CENX - Century Aluminum Company: Strong Market Trends And Tailwinds Ahead

2023-04-24 04:21:33 ET

Summary

- Century Aluminum Company has been able to almost double its revenues from 2017 as the demand for its products is steadily increasing as the need can't be satisfied fast enough.

- The aluminum industry has a positive outlook with a CAGR of 5.61%, which CENX should be able to capitalize from heavily.

- It's often hard to invest when margins look horrible, but in the commodity market that is often when you find the best long-term winners, and I think that is true.

Investment Summary

Century Aluminum Company ( CENX ) is expected to experience rapid growth as the need for better and more reliable aluminum sources is continuously increasing. Since its beginning, CENX has managed to set up production in both the United States and Iceland. They produce a “standard-grade” and “value-added primary aluminum product”. The demand the company has experienced in the last few years has led them to almost double the top line since 2017. The trend seems to be in the right direction with the EPS expected to grow immensely as margins begin to move upwards. The management had some comforting expectations with the adjusted EBITDA expected to land between $10 and $15 million in the first quarter of 2023. This paired with the strong market demand I see the company could capitalize on will get a buy rating from me.

Market Momentum

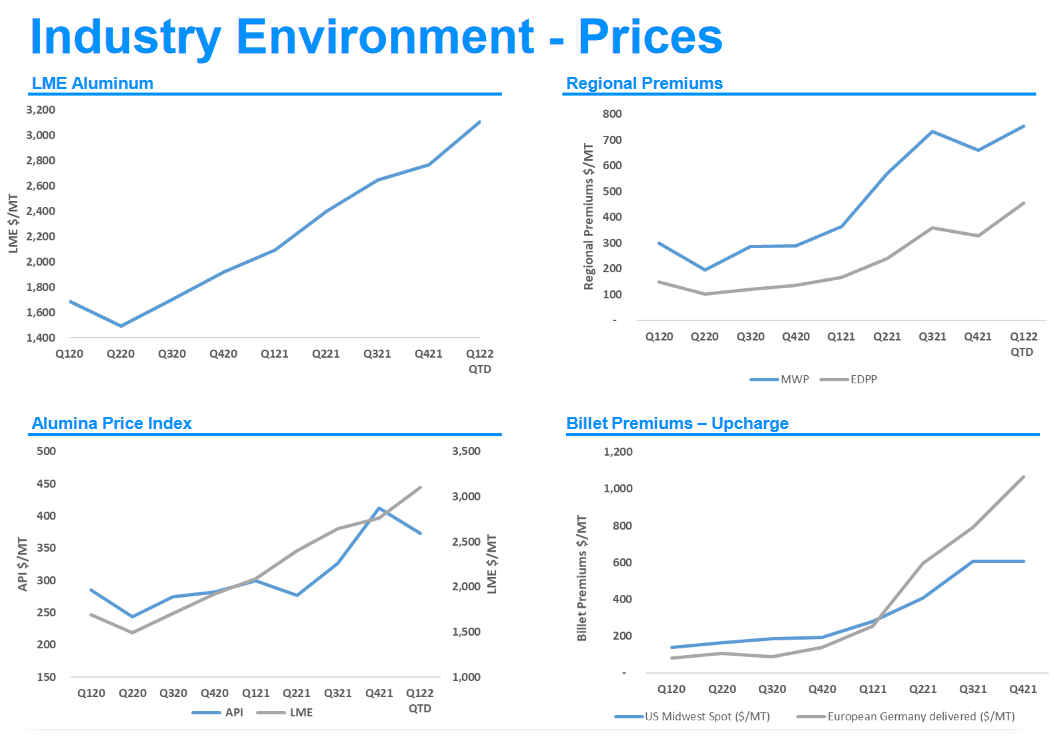

Seeing as CENX has a global customer base and I think they will be able to benefit from the continued demand for aluminum. In a report by precedence research they estimate the market to grow 5.61% between 2022 and 2030. Growth like that should be visible in the revenues for CENX I believe. In the report, some of the reasons for this growth is the continued infrastructure demand in countries like China and India where aluminum plays a major role. But also in the electrification of our society. In China, aluminum refineries are owned by the government and a large portion of the product stays within the country. This leaves a lot of room in the otherwise global market where CENX can market its product and benefit from higher prices.

{kind=link}

These higher prices are hard to estimate for how long they are able to be supported. But some form of pullback might be realistic as more and more companies aim to benefit from these prices. All in all, though, the market has a positive outlook of steady demand for many years moving forward. I think the already quite established position of CENX makes them a good option here to get some exposure to the industry.

Quarterly Result

Looking at the last earnings report by the company they had a solid result for 2022 in my opinion. The EPS came in negative but when adjusted it ended at $0.26 per share and I think the likelihood of margins being increased in the next few years thanks to the company seeing both greater demand and leaving the “high-cost environment” that was 2022 behind them. Inflation and higher interest rates took a toll on earnings.

Without the adjusted numbers for the year, the net loss ended up being $14.1 million which largely was due to $159 million charge for Hawesville asset impairments and $44.3 million from exceptional items.

In the report, the CEO Jesse Gary had the following to say “Global energy prices have reduced markedly since last summer, most significantly in the energy markets in which our U.S. smelters operate. At the same time, aluminum prices have remained buoyant, as long-term decarbonization trends continue to drive growth in global aluminum demand. Combined, these trends leave our businesses well situated to deliver excellent performance in 2023”. I think this is a great comment that highlights that aluminum prices are robust and will be there for a long time because of a large demand that can't be satisfied quickly.

Besides this the company also sees their casthouse project in Iceland being able to start generating revenues in the first quarter of 2024 as they begin producing Natur-Al green billet. It will be interesting to see the growth and impact it will have on the company. Right now it might feel early to invest in the aluminum market but I think CENX offers a good starting point. It's often the most difficult to invest when margins are low and everything looks expensive, but that is where the hidden gems are in the commodity industry.

Risks

Investing in companies exposed to fluctuating commodity prices is always risky. I have already talked about the poor margins that CENX has had in 2022 and I think that if we see a decrease in both the demand and price of aluminum the company might very well have a negative EPS for 2023 like 2022. But as the CEO mentioned, it seems the prices remain sturdy as the need is still there despite a slowing economy .

Looking at the company from a financial point of view, I think the long-term debts of $380 million could be a cause for concern as the company hasn't seen a reverse in the cash flow trend. It's still negative and even amounted to $220 million in 2022. This has helped fuel a continuation of the company diluting shares at a yearly rate of about 1%. I think that this should be an issue over the long term as the EPS should be able to increase faster and in turn, help the share price appreciate faster than shares are diluting too.

Valuation & Wrap Up

As for 2022, the p/e remains negative as the company reported a net loss of course. But looking at the numbers that are estimated for 2023 the p/e lands at under 18 which I really don't think is too bad when the EPS is expected to land at $0.49 which would be a massive increase. What I think might fuel growth this is an easier market to maneuver in and one that doesn't hold the same expense to it as 2022 where some quite significant expenses caused the company to have a negative EPS.

{kind=link}

Another company presenting an opportunity to get exposure to the aluminum trend is Kaiser Aluminum Corporation ( KALU ). They have slightly better margins than CENX using the 2022 numbers, where KALU had over 7% in gross margins whilst CENX had under 2%. But KALU has a significantly higher debt position at over $1 billion but the shares don't seem to be diluting YoY at least which is a bonus. I think there is more of a growth potential with CENX stock though as they have made some strategies in Iceland for example which I think will be able to greatly benefit the revenue growth. Buying when the price has already gone down 60% might seem like a trap. But I think the downside is limited and the upside potential outweighs it. I will be rating the company a buy and watching closely the next few earnings reports to see how the margins are improving.

For further details see:

Century Aluminum Company: Strong Market Trends And Tailwinds Ahead