GIB - CGI Inc.: Probably The Best Canadian Consulting Stock

2023-04-04 22:15:39 ET

Summary

- CGI Inc. is a $22.5-billion market cap Canadian firm that specializes in IT and business consulting services, founded in 1976 and headquartered in Montréal.

- The stock has grown by 1558% over the last 18+ years, which equates to a CAGR of 16.7%.

- In Q1 FY2023, the company reported growth in constant currency across all segments, industries, and service offerings.

- As far as valuation multiples are concerned, the market sets a strong contraction, which, as I think, is unlikely against the background of such an active share buyback.

- I have set a year-end price target of $115.5 per share based on a P/E of 21x and full-year EPS of $5.5 [7.8% above consensus]. Thus the upside is +18.12%.

The Company

CGI Inc. ( GIB ) ( GIB.A:CA ) is a $22.5-billion market cap Canadian firm that specializes in IT and business consulting services, founded in 1976 and headquartered in Montréal. They have a global team of approximately 90,250 professionals [+10.1% YoY] who are referred to as members and are also owners through their share purchase plan, according to the company's most recent 6-K filing [fiscal Q1 FY2023].

CGI's portfolio encompasses business and strategic IT consulting and systems integration services, managed IT and business process services, and intellectual property solutions. CGI's services enable clients to increase agility, scalability, and resilience while achieving operational efficiencies, innovations, and reduced costs. They also ensure security and data privacy controls are embedded into their solutions.

The success of a publicly traded company is measured primarily by the total return it has generated for its investors since going public. Since the company does not pay dividends, you need to look at the growth in its stock price. According to TIKR Terminal, GIB stock has grown by 1558% over the last 18+ years, which equates to a CAGR of 16.7% - obviously, the company was quite well managed, as investors received such a growth rate:

{kind=link}

According to CGI's latest IR presentation , the management differentiates the company's revenue streams into 3 categories:

- Service type: a) Managed IT and business services and b) Business and strategic IT consulting;

- Client geography - 8 distinct regions across the globe with the highest presence in North America [48% of total sales];

- Vertical Market : 5 presence end-markets, with "Government" being the biggest [35%].

CGI's latest IR material, Seeking Alpha [Q1 2023 data]

{kind=link}

As the company's history shows, such a wide diversification of the company's portfolio has enabled CGI to systematically increase its financials - since 2007, revenue per share and EPS figures have increased at a CAGR of 8.17% and 11.78%, respectively.

Author's work [ROIC.ai, Seeking Alpha data]

{kind=link}

Over the same period - since 2007 - the total number of shares outstanding has decreased by 27.4% [CAGR = -1.9%] and CGI's average annual P/E ratio has increased by 49.6% [CAGR = 2.4%]. For this reason, shares grew at a large premium to the company's financial growth - a systematic reduction in the number of shares outstanding increased the P/E ratio and created an "imaginary" comparative overvaluation. I will elaborate on this point in the next section of this article, which is about estimating CGI's price target. But without going into valuation now, and looking only at the financials, it's clear that one cannot approach assessing this stock's fair value by just comparing the current P/E multiple to its historical figures - that will not work.

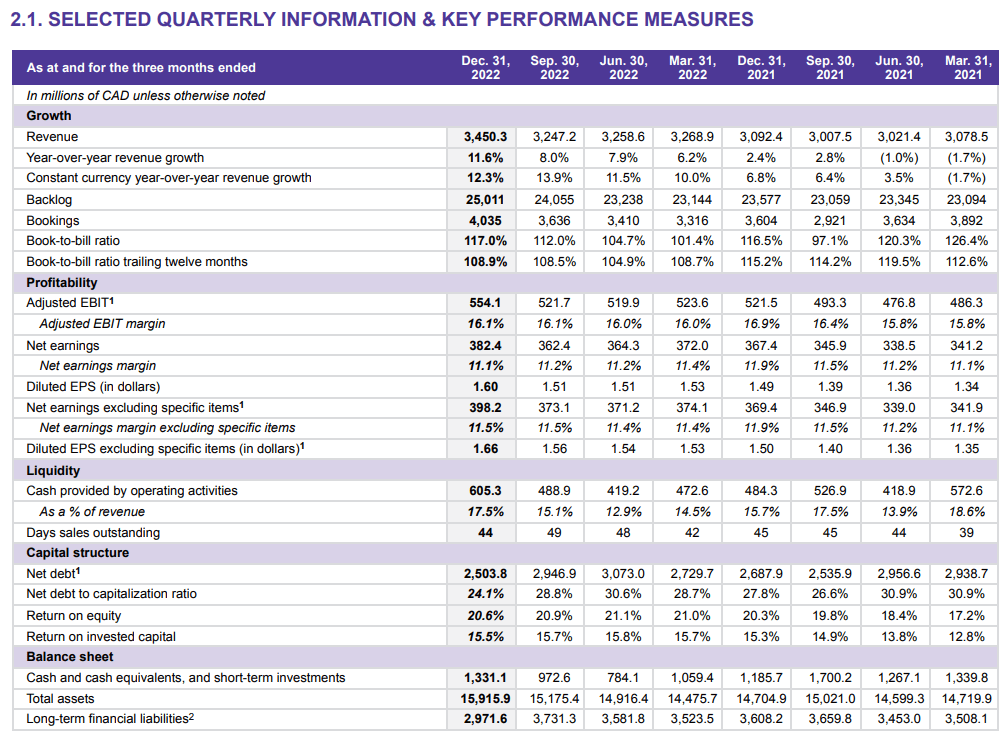

Now I suggest you look at the financials for the last quarter. In Q1 FY2023, CGI reported CAD 3.45 billion, an increase of 11.6% year-on-year, or 12.3% excluding currency effects. The company reported growth in constant currency across all segments, industries, and service offerings [take a look at the revenue mix above]. The Western and Southern Europe, Asia Pacific, and the United Kingdom and Australia segments recorded double-digit growth. Total bookings reached CAD 4 billion [ a record high], resulting in a book-to-bill ratio of 117% for the quarter and 109% for the trailing 12 months. CGI's IP revenue increased in all geographic segments and represented 21.7% of total revenue in Q1. Adjusted EBIT was CAD 554.1 million with an EBIT margin of 16.1%, down 80 basis points due to prior-year acquisitions and higher travel costs. Net income increased to CAD 382.4 million, with diluted EPS of CAD 1.60, up 7.4% YoY.

CGI's latest IR material, Seeking Alpha [Q1 2023 data]

{kind=link}

Yes, the margins have felt across the income statement line, but CGI's return on invested capital [ROIC] amounted to 15.5% - an improvement of 20 basis points, YoY. This is actually one of the highest ratios in the company's history as far as I see.

CGI's latest IR material, Seeking Alpha [Q1 2023 data]

{kind=link}

Cash provided by operating activities was CAD 605 million, an improvement from the previous year. CGI now has a net-debt-to-capitalization ratio of 24.1% and CAD 2.8 billion in cash reserves. The company approved the extension of the NCIB program through February 2024, allowing for the repurchase of up to 18.8 million shares over the next 12 months.

It's remarkable, that 1/3 of the record high bookings in Q1 2023 were comprised of new business engagements, according to the company's CEO, George Schindler. CGI had many long-term digitization engagements in the quarter, including:

- A 10-year agreement with the US Department of State to continue delivering US visa application services in India, using CGI's Atlas360 IP solution;

- A 4-year agreement with the UK government to manage the cybersecurity analytics platform for one of its departments, with new scope focused on iterative development, delivery, and evolution of the platform, and development of a data as a service function to address evolving cyber threats;

- A 5-year managed services agreement with Sodexo to drive digital transformation using CGI's proximity and offshore delivery model

- A 5-year expanded agreement with Laurentian Bank of Canada to manage digitization, strengthen operational efficiencies, and enhance customer experience, with a co-innovation fund focused on transforming the bank's ecosystem;

- Named one of Airbus' major global partners to drive the end-to-end digital transformation of corporate and central services functions over the next 5 years, leveraging CGI's operations in France, Spain, Germany, and India.

Already after the report, we can judge from the latest news that the bookings and the backlog keep peeling up, giving investors a good sign:

SA News, author's notes

Given the huge backlog, I expect the company to be able to continue to actively grow sales and EPS in FY2023 and FY2024, despite all the difficulties. I do not see any obvious red flags, neither in the unit-economic ratios nor in the basic financial analysis ratios.

{kind=link}

Let's now turn to valuation and expectations - the two factors that, along with the company's financial health, should lead CGI's stock for the foreseeable future.

Valuation & Expectations

As previously mentioned, CGI's current P/E ratio cannot be compared to historical levels due to the company's ongoing share buyback program, which reduces the share count and inflates the stock price, resulting in an artificial overvaluation that is likely to persist in the future. However, it's worth noting that many companies in the S&P 500 Index ( SPX ) engage in similar practices, so it may be more useful to evaluate CGI's multiple to the SPX.

Author's work [ROIC.ai, Seeking Alpha data]

{kind=link}

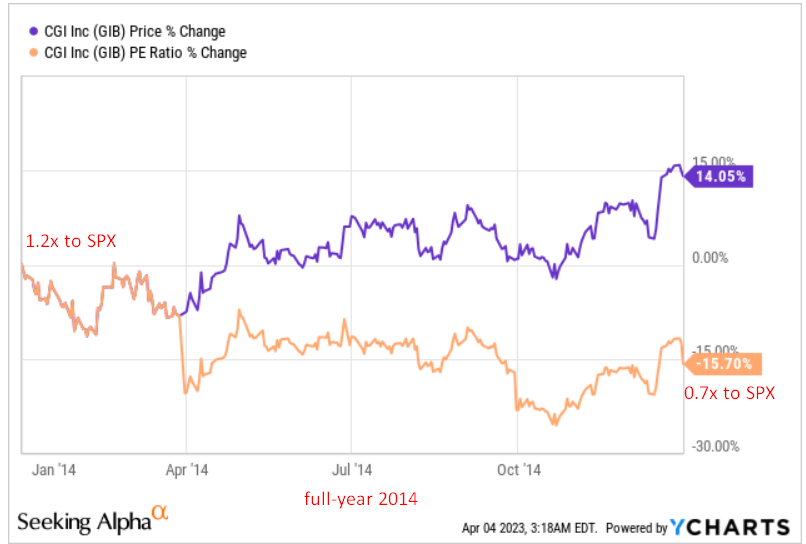

The company is currently trading at a ratio of about 1x to the SPX's one, which is quite a lot by historical standards. However, in 2013, this value was even higher - 1.2x - and that did not stop the stock from rising 14.05% amid a multiple contraction of 15.7%:

YCharts, GIB stock, author's notes

{kind=link}

By the 1st quarter of fiscal 2024, the company is authorized to repurchase up to 18.8 million shares of Class A common stock, representing approximately 7.9% of all of the company's outstanding shares, based on Seeking Alpha financial data . Accordingly, even if this program is not fully implemented, we should expect a strong reduction in the denominator of the fraction in next year's EPS calculation .

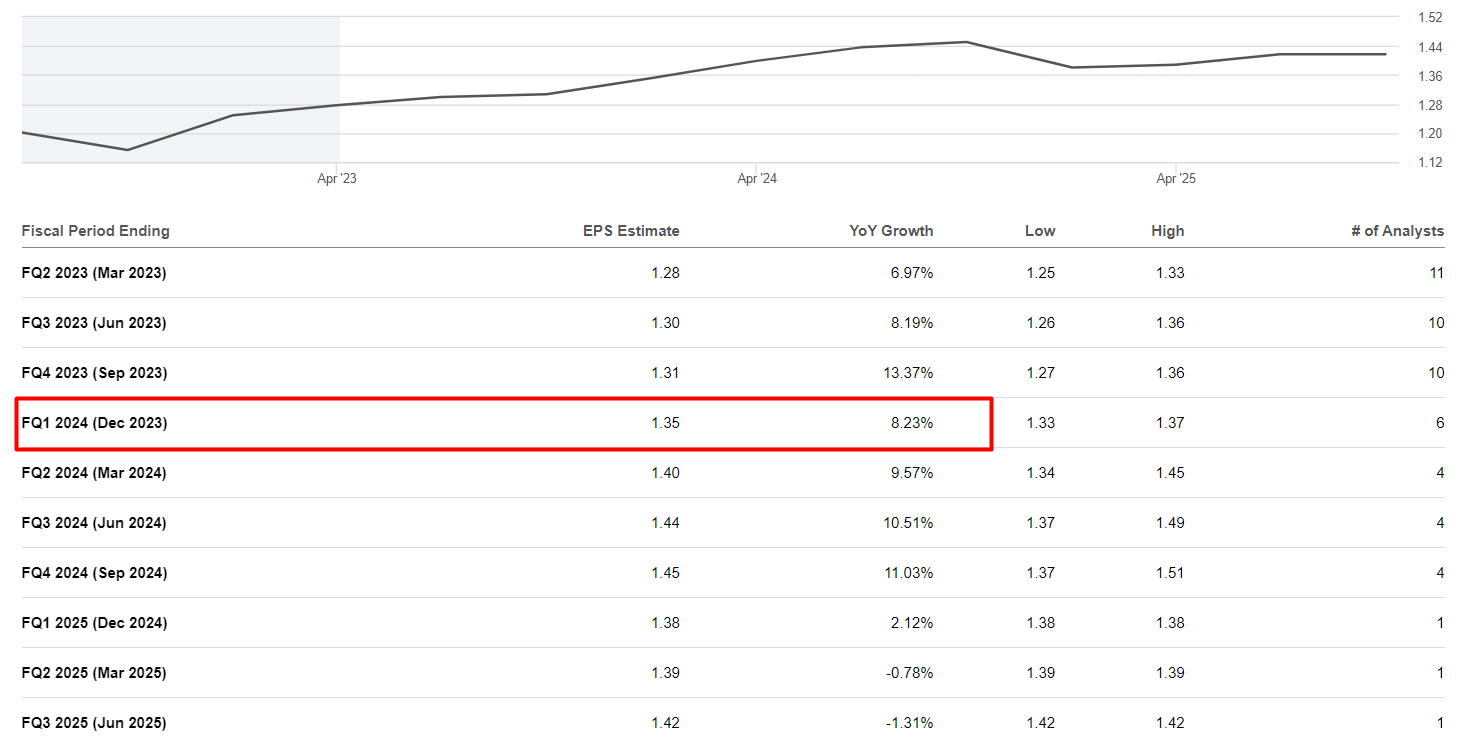

We should keep this in mind when we look at the forecasts of Wall Street analysts, who expect organic EPS growth of just 1-3% for the foreseeable future [taking into account the reduction in the number of shares].

{kind=link}

In addition, CGI should receive a strong tailwind for Q2 FY2023 numbers from the weakening dollar ( DXY ) since the beginning of March due to the fairly broad geographical spread of its business:

Seeking Alpha, DXY, author's notes

{kind=link}

So the consensus EPS growth of 6.97% for Q2 FY2023 seems too low to me - the company has entered into a private agreement with CDPQ to purchase 3.3 million of its Class A subordinate voting shares at $119.58/share, according to Seeking Alpha , and closed the transaction on February 28, 2023. That's already a 1.4% accretion to EPS. As a result, I expect CGI to again beat the Street's consensus on April 26, 2023 [estimated earnings release day].

As far as valuation multiples are concerned, the market sets a strong contraction, which, as I said, is unlikely against the background of such an active share buyback.

{kind=link}

Therefore, I conclude that what appears at first glance to be an overvaluation is largely a fiction - the multiple contraction set for the coming years will most likely not become a reality, and in the next few quarters the actual EPS and revenue numbers will most likely exceed expectations due to the weakening dollar and initially low consensus forecasts.

Summary Thesis

My thesis has risks that must be taken into account. Perhaps the analysts know something I do not, and accordingly, their conclusions about slowing EPS growth and sales soon and assuming a multiple contraction, are reasonable. I am also embarrassed by the 10.1% headcount increase in just one year - CGI will most likely need to optimize costs going forward, otherwise, margins will continue to suffer. This will become especially relevant against the backdrop of a very likely recession in the U.S. - one of the largest end markets for the company.

Despite the risks, I do not think management would have bloated the workforce as much if it had not seen the growing demand for CGI's services - I think the increasing bookings and backlog, which continue to grow, show us the potential for rapid EPS growth in the future against a backdrop of continued share buybacks. The valuation is always likely to be overvalued, which should not prevent the stock from rising further, as it did during similar overvaluation levels in 2013-2014.

I have set a year-end price target of $115.5 per share based on a P/E of 21x and full-year EPS of $5.5 [7.8% above consensus]. Thus the upside is +18.12%.

Thank you for reading!

For further details see:

CGI Inc.: Probably The Best Canadian Consulting Stock