QGEN - Charles River Laboratories International: A Great Business At A Decent Price

Summary

- Charles River Laboratories has proven itself to be a quality player in its space.

- Shares of the company don't look all that cheap, but they aren't exactly expensive either.

- When paired with the consistency of its growth and the robust cash flows of the firm, it becomes a decent candidate for investors to consider.

Buying into a company that has demonstrated consistent and attractive growth can be a great way to make some money. That said, just because growth is occurring doesn't mean an opportunity is truly appealing. If the price being paid for the investment is too lofty, upside for investors can be minimal or can even sour and result in losses. Fortunately for investors in Charles River Laboratories International ( CRL ), the stock is not so lofty as to limit potential by any meaningful degree. But it's also true that shares aren't exactly cheap. All things considered, the company likely does offer some upside potential. Because of that, I have decided to rate it a 'buy', but I wouldn't say that the potential is significantly greater than what the broader market can achieve.

A niche business experiencing rapid growth

The management team at Charles River Laboratories describes the company as a "full-service, non-clinical contract research organization". Initially, the company focused on laboratory animal medicine and science. But since then, it has developed its portfolio of discovery and assessment services. In all, the company provides its customers with a suite of products and services to help with manufacturing activities. And at the end of the day, their goal is to enable their clients to create a more flexible drug development model that reduces costs, increases productivity and effectiveness, and hastens the speed of said products to market. To truly understand the company, however, we should dig into each of its three operating segments.

The first of these segments is called Research Models and Services. Through this, the company supplies research models to drug developers, with over 160 different stocks and strains to work with. Part of the company's business involves keeping a rather large collection of rodent research models strains and purpose-bred rats and mice. The company also offers services related to this that helped to support their clients in the use of research models and drug discovery and development. Approximately 19.5% of the company's revenue came from this segment during the company's 2021 fiscal year.

Next in line, we have the Discovery and Safety Assessment segment. This unit provides services that enable clients to outsource their innovative drug discovery research, as well as other related drug development activities. The company also offers regulatory-required safety testing of potential new drugs, vaccines, industrial and agricultural chemicals, consumer products, veterinary medicines, medical devices, and more through this unit. One of the subsidiaries under this unit offers antibody discovery technologies, while another provides specialized bioanalytical services for antibodies and related therapeutic products. This particular segment was the largest for the company in 2021, accounting for 59.5% of sales.

And finally, we have the Manufacturing segment. According to management, with this unit assists in the production and release of products that are manufactured by its clients. The company does this through three different businesses under the segment. Its microbial solutions unit offers customers in vitro methods of conventional and rapid quality control testing of sterile and non-sterile pharmaceuticals and consumer products. Through its biologics testing solutions segment, the company offers specialized testing of biologics that are normally outsourced by global pharmaceutical and biotechnology companies. And finally, its avian vaccine services subsidiary provides specific-pathogen-free fertile chicken eggs, as well as related chickens and diagnostic products that are used in the production of vaccines. Most notably, this involves veterinary vaccines. 21% of the firm's revenue came from that segment in 2021.

{kind=link}

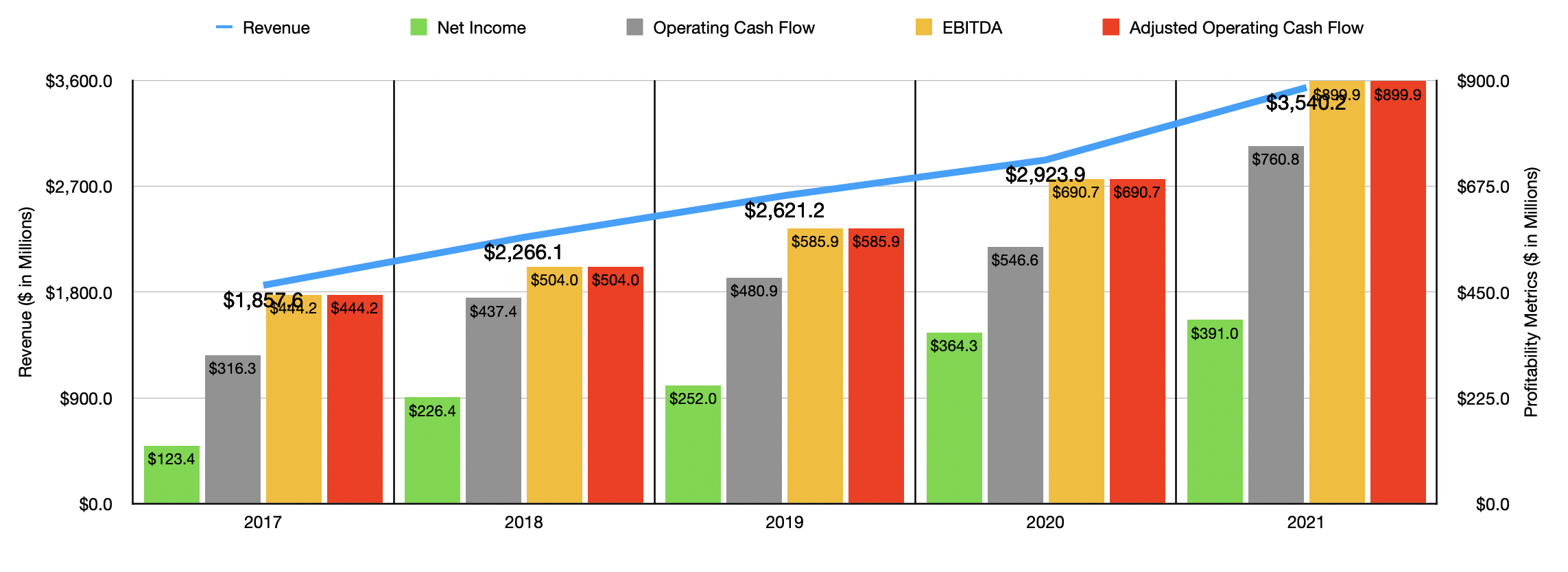

Over the past several years, the financial trajectory achieved by Charles River Laboratories was rather impressive. Sales went from $1.86 billion in 2017 to $3.54 billion in 2021. In no single year during this time did revenue drop. The largest increase for the company during this time came from 2020 to 2021, when revenue jumped 21.1%. This increase, management said, was driven by broad-based growth across all three segments. The Research Models and Services segment, for instance, saw revenue spike by 20.9%. This increase, management said, was driven mostly by higher research model product revenue across all the geographies in which it operates. The Discovery and Safety Assessment Segment reported a year-over-year increase of 14.7%, with sales rising mostly because of high demand from biotechnology and global biopharmaceutical clients, as well as robust pricing for services that the company offered. Two different acquisitions the company made also added $18.3 million to the company's top line. And finally, the Manufacturing segment reported a massive 44.1% increase in sales, with revenue shooting up from $515.4 million to $742.5 million. $109.9 million of this sales increase came from two different acquisitions. But the company also benefited from higher service revenue related to its biologics testing solutions business, as well as increased demand for endotoxin products in its microbial solutions business.

On the bottom line, the trajectory for the company has been very similar to what it has been for sales. Net income, for instance, jumped from $123.4 million in 2017 to $391 million in 2021. Once again, in no one year did the company experience a profitability decline. Other profitability metrics followed a very similar trajectory. Operating cash flow shot up from $316.3 million to $760.8 million over the five-year window covered. Meanwhile, EBITDA for the company rose consistently, climbing from $444.2 million to $899.9 million.

{kind=link}

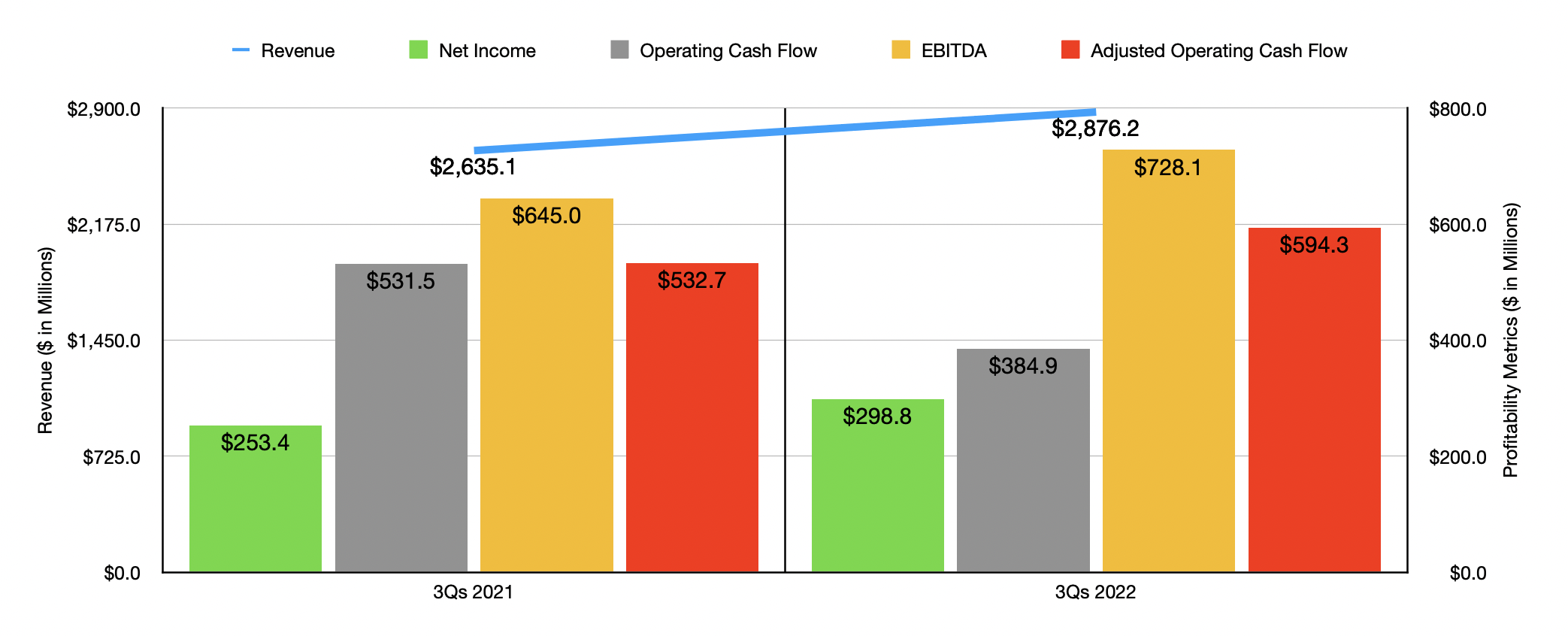

Growth for the company continued into the 2022 fiscal year. For the first nine months of the year, revenue came in at $2.88 billion. That represents an increase of 9.1% over the $2.64 billion reported one year earlier. The greatest increase here for the company came from the Discovery and Safety Assessment segment, with revenue spiking 11.6% from $1.57 billion to $1.76 billion. This rise, management said, was mostly due to service revenue that increased because of higher demand and increased pricing for services. One of the aforementioned acquisitions also added $3.3 million to the sales increase. With the increase in sales for 2022 also came higher profits. During the first nine months of 2022, net income came in at $298.8 million. That stacks up nicely against the $253.4 million reported one year earlier. Operating cash flow actually fell year over year, dropping from $531.5 million to $384.9 million. But if we adjust for changes in working capital, it would have risen from $532.7 million to $594.3 million. Also on the rise was EBITDA, with the metric increasing from $645 million to $728.1 million.

When it comes to the 2022 fiscal year in its entirety, management did say that organic revenue for the company should be between 11% and 12% higher than it was in 2021. But overall revenue, because of a variety of factors, will be up a more modest but still impressive 10% to 11%. Earnings per share should be between $7.90 and $8.05, while operating cash flow should be around $700 million. It's worth noting though that changes in working capital already impacted operating cash flow rather materially in the first nine months of the year. If we adjust for that, it's likely that the figure will be closer to $848.8 million based on my estimates. The earnings per share for the company, meanwhile, would imply net income of around $409 million at the midpoint. If we assume that EBITDA will rise at a similar rate to what adjusted operating cash flow should, then we should anticipate a reading of around $1.02 billion for the year.

{kind=link}

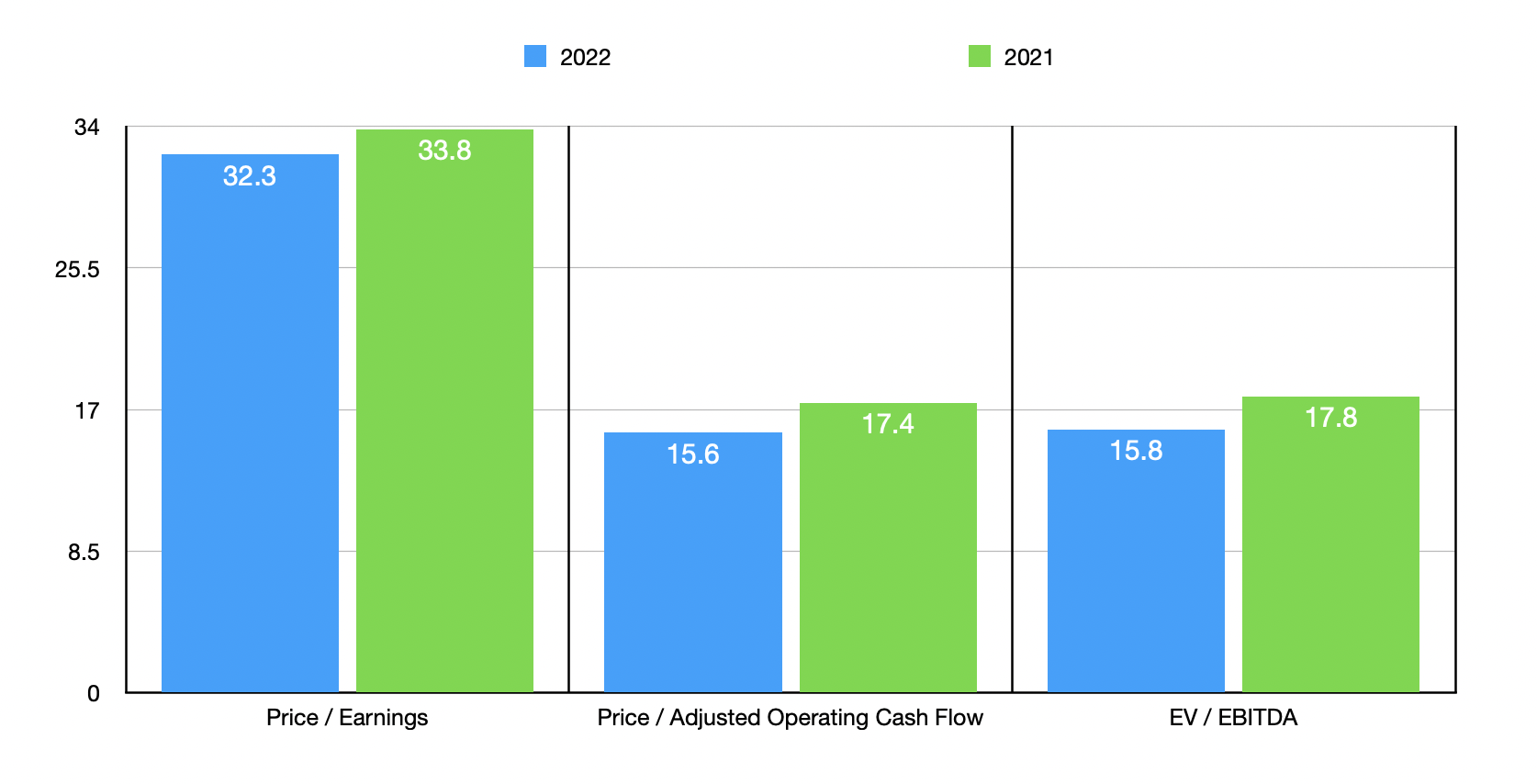

Based on these figures, the company is trading at a price-to-earnings multiple of 32.3. This is very high, but it's also slightly lower than the 33.8 reading that we get using data from 2021. More reasonable is the price to adjusted operating cash flow multiple, which comes in at 15.6. That's down from the 17.4 reading that we get using data from the year prior. And finally, the EV to EBITDA multiple for the company should drop from 17.8 to 15.8. As part of my analysis, I also compared the company to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 4.1 to a high of 66.2. And when it comes to the EV to EBITDA approach, the range was from 3 to 41.6. In both cases, two of the five firms were cheaper than Charles River Laboratories. And finally, using the price to operating cash flow approach, the range was from 14.4 to 69.3. In this case, only one of the five companies was cheaper than our prospect.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Charles River Laboratories International |

| 32.3 |

| 15.6 |

| 15.8 |

| Bio-Techne Corporation ( TECH ) |

| 44.3 |

| 38.9 |

| 28.2 |

| Bio-Rad Laboratories ( BIO ) |

| 4.1 |

| 54.0 |

| 3.0 |

| Qiagen ( QGEN ) |

| 24.6 |

| 14.4 |

| 14.0 |

| Repligen ( RGEN ) |

| 66.2 |

| 69.3 |

| 41.6 |

| Bruker ( BRKR ) |

| 39.6 |

| 45.2 |

| 21.5 |

Takeaway

Fundamentally speaking, Charles River Laboratories is a solid business that will likely continue to perform well in the long run. Truth be told, shares of the company are a bit loftier than I would normally be attracted to. At the same time, however, I find myself drawn not only to the company's business model, but also its consistent growth for both its top line and bottom line results. This certainly deserves something of a premium. Even being a bit lofty, the company is still near the lower end of the scale when compared to similar businesses. All of these factors combined to make me content with rating the company a very soft 'buy' at this time.

For further details see:

Charles River Laboratories International: A Great Business At A Decent Price