EVGO - ChargePoint: Looks Promising And Worrying At The Same Time

Summary

- ChargePoint has been able to demonstrate its ability to attract large customers and grow their spending over time.

- The company has a resilient "land & expand business" model, with 50% upfront revenue and 50% recurring revenue.

- Management reiterates that they expect free cash flow to turn positive by 4Q FY2024.

- My 1-year target price for ChargePoint is $13.50, representing 9% upside from current levels.

Investment thesis

I think that the investment thesis for ChargePoint ( CHPT ) is rather clear cut. It is a pure play on increasing EV penetration in the United States, while having additional upside from its expansion into the European market.

With global auto makers committing to making their vehicles electric as well as favorable regulation and incentives from governments all over the world for EVs, this bodes well for EV adoption in the next decade, which brings a secular tailwind to ChargePoint. As a result, the company is well positioned to enjoy a long runway of growth and margin expansion. As a result, I think of ChargePoint as being in the right place at the right time.

ChargePoint has a full suite of products for its different lines of businesses, a resilient land and expand model, and a strong and established customer base. While I like the EV charging market's secular tailwind, I think we are likely to see increasing competition over the years and I think that ChargePoint's stock is not pricing that in at all. I think that the company has balanced risk/reward profile and I think that there will be better entry points to enter the stock in the future.

Brief introduction

For those who are unfamiliar with ChargePoint, it is a California based company that is one of the leaders in the EV charging business. It has an EV charging network operating in North America and Europe. The company is a leader in North America and operating across verticals in the region and it is operating in 16 European markets.

To date, the company has more than 210,000 ChargePoint ports under management and more than 400,000 ports accessible via roaming.

Apart from the network of charging stations, ChargePoint provides a subscription software and services as well.

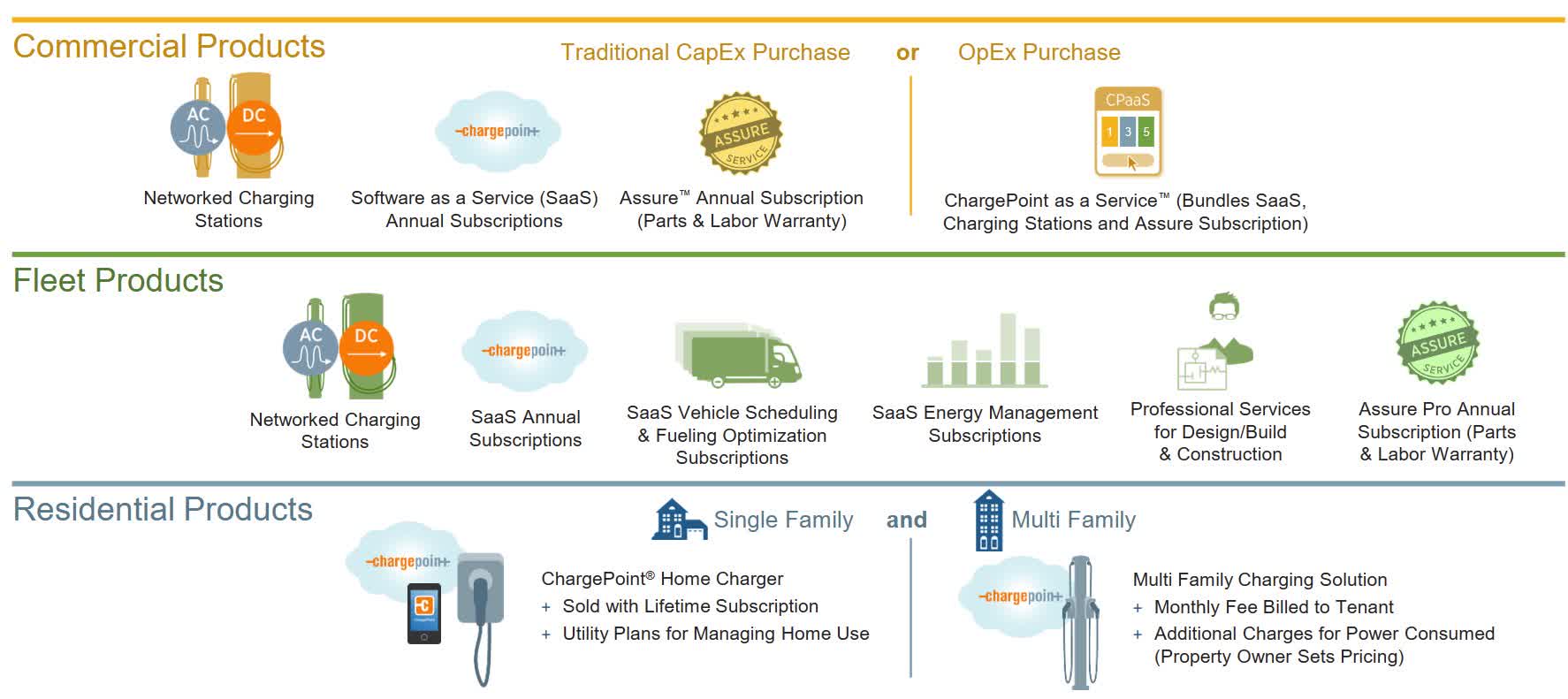

In terms of segments served, ChargePoint targets multiple lines of business including fleet, residential and commercial. As can be seen below, the ChargePoint business model works as a full suite solution, with the company not just providing the networked charging stations, but also annual software as a service subscriptions and annual subscription for servicing and repairs.

{kind=link}

Products for different lines of businesses (ChargePoint IR)

Large and established customer base

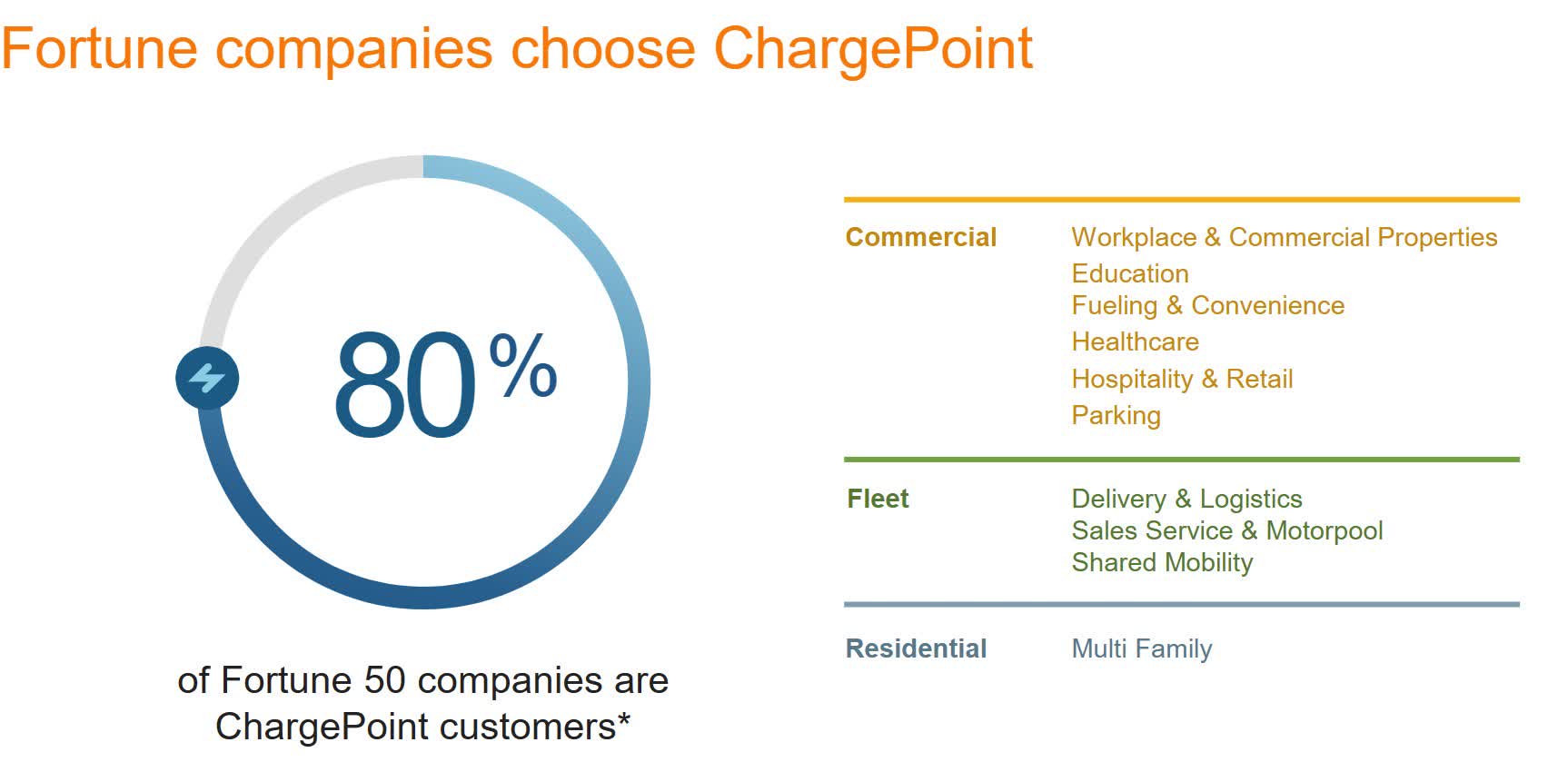

Not just any company chooses ChargePoint.

Fortune 50 companies choose to use ChargePoint, and that tells you a lot.

80% of all Fortune 50 companies are ChargePoint customers, as stated by the company, and these are across its different lines of businesses.

{kind=link}

Fortune 50 companies use ChargePoint (ChargePoint IR)

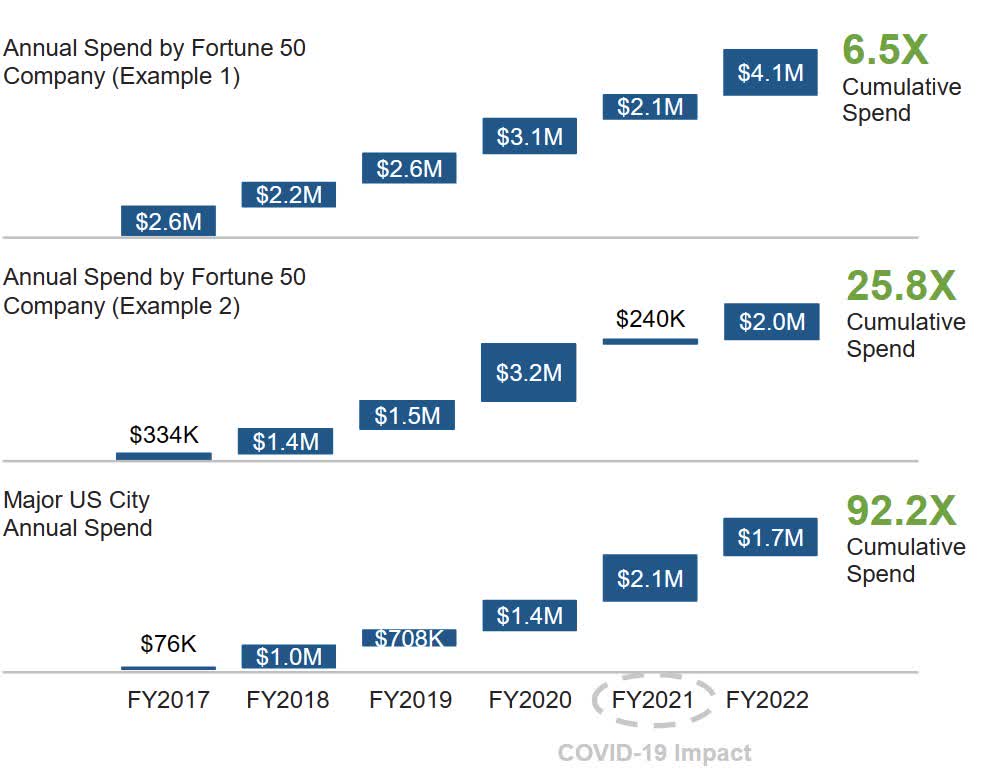

In addition, these large customers keep spending more with ChargePoint.

As shown below, ChargePoint's top 25 customers have seen their cumulative spend grow by 10.5 times from three years ago. This is likely due to expanding wallet share as ChargePoint rolls out subscriptions for service and software, as well as continued EV adoption in North America and Europe.

{kind=link}

ChargePoint top 25 customers spending growth (ChargePoint IR)

Although these were probably handpicked by management, I liked that management showed how its customers have been growing not just from three years ago, but from six years ago. As can be seen below, the large Fortune 50 customers that ChargePoint has today represent huge long-term opportunity for growth in spending.

{kind=link}

Examples of large customer growth (ChargePoint IR)

All in all, ChargePoint as a company has been able to demonstrate its ability to attract large customers and grow their spending over time. With more than 4,000 commercial customers today, ChargePoint looks poised for long-term growth.

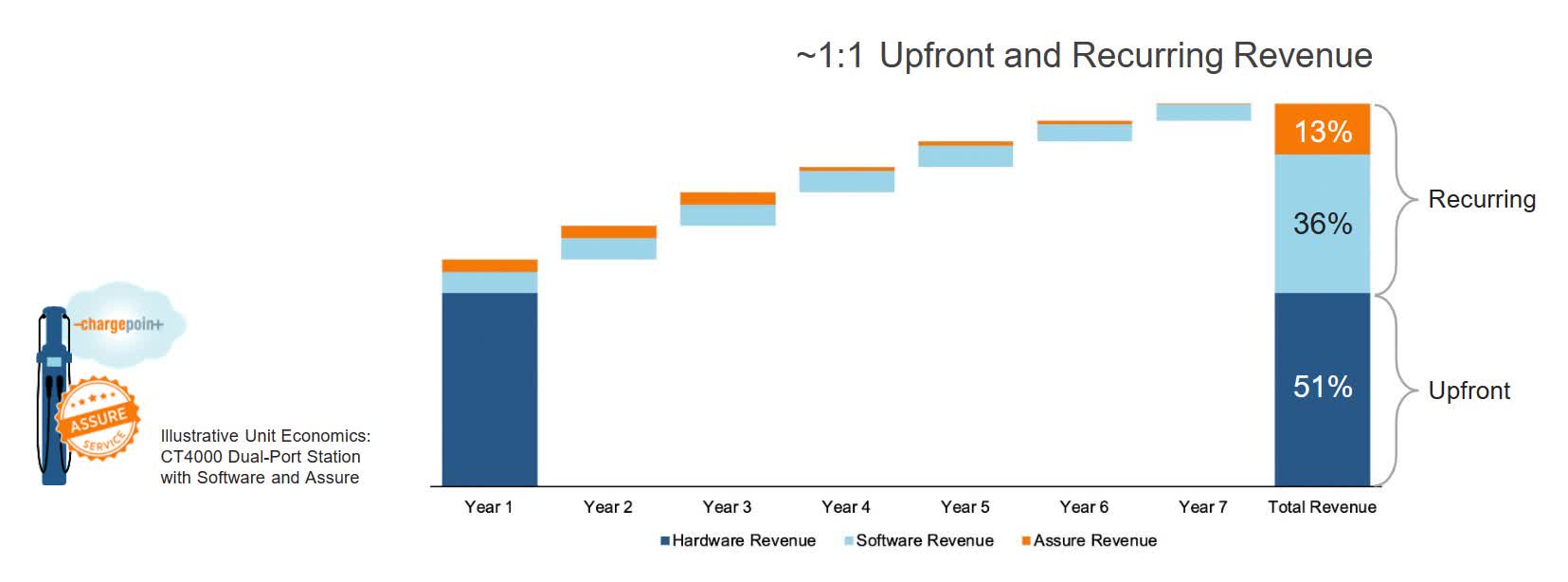

Resilient "land & expand business" model

ChargePoint has done a great job depicting its business model, in my view.

I call it the land & expand business model.

As customers purchase network charging stations, this will bring upfront hardware revenue. After which, ChargePoint has a strong proposition to upsell to customers. This includes its subscription for services and software, both of which will bring long-term recurring revenues.

As can be seen below, 50% of lifetime revenues are generated upfront while the remaining 50% are recurring and earned from year 1 to year 7.

{kind=link}

ChargePoint business model (ChargePoint IR)

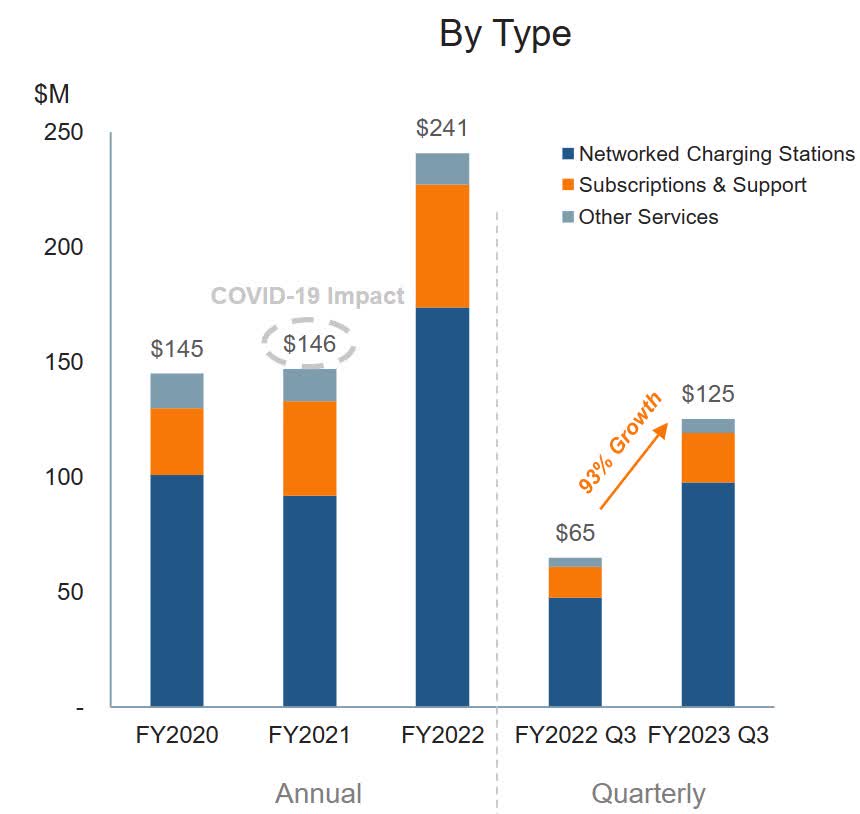

In addition, I just wanted to highlight the revenue mix for ChargePoint by type. About 70% to 75% of the company's revenues come from its networked charging stations. The remainder comes from its software and service subscriptions. This is largely in-line with the business model as I expect the subscription revenue to ramp up over time.

{kind=link}

ChargePoint Revenue by Type (ChargePoint IR)

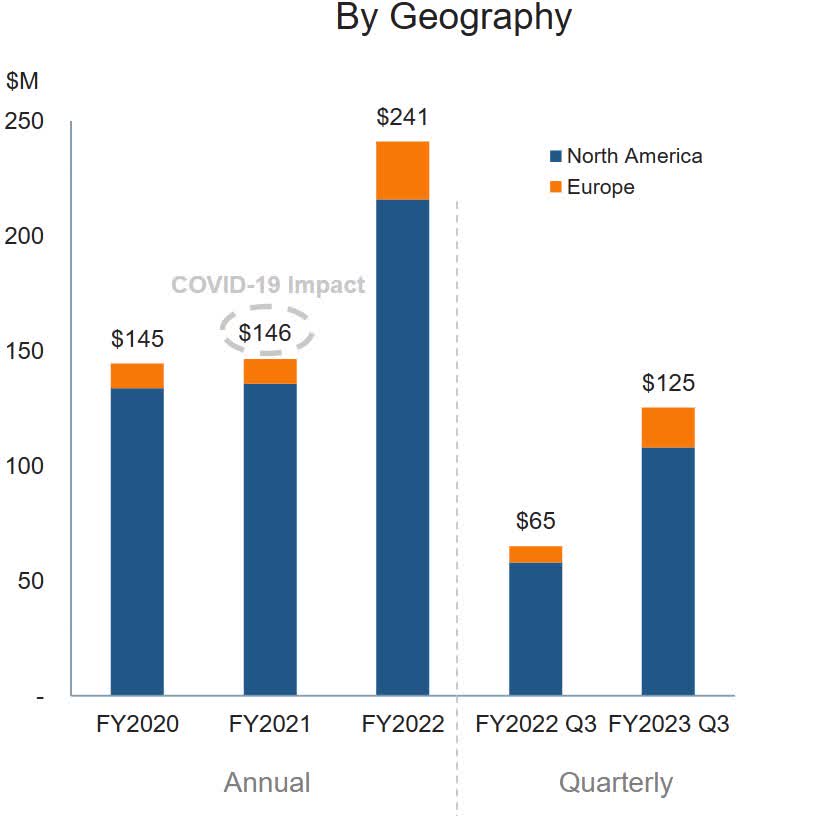

In terms of geography, most of ChargePoint revenues traditionally came from North America, although the mix in Europe increase in 2022.

{kind=link}

ChargePoint revenue by geography (ChargePoint IR)

Earnings were mixed

In 3QFY23, revenues for the quarter missed estimates, coming in at $125 million and at the lower end of guidance. This was largely due to constraints in production for ChargePoint's most mature AC product as a result of supply-drive redesign . As a result in shipping delays for this high margin product, this resulted in one percentage point lower margin improvement in the quarter. This shortfall has now been shipped and demand continued to exceed supply in the current third quarter of FY2023. Management expects that they are still on track to achieve its revenue target for the year. I thought it was positive that the revenue guidance for FY2023 was raised slightly by $5 million at the midpoint to $480 million despite this slight miss in the third quarter.

While gross margins in the third quarter of FY2023 improved quarter on quarter, they were below consensus as a result of pressures from the supply chain. While the gross margin guidance previously provided was withdrawn, there is the expectation that the gross margins will improve in the fourth quarter of FY2023. When removing the supply chain pressures that ChargePoint is experiencing, its positive that gross margins excluding these were in the mid-20s.

Despite the margin shortfall, management executed good operating expenses controls. This resulted in better or narrower than expected adjusted EBITDA loss. The control on operating expenses was critical for the business as it showed improvement in leverage that is needed for the company to reach its positive free cash flow goals by the 4QFY24. Management expects leverage to improve in the future even as we do not see a drop in operating expenses as the company continues to release more core products in the next few years.

Furthermore, the free cash flow burn for the third quarter of FY2023 came in worse than expected, which was due to working capital. The company continues to target positive free cash flow by Q4 FY24.

Valuation

My valuation for ChargePoint is based on a DCF model. My model takes into account 18x terminal EBITDA in 2030. I applied a discount rate of 15% to derive my DCF valuation.

My one-year target price for ChargePoint is $13.50, representing 9% upside from current levels.

Based on the DCF valuation, I think that ChargePoint is fairly valued at current levels. A large part of the positives have been priced in and investors should be patient when putting capital into the stock.

Risks

Competition

I think that while ChargePoint is a leader in the industry, especially in the North American market, there are more competitors looking to ramp up as the EV market heats up. These include publicly listed names like Blink Charging ( BLNK ), EVgo ( EVGO ), amongst others. I think that the competitive landscape is likely to intensify over the next few years as more players enter the EV charging industry given the clear path towards increasing EV adoption. This might lead to competitors providing better or cheaper products that makes it difficult for ChargePoint to compete meaningfully.

Profitability risks

There is a risk that ChargePoint does not reach positive free cash flows by 4QFY2024. The company could face difficulties in resolving the supply chain pressures or have difficulties improving leverage. If this is the case, there is material downside to the company's valuation.

Conclusion

All in all, I think that investors should be patient with ChargePoint. While there is a secular tailwind for the company in the form of global auto makers committing to making their vehicles electric and more favorable regulation and incentives from governments all over the world for EVs, I think that this has all been priced into the stock.

I do like the business fundamentals of ChargePoint. It has a full suite of products for its different lines of businesses, a resilient land and expand model, and a strong and established customer base. That said, I see competition as a problem and I would need this to be priced in before I can get constructive on the stock. Furthermore, valuation of ChargePoint's stock is still not cheap and the risk/reward profile is balanced.

I initiate ChargePoint with a neutral rating. Based on my DCF valuation, I think that ChargePoint is fairly valued at current levels. A large part of the positives have been priced in and investors should be patient when putting capital into the stock.

For further details see:

ChargePoint: Looks Promising And Worrying At The Same Time