DRIV - ChargePoint: Stellar Growth At The Cost Of Profitability - Why Not?

Summary

- At its current rate, the CHPT management may have temporarily sacrificed profitability for the sake of hyper-growth and footprint expansion.

- That works fine for us, given the tremendous emphasis on technological advancement and sales infrastructure, improving CHPT's business opportunities in the intensely competitive market.

- Investors may likely witness a positive cash flow by Q4'24, temporarily supported by its robust cash/investments and total receivables.

- An immense amount of patience and risk tolerance may be rewarded by CY2025, with a speculative adj. EPS of $0.17.

- In a world without macroeconomic uncertainties, CHPT may bullishly rally, significantly aided by the massive EV adoption in the US and EU then.

We have previously covered ChargePoint Holdings, Inc. ( CHPT ) here as a pre-earnings article in November 2022. Its market opportunities in the EU were discussed extensively, where the number of EVs on the road is expected to grow 21-fold to 30M by 2030, up from 1.4M in 2022. The analysis of the company's historical and projected performance revealed that it is unlikely to achieve GAAP profitability before FY2025, due to its aggressive expansion strategy. We recommend you take a quick glance for a better understanding.

For this article, we will be focusing on CHPT's FQ3'23 performance, with an in-depth discussion of the pessimistic market sentiments surrounding new vehicle/ EV sales. However, we will also be sharing why its current trajectory remains bullish for its future growth, due to its strong focus on R&D efforts and sales expansion. These strategies have directly resulted in the growth of its backlog, indicating robust consumer demand despite the worsening macroeconomics.

Investment Thesis - In High-Growth Mode

CHPT delivered sustained top-line growth by FQ3'23, undoubtedly, at the temporary cost of profitability. However, we are not overly concerned, since its gross and EBIT margins show sustained improvements by 1.3 percentage points and 17.1 points QoQ, respectively. Unfortunately, YoY comparison in gross margins continues to suffer by -6.6 points, due to the impact of rising inflationary pressures. Its EBIT margins also remained negative at -66.4% by the latest quarter, due to the expanding operating expenses by 30.2% YoY and Stock-Based Compensation by 60.42% YoY. According to these numbers, the company underperformed consensus expectations, contributing to the stock decline of -14.25% in the week post-earnings call.

Nonetheless, we are impressed by CHPT's progress in customer usage, increasing by 8.13% QoQ and 35.71% YoY to 133M of charging sessions to date. It reported stellar subscription revenues of $21.67M as well, rising excellently by 7.06% QoQ and 61.83% YoY. The company also reported a growing backlog to $175.21M, triggering the expansion of its deferred revenue by 4.54% QoQ to 44.56% YoY. These support the management's commentary that demand continues to outstrip supply. Pasquale Romano, CEO of CHPT, said:

Demand again exceeded supply for the quarter, resulting in additional growth in backlog. We are on track to our revenue target for the year and Rex will provide more color on revenue and particularly on gross margin in his comments. ( Seeking Alpha )

We would like to reiterate that CHPT remains one of our highly monitored stocks, and that the aggressive expansion strategy has given the company a leading edge in the long-term EV movement. We will discuss why the market sentiments may have turned pessimistic, though things may improve in the intermediate term, due to the company's commitment to its next decade's growth. This naturally warrants further discussion following the underwhelming earnings release.

CHPT's Valuations Are Temporarily Dragged Down By Elevated Prices & Slowing Demand

Nevertheless, market analysts remain skeptical about CHPT's short-term prospects, probably attributed to the pessimistic sentiments surrounding new vehicle sales thus far. The November CPI report shows a moderating index for new vehicle sales at 0% sequentially, against 0.7% in September 2022.

This came as no wonder, since many companies such as Ford ( F ), General Motors ( GM ), and Tesla ( TSLA ) have hiked their EV prices several times to counter the rising costs. Ford has further raised its entry-level F-150 Lightning again by an eye-popping total of 40% to $55.97K since its debut in May 2021. GM's Silverado HD prices have been increased by 14.32% to $42.29K since launch, with TSLA also hiking its Model 3 Rear-Wheel Drive by 21.62% to $44.99K .

Furthermore, the supply of unsold new vehicles in the US rose to 1.64M units in November, growing notably by 5.8% sequentially and 81% YoY. Supply also expanded by 6% sequentially and 77% YoY to 53 days simultaneously, partially attributed to higher production output. By October 2022, the consumer savings rate dropped to 2.3% as well, the lowest level since July 2005, due to market weakness. These impact high-ticket sales as reported by Charlie Chesbrough, Senior Economist at Cox Automotive:

Sales had been showing slight gains since September. But they slowed some in November, dropping 22,000 units week-to-week in the most recent data. At the end of November, sales were up only 3% from a year ago. ( Cox Automotive )

The Feds are also poised to keep raising until a terminal rates of 5.1% through 2023, if not longer through 2024, due to the 2% target rate. As a result, we may see a further tightening of consumer discretionary spending and a cooling of the demand for new/ used autos alike. Hence, it is no wonder that the CHPT stock and the Global X Autonomous & Electric Vehicles ETF (NASDAQ: DRIV ) have plunged by -47.41% and -32.20% YTD, respectively, against the S&P 500 Index at -19.68%. The same is also observed with Ford at -44.33% YTD, GM at -40.90%, and TSLA at -62.44%.

CHPT Remains Highly Committed To Its Next Decade Growth

On the other hand, we remain encouraged by CHPT's strategic choice in investing in its technological advancement and sales growth, since these could eventually be top and bottom-line accretive. Over the last twelve months, the company grew its R&D efforts by 54.47% sequentially to $190.75M, with further enhancements planned for its charging platforms and cloud software.

As part of its expansion efforts in the US and EU, CHPT has launched new product lines: the CP6000 and Express Plus DC by H2'22. The new systems offer significant flexibility and serviceability for vehicles of all types and sizes, as well as 350 kW DC fast charging. The latter (equivalent to Level 3 charging) allows drivers to add up to 200 additional miles within fifteen minutes - immensely improving consumer experience indeed, against the conventional Level 1 at 40 hours or Level 2 at 6 hours.

Furthermore, CHPT also raised its SG&A expenses by 52.02% sequentially to $217.39M, which aided the growth of its footprint across business applications. The combination of leading-edge product offerings and conducive sales infrastructure may likely improve its business opportunities against the intensely competitive peers, such as Enphase ( ENPH ), through the recent ClipperCreek acquisition and TSLA's growing Supercharger network at 41.32K stalls globally . To date, CHPT boasts 210K network ports , of which 16.7K is Level 3 charging, with 65K located in the EU.

As per management's guidance, CHPT investors may likely witness a positive cash flow by Q4'24, temporarily supported by its robust $397.16M in cash/investments by the latest quarter. These will ensure its immediate liquidity no matter the soft landing or recession over the next few quarters. We may see the funding market normalize by mid-2023 as well, once the rising inflation has been successfully tamped down to the Fed's satisfaction. It may also contribute to the company's cash flow, due to its lack of GAAP profitability in the short term.

We Remain Bullish About CHPT's Long-Term Prospects

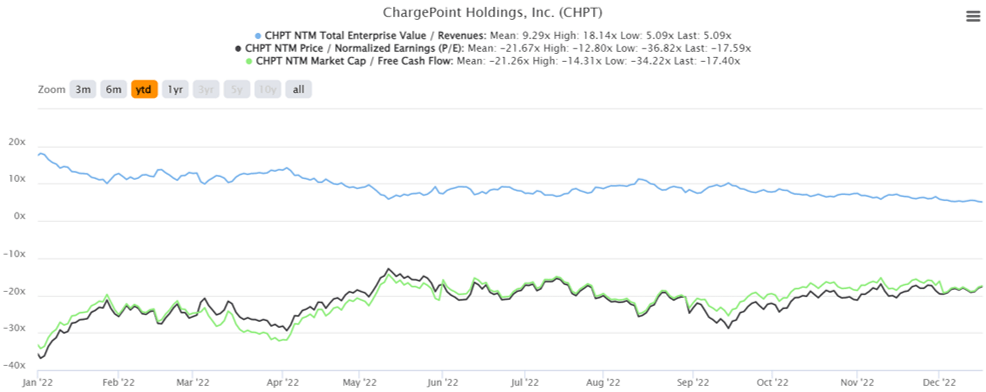

CHPT YTD EV/Revenue, P/E, and Market Cap/FCF Valuations

{kind=link}

CHPT is currently trading at an EV/NTM Revenue of 5.09x, NTM P/E of -17.59x, and NTM Market Cap/FCF of -17.40X, lower than its 2Y mean of 19.11x, -43.88x, and -30.67x, respectively. Otherwise, still lower than its YTD P/E mean of -21.67x. The company is not expected to reach profitability through FY2025 (CY2024), indicating temporal headwinds to its valuations and stock prices indeed.

Nonetheless, we remain bullish about CHPT's prospects through the next decade, especially since market analysts expect accelerated revenue growth at a CAGR of 68% through FY2025 (CY2024), against hyper-pandemic levels of 49.1%. With the bullish consensus price target of $26, we may also see an impressive 148.80% upside from current prices, despite the market-wide uncertainties over the next two years. Once the macroeconomics normalizes and market demand returns, we may see the stock rebound quickly, significantly aided by the speculative profitability from FY2026 (CY2025) onwards at an adj. EPS of $0.17.

As a result, we retain our buy rating on the CHPT stock. However, investors would be well-advised to size their portfolios accordingly, in the event of volatility since the stock may trade sideways at single digits in the intermediate term.

For further details see:

ChargePoint: Stellar Growth At The Cost Of Profitability - Why Not?