NTIP - Charlie Munger Latticework Of Mental Models Picks For August 2023

2023-08-07 09:00:00 ET

Summary

- The article discusses various investment strategies and picks from renowned investors like Charlie Munger, Ben Graham, Peter Lynch, Joel Greenblatt, Warren Buffett, and Nick Sleep.

- It covers different investment models, Graham number picks, PEG ratio with a dividend kicker, The Magic Formula, and Owner Earnings picks.

- This article also fleshes out some of my own personal philosophies and practices.

Charlie Munger's Latticework

One of the most admirable things I hold Charlie Munger in high regard for is his application of multiple philosophies to the thought process of stock picking. A good description of the basic theory of Charlie Munger's latticework comes from Robert Hagstrom's Essential Buffett. Here are a few lines of color regarding one's latticework thought process. This is highly derived from Charlie Munger's 1995 lecture at the University of Southern California entitled "Investing Expertise as a Subdivision of Elementary, Worldly Wisdom".

Wisdom is not reflected in the simple exercise of compiling and quoting facts and figures. Rather, Munger explains, wisdom is very much about how facts align and combine. He believes the only way to achieve wisdom is to be able to hang life's experiences across a broad cross-section of mental models. "You've got to have models in your head," he explained, "and you've got to array your experience- both vicarious and direct-on this latticework of models."

Business professors typically don't include physics in their lectures, and physics teachers don't talk about biology, and biology teachers don't include mathematics, and mathematics teachers don't teach psychology. But Charlie believes we must ignore these "intellectual jurisdictional boundaries" and include all models in our lattice work design. Essential Buffett pp. 19-20

A good friend of Munger's, Mohnish Pabrai, also is highly philosophical. A good, and hard-to-institute philosophy of his is to "Be like Puddy", you know, David Puddy from Seinfeld:

{kind=link}

The basis is, if you made the right decision the first time, stick with it to the end. Elaine breaks up with Puddy after this scene as all he does is nothing but watch the back of the seat on an international flight home. She cannot stand his inaction. I assume the rest of the market will feel the same way about you should you take this philosophy to heart. However, if you have a copy of Christopher Mayer's 100 Baggers , you may begin to realize that all sorts of interesting things can happen by just hanging on. Even Carl Icahn has said some of his largest returns have been small positions of stocks he just forgot about.

Pabrai is also a self-proclaimed "cloner" that gets lots of data and ideas from the best fund manager's 13F filings. I tend to do the same. This field of psychology is the most difficult of all. Trusting your analysis and ignoring the market. Both Pabrai and Warren Buffett have a hard time doing this and have jettisoned several large picks over time due to one problem or another. I have only seen Charlie Munger and the Daily Journal ( DJCO ) 13 F able to withstand any turmoil without much if any turnover.

I am widely diversified as an investor and aim for no more than a 5% turnover per year. This was about the rate Berkshire Hathaway ( BRK.B ) ( BRK.A ) turned over its portfolio on an annual basis when Robert Hagstrom was penning his three excellent books covering Buffett. Munger is the more philosophical of the two. Anyone who owns Poor Charlie's Almanack knows that it's as much about Rudyard Kipling, Cicero, and Benjamin Franklin as it is about the laws of fundamental investing.

Being a former expat of sorts in China, the philosophy of Daoism and Buddhism as well as Qigong practice has helped me in my mental models. My favorite of which is Wu Wei ??, in a sense the art of doing nothing. However, in doing nothing there is the concentration of everything. Effortless action is a better way to put it. It is a description of being in the zone and intuitively making decisions rather than fretting which often leads to inaction. Don't worry about the present or the past, do the work and let time do its job.

In addition to various philosophies, I also like several different types of valuation models, here are a few picks in different valuation model categories.

Ben Graham stocks

Ben Graham stocks can be split up into two categories. One is fair values of competitive companies and the other is the fair value of a failing business trading below cash and cash equivalents per share, or the "cigar butt". The fair value of competitive companies or the Graham Number, is one model I frequently enjoy using. It is the threshold where the P/E times the P/B does not exceed 22.5. Price targets may be set by using the square root of 22.5 X current or forward EPS X Book value per share.

Graham number pick

The most typical Graham Number stocks are found in financials and insurance. These Buffett and Munger favorites grow pretty steadily with inflation and trade at fair values of assets and earnings. The most stable of this lot that both Munger and Buffett support as evidenced by both the Daily Journal Company and Berkshire Hathaway 13 F is Bank of America ( BAC ). Here is Bank of America's inputs for the Graham Number:

- Forward EPS 2023 $3.39

- Book value per share $23.37

- Square root of 22.5 X $3.39 X $23.37 = $42.22

- 26% discount to Graham Number

Still 36% off the high, I believe this is one of the best-run banks. They have a high diversity of client base which in my opinion is a better margin of safety than the analysis of low-yielding hold-to-maturity investments that get closer to par with time. Time is the key. When all your depositors are ultra-high net worth, a few buttons pushes could force a bank to liquidate. Banks should not cater to the rich as a business model and should always have the goal of helping the broader community.

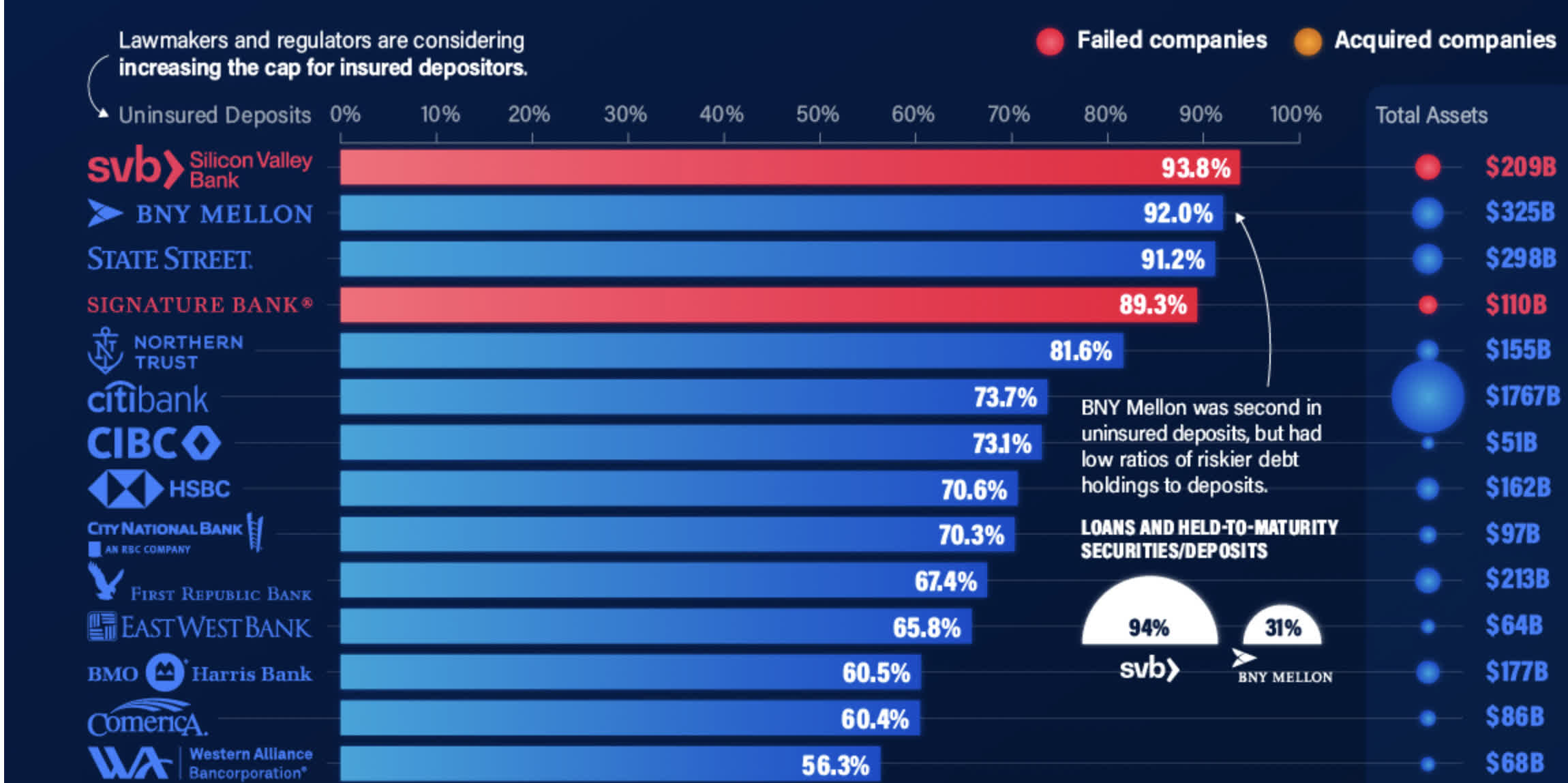

Here is a list of percentage of uninsured deposits by bank:

Top

{kind=link}

Bottom

{kind=link}

As we can see, Bank of America ranks near the bottom in this metric. This means they have a very small amount of accounts over $250,000. They handle a wide array of mortgage and other loan services as well as Zelle payments. Their products are very stick and diversified amongst a diversified client base.

Citigroup ( C ), on the other hand, looks to be the most at risk in this category of SIB banks. One other interesting item is State Street ( STT ) being so high on the list. Besides their banking services, they also run the most widely traded index funds, labeled "Spiders" most famous of which is the SPDR S&P 500 Trust ( SPY ).

Net-net

Net-nets are very hard to find and are almost exclusive to small caps, here is a calculation diagram I put out a while back based on the balance sheet :

my own article

This is an analysis based on the balance sheet. In this assumption we take:

- Current assets or cash and cash equivalents

- Minus total debt and liabilities

- Divide the net amount by shares outstanding.

A good domestic pick given to me by a follower is Network-1 Technologies ( NTIP ). A micro-cap $52 million patent royalty company, they are trading close to net current asset value. Let's observe:

seeking alpha seeking alpha

Here we have the following:

- Cash and short term investments of $46.8 million

- Minus total liabilities of 2.3 million

- Equals $44.5 net cash and cash equivalents

- Divided by 23.8 million shares outstanding equals $1.86 net cash per share.

While the stock has jumped up above $2.23 a share, the volatility makes it one to watch and a good buy below $1.86.

Peter Lynch pick

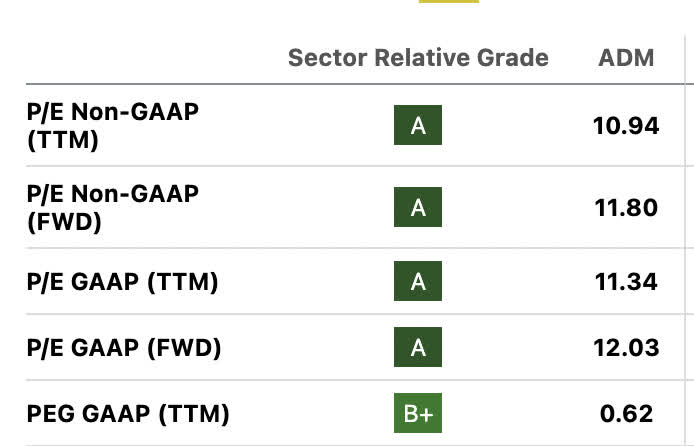

It's getting harder and harder to find some quality PEG ratio picks. Archer-Daniels-Midland ( ADM ) , is one of the better large-cap plays in the market currently tracking this ratio. The multinational food processing and commodities trading company is crushing it.

The Peter Lynch PEG ratio model I like to use is what was laid out in One Up on Wall Street . Find the trailing CAGR percentage, do not go over 25% growth assumptions, and add the dividend to the final multiple. So EPS growth of 10% and a 2% dividend would create a 12 multiple times the current year EPS multiplicand.

{kind=link}

PEG ratio with a dividend kicker for Archer Daniels Midland

- Basic EPS 2018 $3.21/share

- Basic EPS TTM $7.72/share

- Trailing 5 year CAGR of 19.18%

- Plus dividend kicker of 2.12% equals a total multiple of 21.3

- 2023 EPS estimate of $7.3 X 21.3 = $155.49

Archer Daniels is currently trading at $85 a share and seems severely undervalued. It is still 12.63% off its all-time high despite the amazing performance.

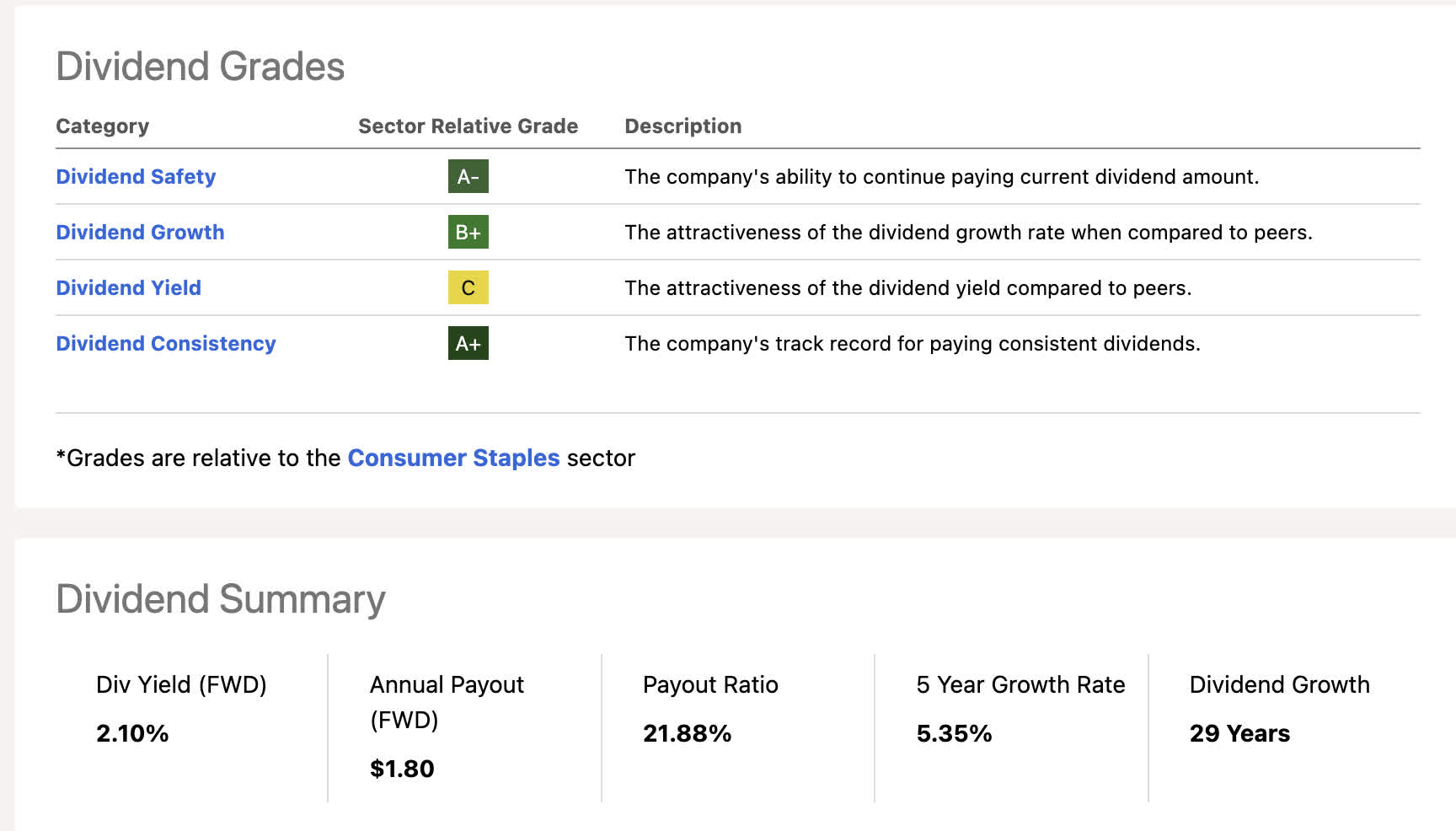

Let's not also forget that Archer Daniels is a dividend aristocrat/king with a solid 5 year growth rate:

{kind=link}

With $6.54 TTM in free cash flow per share, the forward $1.80 dividend is only a payout ratio of free cash flow in the neighborhood of 27%!

Joel Greenblatt pick

Using the "Magic Formula" is one of my favorite ways of looking for broad diversification over a wide variety of stocks. It simply screens for stocks that have a high cumulative score of return on invested capital plus earnings yield. Qualcomm ( QCOM ) remains my favorite in this category .

For the ROIC part of the equation, let's observe the following for Qualcomm:

NOPAT (net operating income after taxes)/total LT + ST borrowings + total equity, aka "invested capital".

- NOPAT = TTM EBIT of 12,692 X (1-11.2%)= 11,270

- Short term debt= 4,433

- Long term debt = 15,486

- Total equity capital= 19,698

- Total invested capital= 39,617

- NOPAT (11,270)/Invested capital (39,617)= 28.4% ROIC

The current earnings yield, the other part of the equation is simply 1/P/E, or the inverse of the P/E ratio. Qualcomm currently has a FWD GAAP P/E of 14.28 which is an earnings yield of 6.9%. Adding 28.4% to 6.9% gets us a score of 35.3 . Anything above 20 is respectable and anything approaching 40 is very cheap.

Warren Buffett pick

Kraft Heinz ( KHC ), a beloved brand and one that Warren Buffet is sticking with through thick and thin. This is still one of my favorite Buffett picks using an "owner earnings" model.

From Hagstrom's book The Warren Buffet Way , net income is first adjusted to add back in depreciation and amortization, which is different than EBITDA, this still accounts for interest and taxes, two very real expenses to a business. Then you subtract capital expenditures. If capex is huge in comparison to D&A, the business will pencil out less valuable, if equal or close to it, then you have an efficiently run business.

Hagstrom also points out that Buffett did not believe in the CAPM required rate of return that incorporates market risk. If the business still has good earnings after adding in D&A and subtracting out capex, then the 10-year treasury risk-free rate is all that was needed.

Owner earnings for Kraft Heinz

All numbers in millions courtesy of Seeking Alpha

- TTM Net Income 3,158

- Plus TTM Depreciation and Amortization 913

- Minus Capex 989

- Equals owner earnings of 3,082

- Discounted at 10 year Treasury Risk Free Rate of 4.07% equals 75,724

- Divided by shares outstanding of 1,228 equals $61.66

Well undervalued, this is a story about debt reduction and fighting inflation. Once those two items get under control, this is a great play and a big spot in my portfolio, top 4-5 depending on the price at any given time.

Interest expense is falling as is long term debt:

Let's also not forget that Berkshire has a spot on the board and has great influence over the company. This is disclosed as a "risk" in Kraft Heinz's annual filings. I see it as more of a "relief" personally. There might also be some debt lifelines available from Berkshire should rolling over maturing debt become too costly. Just my assumption.

Nick Sleep pick

Nick Sleep and Bill Miller are both well known for picking Amazon ( AMZN ) early. Companies that reduce operating income by R&D are favorites when the expense is both large and spawns new creative growth concepts, making R&D both a tax deduction and growth initiative. Meta Platforms ( META ), although having had a large run up, is still my favorite along this model.

Backing out R&D

my own excel

- Meta 5 year adjusted op income CAGR 13.8%

- Meta adjusted op income/share last full year $67,174/2,573 shares outstanding = $26.1 a share adj op income.

- 13.8 multiplier X $26.1 multiplicand = $360.82

Current price $312, 15% upside potential.

While Meta platforms gets closer and closer to a non-buy for me, it's still within range of having moderate upside.

Risks

All these models are ones that I adhere to. Many models are built on past performance but are all analytical of high-quality companies as the basis. With the market being amid another short-term bull, the downside in single names is probably greater than in broad-based ETFs. As an investor that likes to ride the wave and pick up the gold when the tide goes out, I am overweighting my favorite ETFs with new money currently like Vanguard S&P 500 ETF ( VOO ) and Schwab U.S. Dividend Equity ETF™ ( SCHD ). This is inverse to most logic where managers look for more alpha on the upside and more beta on the downside.

The way I see it is, the multi-baggers are on the bottom of the ocean and the ETFs have less risk of downside and guarantee an upwards float in a bull market. Since I'm always buying, this is the way I like to size my bets to reduce downside risks. A bigger skew towards individual buys at the bottom and more indexing at the top.

Conclusion

My mental models lead me to the first question when I see a stock out of favor, firstly, what kind of stock is this? After I answer that question, I harken back to the particular fund manager that had expertise in this segment and apply their philosophy and valuation model.

Always buying your favorite, popular stock is not always the best long-term solution. For long-term investors, create a latticework of mental models and valuation considerations. Finding value and protecting against permanent loss of capital is of the utmost importance. For the AI lovers in the market don't forget:

Addiction can happen to any of us through a subtle process where the bonds of degradation are too light to be felt until they are too strong to be broken- Poor Charlies Almanac quoting Samuel Johnson.

For further details see:

Charlie Munger Latticework Of Mental Models, Picks For August 2023