CHPT - ChargePoint: Excellent Operating Efficiency - Buy At The Next Dip

2023-03-23 16:00:00 ET

Summary

- While the uncertain macroeconomic outlook may have impacted CHPT's execution and market sentiments, its long-term prospects remain stellar.

- The company's operating expenses remained stable over the past four quarters, despite the +87.2% expansion in its top line.

- The US and EU have adopted legislation that will continue to boost EV sales and market share through 2030 and 2035, respectively.

- We believe CHPT still has a chance at success as long as it maintains its liquidity and achieves positive FCF by the end of FY2024.

- Therefore, we continue to rate CHPT as a speculative buy at its next dip.

The EV Investment Thesis Is Not Dead

ChargePoint (CHPT) had been overly beaten in our view, attributed to the double misses in the recent FQ4'23 earnings call and softer FQ1'24 guidance. However, after listening closely to its earnings call, we reckoned the market had overreacted.

The company guided for positive Free Cash Flow [FCF] generation by the end of FY2024, suggesting improved liquidity by then. We had already observed an improving gross margin of 21.8%, operating margins of -49%, and FCF margins of -35.9% by FQ4'23, compared to FQ1'23 levels of 14.8%, -110%, and -90.7%, respectively.

It seems apparent that CHPT has been aggressively reining in costs as well, with operating expenses remaining stable at an average of ~$106M over the past four quarters, despite the +87.2% expansion in its top line at the same time.

Therefore, we remain optimistic about its long-term success, especially aided by the growing adoption of EVs in the US and EU. In 2022, EV sales grew by +61.3%/ +281.75K units YoY in the US to 741.17K units, comprising 5.4% of all cars sold, compared to 2021 levels of 459.42 units and 3%. In the EU, the sum was even more impressive, with 1.58M EVs sold in 2022, comprising 14% ( +4 points YoY ) of total vehicles sold.

With the US targeting " half of all cars sold to be battery-electric, plug-in hybrid or fuel cell-powered" by 2030 and the EU still committed to its ban on the sale of combustion engine vehicles by 2035, we reckon CHPT's path to potential success is not for impatient investors.

We understand the pessimism surrounding EV charging stocks, attributed to the inherent reliability issues in the US power grids. Technically, CHPT has been acting as a middle-man for utility companies and EV users, by monetizing electricity as a commodity, amongst others. Many other oil/gas companies have also entered the foray, such as Shell ( SHEL ) and BP ( BP ), implying intense competition and tighter margins moving forward.

CHPT also faces growing competition from those offering home charging solutions, such as Tesla ( TSLA ) and Enphase Energy ( ENPH ). However, we believe these examples only prove that EVs and their charging solutions/platforms are here to stay, offering drivers another way to commute and fuel up at the same time.

One way or another, the infrastructure build-up will occur over time, significantly aided by legislative funding despite the inherent electrification challenges. While market consolidation may happen over the next two years of pessimistic macroeconomics, as witnessed with Volta's acquisition, CHPT may still fare decently moving forward.

This is significantly aided by the company's expanded partnerships with multiple OEMs, growing footprint, improving software/ hardwares, and increasing annualized subscription revenue of $100M (+49.5% YoY) by the latest quarter. As a result, CHPT's investors need not be discouraged by short-term headwinds in our opinion.

So, Is CHPT Stock A Buy , Sell, or Hold?

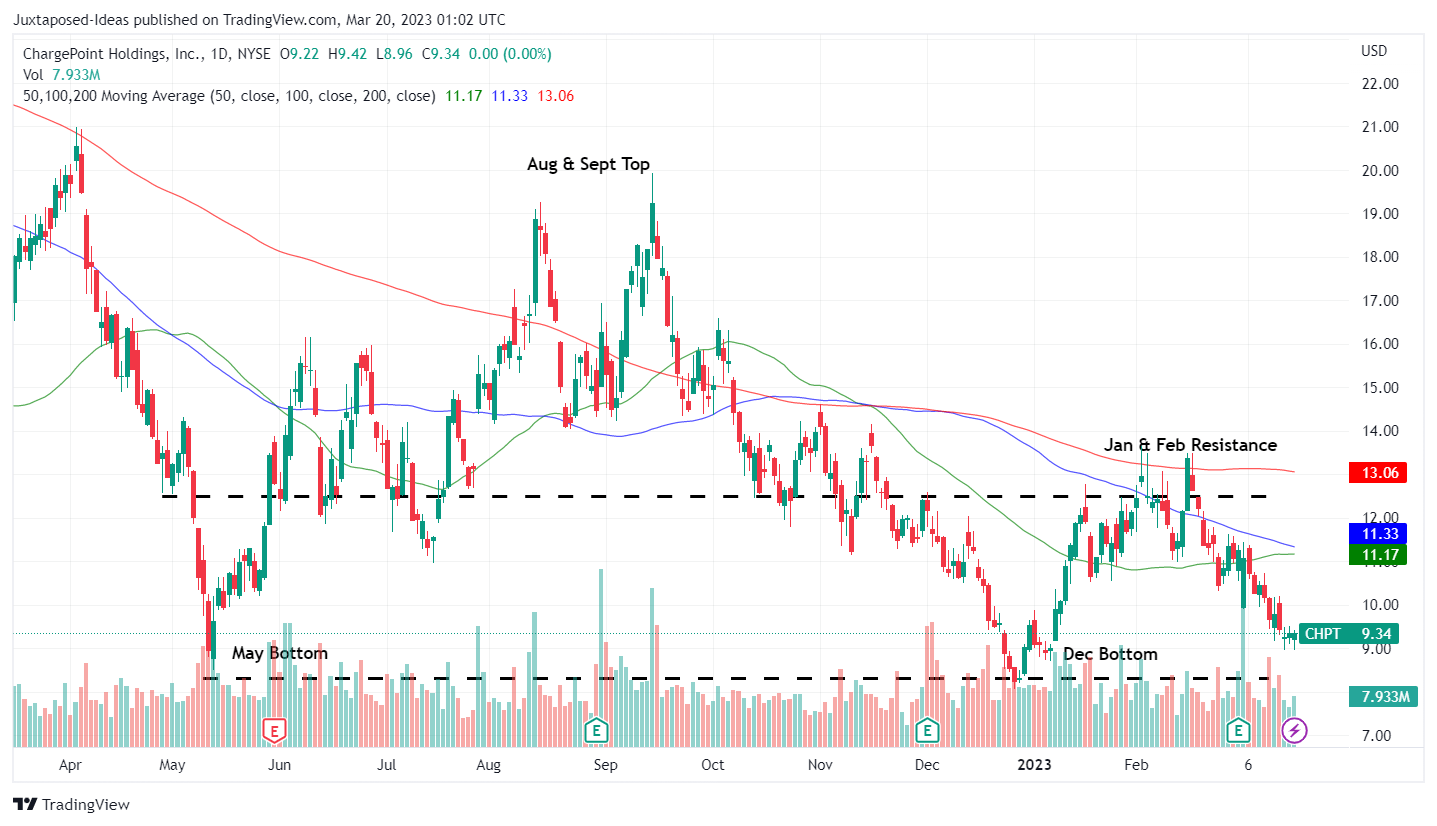

CHPT 1Y Stock Price

CHPT 1Y Stock Price (Trading View)

{kind=link}

At the time of writing, the CHPT stock had lost -14.1% of its value, mostly attributed to its unsatisfactory forward guidance. The company expects to report FQ1'24 revenues of $127M (-16.9% QoQ and +55.5% YoY) at the midpoint, against the consensus estimate of $156.7M (+2.5% QoQ and +91.9% YoY).

CHPT's prudent numbers were likely attributed to a few factors.

Firstly, the company previously raised its FQ4'23 and FY2023 guidance too optimistically by $5M at the midpoint in Q3, leading to the wider quarterly top-line miss of -$11.71M in Q4 and fiscal year miss of -$13.79M.

While we understood the management's choice in offering a more prudent FQ1'24 guidance, the unexpectedly lower numbers naturally triggered a loss of confidence in its forward guidance and execution, as reflected in its stock prices.

Secondly, CHPT remained intrinsically linked to the overall health of the EV market, due to its market-leading position in global charging by footprint, similarly challenged by the opening up of TSLA's supercharging networks.

It was no secret by now that TSLA led the price war, cutting its prices across all its models in the US and China. This sparked market speculation about a reduction in discretionary spending around big-ticket items, such as EVs, whose MSRPs had risen tremendously, as discussed in our previous article here .

Meanwhile, EV sales in the US had drastically moderated in January 2023 to 66.41K units, declining by -16.2%/ -12.85K units MoM from December 2022 levels of 79.26K units. Then again, we must highlight that the first month of the year was usually a slower season, with sales already picking up by +11.4%/ +7.6K units MoM in February 2023 to 74.01K units.

However, with new vehicle inventories up by +61.8%/ +660K YoY to 1.73M units/ 57 days supply by January 2023 and up again by +68%/ +730K YoY to 1.8M units/ 56 days supply by February 2023 , the market fears of slower growth were understandable indeed. This was despite the reduced MSRP prices by multiple automakers and the Inflation Reduction Act's $7.5K in tax credits.

Lastly, the macroeconomic outlook remains uncertain through 2023, with the market pessimism likely at a fever pitch attributed to the failure of Silicon Valley Bank.

Combined with CHPT's continuous cash burn and a balance sheet of $369.13M by the latest quarter, it appears that the company tempered its top-line growth while conserving cash in the short term.

While not related to its forward guidance, market analysts already expected the company to raise more capital by the end of 2023, if not earlier, further diluting existing investors. Since its IPO in March 2021, its share count had grown by +56.8% to 342.8M by the latest quarter, attributed to stock sales and acquisitions thus far. Otherwise, it may also face higher lending costs, further impacting sentiments.

Therefore, the pessimism surrounding CHPT's forward execution is valid in our view, potentially triggering another December 2022 bottom test at around $8.25. Investors looking to add the global leader in EV charging may consider adding at those levels for an improved margin of safety for long-term investing.

Meanwhile, investors must also size their portfolios accordingly, due to the potential volatility.

For further details see:

ChargePoint: Excellent Operating Efficiency - Buy At The Next Dip