GIB - CGI Inc.: I Like The Business But Not The Valuation

2023-10-03 07:03:01 ET

Summary

- CGI Inc. is a high-quality business with solid profitability and strong current revenue growth momentum.

- The company has a wide range of offerings and comprehensive geographical coverage, positioning it well to capture industry tailwinds.

- GIB's fair value is close to the current market price, with limited upside potential, leading to a neutral "Hold" rating.

Investment thesis

CGI Inc. ( GIB ) is a high-quality, under-the-radar business. The company demonstrates solid profitability compared to peers and continues to improve it. Revenue demonstrates strong near-term growth momentum, and the global IT consulting industry is expected to compound at double digits in the next five years. CGI's broad range of offerings and comprehensive geographical coverage make it a well-positioned player to capture industry tailwinds. On the other hand, my valuation analysis suggests that optimism is already priced in. The stock's fair value is close to the current market price, with a shallow upside potential. All in all, I assign CGI's stock a neutral "Hold" rating.

Company information

CGI is a Canadian IT and business consulting services firm. According to the latest 6-K report , the company employs over 90 thousand consultants worldwide.

CGI's fiscal year ends on September 30. The company is managed through nine operating segments split by geographic areas. According to the latest annual report , the company generated 29% of its sales in the U.S. in FY2022.

Compiled by the author based on the latest annual report

Financials

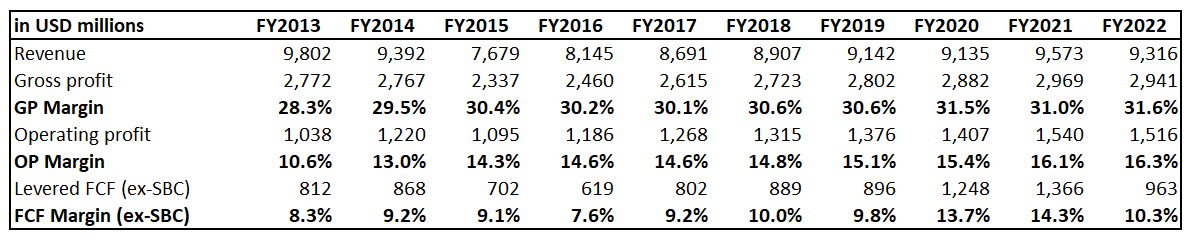

The company's financial performance has been solid over the past decade. Despite no revenue growth, I like that CGI's profitability metrics improved notably. While the gross margin has been more or less steady around 30%, the operating margin has improved significantly from 10.6% to 16.3%. As a result, the free cash flow [FCF] margin ex-stock-based compensation [ex-SBC] has been consistently in double digits in the last three years.

{kind=link}

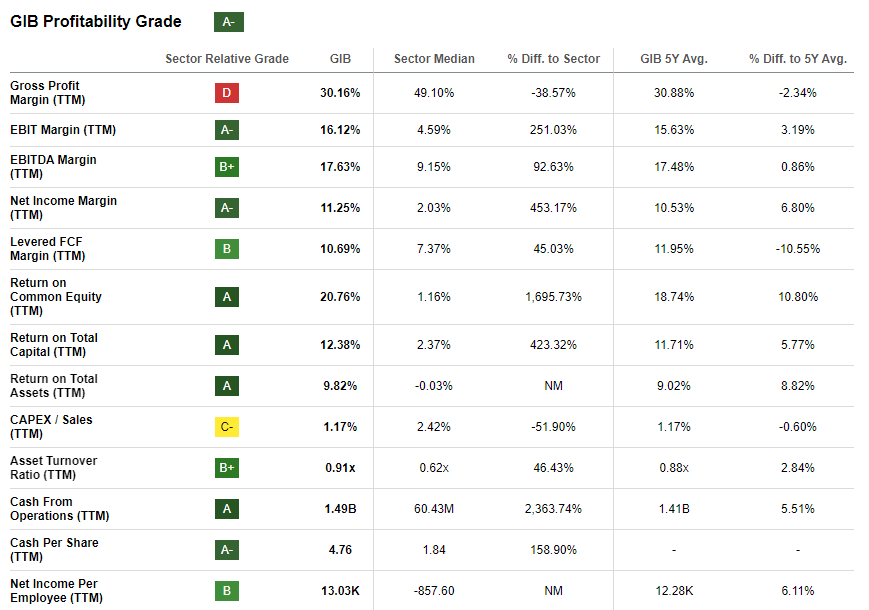

Having a stable and wide FCF margin means the company can maintain a healthy balance sheet. Despite being in a substantial net debt position, the overall leverage ratio looks conservative. I am also comfortable with the debt because CGI's covered ratio is high and far above 10. Short-term liquidity metrics are also in great shape. Despite having a solid FCF margin, the company does not pay dividends. On the other hand, CGI returns money to shareholders via consistent and substantial stock buyback programs.

Seeking Alpha

The latest quarterly earnings were released on July 26, when the company missed consensus estimates. Revenue demonstrated solid growth momentum with approximately 8% YoY growth. The adjusted EPS followed the top line and expanded YoY from $1.20 to $1.36.

Seeking Alpha

The upcoming quarter's earnings release is scheduled for November 8. Consensus estimates forecast quarterly revenue at $2.63 billion, which indicates a solid 9.5% YoY growth. The adjusted EPS is expected by consensus to expand from $1.15 to $1.31, which is also a bullish sign for investors.

Seeking Alpha

Overall, I like the business. Wide geographical diversity is a significant asset, and it also suggests that the company's services are superior to international and local competition. CGI's profitability metrics are expanding over the long term even without revenue growth, which means the management is efficient in improving the revenue mix and can exercise solid pricing power. The company's services and solutions are also diversified, focusing on IT. Given the favorable secular shift to digitalization, CGI's range of services makes it a solid play for investors. According to ReportLinker , the global IT consulting market is expected to compound at 11.4% up to 2027, which is a bullish sign. The company's strong presence globally and stellar profitability give me a high level of conviction that CGI will be able to absorb secular industry tailwinds.

{kind=link}

Valuation

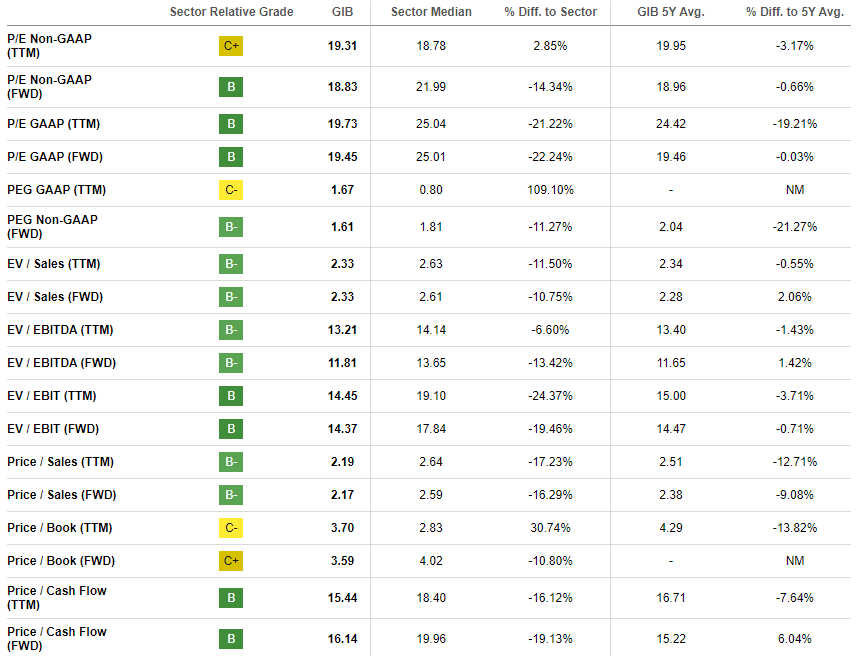

The stock rallied above 14% year-to-date, outperforming the broader U.S. market. Seeking Alpha Quant assigns the stock a decent "C" valuation grade, meaning that the stock is approximately fairly valued. Most of the valuation ratios are notably below the sector median. However, current multiples are very close to historical averages, which might indicate that the current stock price is very close to its intrinsic value.

{kind=link}

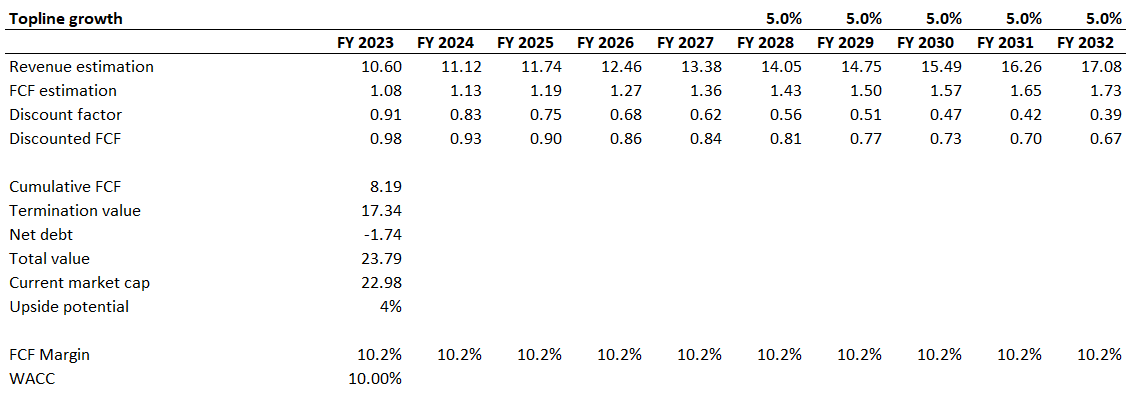

I want to simulate the discounted cash flow [DCF] model to get more evidence. A 10% WACC for discounting looks fair to me since the company's long-term financial performance has been stable. Revenue consensus estimates project mostly single-digit growth for the next five years. For the years beyond, I incorporate a 5% CAGR. I implemented the last decade's FCF average for my DCF model, which is 10.2%. I expect the FCF margin to be, on average, flat for the next decade.

{kind=link}

According to my calculations, the business's fair value is close to the current market cap. The upside potential is minimal. My fair value estimation for the stock price is approximately within the $100-105 range.

Risks to consider

The broader economic climate has a significant impact on the company's operations., directly and indirectly because economic cycles affect the financial success of CGI's clients. Macro challenges might lead clients to cancel, scale down, or postpone existing contracts and delay initiating new projects. Reduced client engagements may spur increased competition, which will pressure service pricing.

While I consider GCI's broad geographical presence an asset, it also exposes the business to numerous risks spanning financial, regulatory, and political spectrums across various countries. The company's earnings might be adversely affected by unfavorable fluctuations in the foreign exchange market. GCI's obligation to comply with a complex web of international and local laws is also a substantial risk. Failing to comply with regulations might lead to legal actions, fines, and penalties. Apart from possible unexpected costs, this is also likely to lead to substantial reputational damage.

The company's asset-lite business model also means low barriers to entry for potential new competition. CGI has a solid brand, and the company should be committed to sustaining its positive image, which will differentiate it from new entrants with no track record.

Bottom line

To conclude, GIB is a "Hold". The company's ability to deliver notable profitability expansion over the long term despite almost no revenue growth is impressive. In my opinion, the expansion of profitability metrics is much better than the growth at all costs. I like the company's comprehensive geographical presence and diverse client services. The balance sheet is strong, and the company is ready to weather possible storms, even long ones. But my valuation analysis suggests that all these bullish signs are already priced in as the stock's fair value is only slightly higher than the current market price.

For further details see:

CGI Inc.: I Like The Business But Not The Valuation