CHPT - ChargePoint's Decline Amidst Tesla's Rising Dominance

2023-06-26 15:45:00 ET

Summary

- Tesla's recent deals with Ford, General Motors, and Rivian have negatively impacted ChargePoint Holdings. In the wake of this, CHPT stock has fallen approximately 27%.

- CHPT faces increased competition from Tesla, which is expanding its hold on the EV charging market, making CHPT a less attractive investment.

- CHPT's high cash burn rate and limited supply of DC charging ports in the U.S. put it in a weak position to compete with Tesla, making it a sell recommendation for investors.

ChargePoint Holdings, Inc. ( CHPT ) dropped roughly 27% following the charging station deals Tesla, Inc. ( TSLA ) announced with Ford ( F ), General Motors Company ( GM ), and more recently Rivian ( RIVN ). These deals come on the heels of Biden's National Electric Vehicle Infrastructure Formula Program, which will grant funding to EV charging stations in an attempt to increase EV purchases.

Usually, this would come as welcomed news for CHPT since it is an EV charging port manufacturer. However, Tesla has secured such a large share of the charging market with these deals, that CHPT will likely suffer as a result. Clearly, TSLA is seeking to expand its hold on the market, leaving little upside for CHPT. With this bearish outlook and increased competition, I believe CHPT is a sell.

CHPT's Losing Position

Before TSLA's deals with General Motors and Ford, mainly TSLA vehicles could access Tesla's DC ports, which are capable of charging EVs at a significantly faster rate than standard AC ports.

While CHPT has an impressive network of 31,000 charging spots across the USA, the company's network is mainly comprised of AC ports which have become less desirable. Even if CHPT is able to continue making investments in DC ports, Tesla's latest deals have impacted a large portion of its addressable market.

Starting in 2025 Ford and GM EVs will be able to utilize DC ports with an adapter, and with time other automakers will likely join in. As things stand, CHPT cannot compete with a behemoth like TSLA, which has more than 45 thousand ports - more than double CHPT's 21 thousand DC port stations globally.

Personally, I don't believe that Tesla made these deals solely for the money. Piper Sandler estimates the deals will add $3 billion in charging revenue from non-Tesla owners by 2030 and $5.4 billion by 2032. Compared to Tesla's typical annual revenue, this is not particularly significant.

However, these deals bring it one step closer to becoming the charging standard for the US, which opens new opportunities for Tesla to capitalize on and assert its dominance.

Tesla's Change of Heart

TSLA previously flaunted the idea of opening its supercharging network to competitors but recently changed its tune. The reason for this shift is likely the $7.5 billion in subsidies offered under Biden's massive infrastructure plan designed to accelerate the adoption of charging infrastructure.

Companies facilitating the installation and operation of 500 thousand EV ports across the country will benefit from this funding. But to be eligible, TSLA must make its DC port system available to non-Tesla EVs as well . Therefore, the timing of this decision could be tied to this federal funding.

Fighting a High Cash Burn Rate

In order to combat TSLA's looming expansion, CHPT needs to drastically increase its network of DC ports. That said, I don't believe CHPT is in a position to do so due to its high cash burn rate.

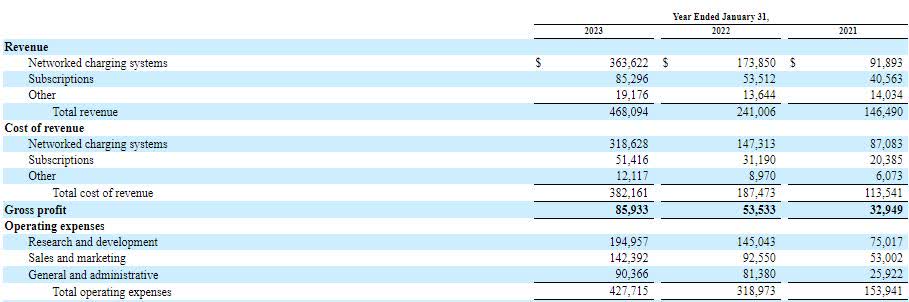

| Year |

| Revenue |

| Cost of Revenue |

| Total Operating Expenses |

| Net Loss |

| 2023 |

| 468,094,000 |

| 382,161,000 |

| 427,715,000 |

| 345,108,000 |

| 2022 |

| 241,006,000 |

| 187,473,000 |

| 318,973,000 |

| 132,241,000 |

| 2021 |

| 146,490,000 |

| 113,541,000 |

| 153,941,000 |

| 197,024,000 |

Looking at CHPT's operating expenses, the company increased its R&D spending 93% from 2021 to 2022 followed by a more moderate increase of 34% from 2022 to 2023. These expenses accounted for 51%, 60%, and 41% of total revenue, respectively.

Meanwhile, sales and marketing increased 74% YoY from 2021 to 2022 and 53% from 2022 to 2023.

{kind=link}

For all this spending, CHPT doesn't have much to show for it, with an operating profit margin of -.73 and a 160% increase YoY in its net loss. With only $246 million in cash and cash equivalents, I believe that the company will need to raise capital in 2024 - something that will be more difficult for its shareholders to stomach as competition in the sector increases.

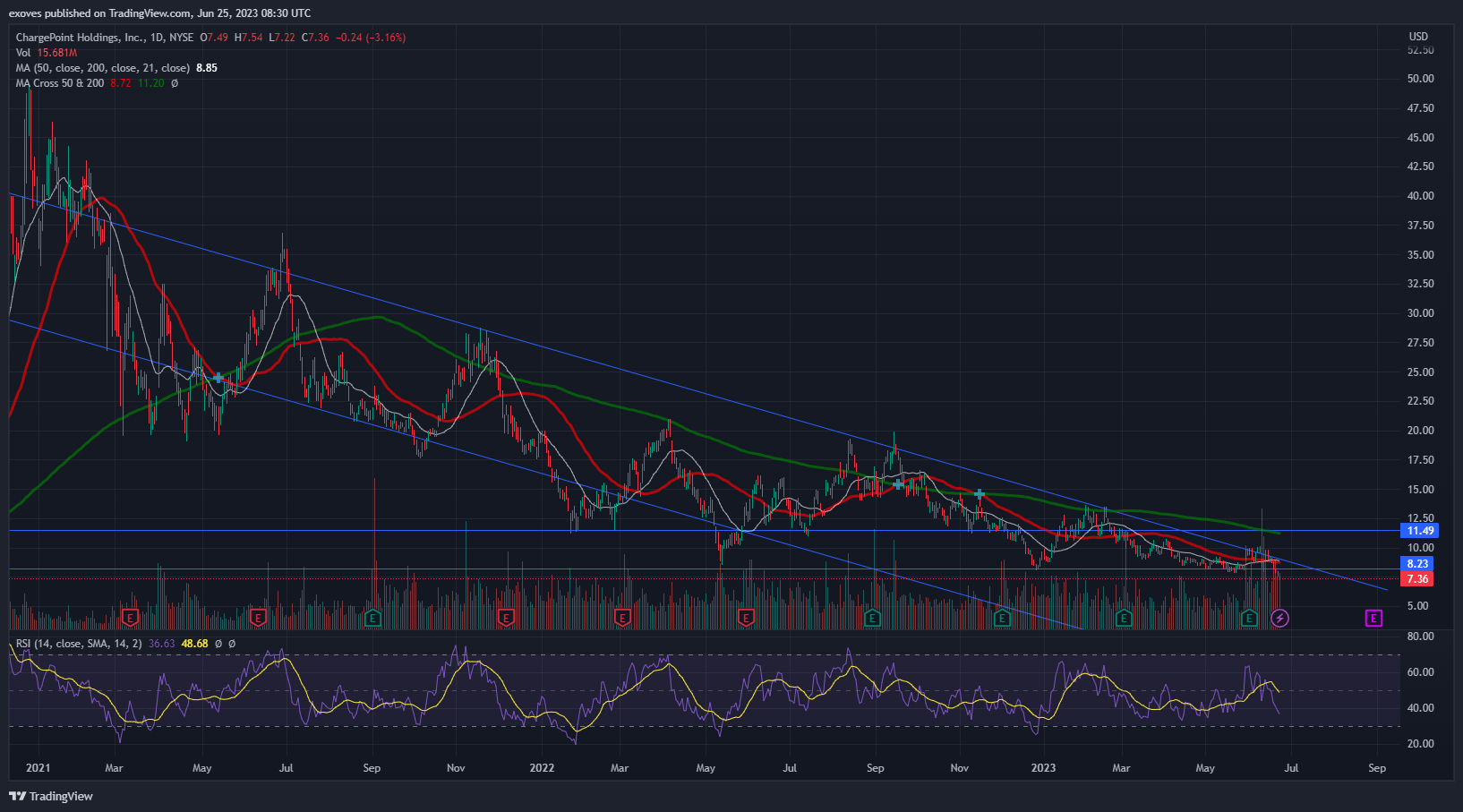

Technical Analysis

{kind=link}

Looking at the daily time frame, CHPT stock has been trading in a downward channel since January 2021. The trend is bearish with CHPT trading below the 200, 50, and 21 MAs. A death cross of the 50 and 200 MAs occurred in November 2022 indicating a bearish trend.

Overall, this paints a bearish picture for CHPT stock, which has fallen below its IPO price and broken an important support near $8.23. We can also see investors reacting to TSLA's deals with automakers, which appears to have instigated a 27% drop since the June 8th announcement. As a result, the RSI is approaching oversold at 36.

As for the fundamentals, TSLA's efforts to establish its charging ports through partnerships with automakers will have a long-lasting impact on CHPT's business. It seems likely that other automakers will join in, shrinking CHPT's share of the market.

Currently, short interest is at 21% which may make now a less-than-ideal time to take a short position. I recommend waiting for the RSI to recalibrate and take a short position near the $8.23 resistance or upper trendline. Investors could keep a tight trailing stop loss or use the 50 MA as a stoploss to minimize risk.

Risks

While I believe CHPT is a good long-term short, there are risks. Given the relatively high short interest, CHPT could squeeze on unexpected news. Taking a short position always has risks but a stoploss can help mitigate them.

Additionally, CHPT has shown notable revenue growth YoY. If the company's management were to revise its spending strategy and optimize its R&D expenses or its marketing spend to achieve better value for the dollars spent, the company could be in a position to achieve profitability over the next few years.

It's also worth noting that my short thesis is primarily based on Tesla's apparent intention to consolidate power in the EV charging sector. If Tesla's latest partnerships fail to attract additional automakers or complications occur resulting in the breakdown of these deals, CHPT's outlook may improve.

Conclusion

As a result of TSLA's deals with some of the country's most prominent automakers, CHPT will likely experience a decline in its user base over the coming years. Given CHPT's limited supply of DC charging ports in the USA and Tesla's ability to flex its power and capital to corner this market, CHPT is in a particularly poor position to face off with growing competition.

This combined with CHPT's overall bearish stock performance and high cash burn make CHPT a sell. Investors can take the opportunity to short the stock in anticipation of the company's continuing struggles to achieve profitability.

For further details see:

ChargePoint's Decline Amidst Tesla's Rising Dominance