CHPT - ChargePoint: Can They Turn The Corner?

2023-12-21 10:11:10 ET

Summary

- ChargePoint Holdings, Inc. is in the electric vehicle charging infrastructure industry, which is expected to experience increasing demand.

- The company's financial situation is unattractive, with declining revenue and negative margins.

- They plan to reach positive Adjusted EBITDA in Q4 2024.

- Because of their financials and guidance, I cannot justify initiating a position.

- I currently rate CHPT as a Hold.

Thesis

ChargePoint Holdings, Inc. (CHPT) is in an industry which I expect to experience increasing demand for years to come. However, their financial situation was far too unattractive the last time I reviewed them as a potential investment, and it's only gotten worse since then. This is an update to my last article . After looking over their financials and valuation, I presently rate ChargePoint as a Hold.

Company Background

ChargePoint provides electric vehicle charging infrastructure and software. They are headquartered in Campbell, California and were originally founded in 2007 under the name Coulomb Technologies.

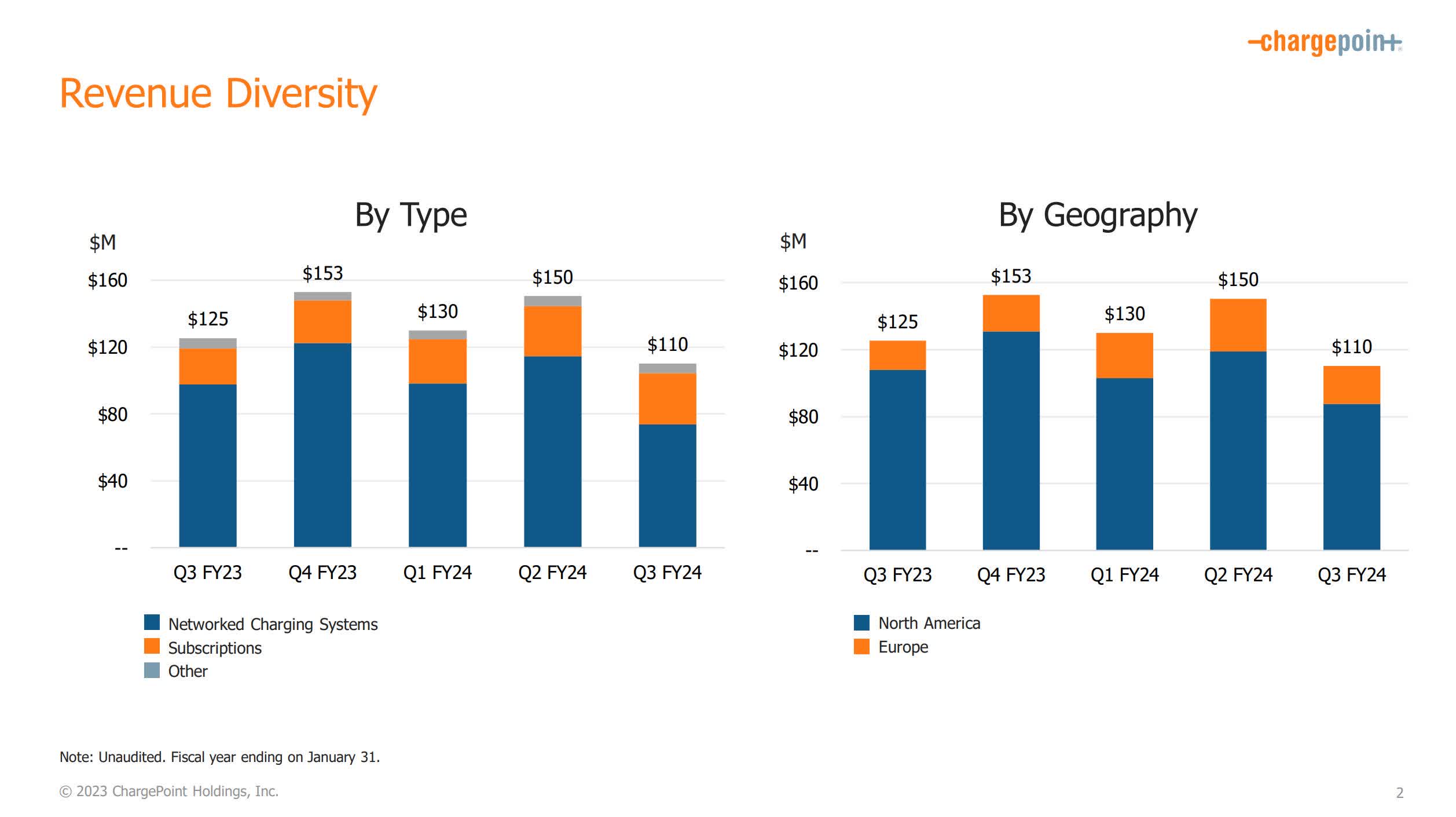

CHPT Revenue Diversity (Q3 2023 Presentation Page 2)

{kind=link}

Long-Term Trends

The global electric vehicle charging station industry is expected to experience a CAGR of 30.26% until 2028. The global electric vehicles market is projected to have a CAGR of 10.07% until 2028. Within just the United States, the charging market is projected to have a CAGR of 24% through 2028, and for the electric vehicle market it's a CAGR of 44.43% .

Guidance

Their most recent earnings call transcript can be found here . I am only going to cover some of the highlights from it. Investors should read it in its entirety.

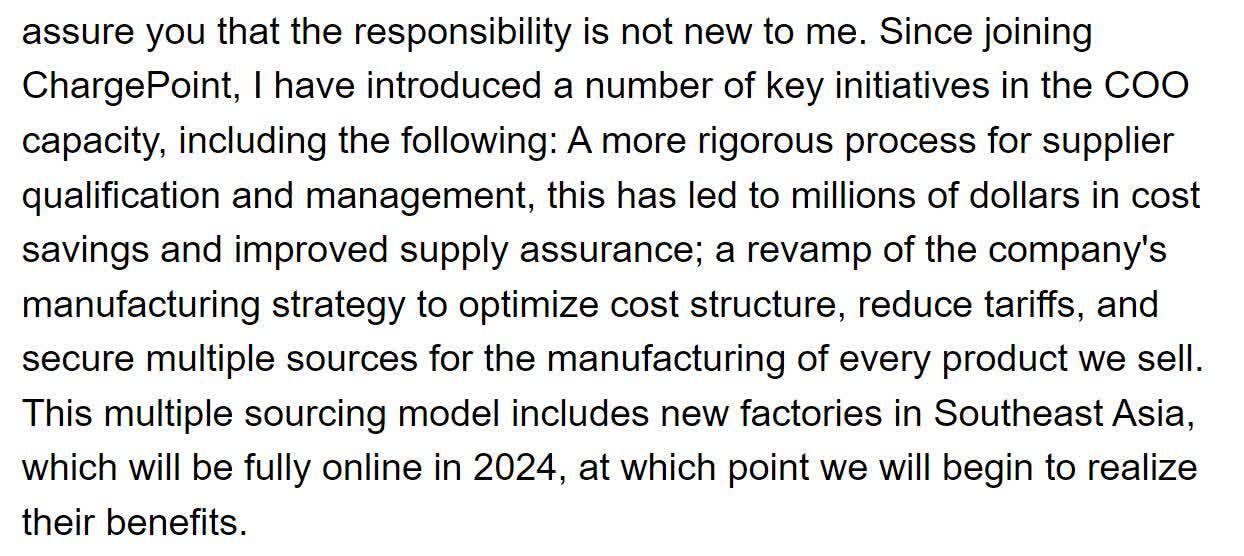

The Chief Operations Officer has stepped up into the CEO role. They plan on continuing the cost savings initiatives they were working on when they were the COO. The company expects to bring new manufacturing capability in Southeast Asia online in 2024.

Guidance 1 (Q3 2023 Earnings Call Transcript)

{kind=link}

They believe they may be able to reach positive Adjusted EBITDA in Q4 of 2024.

Guidance 2 (Q3 2023 Earnings Call Transcript)

{kind=link}

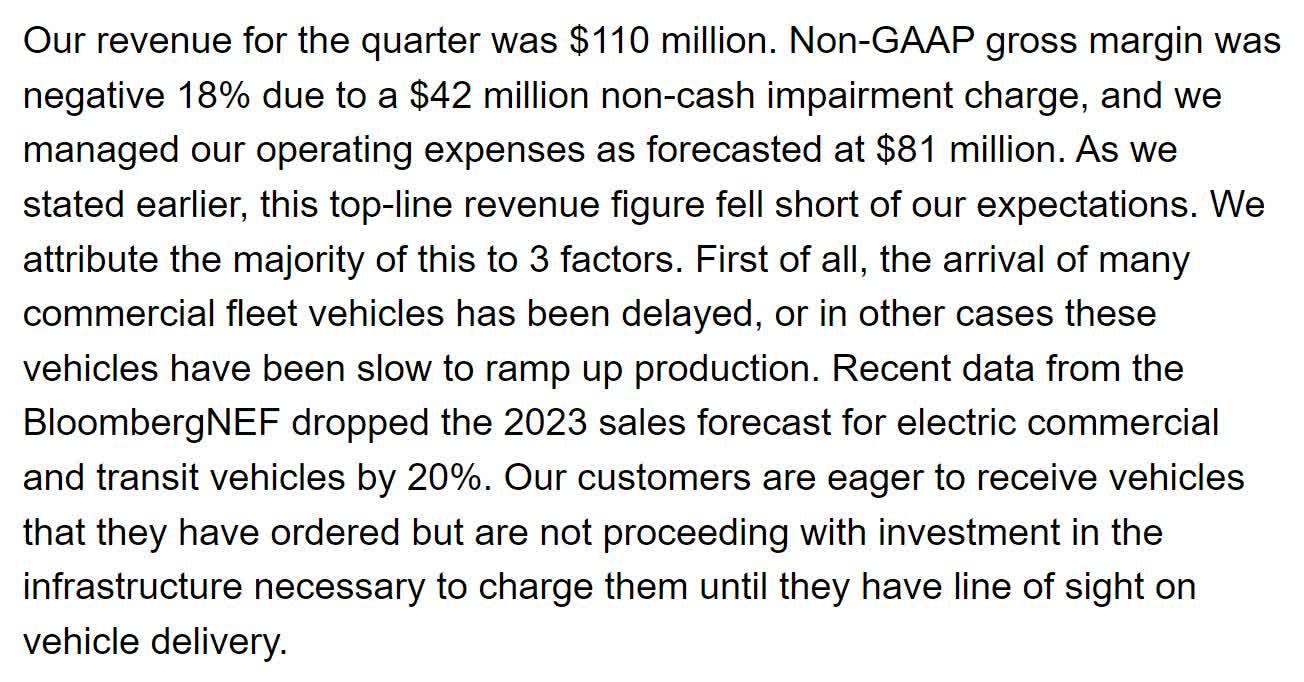

Revenue fell short of expectations this quarter due to EV delivery delays which resulted in a decline in demand.

Guidance 3 (Q3 2023 Earnings Call Transcript)

{kind=link}

Their downstream supply chain has moved to more of an on-demand model and is no longer carrying as much inventory.

Guidance 4 (Q3 2023 Earnings Call Transcript)

{kind=link}

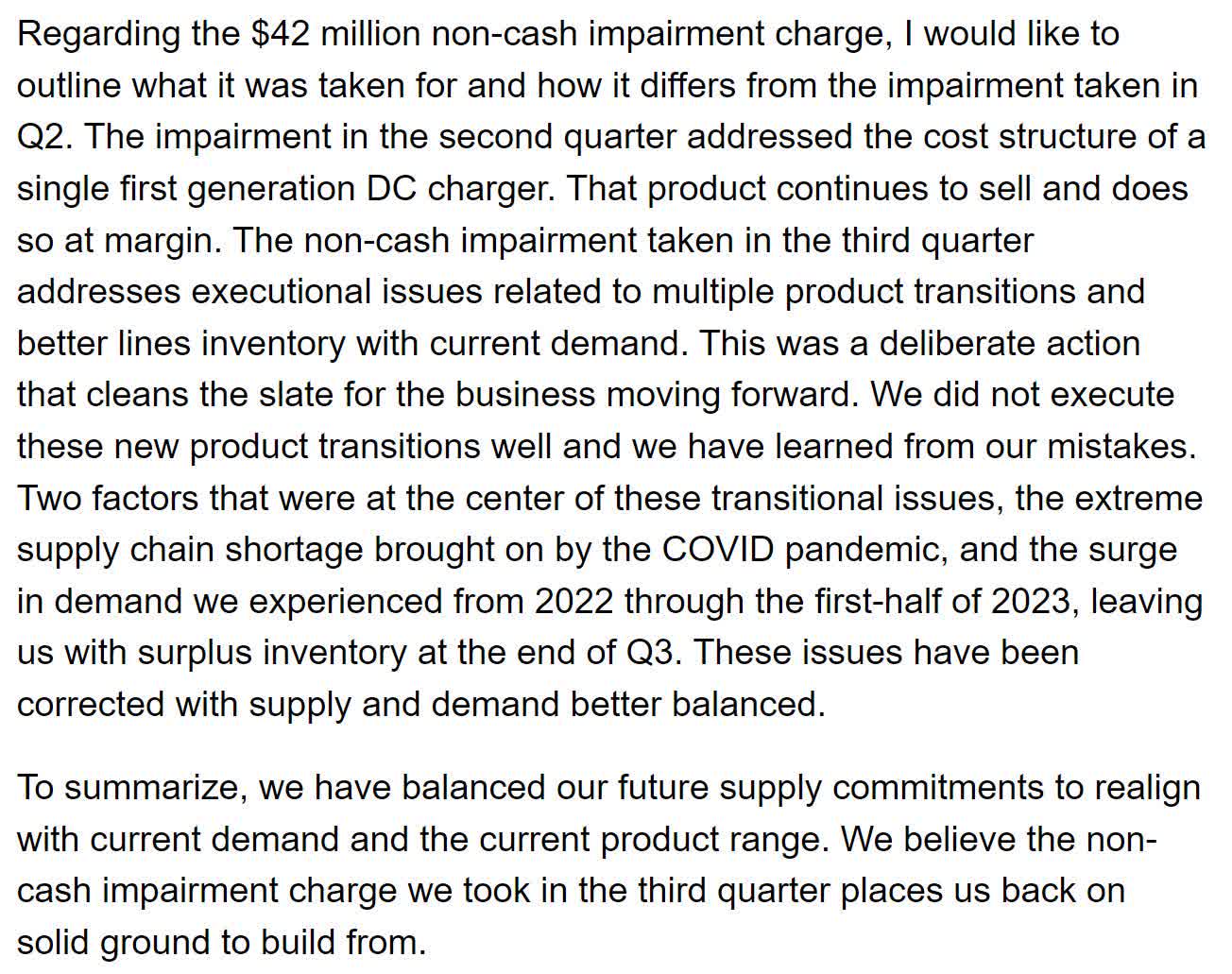

They took a $42M non-cash impairment due to a product transition. They had a significant amount of hardware in their inventory which there was not enough demand for. I believe this is a reference to being forced to transition to the North American Charging Standard.

Guidance 5 (Q3 2023 Earnings Call Transcript)

{kind=link}

They increased their cash on hand from $232M to $397M. Considering that their total common shares outstanding increased from 359.8M in Q2 to 417.9M in Q3, I view this dilution as an attempt to give the company additional time before they will run out of cash.

Guidance 6 (Q3 2023 Earnings Call Transcript)

{kind=link}

They began to roll out their North American Charging Standard compliant hardware. The company also performed a major update to their driver app.

Guidance 7 (Q3 2023 Earnings Call Transcript)

{kind=link}

The amount of energy dispensed through their chargers rose by 18% over the quarter. YoY, this was a 70% increase. They signed another contract with a German sports car manufacturer to use their software. ChargePoint also brought online the first station for their Mercedes-Benz charging network in Atlanta.

Guidance 8 (Q3 2023 Earnings Call Transcript)

{kind=link}

They continue to maintain a significant network of both customers and infrastructure.

Guidance 9 (Q3 2023 Earnings Call Transcript)

{kind=link}

They did not give guidance for this upcoming Q4, but plan on resuming regular guidance next quarter.

Guidance 10 (Q3 2023 Earnings Call Transcript)

{kind=link}

Quarterly Financials

Their quarterly financials are showing the company was steadily growing revenue until January of 2023. Eight quarters ago ChargePoint had a quarterly revenue of $65M. Four quarters ago that had increased to $125.3M. By this most recent quarter that had declined to $110.3M. This represents a total two-year increase of 69.69% at an average quarterly rate of 8.71%.

CHPT Quarterly Revenue (By Author)

{kind=link}

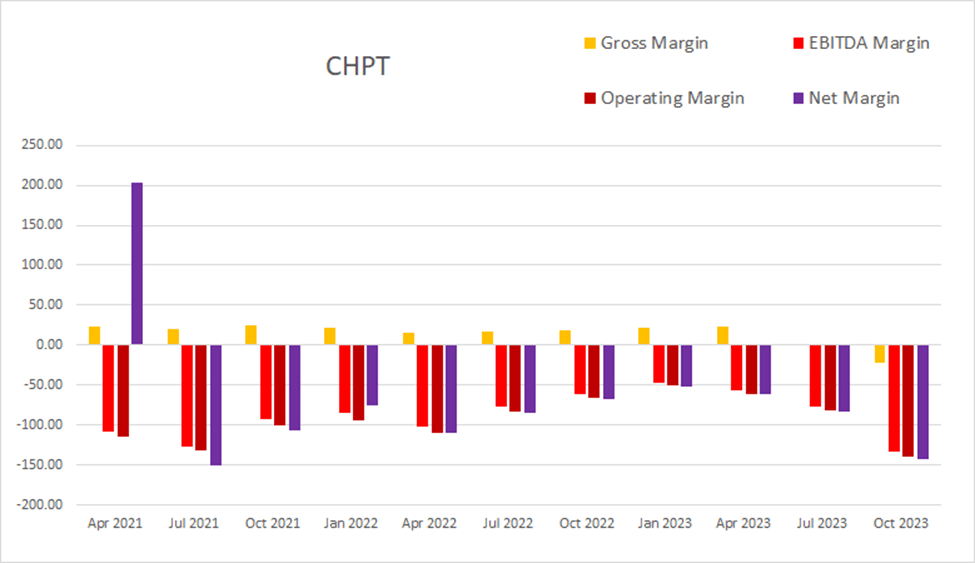

Their already low gross margins have declined over the last two quarters. As of the most recent quarter gross margins were -21.67%, EBITDA margins were -132.91%, operating margins were -139.44%, and net margins were at -143.43%.

CHPT Quarterly Margins (By Author)

{kind=link}

The sum of their last eight quarters of dilution comes to 24.55%; over the last four quarters the pace of dilution has increased and comes to 21.41%.

CHPT Quarterly Chare Count vs. Cash vs. Income (By Author)

{kind=link}

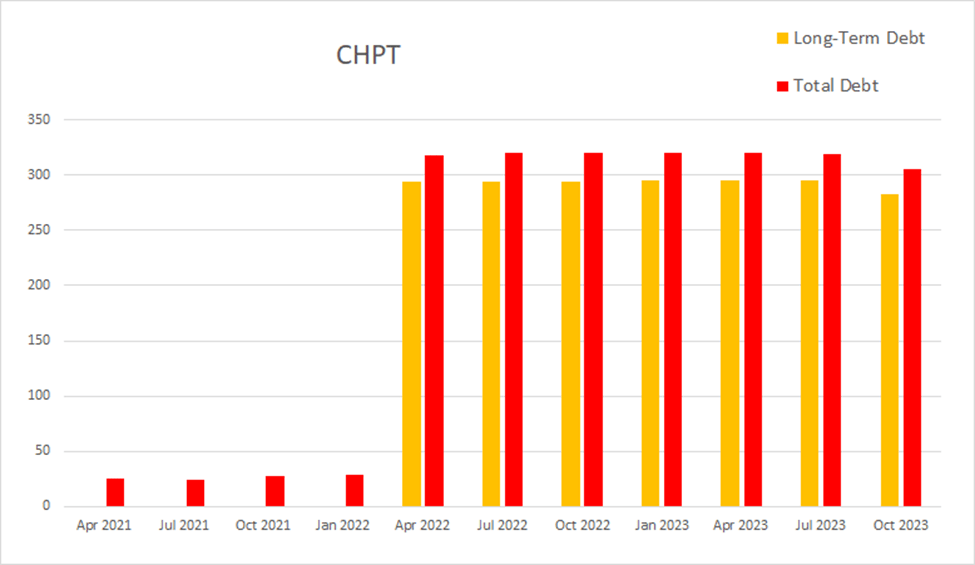

The most recent quarter, ChargePoint had -$2M in net interest expense, total debt was at $305.6M, and long-term debt was at $282.7M.

CHPT Quarterly Debt (By Author)

{kind=link}

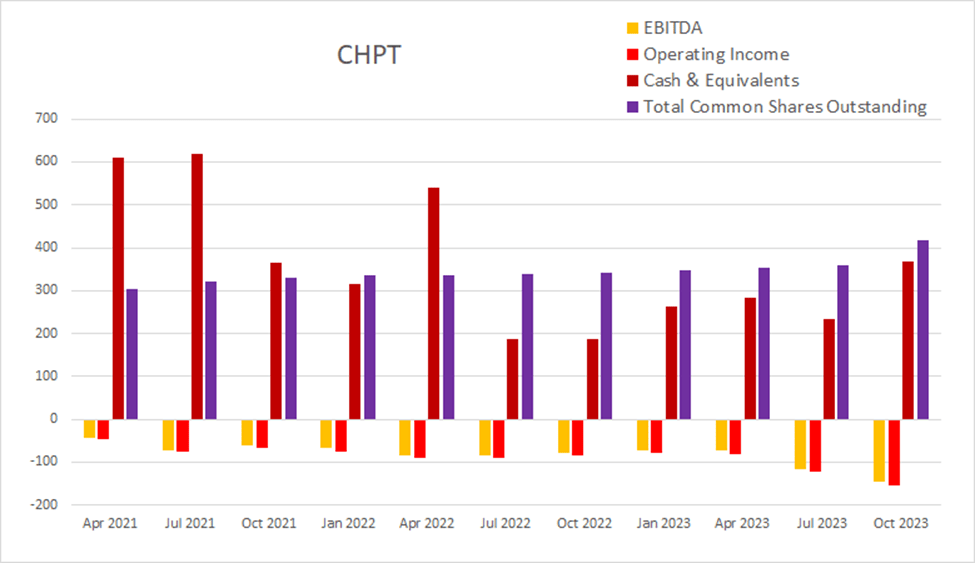

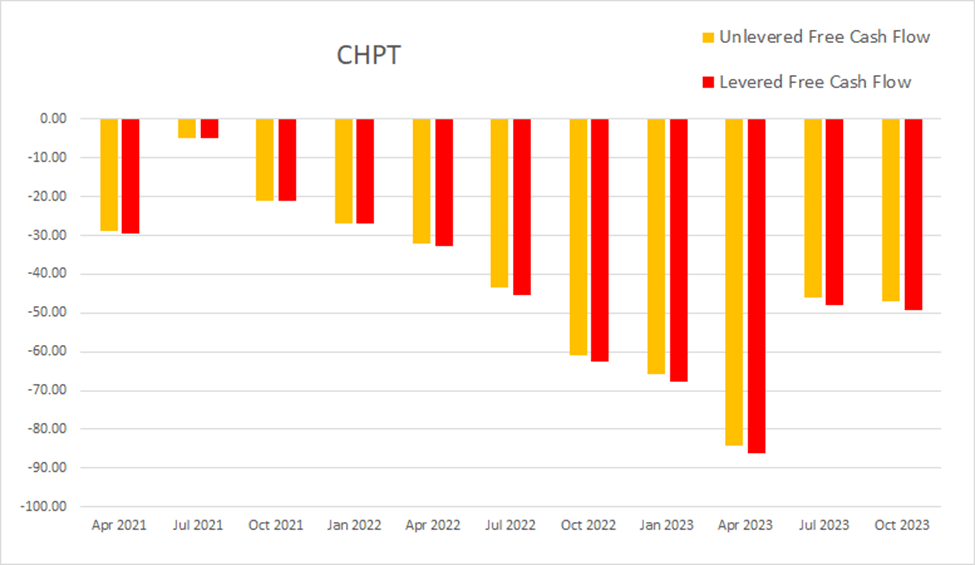

As of the most recent earnings report, cash and equivalents were $367M, quarterly operating income was -$154M, EBITDA was -$146.6M, net income was -$158.2M, unlevered free cash flow was -$46.90M, and levered free cash flow was -$49.3M.

CHPT Quarterly Cash Flow (By Author)

{kind=link}

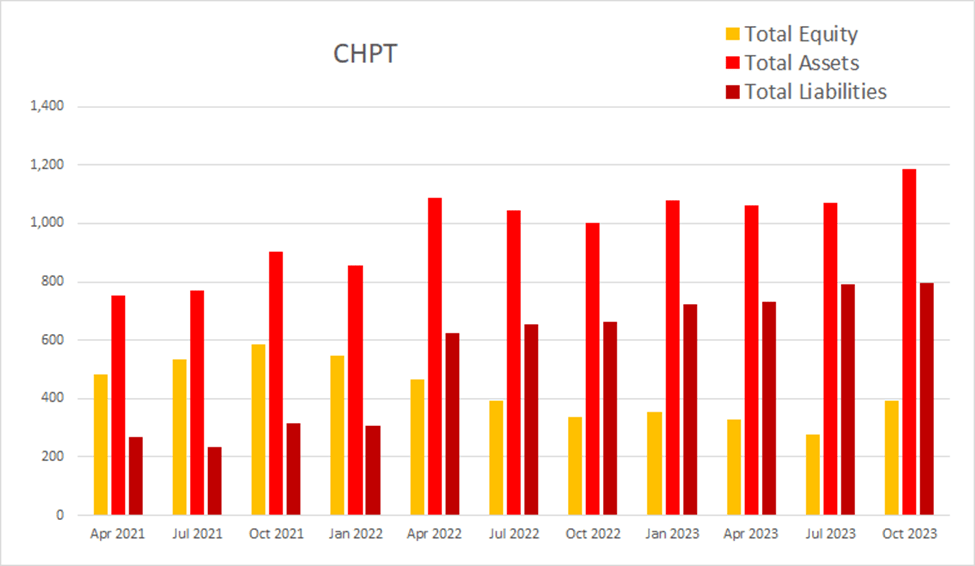

Total equity fell from October of 2021 before reaching a low in July of 2023. It rose again this most recent quarter.

CHPT Quarterly Total Equity (By Author)

{kind=link}

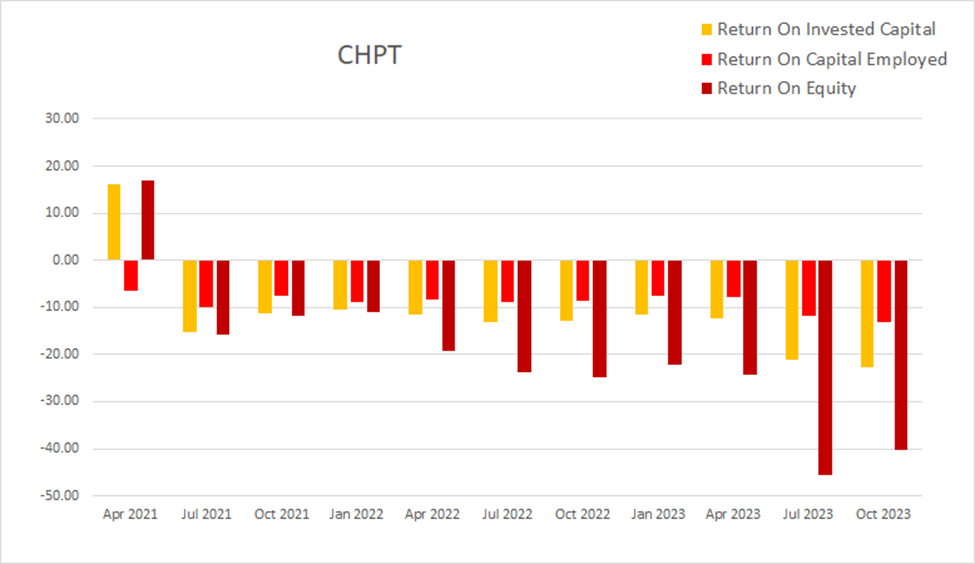

Their returns remain negative. As of the most recent earnings report ROIC was -22.66%, ROCE was -13.20%, and ROE was -40.30%.

CHPT Quarterly Returns (By Author)

{kind=link}

Valuation

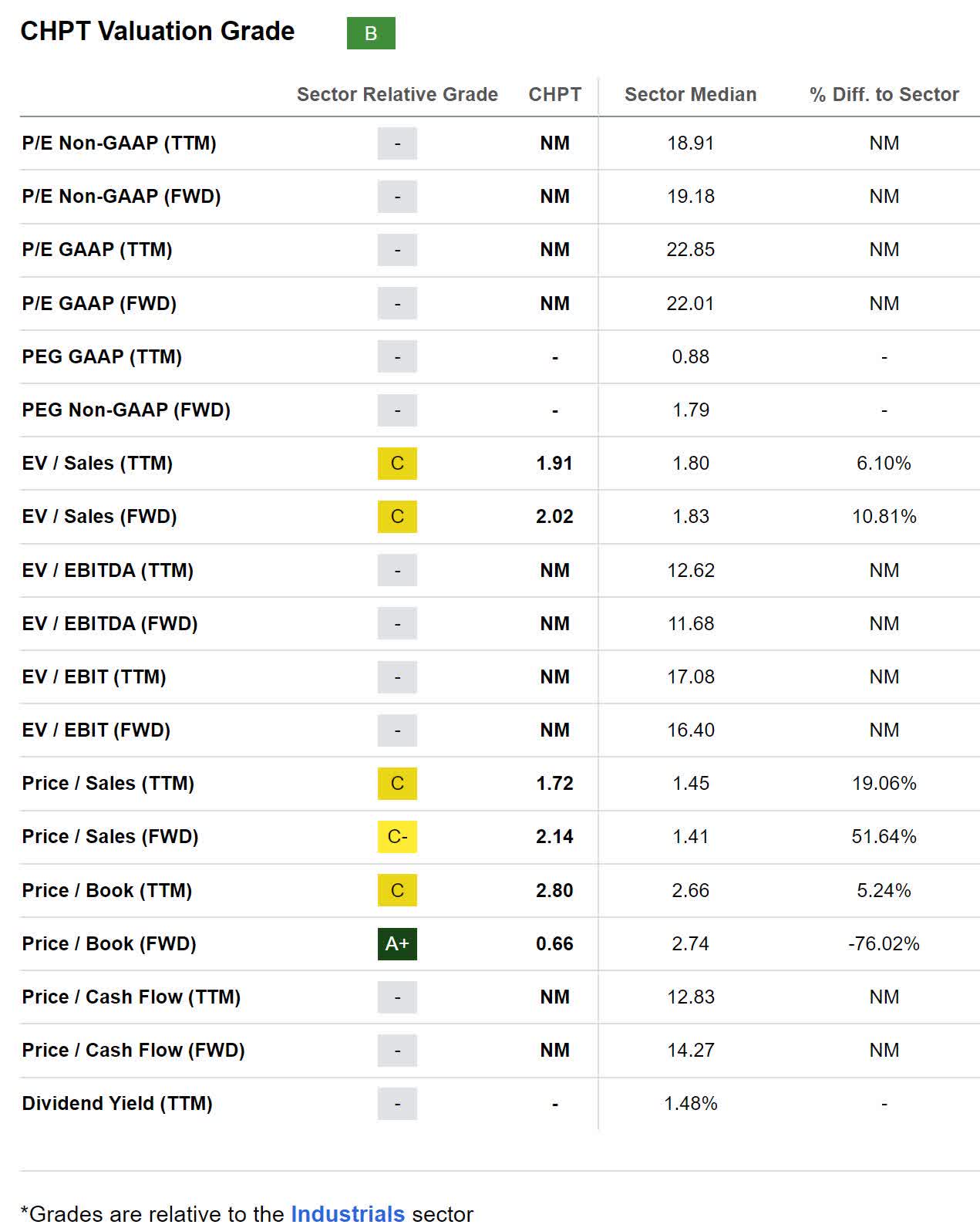

As of December 10th, 2023, ChargePoint had a market capitalization of $1.10B and traded for $2.48 per share. They are not net income positive and have negative EBITDA and cash flow, so most of the valuation methods I am used to employing are useless. This most recent quarter, their tangible book value per share was at $0.24.

CHPT Valuation (Seeking Alpha)

{kind=link}

Risks

Because they recently raised cash, ChargePoint is now less likely to have to dilute again in the near future. This does not mean they won't have to dilute again before they reach positive cash flow. If they don't improve their cash flow situation, as they run low on cash the risk of future dilution will increase.

If they do not improve their gross margins, no amount of revenue growth will improve their cash flow situation. Even if they return to the gross margins they were typically experiencing before the recent decline, the company would have to go through significant efficiency improvements to find themselves actually profitable.

CHPT Quarterly Margin Table (By Author)

{kind=link}

Catalysts

The company is currently extremely unprofitable. Although their goal of reaching positive Adjusted EBITDA is a step in the right direction, I believe a significant rise in share price will not happen until they reach positive cash flow.

Conclusions

Overall, this appears to be a low margin business model with a significant spending problem. Considering they don't expect to even reach Adjusted EBITDA positive until Q4 2024, I consider them absolutely uninvestible. While this may change in coming years, I don't have high hopes that they will be able to turn the corner into profitability for quite some time. The long-term trends around EV use incentivize me to not dismiss the charging infrastructure industry entirely, so I will continue checking in on ChargePoint from time to time.

For further details see:

ChargePoint: Can They Turn The Corner?