CPWHF - Ceres Power: Business Model Concerns Persist

2023-09-28 17:04:13 ET

Summary

- Ceres Power, a British fuel cell company, has a promising technology but an unproven business model.

- Ongoing enthusiasm surrounds the prospect of a significant joint venture in China, but the slow pace of the deal is concerning.

- The company's long-term liquidity outlook is uncertain, and further dilution risk may be ahead if the China JV does not materialize.

The British fuel cell company Ceres Power ( CPWHF ) has the same promising technology it has had for years. But I believe it also still has the same unproven business model it has had for years.

I last wrote on the name last September in my “sell” piece Ceres Power: Ongoing Disappointment , since then the shares are flat according to Seeking Alpha data (although I think that reflects exchange rate difference, as the London sterling-denominated shares have declined 13% in that period). I continue to rate the shares as a “sell”.

Business Progress

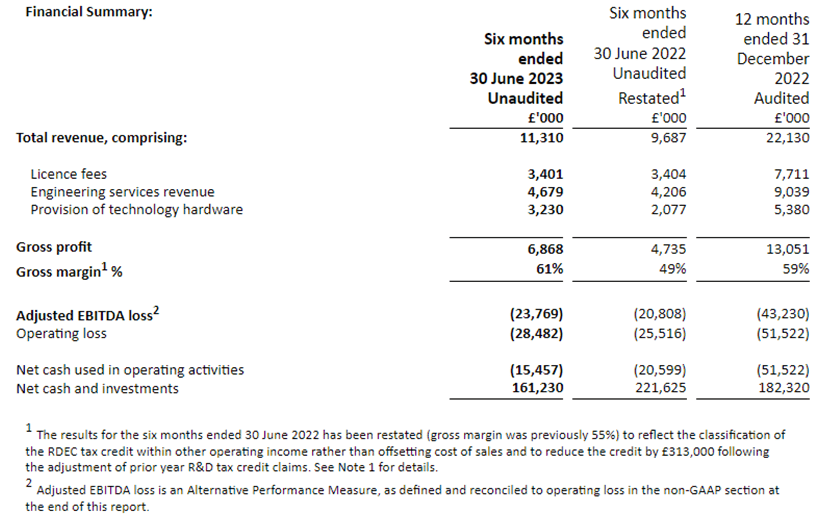

The company published its interim results on 28 September.

Interim revenue came in at £11.3m, up from £9.7m in the equivalent prior year period. The gross margin was 61% (up from 49%) and cash and short-term equivalents at the end of June stood at £161m, a decline of around £21m over the six-month period.

{kind=link}

Is there progress? Yes. However, it is slow.

Strategic Developments

A lot of ongoing enthusiasm for Ceres pertains to the prospect of a sizeable JV in China. Note that this was already penciled in to expectations for the shares when I last wrote about it almost a year ago.

In a trading update in July, the company had this to say on the seemingly elusive China JV closing:

Bosch and Weichai ( WEICF ) have reconfirmed to Ceres their commitment to the China JVs and are targeting signature this year. However, given the continued delay which is not within Ceres' control, and the time required post signature for regulatory clearances, we are taking a prudent view that the revenue associated with the JVs is now unlikely to be recognised this year. This reduces our expectation for 2023.

In the interim results, the company said:

As flagged in our recent trading update, the timing of the establishment of the China JVs with Bosch and Weichai, and the associated revenue, remains uncertain. We continue to make good progress in other areas of the SOFC business particularly in our partnerships with Bosch and Doosan.

The revenue for the full year will be impacted by the China JVs as already flagged in our recent trading update, and full-year numbers will depend on the timing of securing new licence partners.

At face value, that all still sounds positive. However, the slow pace of this concerns me. Time kills all deals and it is hard to ascertain from the pace of this deal being discussed to date how enthusiastic the various parties are to complete it. Announcement that it has been signed, on attractive terms, could certainly provide a fillip to the Ceres Power share price. I also see a risk of the reverse happening. If delays continue and the deal simply fizzle out at some stage, that could send the shares down substantially.

Other recent commercial developments include Bosch receiving funding to enable mass production of a solid oxide fuel cell product, which uses Ceres’ technology, Doosan’s 50MW factory in Korea is being constructed and is expected to be commissioned next year and an electrolyser is undergoing commissioning in anticipation of deployment by Shell in India this year.

These are all positive news items and in the long run I think a portfolio of such contract wins could be a more astute strategy for Ceres then relying heavily on big wins like the proposed China JV.

However, what remains less clear is what such commercial developments mean for the topline and especially for the bottom line. After several decades in business, though, I am not sure this news flow is sufficiently compelling to support the current share price.

Long-Term Liquidity Outlook

In my last piece, I wrote,

For now I do not see liquidity as a concern even if the company continues in its current lossmaking, cash-burning mode. Ceres ended the first half with £222m in net cash and equivalents, which I consider gives it a comfortably liquidity cushion for the short- and medium-term. In the longer term, though, if the company needs to boost its liquidity again in future, I see the risk of further rights issues diluting shareholders as has been the case in the past. The company has continued to increase its share count, most recently in June.

Fast forward almost a year and that £222m has declined to £161m by the end of June and, if that run rate continues, likely to be just short of £150m now.

So my sentiment from a year ago remains the same today. For now, the company has a liquidity headroom of two to three years. If the China JV is finalized and that brings a cash injection, that could help liquidity but the flipside is that any such development could also add costs as well as cash.

But, if the China JV doesn’t go ahead as hoped, I reckon Ceres could be looking to raise funds in 18-24 months to boost liquidity. So I see further dilution risk ahead.

Risks

Liquidity does not look like a short term risk but it is one over the coming few years at the current rate of cash burn.

The China JV signing or not signing is also a risk. I think Ceres has put a lot of focus on this and would prefer they spread their sales efforts more broadly to be less dependent on a single opportunity that could fall prey to regulatory concerns or commercial considerations.

Meanwhile, competition in the space continues to grow and that could threaten or eradicate Ceres' competitive advantage.

Valuation Still Looks Hard to Justify

This is a consistently loss making company that is burning around £60m of cash a year.

Its market capitalization is £625m, which allowing for the cash on the balance sheet suggests an enterprise value of around half a billion pounds. That equates to around 22 times last year’s sales. Even if the second half of this year shows a similar year-on-year increase to the first half, we are still looking at a price to sales ratio of around 20. We could compare that to peer valuations but as a conservative investor I prefer simply to compare it to what I think is reasonable, independently of the large valuations in the sector. That said, compared to the P/S ratio of 5 or so at Plug Power ( PLUG ), Ceres' valuation on a P/S basis still looks very high.

A lot currently rides on the China JV. I think it is partly baked into the share price. If the JV eventuates, I am not sure it will lead to a significant long-term upwards rerating of the Ceres Power share price, though I would expect an immediate boost in reaction. It would also make the company heavily reliant on one set of customers. Even if it does get confirmed, I have doubts that Ceres has the negotiation cards the other side does, so am not convinced it will get a great deal. I feel Ceres needs the China JV more than China JV partners Bosch and Weichai need Ceres.

If the JV does not get confirmed, I think the valuation could fall to reflect something more like the current market reality of the Ceres business as it continues to bleed red ink.

I continue to see the shares as overvalued and accordingly maintain my “sell” rating.

For further details see:

Ceres Power: Business Model Concerns Persist