CPF - Central Pacific Financial: A 5.4% Yield With A 45% Payout Ratio

Summary

- Central Pacific Financial is a Hawaii-focused local bank with just under $8B in total assets.

- The EPS in Q3 came in at just over 60 cents, resulting in a P/E multiple of less than 8.

- We will have to keep an eye on the economic situation in Hawaii, but I like the breakdown of the loan book and the very decent LTV ratios.

- The dividend yield is pretty attractive, especially given the relatively low payout ratio.

Introduction

The last time I discussed Central Pacific Financial ( CPF ) was in March 2021 . The bank’s share price had almost doubled in the six months leading up to the article but unfortunately CPF was unable to maintain the momentum and the share price is currently just over 25% lower than where the stock was trading at in March 2021. As we are now more than eighteen months later and as the bank has reported on seven additional quarters, I felt this could be a good time to revisit my 2021 thesis.

A quick look at the Q3 results

Central Pacific is focusing on the Hawaiian islands and tourism obviously is a very important source of income and an important contributor to the GDP of the islands. In 2021, I was quite charmed to see the largest position in the loan book was residential real estate, which made up about 34% of the total loan book with an additional 11% of the loan book classified as home equity loans with on top of that, 10% of the loan book consisted of consumer loans. While that still means about 45% of the loan book was exposed to commercial loans , CPF was strongly diversified and I think this has helped the bank to navigate through the COVID crisis.

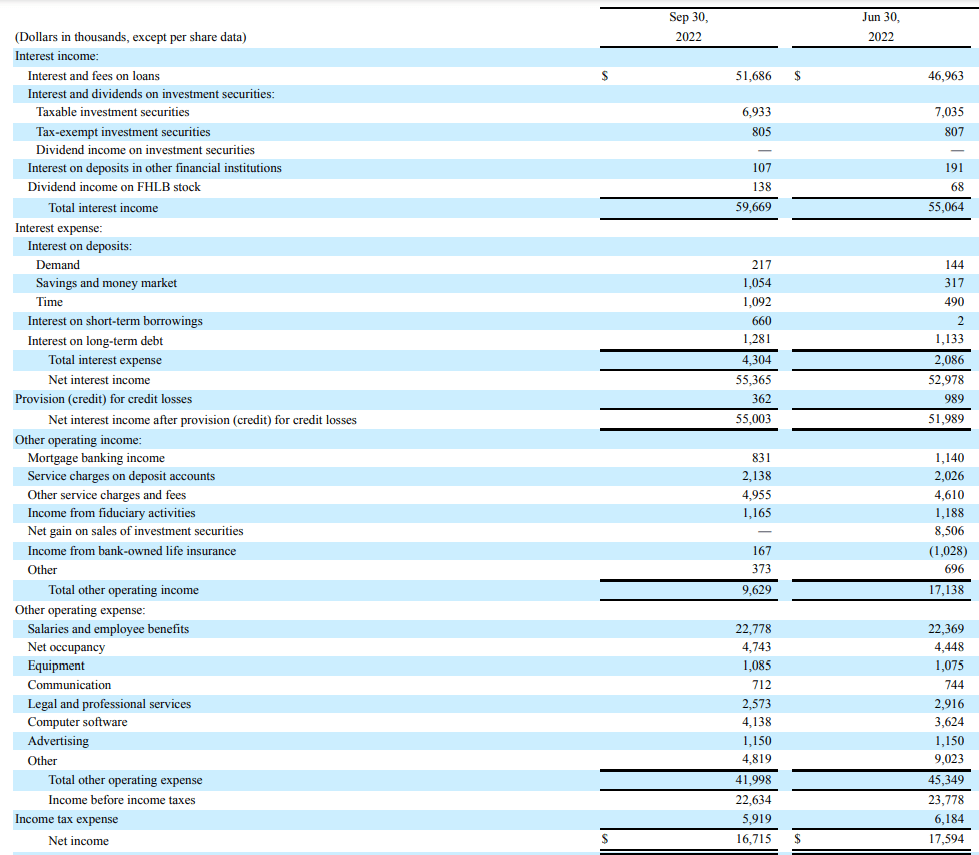

Fortunately the bank is also benefiting from the increasing interest rate environment. The total interest income increased by just over 8% to almost $60M and although the interest expenses more than doubled, the net interest income still increased by approximately 4% to $55.4M. And as you can see below, the net loan loss provision was just a few hundred thousand dollar and this helped to boost the pre-tax income to $22.6M. While that is lowest result in several quarters, keep in mind the Q2 result was boosted by a $8.5M gain on the sale of investment securities while the quarters before that included the reversal of loan loss provisions.

{kind=link}

So while you see a decrease of the pre-tax income, the net income and the EPS, CPF actually performed quite well and the reported EPS of $0.61 is a ‘clean’ result: there are no non-recurring items that had a (positive or negative) impact on the bottom line.

Meanwhile, the bank is still paying a quarterly dividend of $0.26 per share and the $1.04 annualized dividend means the yield has increased to just over 5.4% based on the current share price of $19.19. This makes Central Pacific quite attractive for income investors as well.

The book value has been sliding but CPF is playing it smart

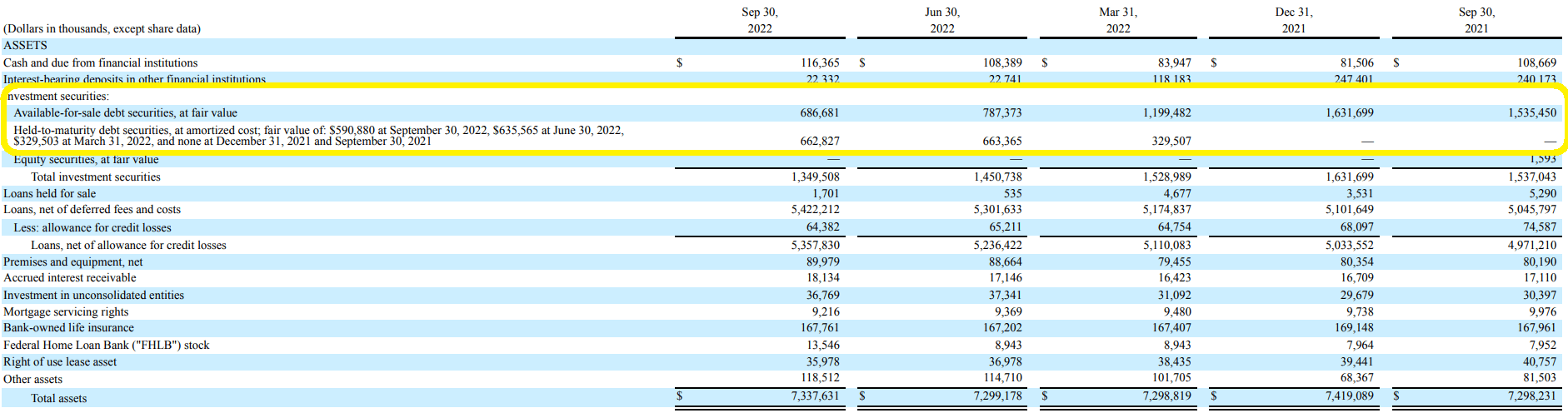

Another element about CPF I certainly appreciate is the decision to move a bunch of the securities available for sale to the ‘held to maturity’ category. As you may know, securities classified as available for sale need to be marked to market which means that in the current interest rate environment the unrealized losses on these positions are adding up. This does not impact the income statement, but does have a negative impact on the book value and book value per share. As you can see in the image below, CPF has been gradually reducing the position size of its securities available for sale, and has been gradually building up the debt securities held to maturity (which are not subject to the mark-to-market requirement).

{kind=link}

This does not mean CPF was immune to the changing interest rates but it was able to keep the damage limited. As of the end of September, the equity value on the balance sheet was approximately $438M, resulting in a book value and tangible book value per share of $16.08. This means the stock is trading at a small premium of just under 20% and that’s acceptable given the strong credit history and the attractive earnings profile of the bank.

{kind=link}

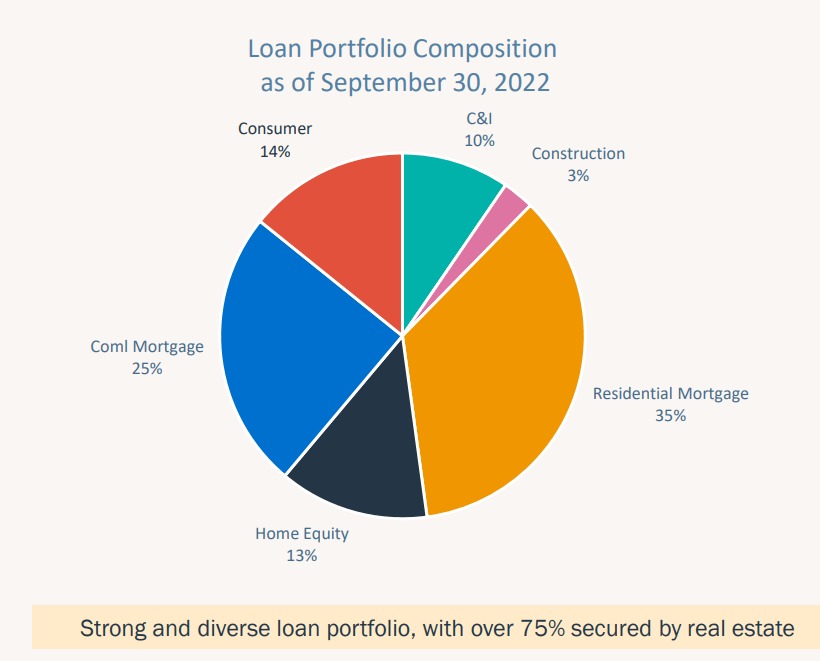

As explained earlier in this article, one of the main features why I liked Central Pacific in 2021 was its high exposure to residential real estate and non-commercial loans. I argued that 55% of the loan book consisted of these consumer loans with almost half of the loan book being represented by residential real estate related loans. In the past eighteen months, CPF has further increased the percentage of its loan book invested in residential real estate.

{kind=link}

As of the end of September, 48% of the $5.4B loan book was invested in residential mortgages and home equity related investments with an additional 14% of the loan book (approximately $750M) invested in consumer-related loans. The bank also disclosed the LTV ratios for these loans: the average LTV ratio in the residential mortgage and home equity segment is 64% and 61%, respectively. On top of that, the LTV ratio in the commercial mortgage segment is also just 61% so even though we can expect the higher interest rates to have a negative impact on the capitalization rates, CPF should be pretty shielded thanks to the very decent LTV ratios. And the higher interest rates on the markets should also have a positive impact on the net interest income which could make it easier to increase the loan loss provisions (if needed) to further bolster the level of provisions.

Investment thesis

Central Pacific Financial is an interesting bank. The increasing interest rates should be a positive for the bank but we also have to keep an eye on how Hawaii is getting through this inflation-crisis. I can imagine there will be an impact on the tourism industry as budgets get cut while foreign tourists may be deterred by the strong US Dollar.

That’s why I’m still a bit cautious but I think the bank offers good value for money. The dividend should be safe and offers a nice compensation while waiting for the bank to trade at a slightly higher multiple than the 8 times earnings CPF is currently trading at.

I currently have no position in Central Pacific but I am definitely watching with interest.

For further details see:

Central Pacific Financial: A 5.4% Yield With A 45% Payout Ratio