CRL - Charles River Laboratories: Mr. Market Went From Overvaluation To Undervaluation

2023-11-26 09:13:34 ET

Summary

- Charles River Laboratories provides essential products and services to accelerate research and drug development efforts.

- The company benefits from competitive advantages thanks to the entry barriers, since its clients usually opt for suppliers with greater scale and reputation.

- During 2021, the market overvalued the company's shares, but the current price seems attractive and there have been no structural changes in the business.

Investment Thesis

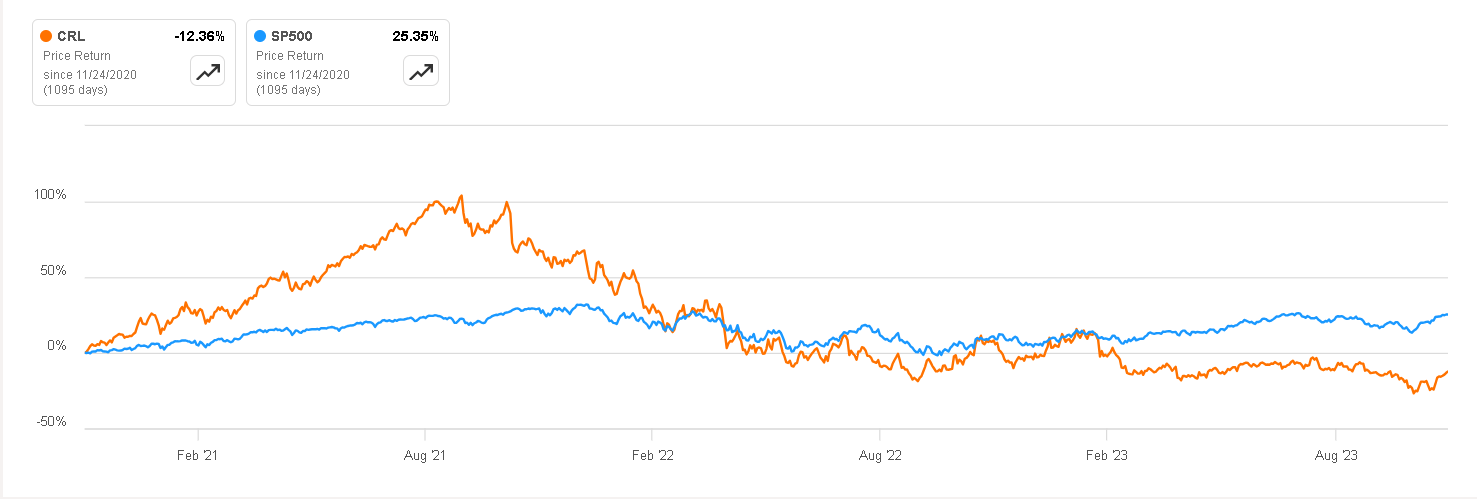

Charles River Laboratories ( CRL ) operates in the lucrative and stable Diagnostics & Research sector for biopharmaceutical companies. The company was a remarkable outperformer , delivering impressive returns of 15% annually compounded over 21 years, reaching its zenith in 2021. However, this success was accompanied by substantial overvaluation, leading to a subsequent decline of almost 60% from its all-time highs.

This situation prompts the question of whether the current state presents a favorable entry point or if there are underlying structural issues justifying the market's correction. In this article, we will delve into the company's business model, exploring the benefits of operating in this sector. Additionally, we'll assess the factors that may have contributed to the market transitioning from overvaluation to undervaluation within a span of two years.

Performance vs S&P500 (Seeking Alpha)

{kind=link}

Business Overview

Charles River Laboratories provides essential products and services to help pharmaceutical and biotechnology companies, government agencies, and academic institutions accelerate their research and drug development efforts. The outsourced drug discovery services are commonly used by pharmaceutical and biotechnology companies to improve efficiency, use the expertise of laboratories specialized in the creation of specific drugs, cost-effectiveness, and strategic flexibility, that's why Charles River plays a crucial role in the drug development process .

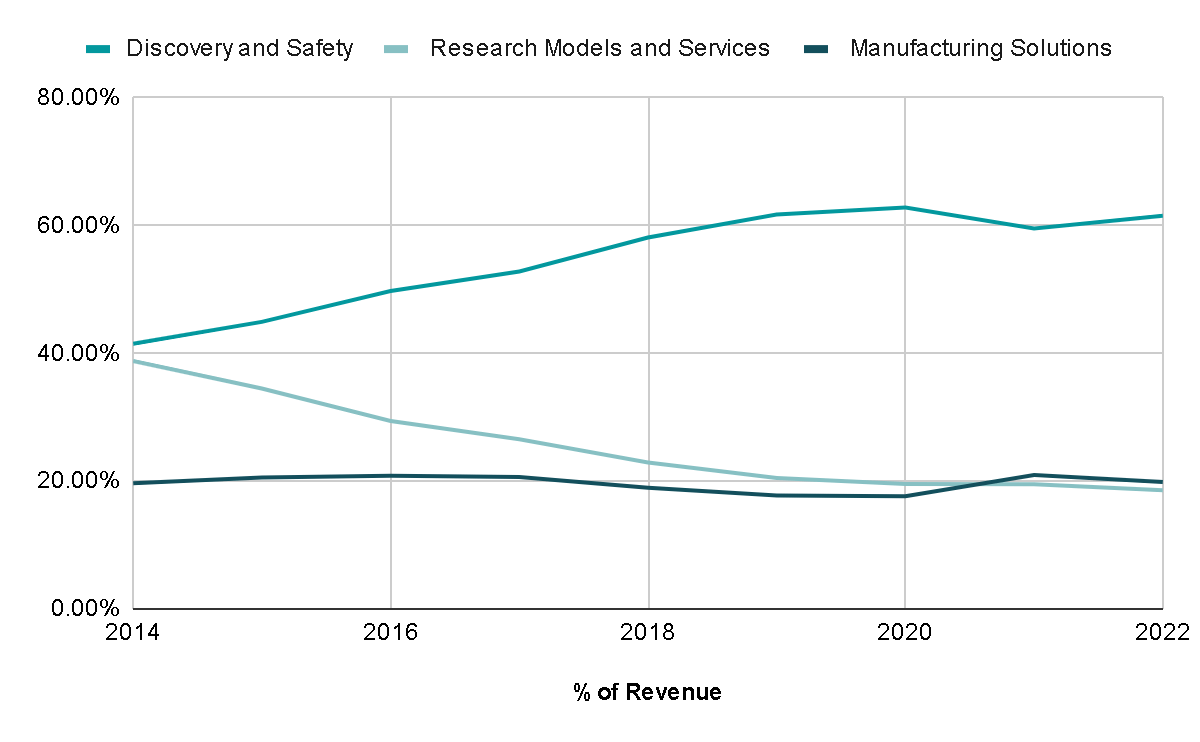

The company operates under three main segments : Research Models and Services, Discovery and Safety Assessment and Manufacturing Solutions.

Currently, 63% of revenue comes from the Discovery and Safety segment, which ten years ago represented only 41%. Also, the Research Models and Services segment has increasingly lost less weight in sales and currently represents 19%. Below we will delve into each segment to understand why this radical change has occurred.

{kind=link}

Discovery and Safety Assessment

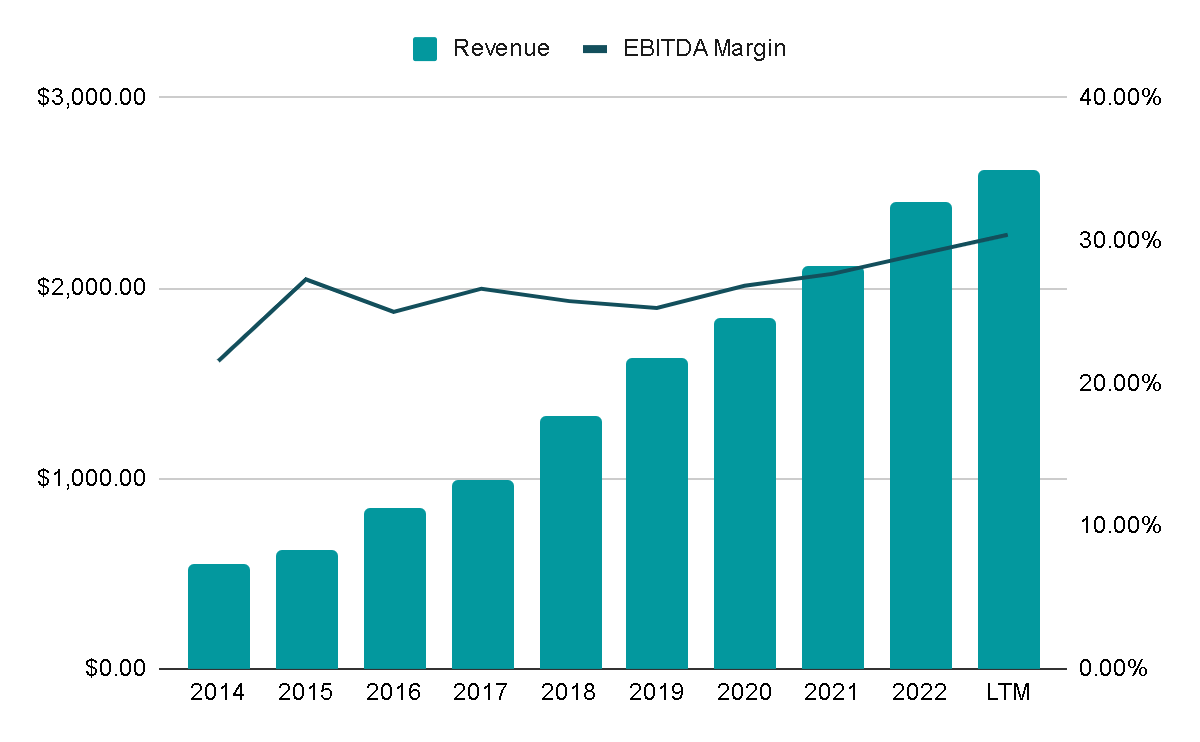

Let's first examine the segment that has reported the most significant growth in the last decade, at a rate of 20% annually, making it the segment with the highest weight in the distribution of sales.

In this segment, the company provides services that allow its clients to outsource their innovative drug discovery research and preclinical drug development activities. They also offer assistance with the regulatory-required safety testing of potential new drugs, vaccines, veterinary medicines, and medical devices. In general, these services address the needs of large global pharmaceutical companies seeking to transition to an outsourced drug development model to reduce fixed costs and gain access to additional scientific expertise and capabilities.

{kind=link}

In the past, I have analyzed companies that offer services similar to these, such as Medpace and IQVIA . Typically, these companies have EBITDA margins around 20% in segments similar to this one. In contrast, CRL's margins have averaged 25%, indicating a more profitable business in a sector with great and stable demand and from which mid-single digit growth is expected in the next decade.

Manufacturing Solutions

In this segment, the company collaborates with clients in the biopharmaceutical industry to ensure the quality and safety of production and release of commercial therapies and products manufactured by them. This involves conducting quality control testing, developing processes, and manufacturing advanced therapies, including Cell and Gene Therapy (C>) drugs. In this manner, the company supports the entire journey from clinical trials to the full-scale commercial production of these advanced treatments.

As the products in this segment mainly consist of tests, consumable cartridges, and reagents, a significant portion of the segment's revenues comes from recurring sources . An example of such products is the Endosafe test, which is regularly used by customers for lot release testing of medical devices and injectable drugs to detect endotoxin contamination.

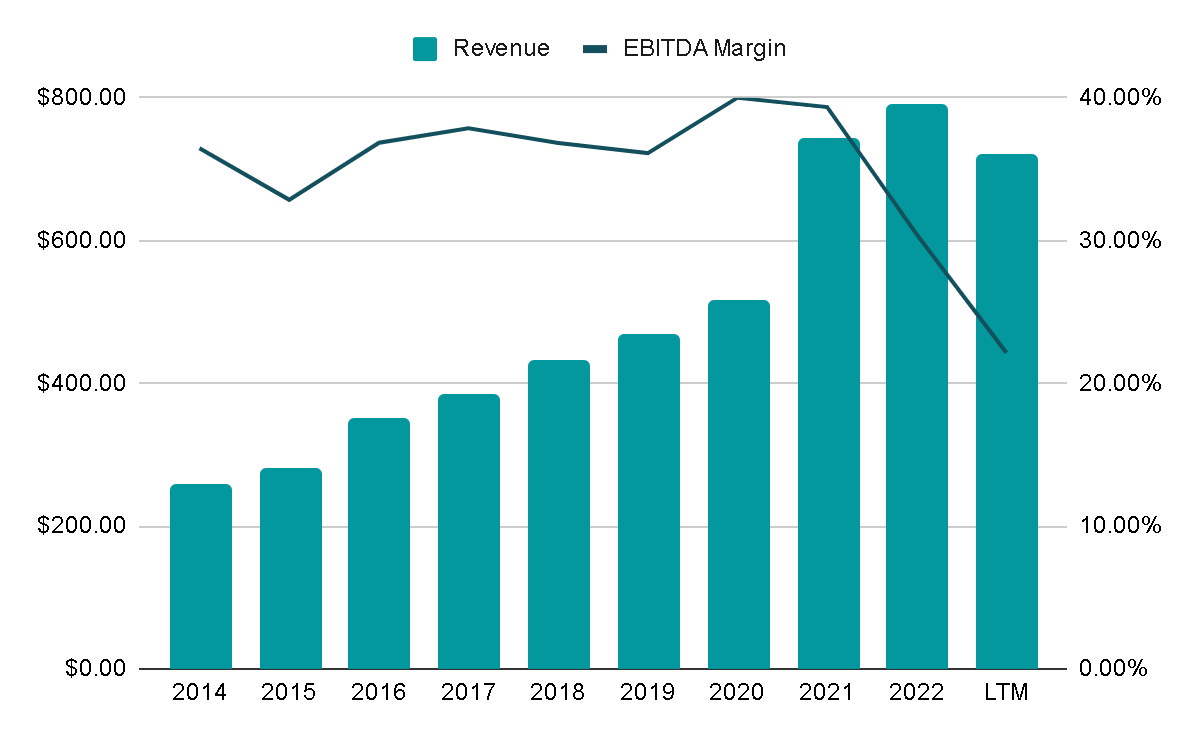

Revenue from this segment showed annual growth of 15% over the last decade, maintaining an average EBITDA margin of 36%. However, in December 2022, the company sold the Avian Vaccine Services business, which was previously included in this segment. This resulted in the removal of almost $19 million in sales generated by Avian. In addition to the loss of Avian's EBIT, the company recorded an impairment in this segment, which explains the significant drop reported in the EBITDA margin.

{kind=link}

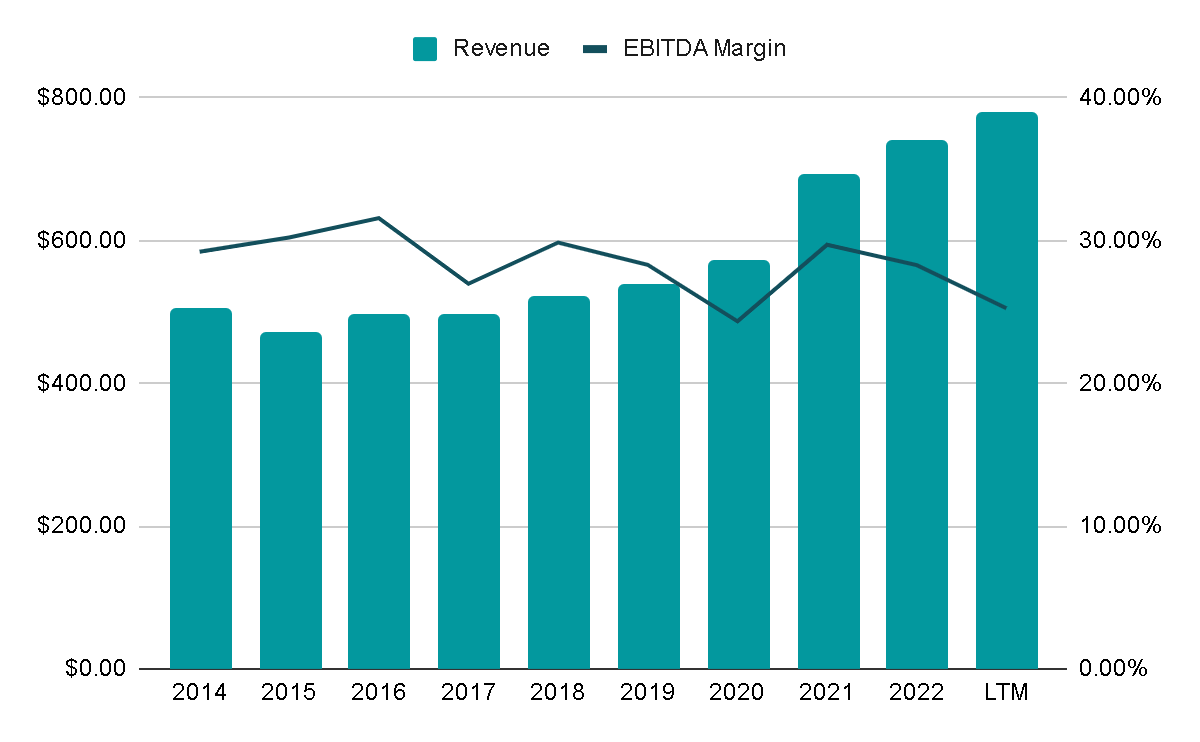

Research Models Services

In this segment, the company provides solutions tailored to support clients in utilizing research models for basic research and screening non-clinical drug candidates. These services meet the outsourcing needs of pharmaceutical and biotechnology companies, allowing them to focus on core aspects of drug discovery. The services encompass tasks such as maintaining and monitoring research models, as well as managing research operations for government entities, academic organizations, and commercial clients.

A significant portion of these models includes genetically engineered mice and rats , along with other species commonly used in biomedical research. These models play a crucial role in studying diseases, testing drugs, and advancing scientific understanding. Despite the negative press surrounding the use of animals in clinical tests, the reality is that these animals remain essential for the progress of biomedical research.

While this segment has consistently grown at 5% annually over the last decade, with average EBITDA margins of 28%, it has experienced a reduction in sales weight. This decline is not due to lack of growth or poor margins; in fact, the segment has performed well. However, other segments within the company are growing considerably more, suggesting that the company is prioritizing its focus on their continued growth

{kind=link}

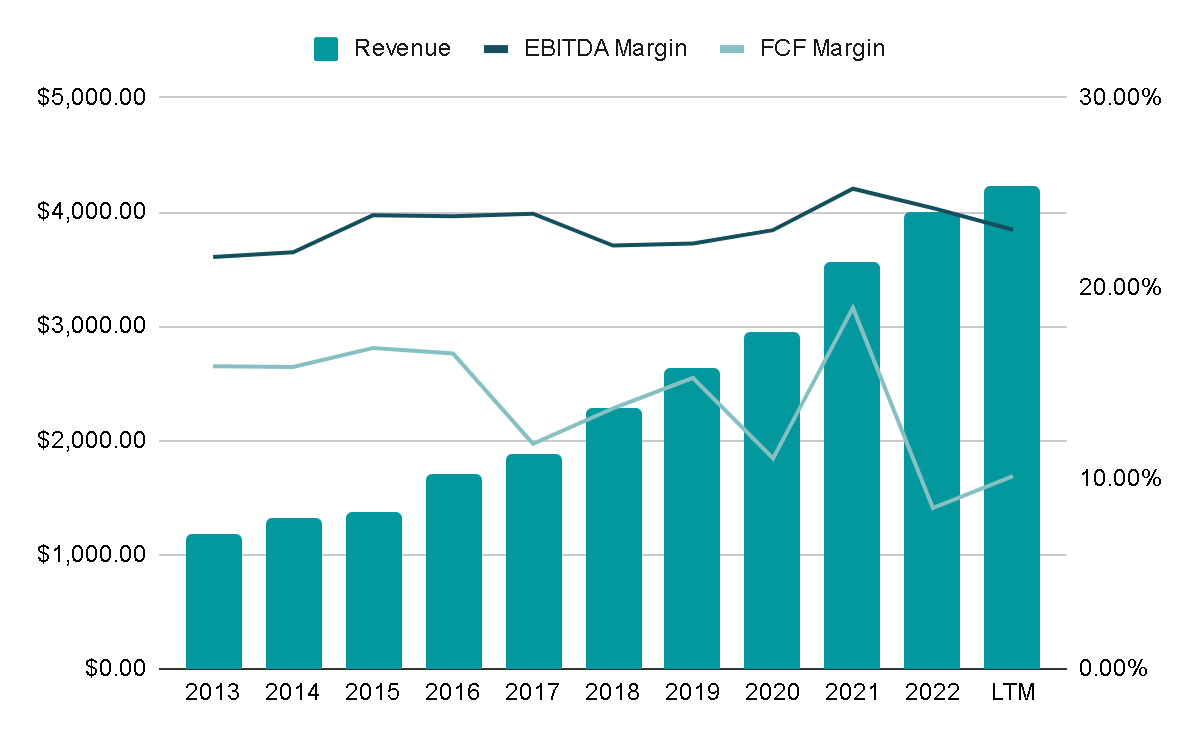

Key Ratios

Overall, across the three segments, the company has achieved annual revenue growth rates of 15% over the last decade, maintaining relatively stable average EBITDA margins of 23%. On the other hand, the Free Cash Flow margin has decreased compared to the margins maintained ten years ago, but later we will see why this is due.

{kind=link}

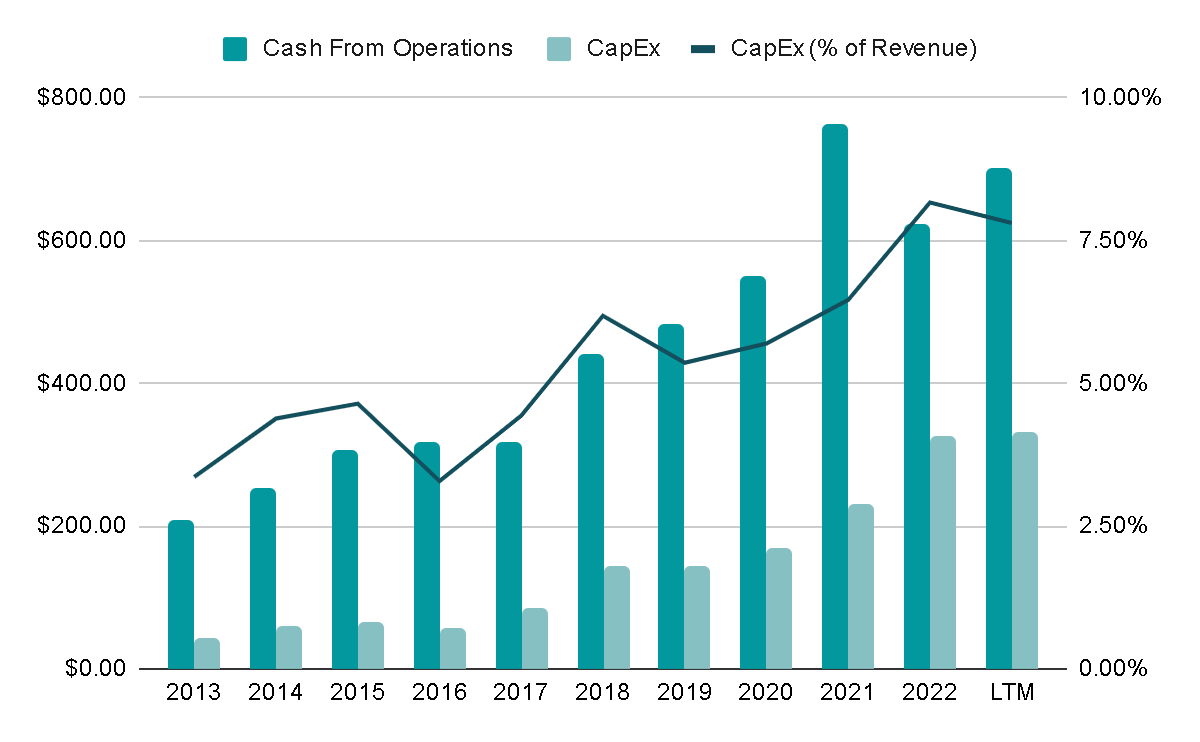

When examining the cash flow statement, it's evident that the company consistently generates increasing cash from operations each year, which is a positive trend. However, this enhanced cash generation is not fully reflected in Free Cash Flow. The reason behind this is the company's growing investment in Capital Expenditures . These investments are directed towards ensuring compliance with applicable regulations, supporting business growth, and making strategic acquisitions. Notably, management appears to be adopting a more conservative approach to capital spending and during the year they slightly reduced the guidance of CapEx that will be used for the full year.

The year-over-year increase was primarily due to favorable changes in working capital as well as lower capital expenditures. For the year, we have narrowed our free cash flow guidance to a range of $340 million to $360 million.

We continue to take a disciplined approach to managing our capital deployment and are committed to aligning our capacity and capital investments with the current demand trends.

{kind=link}

The company has capitalized on market fragmentation by implementing a consolidation strategy through acquisitions. This approach aims to expand the portfolio of products and services, leverage economies of scale, and broaden the geographic footprint.

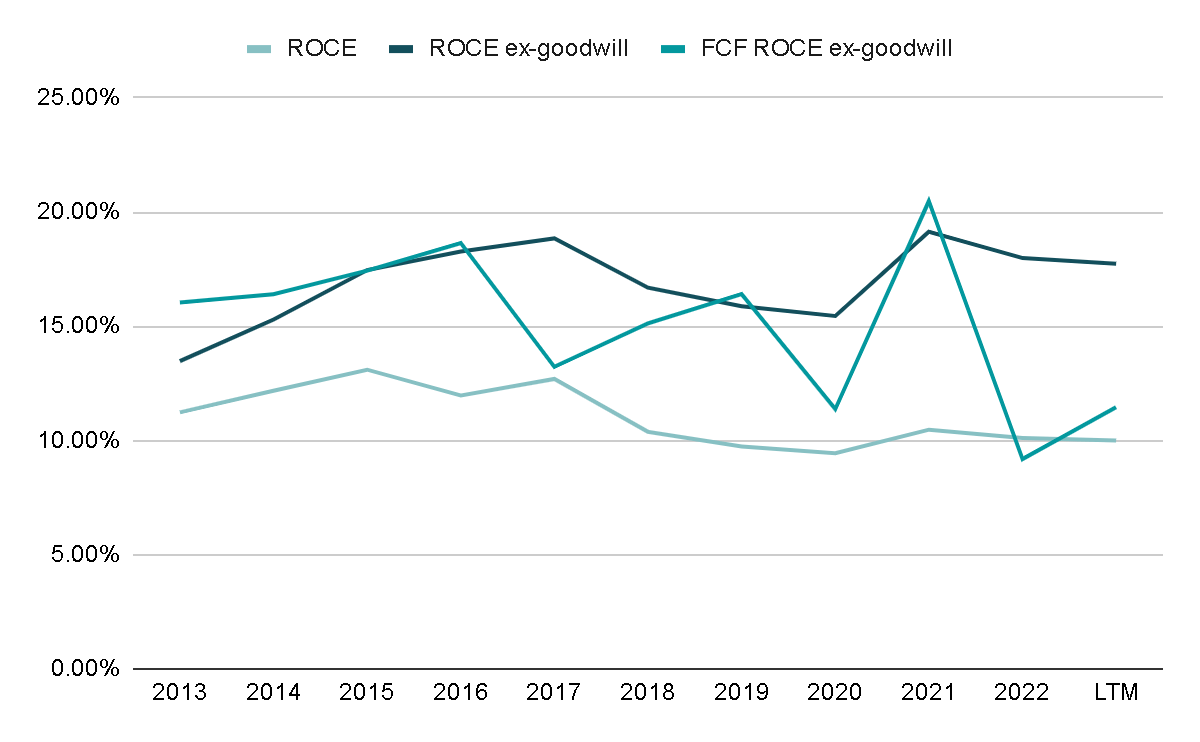

To assess the value generated for shareholders through these acquisitions, we can analyze the Return on Capital Employed. Over the last decade, this ratio has averaged 11%. However, it's important to note that this ratio is influenced by the goodwill burden resulting from numerous acquisitions. When adjusting for goodwill to provide a more accurate reflection of the underlying profitability, assuming the company halts growth through acquisitions in the future, the average ROCE over the last decade rises to 17%.

In the last five years alone, the company has dedicated 16% of the capital employed, equivalent to $3.3 billion, to acquisitions, reaffirming its clear capital allocation policy.

{kind=link}

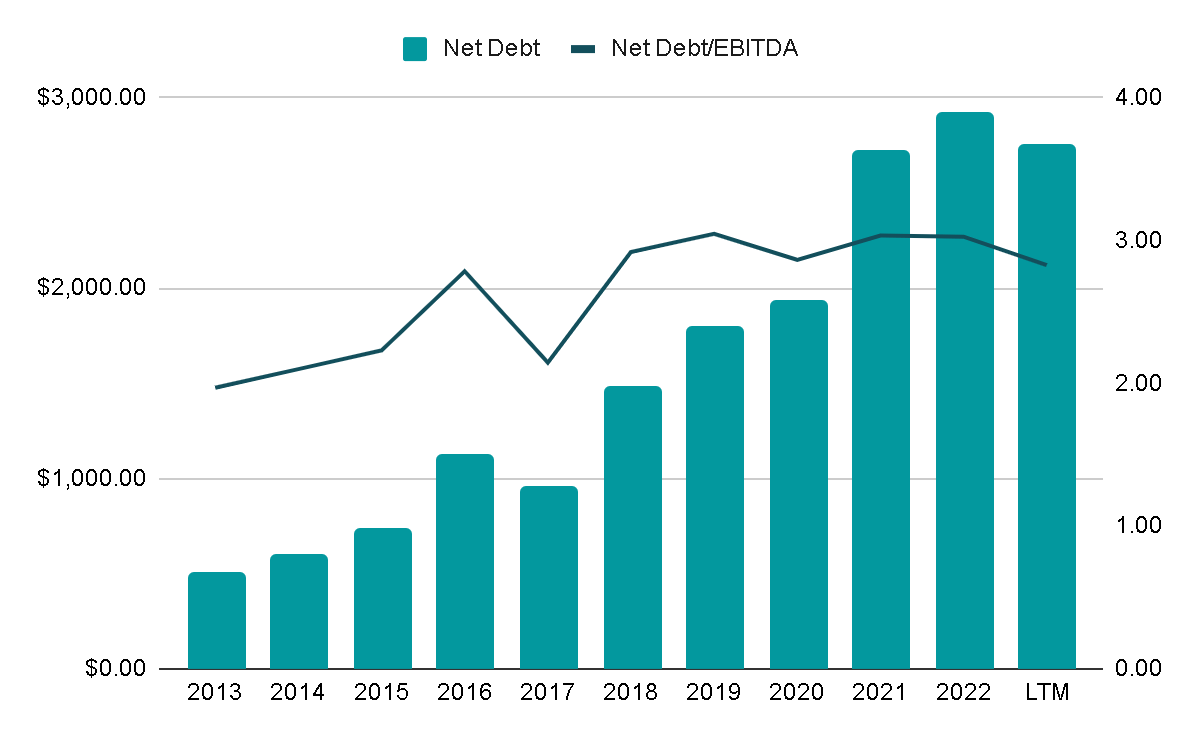

A concerning aspect is that Charles River has consistently relied on debt issuance to fund its growth through acquisitions. Over the last five years, a substantial 86% of the capital used for these purposes came from debt, while only 13% originated from cash generated by operations.

As of now, the company holds $2.9 billion in debt , with 52% in bonds maturing in 2028, 2029, and 2031, featuring an average fixed interest rate of 4%. The remaining debt is in a revolving credit facility, which the company is prioritizing paying down in the coming months.

We continuously evaluate our capital priorities and intend to deploy capital to the areas that we believe will generate the greatest returns. Over the longer term we continue to believe that strategic acquisitions will generate the greater shareholder returns by enhancing our growth potential. But in the near term, we intend to continue to focus on debt repayment.

Presently, the Net Debt/EBITDA ratio stands at around 2.8x, which is relatively high. It is expected that the company will continue efforts to reduce this ratio, especially considering that in 2021, it reached levels as high as 3.05x

{kind=link}

Valuation

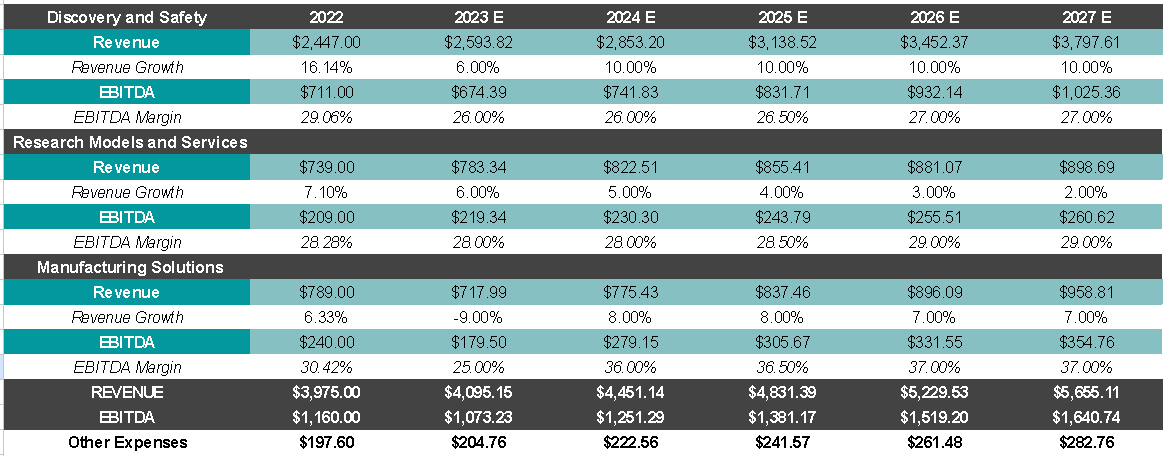

To estimate the intrinsic value of the company, I plan to project the growth of each segment based on historical behavior and the performance of the last twelve months.

For the Discovery and Safety segment, which is the most significant in sales, I anticipate a year-over-year revenue growth of 6%, considering the growth in the last twelve months. Subsequently, I expect a compounded annual growth rate of 10%, slightly lower than the 20% annual growth observed over the last decade. Additionally, I anticipate a slight expansion in EBITDA margins, reaching 27%.

In the Research Models and Services segment, I anticipate moderate growth of 3.5% compounded annually, aiming for margins of 29%, a level achieved in previous years.

Regarding the Manufacturing Solutions segment, despite the impact of the Avian divestment, I anticipate annual growth rates of 7 to 8% in the coming years. I expect the segment to recover its high margins in the future when the impairment stops affecting profits.

{kind=link}

This projection would result in a revenue growth of 8.5%, which appears to be a fairly conservative estimat e. During the Investor Day in September , the management mentioned an expected growth of 6 to 8% organically. Therefore, the final growth could potentially reach double digits.

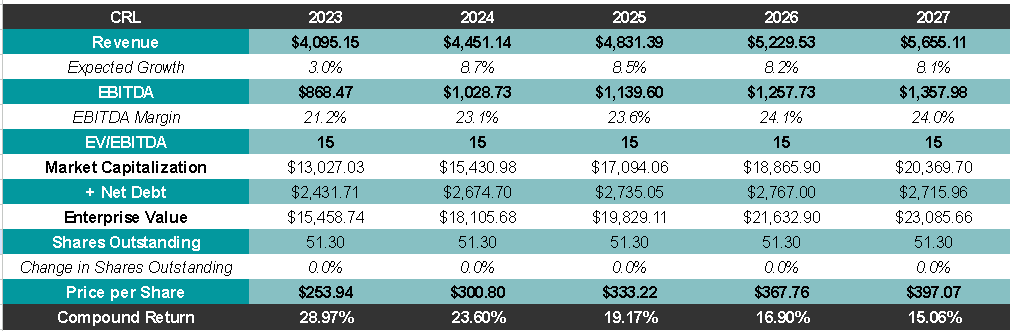

To determine the consolidated EBITDA, we need to deduct the 'Unallocated Corporate Expenses' item, typically representing 5% of revenue. This would provide the company's total EBITDA. Applying a 15x EV/EBITDA multiple, the projected share price within five years could be nearly $400 USD. This implies a 15% annual return compared to the current price of $197 USD, suggesting an attractive valuation even with a somewhat conservative estimate.

{kind=link}

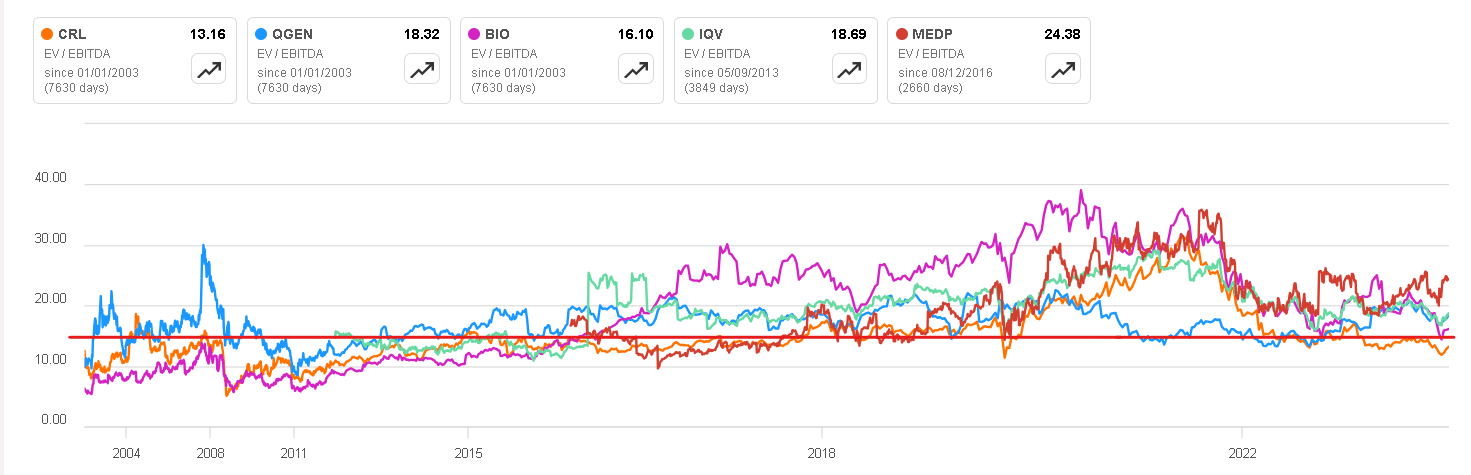

In the following image we can see how the average EV/EBITDA multiple of the company and some competitors and comparable companies is usually around 15x on average, which is why I chose this exit multiple in the valuation.

{kind=link}

Final Thoughts

Charles River Laboratories appears to be a high-quality company, boasting a business model fortified by formidable barriers to entry, particularly in terms of scale and reputation. The challenge for potential new competitors lies in the difficulty of swiftly disrupting the sector with low prices. Customers choose their suppliers based on a track record of successful clinical trials and the capacity to deliver at a large scale. These competitive advantages are evident in the company's robust margins.

Moreover, the valuation appears to have reverted to reasonable levels after reaching 30x EBITDA in 2021. With conservative assumptions, the potential for a substantial return seems promising. Given these factors, I consider the company to be a ' buy ' opportunity.

However, there are risks and aspects to monitor. One key area is the level of debt, which warrants close attention to ensure that management fulfills its commitment to reduce it. Additionally, there is the risk of the company making acquisitions that are either overpriced or fail to deliver the anticipated value, potentially resulting in impairments and temporary damage to profits.

For further details see:

Charles River Laboratories: Mr. Market Went From Overvaluation To Undervaluation