CHPT - ChargePoint: Positioned For Growth In The EV Charging Market

2023-07-03 21:19:51 ET

Summary

- ChargePoint is a leading player in the North American Level 2 commercial charging market.

- The company is also expected to benefit from public EV infrastructure spending, as subsidies reduce the cost of charging stations for its customers.

- CHPT's growth is not solely dependent on the rapid adoption of electric vehicles, as ChargePoint's unique business model allows for steady progress even if automakers' targets are delayed.

- I view CHPT stock as a long-term buy and have an end-of-fiscal year 2024 price target of $12 on the stock.

Thesis

ChargePoint Holdings, Inc. ( CHPT ) is a prominent player in the North American Level 2 commercial charging market and is experiencing emerging growth prospects in North American DC fast charging ((DCFC)) and Level 2/DCFC in Europe. ChargePoint's growth prospects are not solely dependent on the rapid adoption of electric vehicles, as its unique business model allows for steady progress and expansion even if automakers' targets are delayed. By integrating its cloud software with hardware, ChargePoint creates positive network effects with its customers and drivers, leading to reliable recurring revenue. Over the next 5-10 years, I expect ChargePoint to achieve significant growth, surpassing the expansion rate of electric vehicles in the US and Europe. I am positive on the company's growth prospects and hence view the stock as a long-term buy. My end-of-fiscal 2024 price target of $12 is based on an assumed forward EV/Sales multiple of 5x applied to the 2025 revenue estimate of $1.04 billion.

Company Description

ChargePoint's mission is to help accelerate EV adoption by providing customers with a convenient, reliable network through which they can charge their vehicles. ChargePoint provides businesses, fleets, and individual drivers with a public charging network, in addition to hardware, software, and servicing solutions. ChargePoint's Level 2 and DC fast charging stations are located across commercial properties, fleet depots, and travel corridors.

Q1 2024 Review & Outlook

ChargePoint exceeded revenue expectations in the first quarter of fiscal year 2024 due to strong performance in its fleet and European segments, which offset slightly weaker demand from commercial and residential customers. This can be attributed to customers delaying non-essential spending in an uncertain economic climate. The company achieved a 2% sequential increase in margins, reaching 25% on a non-GAAP basis, driven by operational improvements, increased scale, and improved supply chains. ChargePoint is maintaining caution in operating expenses while continuing to invest in important initiatives, including service support. Although the revenue guidance for the second quarter of the fiscal year 2024 was lower than anticipated due to softer commercial demand, the company remains confident in a stronger performance in the second half of the year based on typical sales cycles and seasonal patterns.

One key takeaway from the earnings call is the diversification of ChargePoint's business across different industries and regions, allowing the company to offset weakness in certain areas with strength in others. The fleet segment, in particular, is showing promise as multi-vehicle fleets, such as rental cars and transit buses, are beginning to transition to electric vehicles. Unlike the commercial segment, fleet charging infrastructure is considered a necessary investment as it can lower operators' costs. While commercial demand has been relatively soft in recent quarters, ChargePoint expects workplace charging to increase in the second half of 2023 as return-to-office mandates take effect, resulting in charging demand being concentrated on fewer days of the week compared to pre-COVID times. ChargePoint also sees an attractive opportunity for expansion in multi-family residential charging as electric vehicle adoption continues.

Diversification Provides a Solid Hedge

ChargePoint's diversification across charging verticals and geographical regions ensures its resilience in an uncertain macroeconomic environment, where demand and spending patterns can vary across different markets. Despite the current weak demand in the commercial and residential sectors, the company's fleet and European segments show strong fundamentals. Notably, ChargePoint has doubled its fleet billings YoY, even without significant volumes of commercial electric vehicles available. This indicates that the company is gaining early market share, likely due to its robust fleet management tools and established track record in scaling operations. Additionally, with high adoption rates of electric vehicles in Europe, ChargePoint has a significant opportunity to continue expanding its market share in this region. This provides an added advantage as it serves as a hedge against potential downturns in either the European or US macroeconomic landscape.

{kind=link}

Secular Tailwinds Behind Growth

ChargePoint is the leading player in the industry, with well-established relationships -- is positioned to benefit from public EV infrastructure spending, as subsidies reduce the cost of charging stations for its customers. The Biden administration has allocated public funds by state and year for the next five years, intending to add 500,000 stations by 2030, spending $7.5 billion in EV charging. The total cost of the initiative amounts to $5 billion , expanding capacity along 75,000 highway miles, placing the onus on states to vet specific projects and dole out funds, with California and Texas accounting for 20% of the budget.

{kind=link}

Valuation

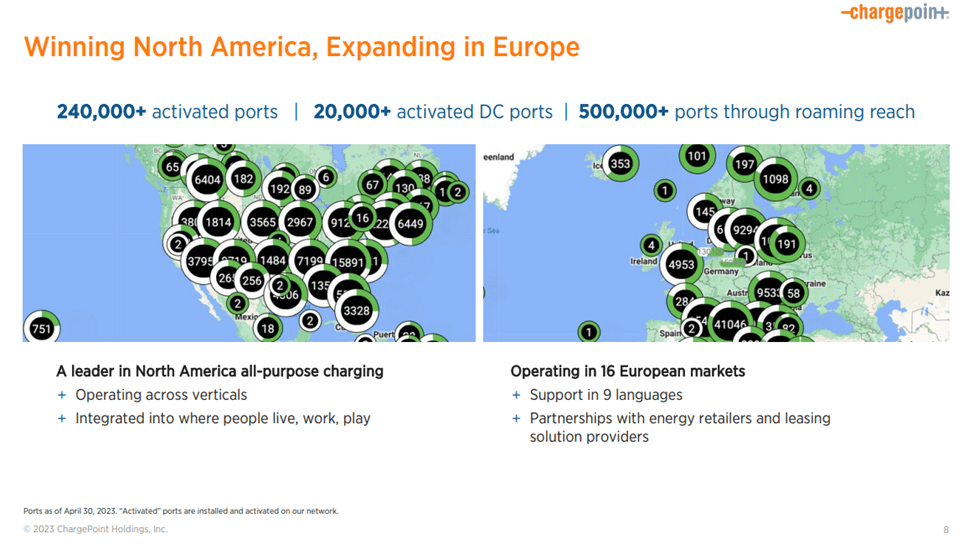

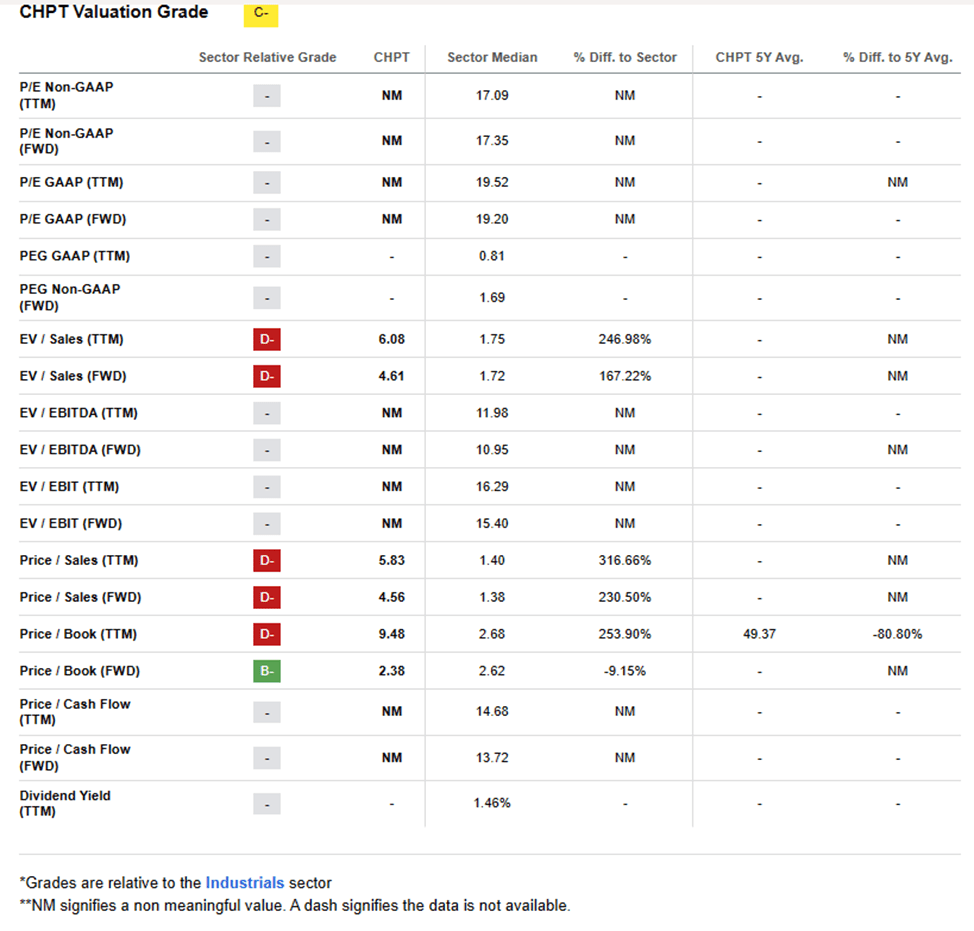

ChargePoint expects to defend its market share (~65% today in North America) given the extent of its scale, network effects, and channel partners, which are difficult to replicate and sees an opportunity to grow its port count from ~240K to a few million by 2030. ChargePoint has a strong network of channel partners (which accounts for 60-70% of sales) which it can also leverage for the NEVI program, which continues to progress as a demand driver, and where ChargePoint appears to be confident in winning contracts. I think ChargePoint's vast network, spanning all verticals, and clout and mindshare with distribution/channel partners is an underappreciated part of the story. My end-of-fiscal 2024 price target of $12 is based on an assumed forward EV/Sales multiple of 5x applied to the 2025 revenue estimate of $1.04 billion. My assigned 5x EV/S multiple implies a slight premium to where emerging cleantech, EV, battery, and renewable stocks are currently trading based on what I believe to be higher growth, margin expansion opportunities, and a clear path to profitability.

{kind=link}

Risks

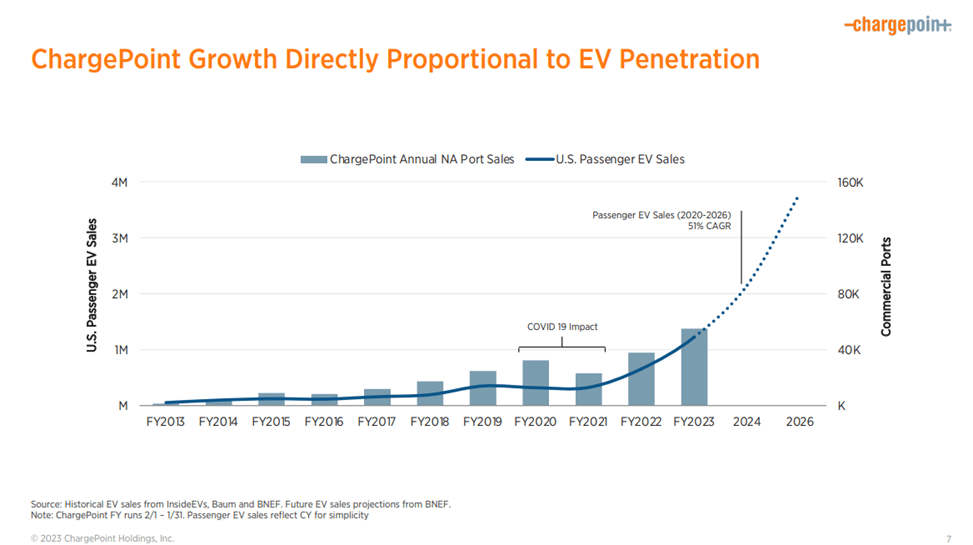

As the electric vehicle market expands, competition is expected to intensify as other industry players seek to capitalize on growing acceptance, government incentives, and the rapid development of charging infrastructure. If ChargePoint fails to maintain a competitive edge in terms of its hardware and software products, there is a risk of price erosion and the loss of network effects. On the other hand, if ChargePoint can demonstrate superior cost efficiency, technological leadership and effectively leverage its early entry advantage, the company's financial performance could surpass expectations. Moreover, ChargePoint's growth projections are currently aligned with the pace of new passenger EV sales growth based on historical correlation. However, if EV sales growth falls short of expectations or if ChargePoint's growth lags behind the broader EV market, its financial performance could decline. Conversely, if EV sales exceed expectations, ChargePoint's financial performance could experience significant benefits.

Conclusion

With a dominant market position in Level 2 AC electric vehicle charging hardware, cloud software, and services in North America, ChargePoint is also capitalizing on growing opportunities in Europe and emerging commercial and fleet applications in both regions. ChargePoint's growth trajectory does not solely rely on a surge in electric vehicle adoption. The company's unique business model allows for consistent progress and expansion, even if automakers' ambitious goals are delayed. The integration of its cloud software with hardware enables ChargePoint to generate positive network effects with its customers and drivers, resulting in predictable recurring revenue. I view the stock as a long-term buy and have an end-of-fiscal year 2024 price target of $12 on the stock.

For further details see:

ChargePoint: Positioned For Growth In The EV Charging Market