CGDV - CGDV: Actively Managed Dividend ETF Beating The Market

2023-09-21 04:41:00 ET

Summary

- CGDV is an actively managed dividend ETF that outperformed SPY in 2022 and has kept pace in 2023, an impressive feat given how growth stocks have dominated much of the year.

- With a February 2022 launch date, CGDV has already amassed over $3 billion in assets under management. Its unique multi-manager structure is a key selling point.

- CGDV's five managers have a diverse set of backgrounds, areas of expertise, and styles that should help mitigate losses in case market conditions change quickly.

- The portfolio currently trades at 21x forward earnings on a weighted average basis, or five points cheaper than SPY. This article also compares CGDV's fundamentals against VIG, a well-established, low-cost dividend growth ETF.

- Overall, I'm impressed. CGDV is the type of ETF you likely haven't come across before, and I think it belongs on the watchlist of value investors.

Investment Thesis

The purpose of this article is to initiate coverage on the Capital Group Dividend Value ETF ( CGDV ), a 19-month-old actively-managed fund that has outperformed the SPDR S&P 500 Trust ETF ( SPY ) by 6.80% with less volatility. While most of that beat occurred last year, CGDV has kept pace with SPY in 2023, an impressive feat for a dividend fund in a strong bull market. In this article, I'll evaluate Capital Group's unique multi-manager structure, compare its fundamentals against passive alternatives, and judge whether CGDV is worth owning at this time.

CGDV Overview

Manager Profiles

CGDV may be new, but Capital Group is not. According to its website , Capital Group was founded in 1931 and is "one of the largest investment management organizations, managing more than US$2.2 trillion." A brief description of the firm's general investment approach is below:

{kind=link}

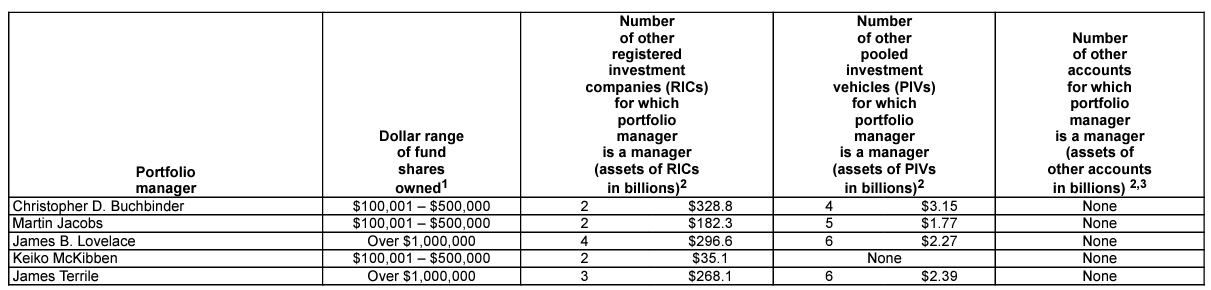

A unique feature is Capital Group's multi-manager structure , each with a particular background, style, and approach. In CGDV's case, five portfolio managers are listed in the fund's Statement of Additional Information .

{kind=link}

Christopher D. Buchbinder also co-manages two other registered investment companies with a combined $328.8 billion in assets as of May 31, 2023. The largest is the Growth Fund of America ( CGFAX ), to which Capital Group is the advisor. Mr. Buchbinder brings 27 years of experience to CGDV, all with Capital Group. Martin Jacobs , James B. Lovelace , Keiko McKibben , and James Terrile add a combined 132 years of investment experience, 73 with Capital Group. I've opened with this because I don't want readers to get the impression that CGDV is some experimental ETF. It's run by industry veterans deeply familiar with the Capital System and each other.

As mentioned, CGDV has a multi-manager structure. I've listed each manager's area of expertise below, according to the link bios above:

- Buchbinder: telcos, autos, auto parts and equipment

- Jacobs: industrial machinery and electrical equipment

- Lovelace: beverages, tobacco, restaurants, household/personal products

- McKibben: aerospace and defense, IT, machinery, business services

- Terrile: health care supplies and equipment, pharmaceuticals, biotech

There appears to be little overlap, which is ideal. However, from a sector perspective, expert coverage on Energy, Financials, Materials, Real Estate, and Utilities is absent, or at least not mentioned prominently on the Capital Group website.

Strategy Discussion

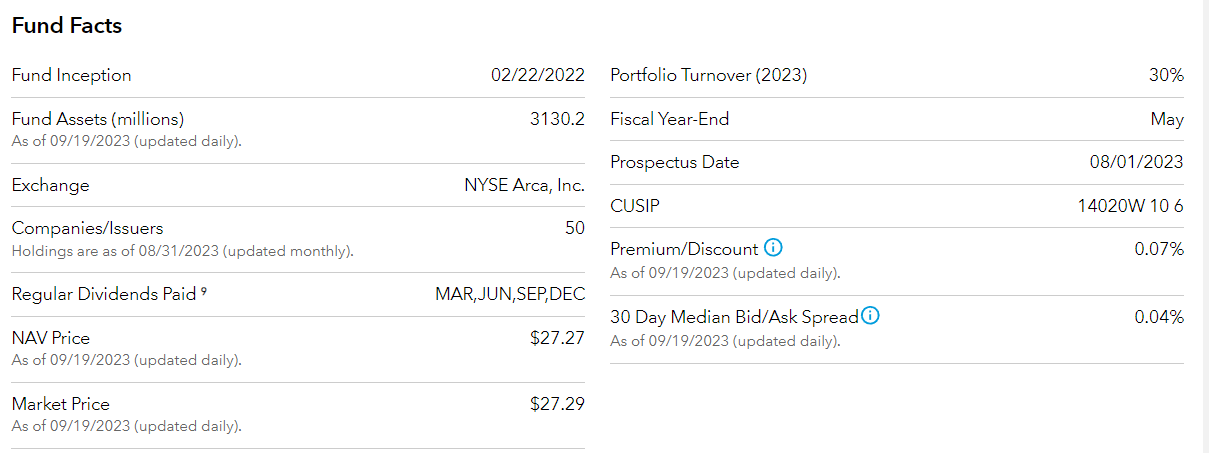

The stated investment objective of CGDV is to "produce income exceeding the average yield on U.S. stocks generally and to provide an opportunity for growth of principal consistent with sound common stock investing." The fund primarily invests in large-cap U.S. stocks but can hold up to 10% of assets outside the U.S. Additional fund facts are listed below.

{kind=link}

As shown, dividends are paid quarterly in March, June, September, and December, and the ETF has increased its assets under management to $3.13 billion since its February 22, 2022, launch date. Portfolio turnover for the most recent fiscal year was 30%, much lower than I expected for an actively managed fund. This figure suggests that managers have high conviction and aren't looking for short-term profits. High conviction is admirable but can get you into trouble if you fail to recognize changing market conditions. However, CGDV's multi-manager structure should mitigate that issue since each manager is responsible for only a portion of the fund.

CGDV's expense ratio is 0.33%, which is reasonable but goes against the main objective of delivering above-average income to shareholders. The goal of providing a yield above the benchmark S&P 500 Index isn't an ambitious one, and 0.33% in fees is a substantial portion of the dividend income the fund's underlying holdings generate. It doesn't look like an appropriate product for income investors without significant dividend growth, which I'll evaluate later.

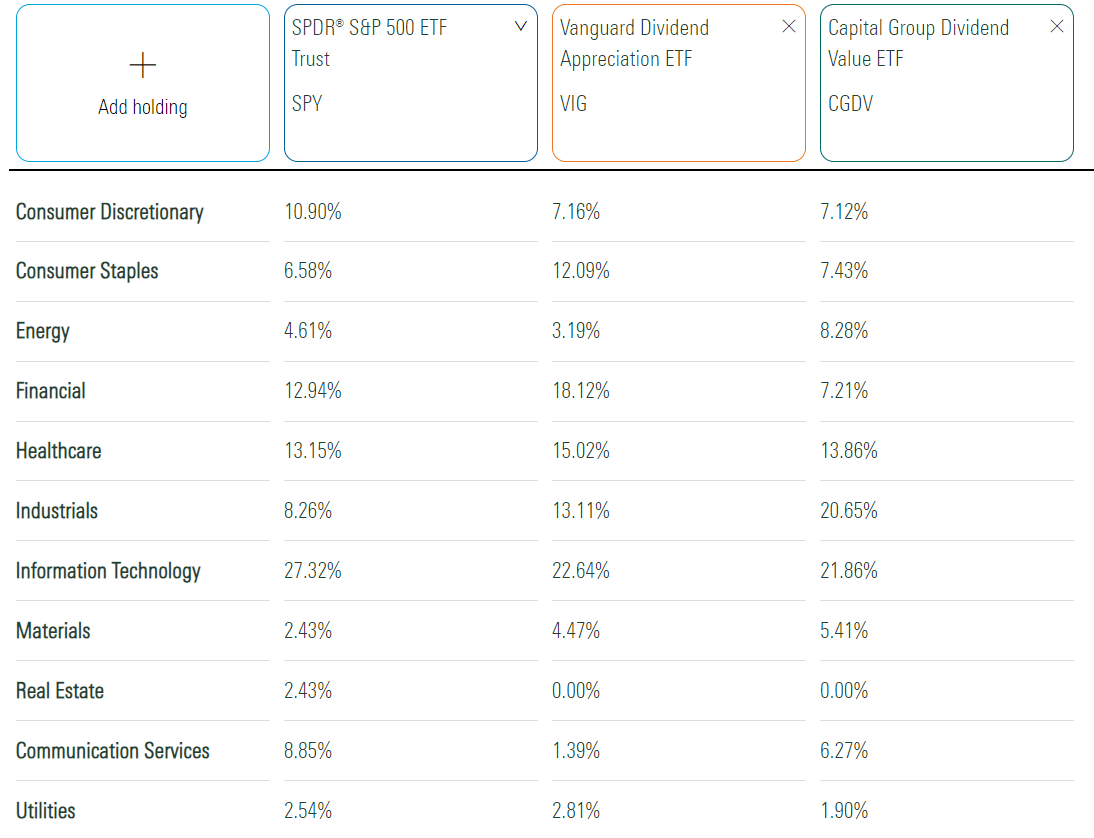

Sector Exposures and Top Ten Holdings

The following table highlights sector exposures for SPY, CGDV, and the Vanguard Dividend Appreciation ETF ( VIG ). I chose VIG as a comparator because it has a yield slightly above SPY and is a well-established dividend fund with low fees.

{kind=link}

CGDV doesn't hold any REITs, indicating that its distributions should be mostly qualified for tax purposes. Relative to SPY, it overweights Industrials by 12.39%, which may be coincidental or reflective of the portfolio managers' areas of expertise. Mr. Jacobs holds a bachelor's degree in industrial and systems engineering, while Ms. McKibben's background in analyzing aerospace and defense stocks is on display in CGDV. The ETF holds RTX Corporation ( RTX ) and General Dynamics ( GD ) for a combined industry weighting of 5.67%, the fourth-largest behind Semiconductors (12.37%), Tobacco (6.35%), and Systems Software (5.78%). While I can't say for sure, the managers seem to prefer investing in what they know, a bias I think most investors hold.

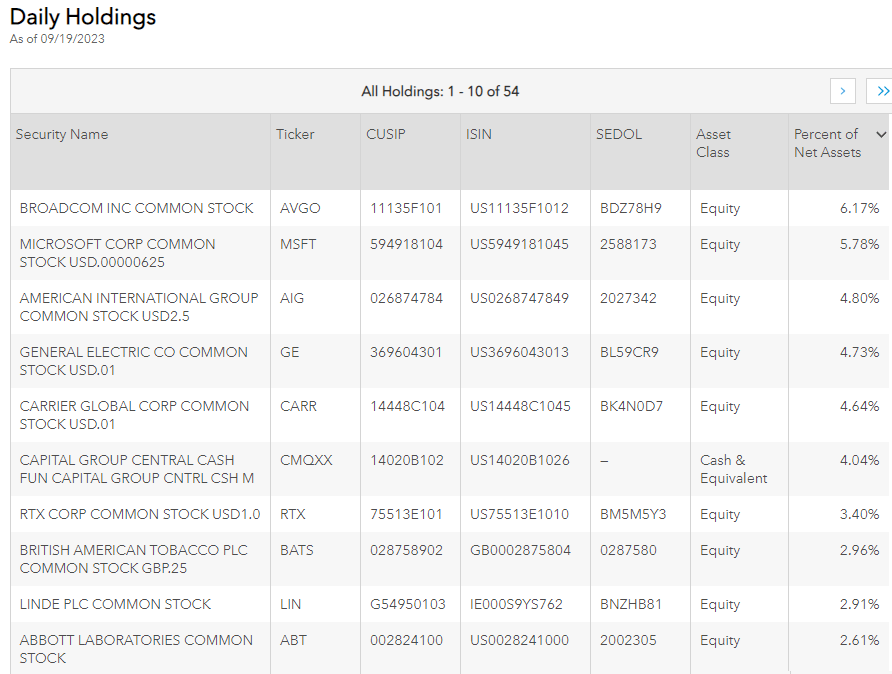

CGDV's top ten holdings are listed below, totaling 42.04% of the portfolio. The fund is led by Broadcom ( AVGO ), Microsoft ( MSFT ), and American International Group ( AIG ), which yield 2.17%, 0.91%, and 2.31%. We can deduce that fund managers do not screen out stocks based on their yields relative to the S&P 500 Index. Instead, managers retain flexibility in their investment choices so long as the net yield of the portfolio is satisfactory.

{kind=link}

There are 54 holdings listed, but only 49 equities. The most significant cash position is 4.04% to the Capital Group Central Cash Fund ( CMQXX ), which has a 30-day SEC yield of 5.39%.

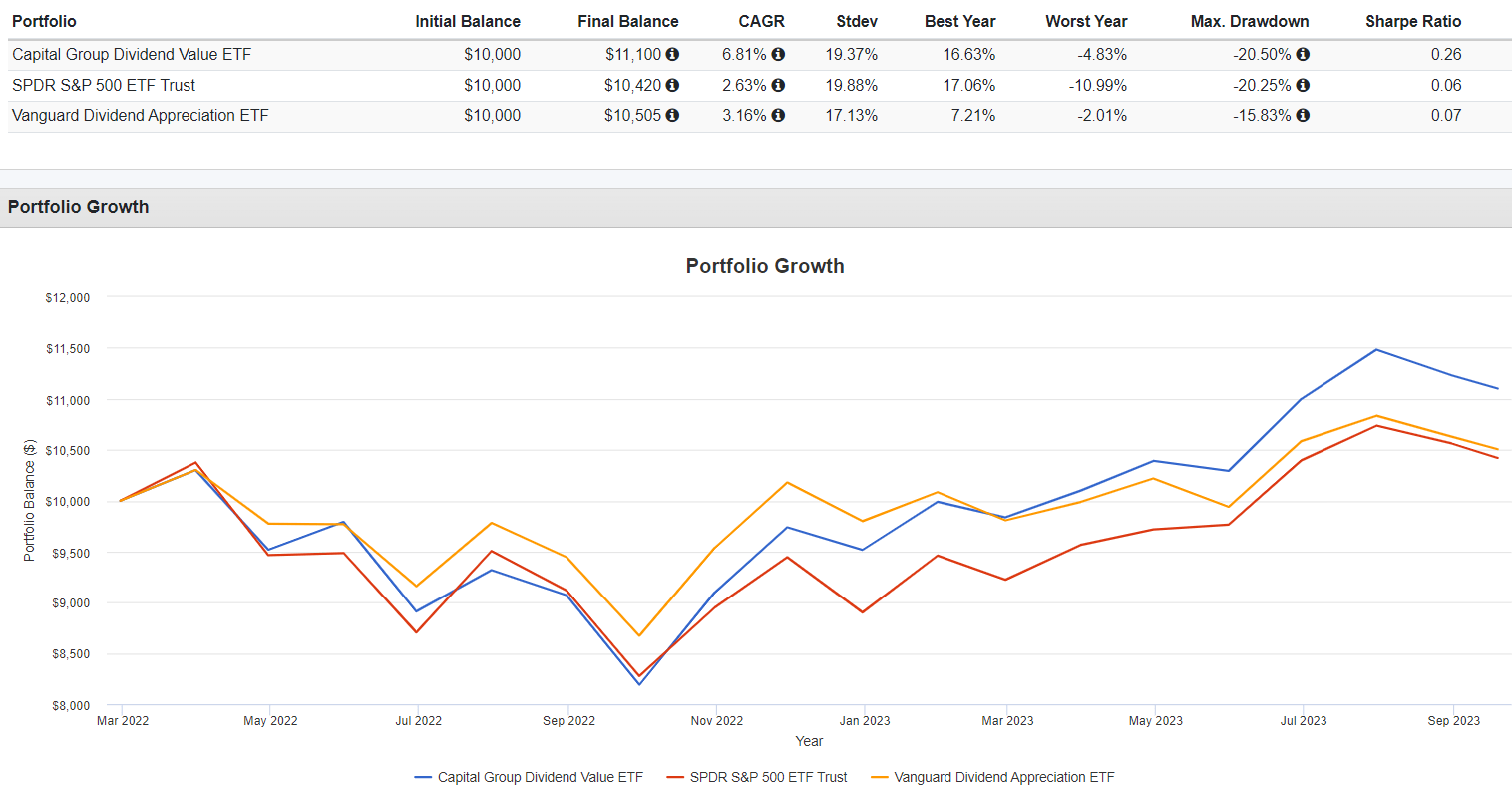

Performance

Unfortunately, CGDV doesn't have much of a track record yet. However, it's gained an annualized 6.81% since March 2022, beating SPY and VIG by 4.18% and 3.56% per year, respectively.

{kind=link}

What's better is that CGDV has kept pace with SPY in 2023 (16.63% vs. 17.06%). I could only find two large-cap dividend-oriented ETFs in the same ballpark: the Siren DIVCON Leaders Dividend ETF ( LEAD ) and the Franklin U.S. Core Dividend Tilt Index ETF ( UDIV ). LEAD and UDIV overweight Technology at 34% and 31%, so it should be no surprise. However, they were also the second- and third-worst-performing dividend ETFs in 2022, so CGDV's results are far more impressive.

CGDV Analysis

Industry Breakdown

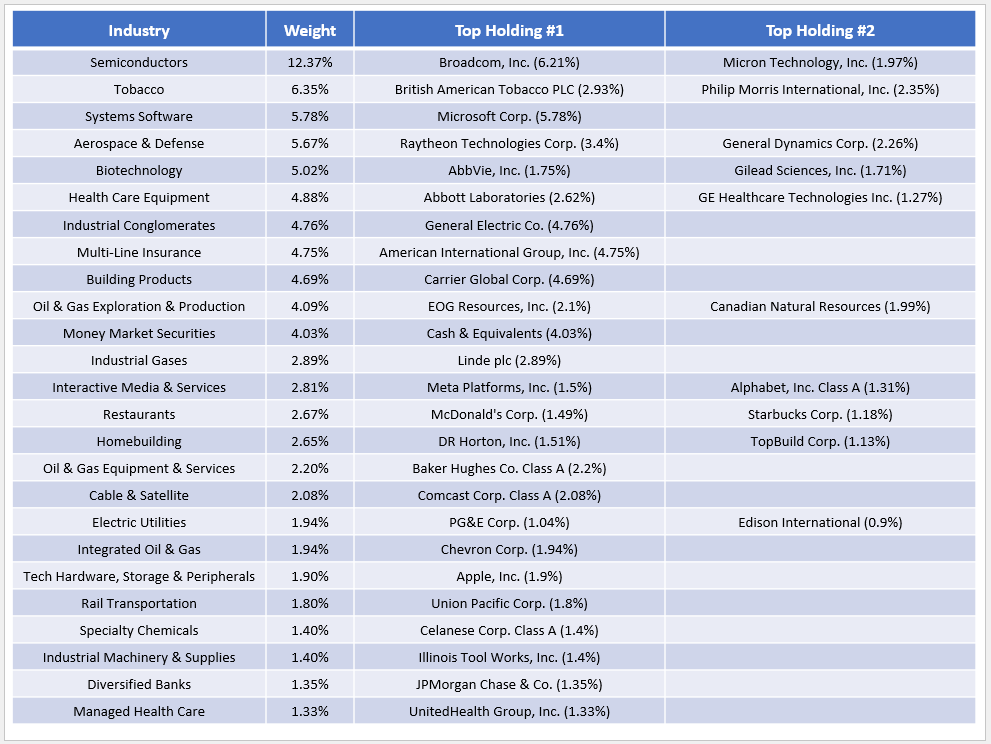

With only 49 equities, CGDV doesn't offer much diversification. However, the fund makes a reasonable attempt by allocating across 34 industries. I've listed the top 25 below, which cover 90.77% of the portfolio, and the top two holdings in each industry, where applicable.

{kind=link}

From this industry-level perspective, the diversification picture isn't too bad. Other successful ETFs have 90%+ of assets in their top 25 industries, including the Schwab U.S. Dividend Equity ETF ( SCHD ) at 92.91%. Therefore, while not ideal, I don't think this disqualifies CGDV from being a core holding. However, it may work best as a complementary fund.

CGDV Fundamentals By Company

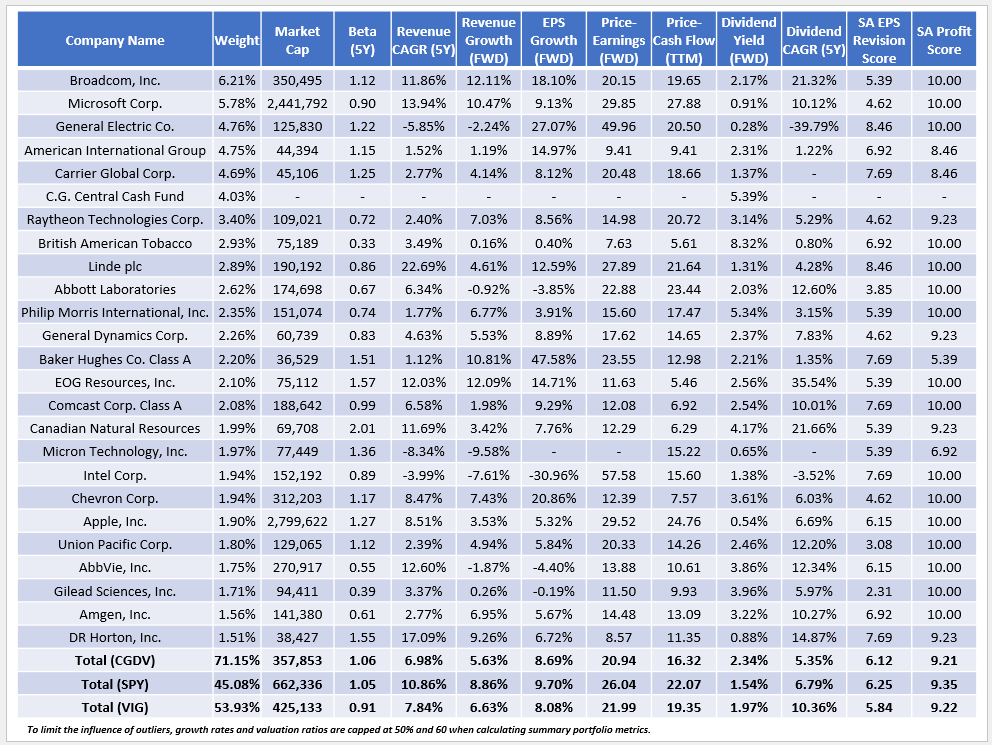

The following table highlights selected fundamental metrics for CGDV's top 25 holdings, totaling 71.15% of the portfolio. I've also included summary metrics for SPY and VIG in the bottom rows.

{kind=link}

A few observations:

1. CGDV's 1.06 five-year beta stands out because it's not typical of a dividend-oriented fund. Looking through my ETF Database, there are only a handful with five-year betas (based on current holdings) above 1.00 and weighted average market capitalizations above $100 billion, including:

- Siren DIVCON Leaders Dividend ETF: 1.11

- RiverFront Dynamic US Dividend Advantage ETF ( RFDA ): 1.10

- Freedom Day Dividend ETF ( MBOX ): 1.06

- FlexShares Quality Dividend Index Fund ( QDF ): 1.04

- Franklin U.S. Core Dividend Tilt Index ETF: 1.03

- Fidelity High Dividend ETF ( FDVV ): 1.02

- iShares Core Dividend ETF ( DIVB ): 1.00

Except for MBOX and DIVB, all these funds are performing better than average among dividend ETFs this year, a statistic that supports their higher betas. While these figures also suggest they'll decline in line with the market in downturns, it's more complicated than that. To illustrate, MBOX and FDVV, which yield 2.77% and 3.39%, did far better than lower-yielding funds like LEAD last year. Sector composition and market sentiment toward growth/value stocks will likely be better indicators.

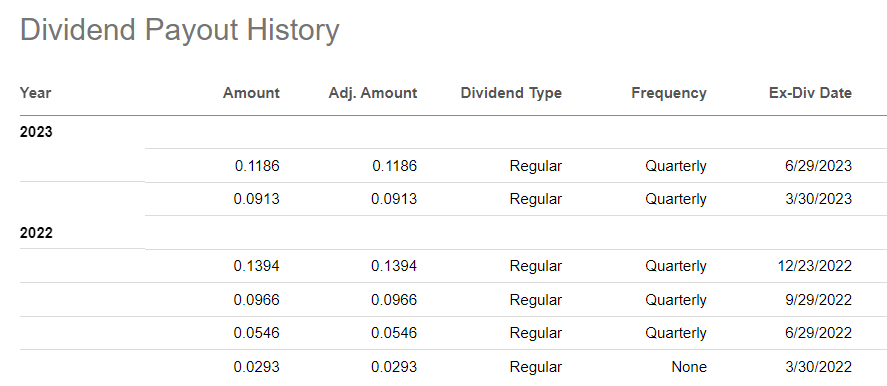

2. CGDV's constituents yield a weighted average of 2.34%, and investors should net approximately 2.01% after fees. The fund's trailing dividend yield is only 1.63%, but I believe this relates to how new it is. Early shareholders often experience dividend dilution because the fund typically grows at its fastest pace (percentage-wise) early on. Simply put, an ETF can only distribute income received, and if the ETF experiences a significant increase in outstanding shares just before the ex-dividend date, it must share that fixed pot among more investors, resulting in lower dividends per share. Based on the history below, the dividend is beginning to stabilize. The most recent $0.1186 quarterly payment works out to a 1.73% yield, and I expect next quarter's will be even bigger.

{kind=link}

3. CGDV's constituents only grew their dividends by 5.35% per year over the last five years, far less than the double-digit dividend growth offered by VIG. Since CGDV's yield is on the low end, I hoped this statistic would make up for it from an income perspective. Unfortunately, I can't see it as attractive to income investors, which is odd, given the fund's investment objectives.

4. Compared with VIG, CGDV offers a slightly more attractive combination of sales growth, earnings per share growth, and valuation (forward earnings and trailing cash flow). Compared with SPY, its 8.69% estimated earnings per share growth rate is only 1.01% less, but its forward earnings valuation is 5.10 points cheaper (20.94x vs. 26.04x). I like this setup, though it's not necessarily better than VIG, especially since it's much less diversified. The potential to underperform exists if a few key industries fall out of favor, and I'm not yet sure how quickly managers will adapt to changing markets. Remember that portfolio turnover was only 30% over the last year.

5. CGDV has a solid 9.21/10 Seeking Alpha Profit Score, which I calculated using individual Seeking Alpha Profitability Grades on a weighted average basis. However, it's similar to VIG's 9.22/10 score and SPY's 9.35/10 score. Among the 28 dividend ETFs I track with market capitalizations above $100 billion, the average score is 9.04, so it's nothing special. Many high-dividend funds have lower scores (e.g., DHS , FDV ), with SCHD the notable exception at 9.48/10. Still, at least CGDV doesn't appear to sacrifice quality for yield, as that's a recipe for long-term underperformance.

Investment Recommendation

My initial view of CGDV is favorable. I like Capital Group's multi-manager structure and how the five managers running the fund have differing backgrounds, areas of expertise, and styles. They proved themselves last year, with CBDV outperforming the broader market, as you would expect with a value-oriented fund. However, what's more impressive is how they've kept pace with SPY this year in an environment seemingly reserved for growth stocks. My main criticism is how CGDV is not designed for income investors. Based on its current holdings and expense ratio, I expect only a meager 2.01% dividend yield with weak dividend growth. In short, it's not a replacement for an ETF like VIG or a rare income/growth potential combination like what SCHD offers.

Still, that's not to say it's not a good value fund. I think it is, and while I'd typically reserve judgment for a new fund until it becomes more established, the Capital Group team is about as established in the investment management industry as you could ask for, and I respect their experience. Therefore, I've assigned a "buy" rating to CGDV, and I look forward to covering the fund more regularly from now on.

For further details see:

CGDV: Actively Managed Dividend ETF Beating The Market