provides seeds, bird feed, plants, and fertilizers.

Financials

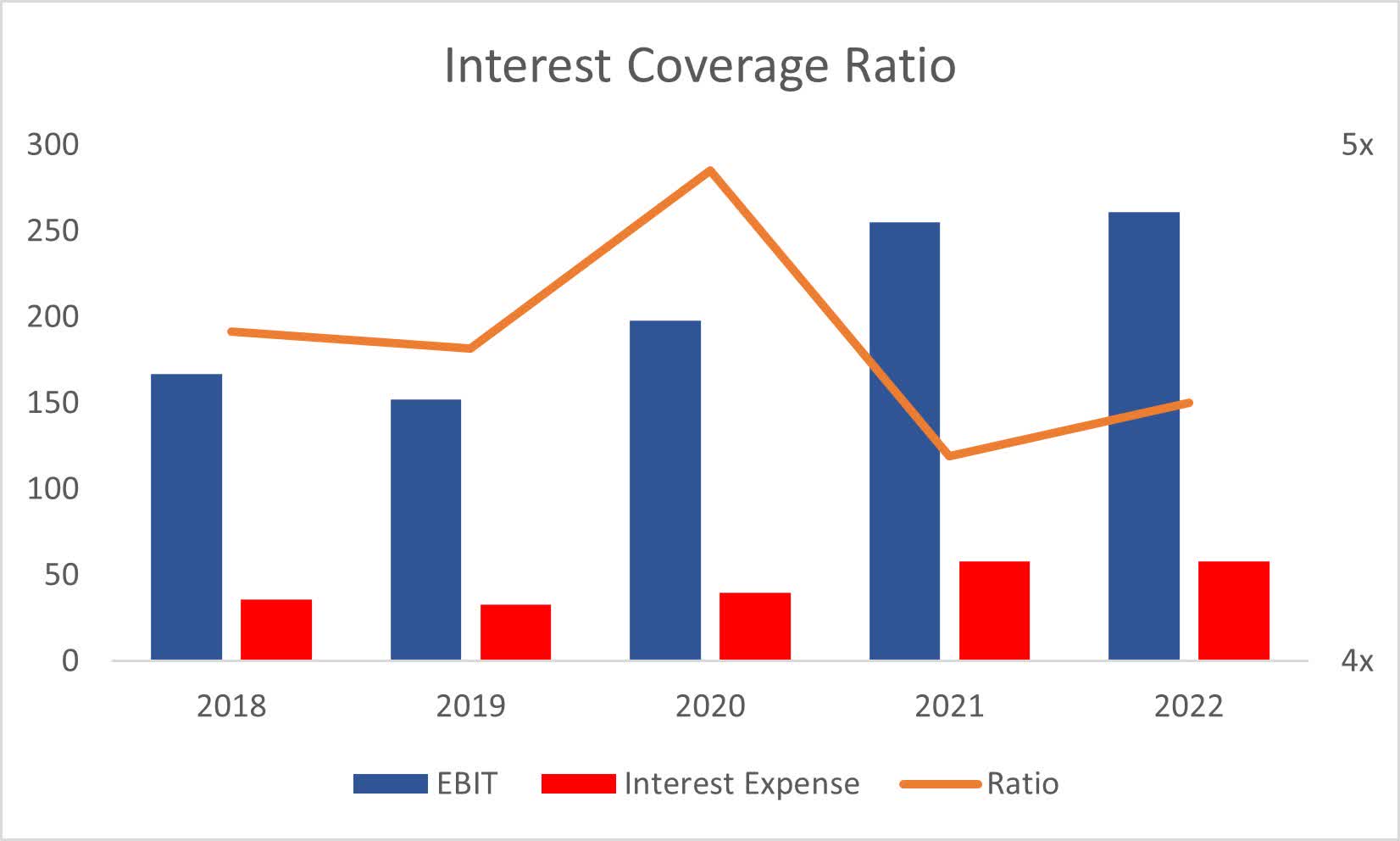

As of Q3 '23, the company had $333m in cash and equivalents against around $1.2B in long-term debt. For a company that has a little over $2B market cap, that is a decent amount of debt, which would deter many investors as soon as they see that number. Is it worrisome? Well, the company's historical interest coverage ratio has been around 5x for the last 5 years, which is right at the minimum I look for in a company. This means that EBIT can cover annual interest expense on debt around 5 times over. Many analysts look for at least a 2x coverage ratio, which is considered healthy. I like to look for around 5x because I want to be more conservative. It's safe to say the company is at no risk of insolvency in my opinion.

{kind=link}

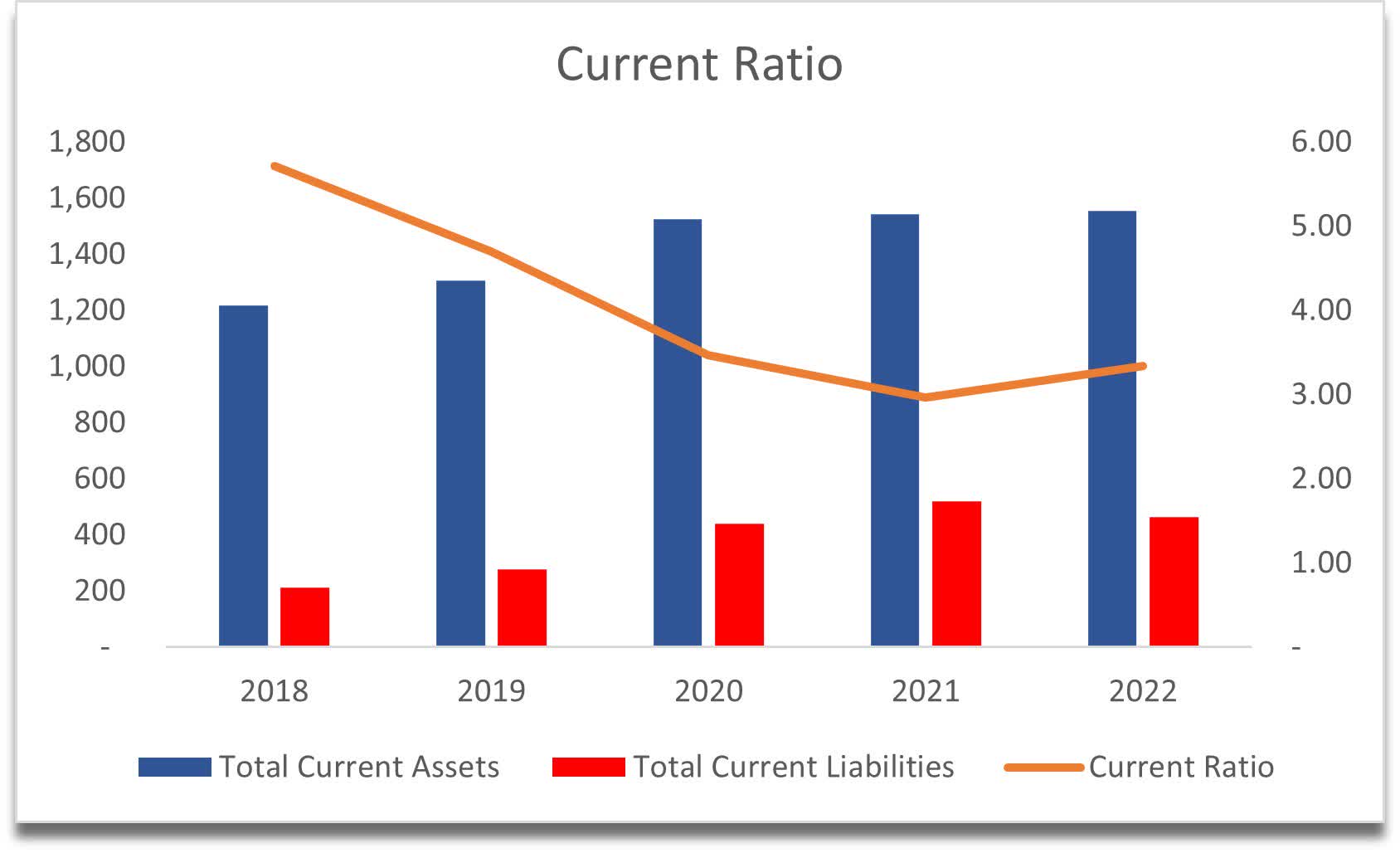

The company's current ratio is very strong and has been stronger in previous years. In my opinion, the ratio is a little too strong, to the point where it is not efficient. This tells us that the management isn't utilizing the company's available assets fully, like hoarding cash instead of using it to further the company's growth, or having too much inventory, which is costing the company its cash flow and profits. It also leads to increased storage and holding costs, which lowers the company's cash flow. Inventory increased by around 37% from FY21 to FY22, which is quite above the company's historical average. In short, the high current ratio is good because it means the company can easily pay off its short-term obligations, but it is also not efficient because the company is not proactive with its assets to further the growth of the company. What I consider to be an efficient ratio is in the range of 1.5-2.0.

{kind=link}

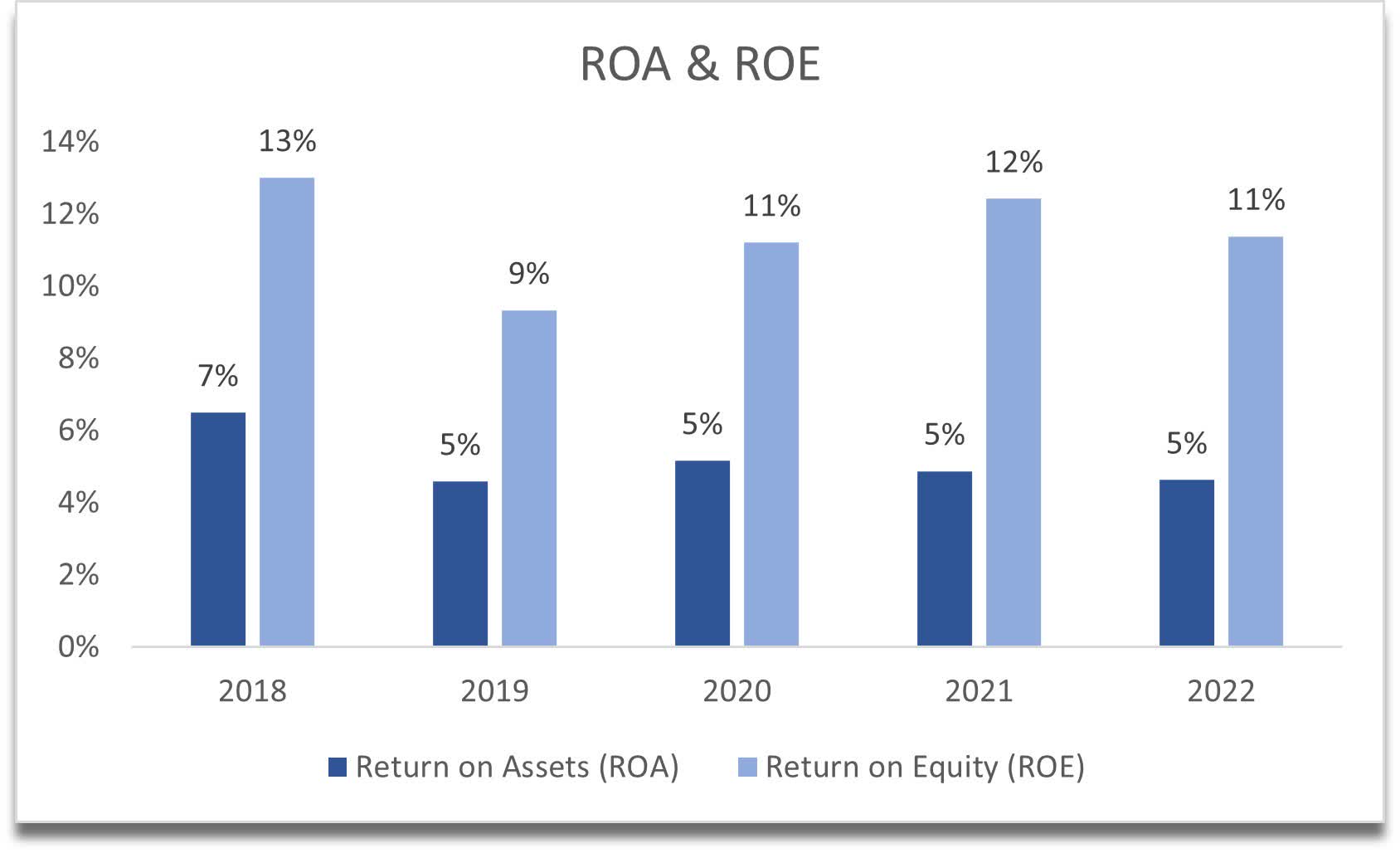

The company's ROA and ROE have been relatively stable over the years and just about at the minimum of what I like to see from a company, which is 5% for ROA and 10% for ROE. This tells me that the management is decent at utilizing the company's assets and shareholder capital, however, ROA could be improved slightly more.

{kind=link}

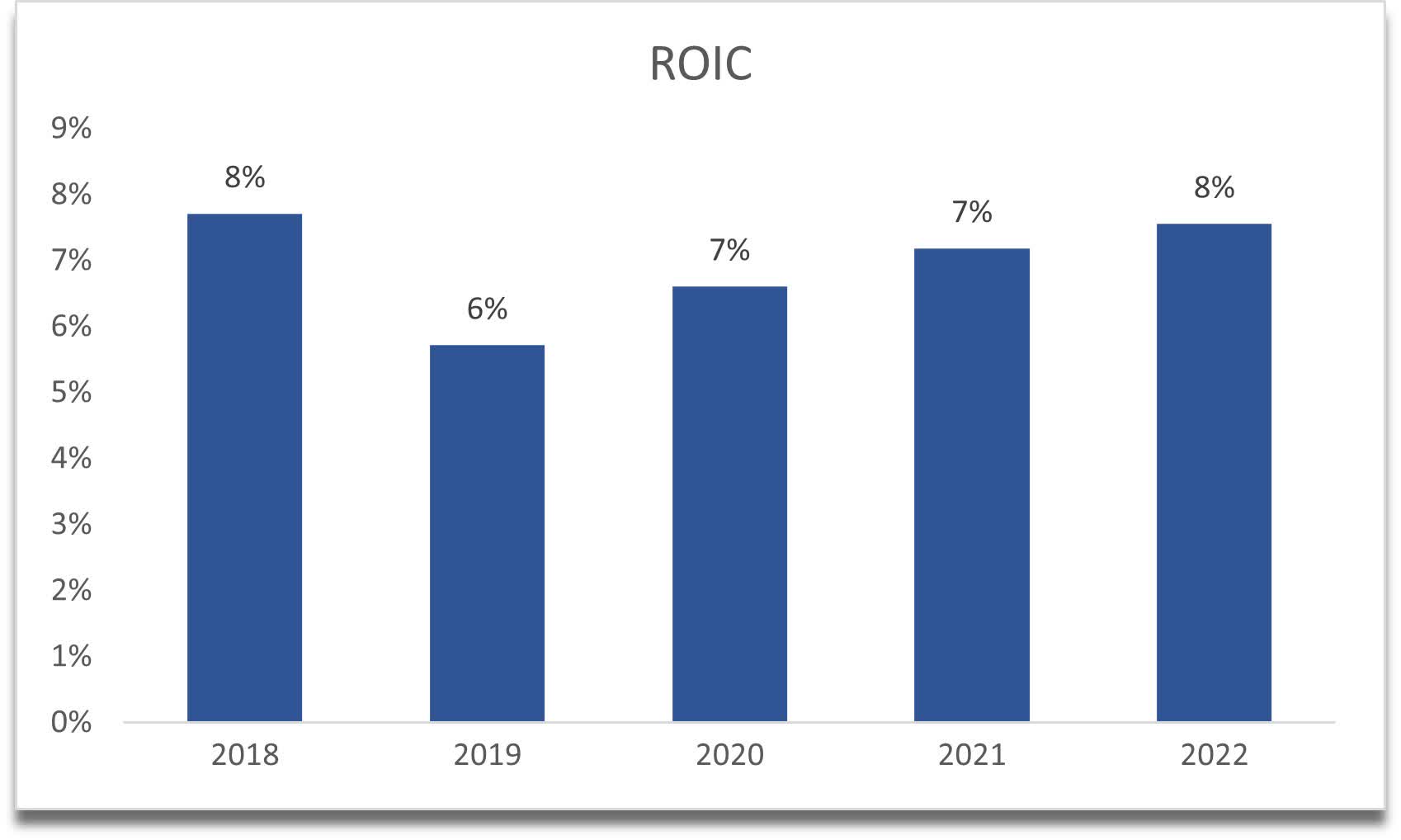

CENT's return on invested capital shows a similar story. It has been relatively stable over the last 5 years, with slight improvements from FY19. I usually look for at least a 10% ROIC, which the company is lacking here for now, however, if the trend continues, we could see it go over 10% in a couple of years. For now, I will have to add a bit more margin of safety in the valuation section.

{kind=link}

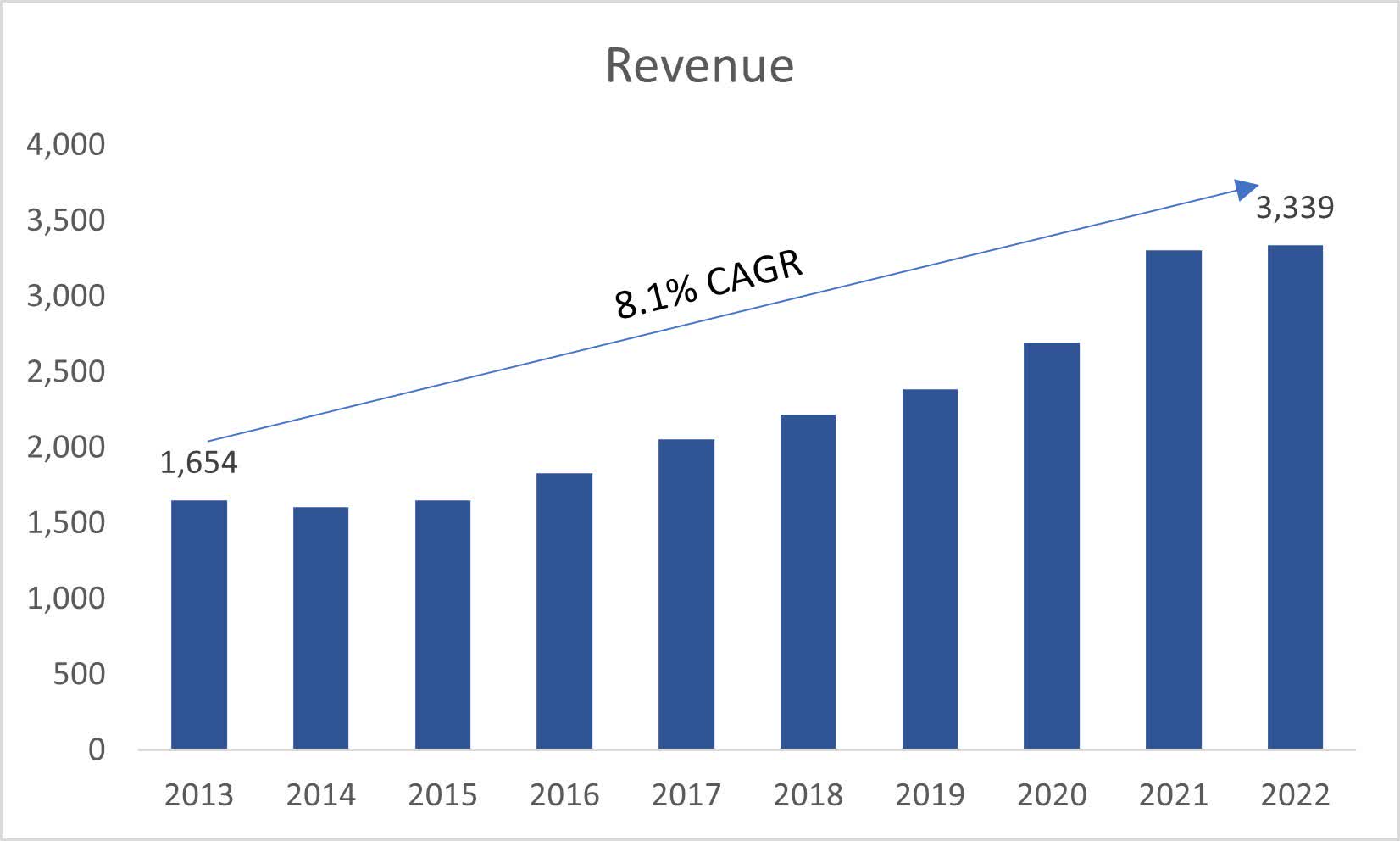

In terms of revenues, I see that the company managed to grow at around 8% CAGR over the last decade, which is not bad growth, but nothing extraordinary, either. Analysts are estimating the company will see negative growth of 1.3% for FY23, and just over 1% growth the following year, which is well below the company's average. I take these estimates with a grain of salt and will come up with some reasonable estimates for my analysis later on. The company has been growing revenues at a very steady pace, and I think that the recent numbers plateauing is an anomaly, and the company will resume the trajectory upwards.

{kind=link}

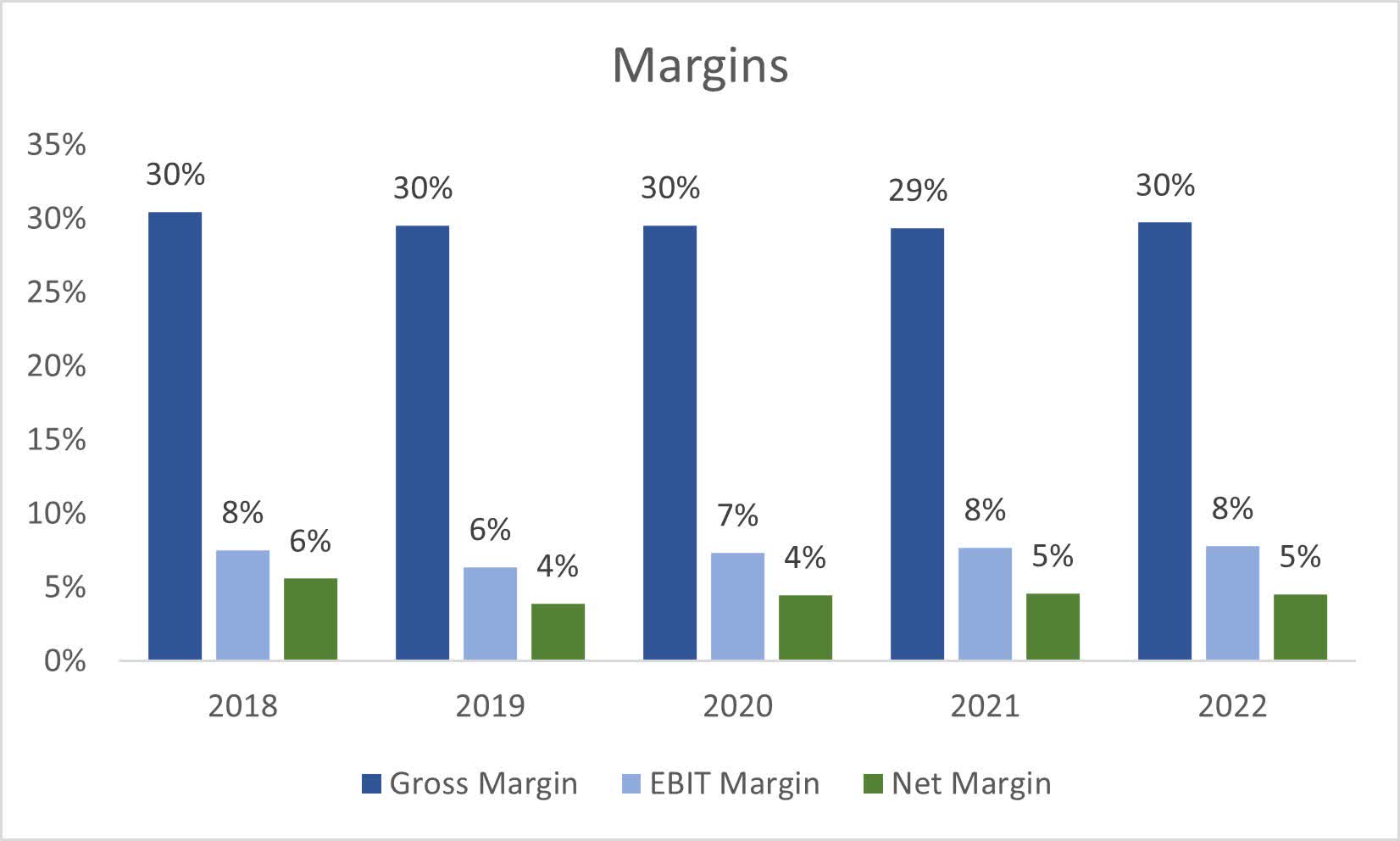

In terms of margins, these have also been very stable over the last 5 years, which makes for an easy estimation in future calculations. The company is operating in a sector that has relatively low margins, so any small improvement here would play a huge role in the company's intrinsic value. As of the latest quarter Q3, the company's margins seem to be holding up at about the same numbers as seen historically.

{kind=link}

Overall, I see a company that's been keeping it quite steady over the years, which isn't a bad thing, but certainly not the greatest either. I would prefer to see some improvements in some aspects of the financials, like an improvement in margins and ROIC, which would make this company a lot more attractive as an investment and would require a smaller margin of safety in the end. A big question is what kind of revenue growth the company is going to achieve in the future. Is it going to be less than the current inflation numbers? Only time will tell.

Valuation

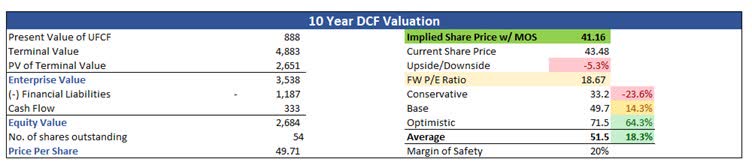

I decided to be slightly more optimistic in terms of revenue growth than what the analysts are estimating because, over the long term, the company should see a rebound in sales. I am also going to be a little more conservative than the company's past revenue growth of 8% CAGR. For the base case scenario, I went with a 3.5% CAGR, which will provide me with an extra margin of safety. For the optimistic case, I went with a 5.5% CAGR, while for the conservative case, I went with a 1.5% CAGR to give myself a range of possible outcomes. These numbers look to be achievable and either of the three is possible in my opinion.

For EPS for the base case, I decided to go with around $2.33 a share for FY23, which is slightly lower than estimates. Again, this gives me more margin of safety. After that, the EPS is going to grow at around 8% CAGR until FY32. For the optimistic case, I went with around 9% CAGR for the decade, while for the conservative case, I went with around 6% CAGR.

On top of these estimates, I am going to add a 20% margin of safety to be extra cautious, as it is better to be safe than sorry when it comes to investments. You can buy a great company, but if you overpaid, you may still end up losing in the end. With that said, I believe CENT's intrinsic value is around $41.16 a share, which means the company is trading at close to its fair value.

{kind=link}

Closing Comments

The company's operations have been going steadily over the years and that is not a bad thing. It may deter some investors because it is so unexciting. The high debt number is also a big deterrent for many. I think the company may see lower numbers than my PT in the near future because of macroeconomic headwinds like persistent inflation and higher interest rates for longer, which no doubt will bring volatility to the stock market.

I am assigning a hold rating for now until the company comes down further in the share price and until it reports its full-year results, which should be sometime at the end of November. After that, I will revisit the company and see what the management sees for the whole of next year in terms of demand, high inventory counts, and margins. I would like to see efficiency improvements, which will undoubtedly change the company's intrinsic value for the better if the management can implement some cost-cutting initiatives.

For further details see:

Central Garden & Pet: Underwhelming Financials, Lack Of Growth Not Appealing