CHPT - ChargePoint's Investment Thesis Has Soured As Insiders Sell And Bulls Flee

2023-10-10 16:00:00 ET

Summary

- CHPT's execution has worsened as inventories grow, gross margins suffer, and balance sheet deteriorates in FQ2'24.

- Linse Michael , a director in CHPT, has effectively liquidated 100% of his position, naturally raising further doubts about the company's prospects.

- While the management has guided a decent FY2024 revenue, while reiterating its CY2024 goal of "generating positive non-GAAP adjusted EBITDA,” the stock has unfortunately entered penny stock territory.

- Its short interest has also risen to 22.44%, implying that the stock is now "considered speculative, high-risk investment as it experience higher volatility and lower liquidity."

- While the bulls may continue holding on to CHPT, they must also be very patient and have higher risk appetite, since its eventual reversal remain speculative depending on when bullish support materializes.

The CHPT Investment Thesis Has Soured, As Insider Selling Intensifies & Bullish Support Wanes

We previously covered ChargePoint Holdings ( CHPT ) in June 2023, discussing the negative sentiments surrounding its prospects as Tesla ( TSLA ) entered the supercharging scene, naturally triggering the sold-off status at that time.

In this article, we will be discussing why Mr. Market has grown further pessimistic on its execution as inventories grow, gross margins suffer, and its balance sheet deteriorates in the FQ2'24 quarter.

For example, the CHPT still reports adj EBITDA losses of -$81.2M in FQ2'24 ( -66% QoQ / -44.4% YoY), despite the sustained top-line growth to $150.49M (+15.7% QoQ/ +39% YoY).

This is partly attributed to the impacted GAAP gross margins of 0.7% (-22.8 points QoQ/ -16.1 YoY), with an -$28M of inventory impairment charge "to address legacy supply chain-related costs and supply overruns on a particular DC product."

This is a big concern in our opinion, since it is uncertain if EV charging company's impairment charges may continue for a few more quarters, given the elevated inventory levels of $143.58M in the latest quarter (+24.6% QoQ/ +168.7% YoY).

CHPT's bloated inventory levels compared to FY2019 levels of $25.42M (inline YoY) implies an impacted demand indeed, especially highlighting its lack of moat in the currently crowded EV charging space.

This is despite its large footprint globally with 255K active ports ( +4.9% QoQ / +27.5% YoY ) and 22K DC fast ports (+4.7% QoQ/ +46.6% YoY) by FQ2'24.

While the CHPT management has already drastically reorganized its operations with a -10% reduction in headcount, expected to generate an approximate $30M in annual operating expenses, we are not overly convinced yet.

This is because the eventual sum is still too little, compared to its annualized operating expenses of $497.84M in the latest quarter (+12.6% QoQ/ +14.6% YoY).

For now, the CHPT management has guided a decent FY2024 revenues of $617.50M at the midpoint (+31.9% YoY), while reiterating its CY2024 goal of "generating positive non-GAAP adjusted EBITDA."

While these numbers continue to suggest a high growth trend, it is also apparent that Mr. Market is expecting a lot more, compared to the consensus FY2024 revenue estimates of $678M (+44.8% YoY) and the company's previous FY2023 growth rate of +94.2% YoY.

On the one hand, CHPT appears to have more than enough liquidity on its balance sheet at $263.9M (-6.8% QoQ/ -44% YoY) to last a few more quarters.

On the other hand, based on its current cash burn rate of $49.85M quarterly and $238.04M annually, we may see the company further rely on dilutive capital raises and/ or debt to sustain its operations.

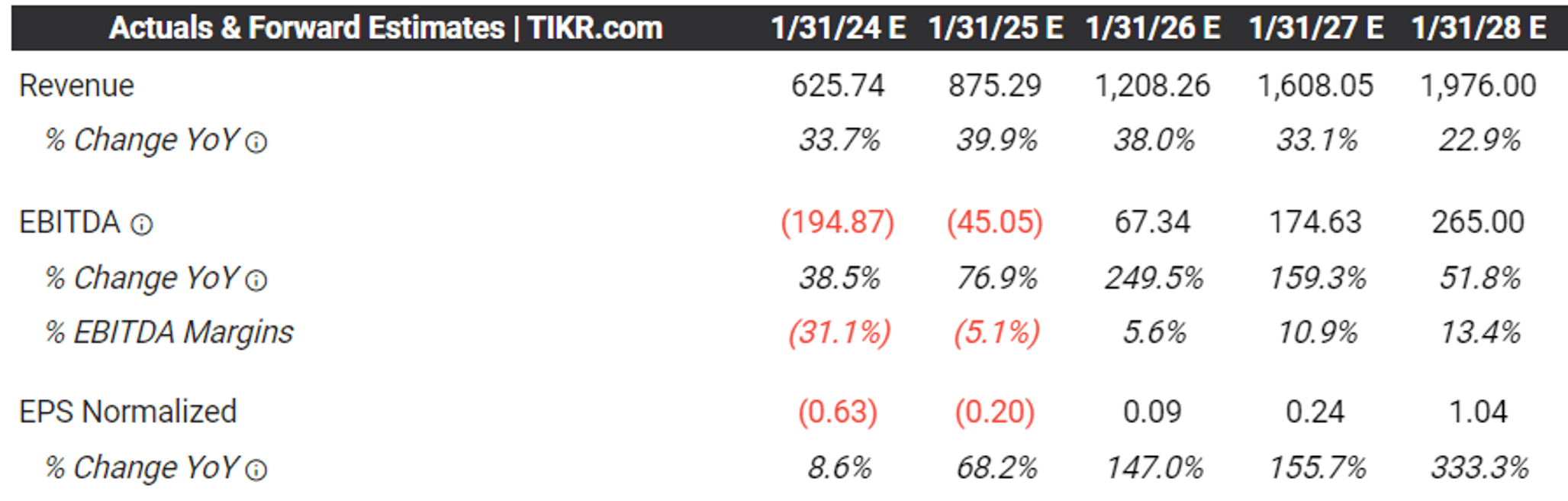

The Consensus Forward Estimates

{kind=link}

While the consensus has estimated that CHPT may eventually achieve breakeven EPS profitability by CY2025/ FY2026, potentially signaling the stock's potential reversal then, investors must also contend with more volatility and uncertainty over the next few years.

The Fed now only expects a normalized economy only by 2026, implying that the elevated interest rate environment may be prolonged for a little longer.

As borrowing costs remain elevated at 7.51% (+0.11 points MoM/ +2.24 YoY/ +2.88 from 2019 averages of 4.63%), the US EV sales may remain impacted, with the supply of EV remaining elevated at over 100 days compared to the industry-wide supply at 53 days.

CHPT's Revenues By Region

Seeking Alpha

While the CHPT management has guided that "Europe is performing beautifully," we are uncertain if the region's outperformance is able to make up for the shortfall in the US, since the North American region comprises approximately 80% of its overall top-line in the latest quarter.

As a result of these headwinds, it appears that we must temporarily reign in our bullish sentiments since its near-term prospects remain uncertain.

So, Is CHPT Stock A Buy , Sell, or Hold?

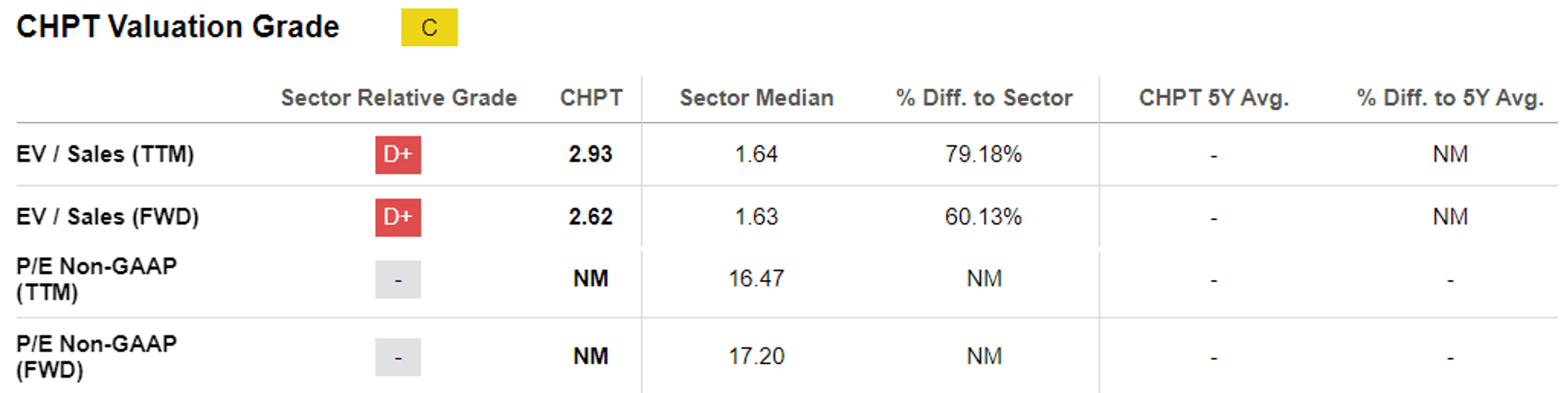

CHPT Valuations

{kind=link}

Since CHPT has yet to record any sustainable adj or GAAP profitability, the only metric we may use to measure its performance is the FWD EV/ Sales of 2.62x, which remains elevated compared to the sector medians.

While the EV charging company may still record a high growth top-line cadence, though normalized from its hyper-pandemic levels, it is apparent that Mr. Market has discounted its execution.

The same sentiment has been demonstrated by the sustained moderation in its FWD EV/ Sales valuation from the March 2021 peak of 50.93x, April 2022 peak of 14.28x, and February 2023 peak of 6.59x.

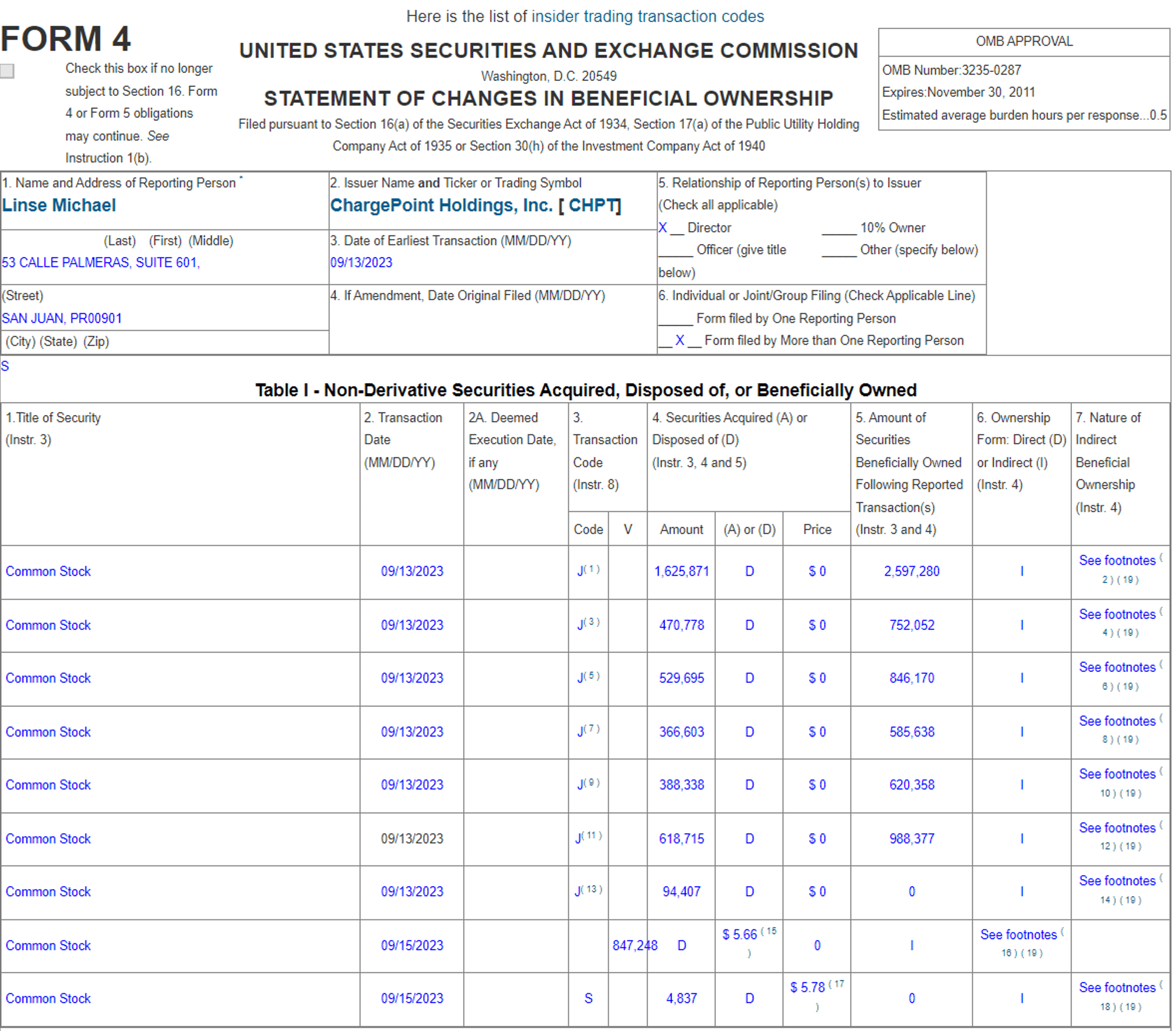

CHPT Insider Selling - Linse Michael

{kind=link}

As mentioned by Peter Lynch, "Insiders might sell their shares for any number of reasons, but they buy them for only one: they think the price will rise." While we do not typically rely on insider selling information, the immense trading over the past few months has also dampened the bullish sentiments.

Most importantly, Linse Michael , a director in CHPT, has effectively liquidated 100% of his position over two days in September 2023, naturally raising further pessimism and doubts about the company's prospects.

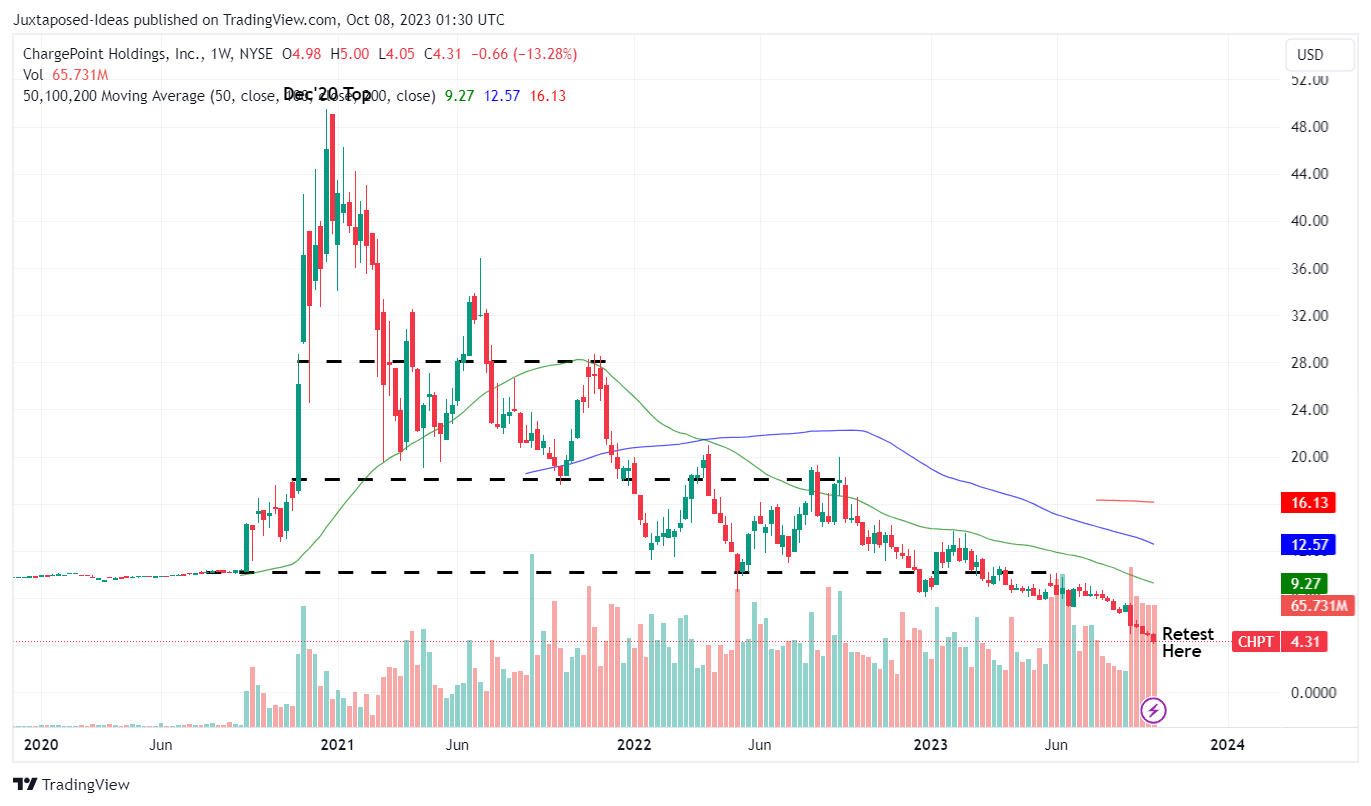

CHPT 4Y Stock Price

{kind=link}

Combined with the underwhelming FQ2'24 performance and lower than expected FY2024 guidance, it is unsurprising that CHPT has also plunged drastically and entered the dangerous penny stock territory by the end of the month.

In addition, its short interest has also risen to 22.44% at the time of writing, implying that the stock is now "considered speculative, high-risk investment as it experience higher volatility and lower liquidity."

As a result of the potential capital losses, we do not recommend investors to add or dollar cost average here, since CHPT may be a new battleground stock, with the volatility from aggressive short sellers likely negating the potential upside from these bottom levels.

This results in our Hold (Neutral) rating here.

While the bulls may continue holding on to CHPT, they must also be very patient and have a higher risk appetite, since the stock's eventual reversal remains speculative depending on when bullish support materializes.

For further details see:

ChargePoint's Investment Thesis Has Soured, As Insiders Sell And Bulls Flee