IBKR - Charles Schwab: It's Not Cheap And There Is Not A Catalyst Yet

2023-11-29 06:48:51 ET

Summary

- Charles Schwab is facing headwinds due to high interest rates and a decline in deposit accounts, impacting its margins.

- The company's growth prospects include adding new brokerage accounts and managing client assets, but these may not be strong catalysts for the stock price in the short or medium term.

- Compared to traditional banks, SCHW's business model is less resilient and its stock price is not attractive, making traditional banks a better investment option.

- We rate the stock as a hold, as we think that is still a solid name, but there are better alternatives.

We rate Charles Schwab (NYSE: SCHW) ((CS)) as a hold as the company is still facing certain headwinds associated with the high interest rates and there is not a clear catalyst in the near term. One of the factors that has concerned investors is the cash sorting strategy of CS's clients, which means that deposit accounts are being reduced as clients want to take advantage of money market funds given their high returns offered due to the Fed's policy of interest rate hikes in the last two years. As a result, the margins are being pushed down, so the market is expecting some visibility about CS's future performance. We will assess if CS deserves to be on your radar, and we will estimate its intrinsic value. The stock price is not attractive now considering the price/book value, as our preferred metric to gauge the valuation multiple of a bank given that it incorporates the quality of the balance sheet, which is a very important factor to include in any bank's valuation. Let's review the company.

Business model and Q3 2023 results

CS is a corporation that offers loan and saving services and is also involved in offering other services such as wealth management, banking, asset management, custody, and financial advisory services. CS could be seen as a bank, but its loan portfolio barely represents around 8% of the total assets, while the revenues associated with loans only represent 10% of the total interest income.

A traditional bank, as we assessed in our previous article about Bank of America (BAC), used to have a loan portfolio that represented around 30% of its total assets.

Author, Quarterly reports

In the table above, we can see why CS is seen more as a brokerage firm than a bank, as most of its revenues come from its brokerage services. We cannot dismiss the Available for Sale ((AFS)) and Held to Maturity ((HTM)) securities as both types of investments contribute to around 37% of CS's interest income combined; we will talk about them later in this article.

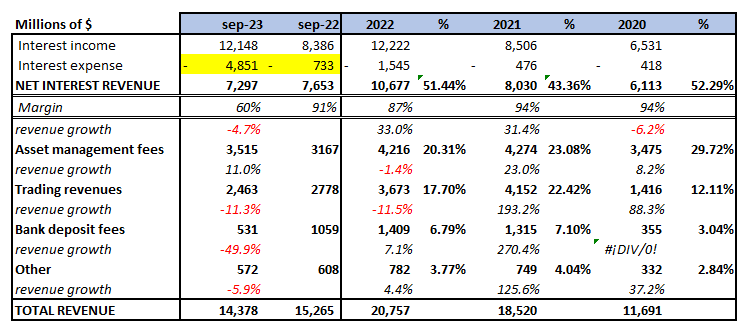

Even with these characteristics, we see CS as a hybrid, a combination of a bank and a brokerage firm, as its most important source of funding within the liabilities is the deposits, like a traditional bank. Now, exploring a more general revenue breakdown, including all the CS's revenue sources, we can see something that concerns some investors:

Revenue Breakdown (Author, Annual Reports)

{kind=link}

Indeed, since 2022, interest expenses have surged substantially, particularly in September 2023 YoY, as shaded in yellow in the table above. Also, we see how the net interest revenue experienced a negative growth of -4.7% in September 2023 YoY. The factor behind this can be seen in the following table, which shows the breakdown of interest expenses:

Author

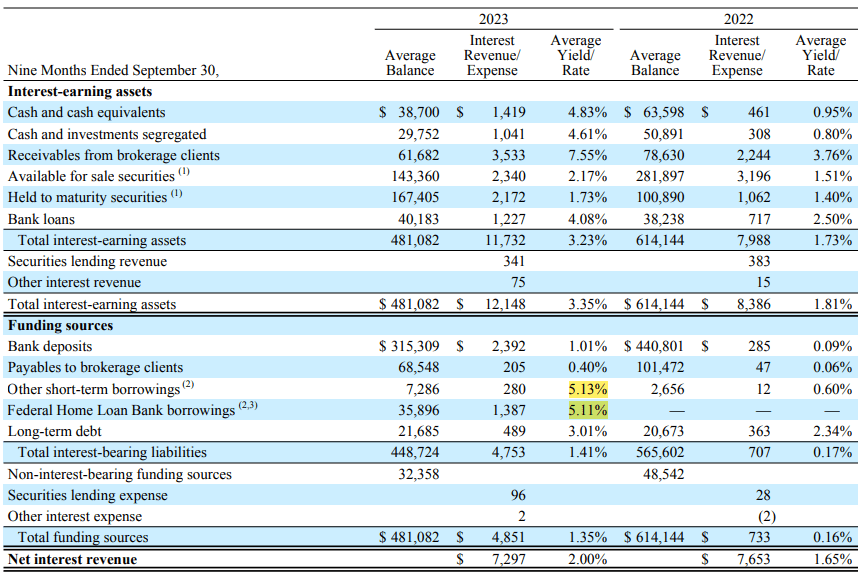

We see that there are two factors pushing up the whole interest expense associated with the higher cost of short-term funding: the higher rates paid to deposits and the higher cost of the Federal Home Loan Bank's ((FHLB)) advances, higher costs aligned with the Fed's interest rate hikes, and we can see much more clearly how those costs increased substantially in the next table:

{kind=link}

We can see how the cost of the most important CS's sources of funding, such as those related to bank deposits and FHLB advances, increased significantly; for example, the yield rate from deposit banks increased from 0.09% in December 2022 to 1.01% in September 2023. The same behavior is seen with FHLB advances, whose yield rate increased from 0.6% to 5.13% in the same period.

In the same table, we see that deposits are declining and the FHLB advances are increasing; we can picture the problem by looking at the next chart:

Charles Schwab Monthly Client Metrics

CS's deposits were declining as clients were taking out their money from their deposits in CS to relocate it into the money market funds to harness a way better yield of 5% compared to the 1% offered by those deposit accounts. In order to satisfy the demand for that cash in deposits from its clients, CS issued brokerage CDs and used FHLB advances to pay that demand for cash.

CS is a member of the FHLB system, so CS can get access to liquidity from this government-sponsored enterprise, which was created to support mortgage lending and community investment. This is thanks to the focus of CS's loan portfolio on residential real estate loans through the offer of First Mortgages and home equity lines of credit (HELOCs).

In the chart above, we can see that deposits dropped around $200 billion since October 2022, so it's understandable that the market is concerned about this issue as there would be more withdrawals in scenarios where the Fed keeps raising interest rates and CS would need to keep using more expensive sources of funding to please the demand of its clients.

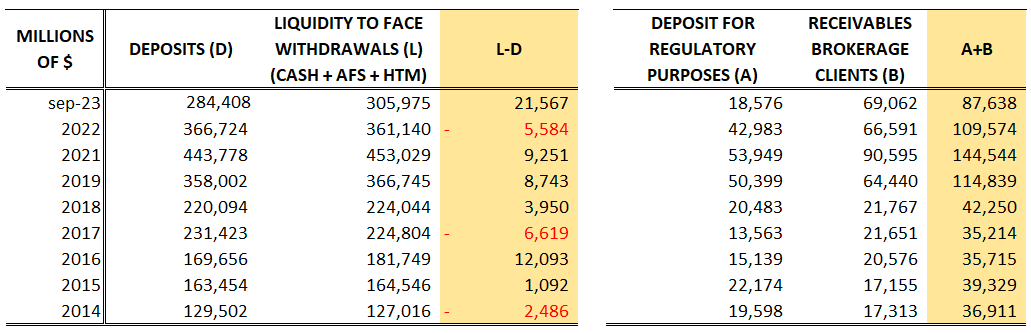

In order to dissipate any concern about the CS's liquidity, we elaborated a table that shows that the CS is well covered to face even harder scenarios:

{kind=link}

We can see the liquidity needed to face a scenario where the withdrawals reach 100% of the deposits. Deposits can be fully covered using CS's liquidity to face withdrawals such as cash, AFS, and HTM securities with an excess of $21.5 billion ((L-D)) as of September 2023. Of course, there were years when that liquidity was not enough to cover deposits, but we should remember that CS holds deposits for regulatory purposes and receivables brokerage clients to cover that additional demand for liquidity (A+B).

In addition, even if we take an even worst-case scenario where deposits for regulatory purposes and receivables of brokerage clients are not enough to cover its clients' deposit accounts, and in cases where CS is not able to use sources of funding, CS is under the Federal Deposit Insurance Corporation's FDIC insurance, which protects up to $250,000 per depositor.

Last but not least, CS is a member of the Securities Investor Protection Corporation ((SIPC)), which protects clients from brokerage firms in the rare cases where these firms get into bankruptcy and clients' assets are lost due to fraudulent practices and other causes.

As such, we should point out that the concerns of the market about CS might not be associated with its solvency but with the pressure on its interest expenses given the high interest rates managed by the Fed and the CS's requirements to get more expensive short-term funding, which would impact its margins more.

Of course, if the Fed keeps raising interest rates, that would add additional pressure to the interest expenses, impacting even more of CS's net margins; in that scenario, we would expect a further decline in the stock price. However, we do not think that the Fed will continue with this policy, so there is a chance that interest rates might have reached a ceiling. We will discuss later if the current stock price is attractive or not.

Growth prospects

CS has added 2.9 million new brokerage accounts in 2023, reaching a total of 34.5 million accounts. In the first nine months of 2022, CS added 3.1 million new brokerage accounts, so there was a slowdown in the growth of new accounts but nothing critical.

As of September 2023, CS manages $7.84 trillion of client assets, higher than the $7.05 trillion in 2022 but still lower than the $8.14 trillion managed in 2021; however, with the acquisition of Ameritrade in 2019, CS is transitioning $1.8 trillion of new client assets, 16.6 million client brokerage accounts, and about 3.6 million trades per day. Ameritrade will bring lots of growth opportunities once the integration is completed.

Historically, CS has achieved organic growth of 5% to 7%, and now the management is working to deliver a net new asset (NNA) growth of 3% to 5% from CS's existing clients and 2% to 3% of NNA growth from new clients in the next few years, according to the last fall business update . The management is focusing its efforts on reinforcing the improvements in the client's experience using CS's platforms in such a way that clients get industry-leading value, exceptional service, and transparency in every interaction they have.

CS is developing new ways to build new growth opportunities through bank loans while reinforcing the wealth management segment; indeed, one of the types of loans offered by CS is the Pledge Asset Line ((PAL)), which represents around 33% of the total loan portfolio as of September 2023 and has been playing an important role in the wealth management relationships. This has been improved through the offering of a fully digital onboarding experience that enables advisors to get access to PAL for their clients. This new PAL process takes way less time to submit while getting approval for applications in just one or two days.

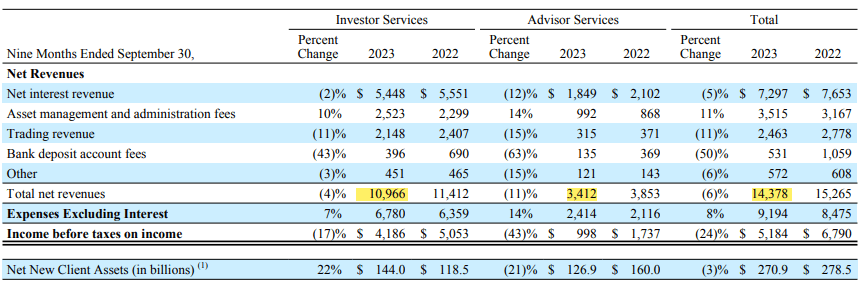

These kinds of improvements enable advisors to compete with banks while retaining assets. In this sense, CS is investing strongly in advisory services, as these services represent around 23% of the total net revenue if we show a revenue breakdown according to the segment, Investor and Advisor Services:

{kind=link}

CS has around $530 billion in retail assets receiving ongoing advisory services, which means that these clients see CS's advisory services as a place to get advice, so it's understandable to be more focused on this area as a way to make this area bigger from the total net revenues.

Another CS business opportunity is related to the workplace business as it enables millions of participants to get a fresh approach to stock or retirement plan options. Many of these employees are investing for the first time, which represents an opportunity for CS to offer future retail and adviser services. The CS's workplace segment connects more than 5,500 employers, 2,700 advisory firms, and 2.5 million investor households. As such, this business has the capacity to attract recurrent new clients in the next few years through the NNA of existing clients and the NNA of new clients.

However, even when all of these growth prospects are interesting, neither of them would represent a strong catalyst to move the stock price in the short term or even in the middle term. Even if we think that they might work better as future catalysts in the long term, the stock would need other positive forces beyond CS's control, like the Fed's future policy. Another factor that we need to consider is whether the stock is really attractive or not and how strong CS's business model is compared to that of traditional banks or other brokerage firms. Let's see these factors.

Charles Schwab compared to traditional banks

We assess different metrics to compare CS's performance with those of the most important banks in the US. We want to show you the next table:

{kind=link}

As we mentioned before, CS is a hybrid between a bank and a brokerage firm, considering it more the latter given the important portion of revenues that comes from its brokerage services, so it would be expected that its provisions over loans are lower than other banks as its loan portfolio is more limited to some segments and represents less than 10% of its total assets compared to other traditional banks whose loan portfolios represent around 30% of their total assets.

Nevertheless, even when the CS's loan portfolio represents a lower proportion of its total assets compared to other traditional banks, its deposits still represent more than 50% of its total liabilities, representing its main source of funding, as is the case with many traditional banks, so we consider the comparison of the CS's performance with other banks relevant.

CS shows good net margins in column 4, but we would have expected that given its lower regulatory requirements, CS would have shown way better net margins than traditional banks, whose net margins are more or less similar to CS. CS shows a very good capital adequacy ratio of an average of 26.8% compared to the minimum requirement of 8%, which indicates that CS has enough capital to more than fulfill the capital requirements set by regulators.

CS is way more exposed to held-to-maturity ((HTM)) securities than any other traditional bank. In column 7 of the table above, we see that CS has HTM securities representing more than 30% of the total assets, whereas banks like Bank of America or JPMorgan (JPM) or Citi (C) have a way lower participation of these securities over their total assets, so those banks are less exposed to being impacted by the Fed's policy of more interest rate hikes.

We know that these securities are particularly affected by the Fed's interest rate hikes as their worth is reduced; this effect is even stronger for those securities with longer-term maturities, as longer-term bonds have more sensitivity to interest rate movements. As such, we've separated those securities with maturities beyond 5 years in column 8 to know how much they represent over the total HTM securities held by CS.

Maybe you would say that the CS's HTM securities with longer-term maturities only represent 71.92% of the total HTM securities held in its balance sheet, similar to the proportion held by JPM, the bank with the highest quality in risk management and profitability in the banking industry; however, in JPM's case, the overall HTM securities only represent 9% of its total assets, not 32% as in the CS's case.

We need to consider that CS did not hold HTM securities in the years 2020 and 2021 but started buying those securities strongly in 2022. As a result, its negative accumulated other comprehensive income ((AOCI)) has increased significantly from $1 billion in 2021 to $22 billion in 2022, with that negative number included as part of the equity, so the ROE jumped to 19% in 2022 from 10% in 2021. But we do not take this as something positive since the higher ROE is not a result of higher margins and revenue growth but of a reduction in the denominator through the reduction of equity while decreasing the value of important assets on the balance sheet.

In column 9, we see how CS's deposits have declined in the last 3 years, as we've seen previously when we talked about the cash sorting strategy of CS's clients to take advantage of the higher interest rates offered by money market funds. We've taken the last 3 years as we know that the global economy has experienced difficulties as a result of the pandemic, and these kinds of scenarios help us to see which business models are stronger under those scenarios.

Even if we consider CS a solid name as a brokerage firm, we see that traditional banks have business models that are more resilient to endure difficult periods, as we see, for instance, how deposits from Bank of America, JPMorgan, and Citi have increased rather than declined in the last 3 years as a result of their more diversified depositors.

Therefore, in terms of business quality, we think that traditional banks are stronger than companies like CS, so if we are thinking about buying CS shares, it would be more reasonable to incorporate banks like Bank of America, JPMorgan, or Citi first in our portfolio; we talked about these kinds of investment decisions in our previous article about Bank of America.

Now, we need to know if the CS's current stock price is attractive or not.

Valuation

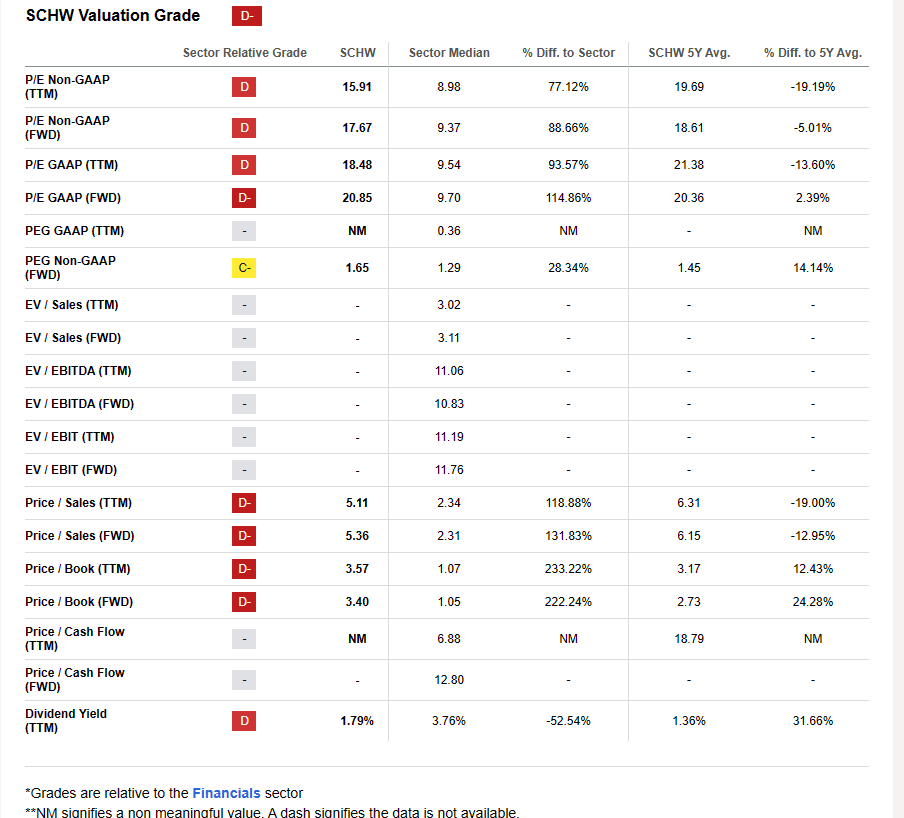

According to Seeking Alpha, CS is not cheap at all:

{kind=link}

Now, we mentioned earlier that we like to take the price/book value as a good indicator to gauge if a bank is cheap or not. The reason is that the book value ((BV)) in banks reflects well the current situation of a bank as the assets and liabilities are at their fair value. In other words, we like this ratio for banks since it incorporates the quality of their balance sheets, and given how leveraged they are by their own nature, it's critical to incorporate that quality in some way.

For instance, if the assets' value of the bank experiences a significant decline, the BV will be reduced as well. If the liabilities increase substantially, the BV will be reduced as a result. We take the CS's P/BV to be compared with that of the other peers; in addition, we've taken the average P/BV of the last 5 years in each case, so we get the following:

Author, TIKR

So, CS's P/BV is not only more expensive than its average of the last 5 years, but it's also more expensive than the P/BV of the traditional banks. Not only that, it turns out that those P/BV's of traditional banks are cheaper than their respective averages of the last 5 years.

Thus, right now, we see that the CS stock price is not cheap at all; even if the stock were cheap now, we would consider Bank of America, JPMorgan, or even Citi first.

Risks

The main risk to our thesis is that the Fed's policy is reversed; in other words, the interest rates are actually reduced in the next few months. However, we do not think that a policy of reduction of interest rates could happen soon, as Fed officials have said that a reversal in the Fed's policy will not happen on the immediate horizon.

Another risk is related to the integration of CS's acquisition of Ameritrade, as it could certainly be a good catalyst for CS's results, particularly in 2024 when the integration might be completed. Nevertheless, we think that CS has taken a lot of time in that integration process, as that acquisition was made in 2019 and is expected to be completed in the first half of 2024.

Our impression is that CS has dedicated so many resources to that integration process, neglecting other business segments that delivered poor performance as of September 2023, such as the trading segment, whose revenue growth has been declining since 2022.

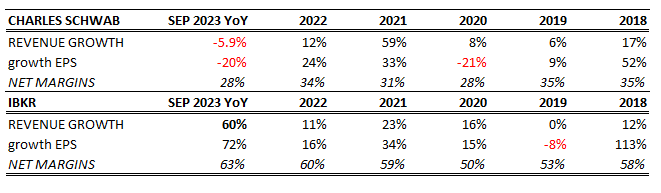

Also, as we've mentioned in the growth prospects section, CS is working in many aspects to make its platform and services more sticky, and that's something positive to compete with banks; however, we haven't mentioned anything about its closest competitor as a brokerage firm, Interactive Brokers (IBKR). IBKR is a pure brokerage firm that holds neither HTM securities in its assets nor deposits in its liabilities.

IBKR is not facing pressure in its margins due to the interest rate hikes, as in CS's case, while being a competitor offering an even wider range of products and services and access to more electronic exchanges and market centers, etc. There is no surprise that IBKR has shown a better performance in 2023 as of September 2023 in the context of interest rate hikes, as is shown in the next table:

{kind=link}

Thus, traditional banks and IBKR have shown better performance in 2023 than CS, and CS stock price is not cheap; all these combinations of factors make us think that traditional banks are better alternatives in terms of the quality of the business model and stock price.

Final Thoughts

We think that CS is not a good buy right now, as we've seen that the stock price is not cheap and there is no strong and clear catalyst that might boost the stock price in the short term or even in the middle term. In addition, we've seen that more traditional banks, such as Bank of America, JPMorgan, or even Citi, are trading at more attractive levels right now while showing more resilient business models to resist times of macroeconomic headwinds.

Therefore, if you are thinking of buying CS shares, it's more rational to consider buying some of the three traditional banks we've mentioned in the article. In addition, CS is trading at a premium considering its P/BV compared to its own average in the last 5 years and compared to traditional banks, and we do not think that it deserves such a premium given the difficult context in the economy and the high competition in its sector.

The growth prospects are interesting, but they might work better under more predictable conditions related to the Fed's policy. Another uncertainty is that CS has been working hard on the Ameritrade integration for the last 3 years, so if the results of that integration are not as good as expected, the market might punish the stock price even more.

For further details see:

Charles Schwab: It's Not Cheap, And There Is Not A Catalyst Yet