GTLS - Chart Industries: Climbing Backlog Is Undoing The Debt Disaster

2023-08-29 04:57:04 ET

Summary

- Chart Industries' stock is climbing at a healthy rate back towards previous levels despite concerns about high debt levels from a recent acquisition.

- The company's key debt ratio has crossed an important threshold, easing market concerns and setting the stage for deleveraging faster than planned.

- Business is booming for Chart Industries, with a strong product mix and diversification away from the oil and gas industry.

- The slower pace of orders in the current quarter (compared to first quarter) is not a concern due to the lumpiness of larger orders for this relatively small company.

- The sales synergies are what will justify the Howden acquisition.

Chart Industries (GTLS) recently reported that the backlog climbed about 24% compared to a year earlier and was higher than the first quarter backlog. This is a stock that very much trades based upon the backlog performance. As a result, the stock is climbing back towards previous levels despite the market's concern about high debt levels from the recent acquisition.

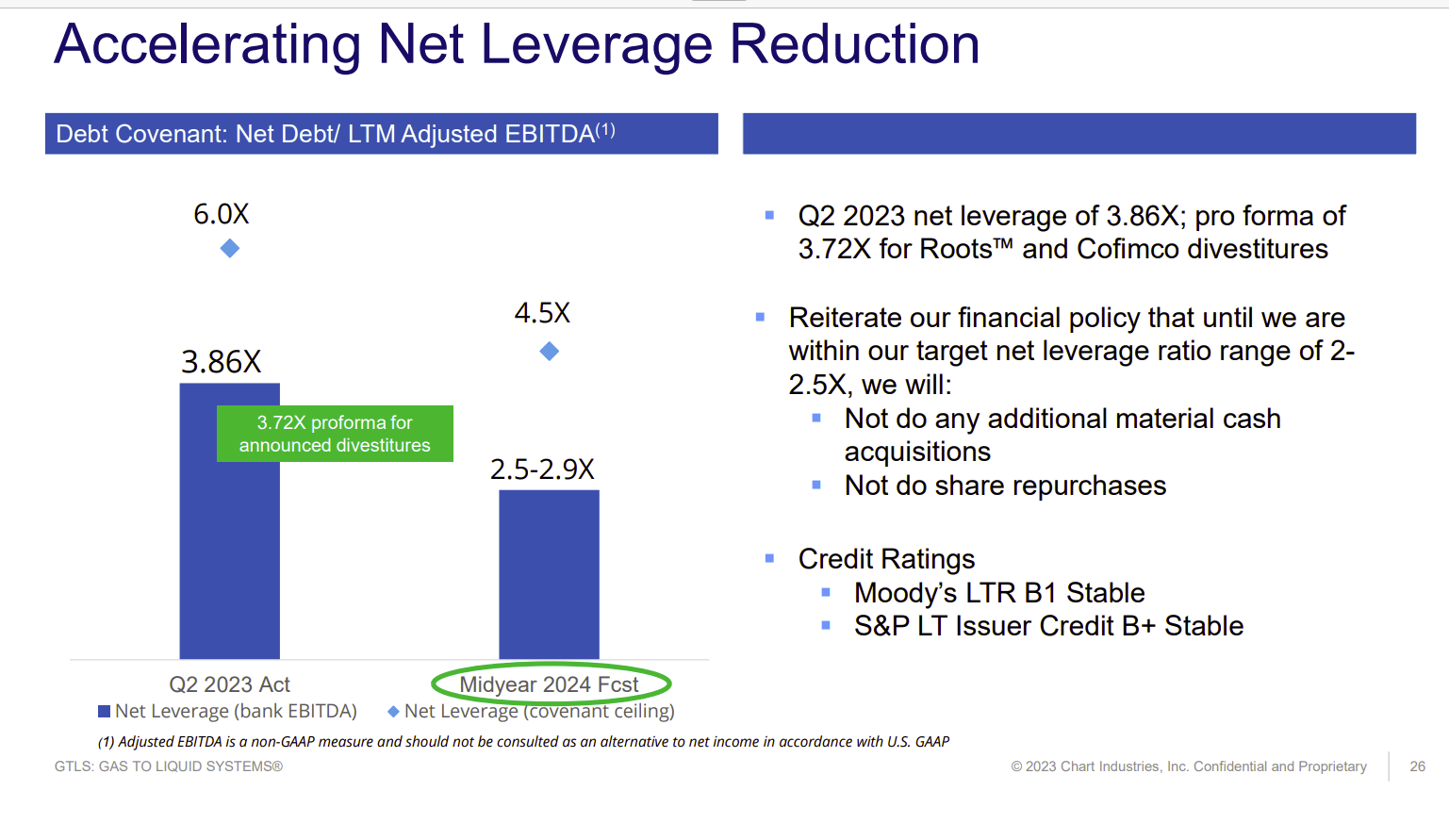

Management also announced that the key debt ratio (that had Mr. Market so nervous) crossed the 4's threshold into the 3's. That appears to be an important accomplishment that is setting the market at ease because now the deleveraging process promised by management is proceeding as planned.

Deleveraging is always far more important at the start when an unexpected curve by the business cycle or the market can derail even some of the best laid plans. But as that leverage ratio gets closer to historical levels, market concerns will continue to fade and the stock price will climb as those concerns fade as well.

Second Quarter Results

Business is still booming.

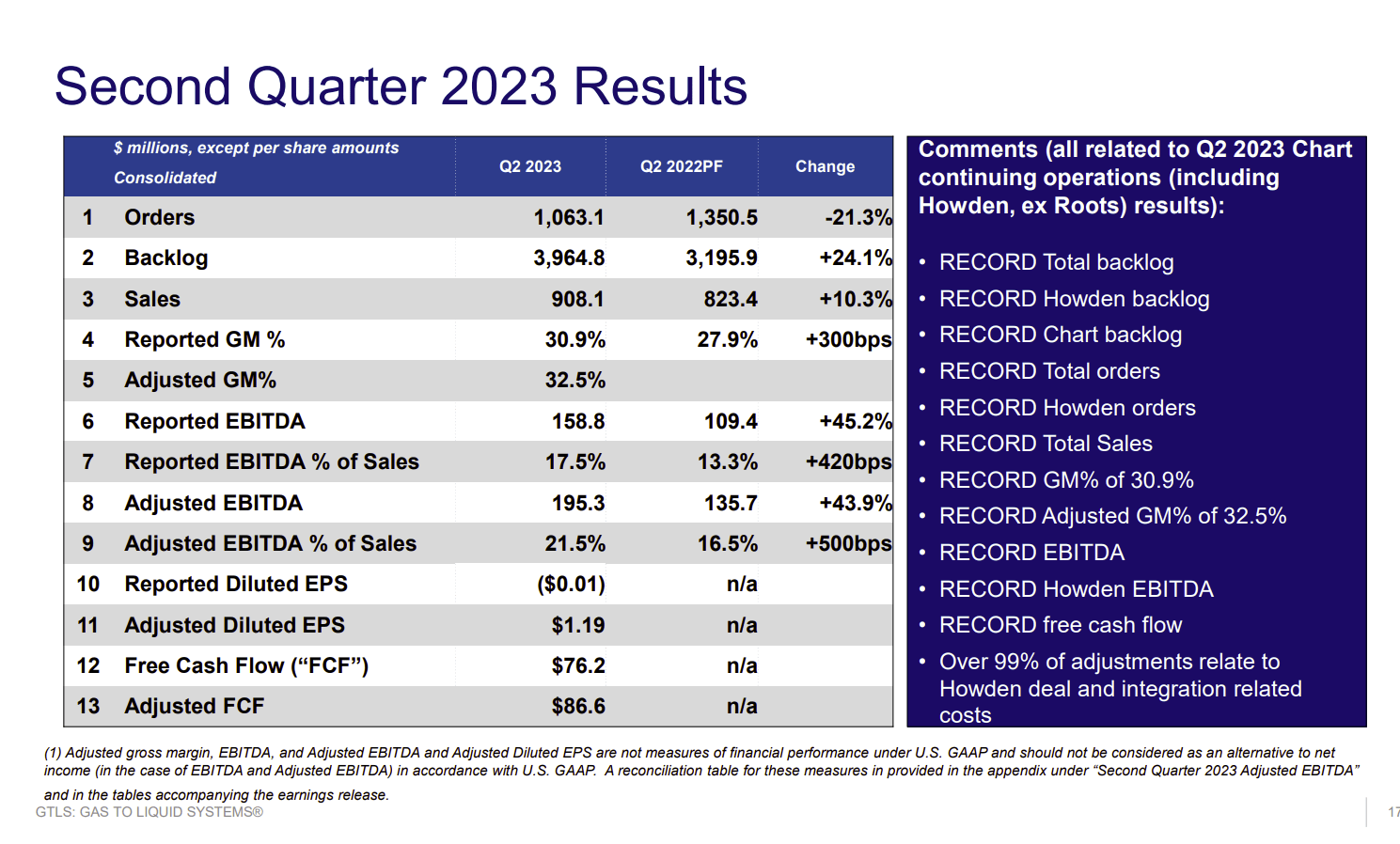

Chart Industries Summary Of Second Quarter 2023, Results (Chart Industries Corporate Presentation Second Quarter 2023)

{kind=link}

About the only concern in the above chart was that the order rate slowed. Order rates tend to be lumpy for the company as it is relatively small player in an area with large projects. Therefore, the backlog comparison is important and often takes precedence over the order rate.

A lower order rate is only concerning if it continues. But management has stated that they are waiting on some significant orders that they expect to get. Timing however is uncertain. It is very likely that those orders will cause a negative comparison in the following year.

It should also be noted that large projects which often generate big orders can distort the order trend. The market (after a lot of years) does seem to realize this and therefore concentrates on the majority of orders while treating the big orders (from large projects) as "extra". It sure took a long time for that to happen though.

Short of the large projects and special items, business appears to be booming. Howden has caused the product mix to have larger margins which the market loves.

The company also continues to diversify away from the oil and gas business that it began with decades ago. That business is still important. So, management is unlikely to abandon the business. But management is adding other businesses that will steady the results to offset the cyclical nature of oil and gas projects.

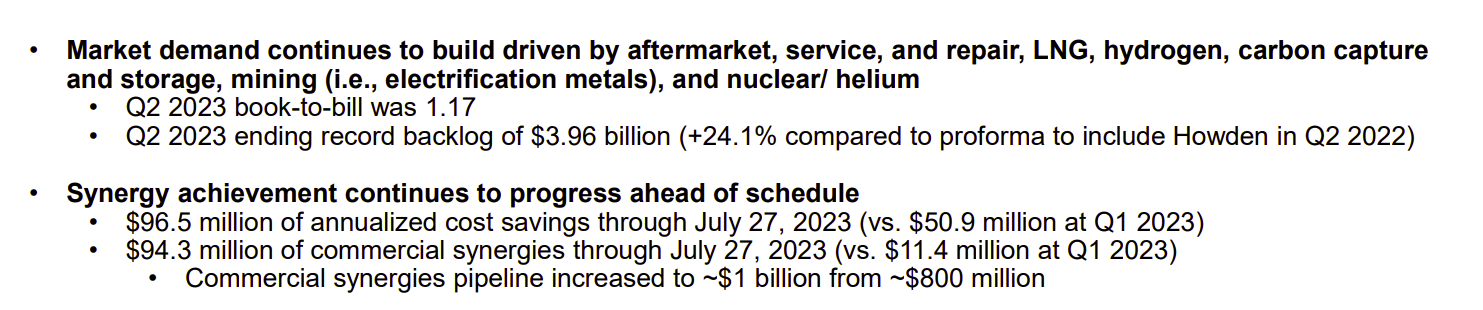

Growth Markets And Synergies

Chart has entered a lot of large fragmented markets where it can compete as a "one stop shop" to take advantage of competitors that do not have as broad a product line.

Chart Industries Sales Advantages Post Howden Acquisition (Chart Industries Second Quarter 2023, Earnings Conference Call Slides)

{kind=link}

The company now has a broad array of services in such hot markets as carbon capture and hydrogen. This product line broadening also aids sales efforts in established markets like oil and gas where the company first began as a business.

Management has long combined sales efforts for the necessary benefits to make acquisitions worthwhile. That is clearly the case here because there is not a lot of manufacturing savings available.

Typically Chart management keeps the incoming management. That management continues business as usual while the combined company works together for sales that neither could compete for as separate entities. Clearly from the slide above, that is where the benefits of the combination lie.

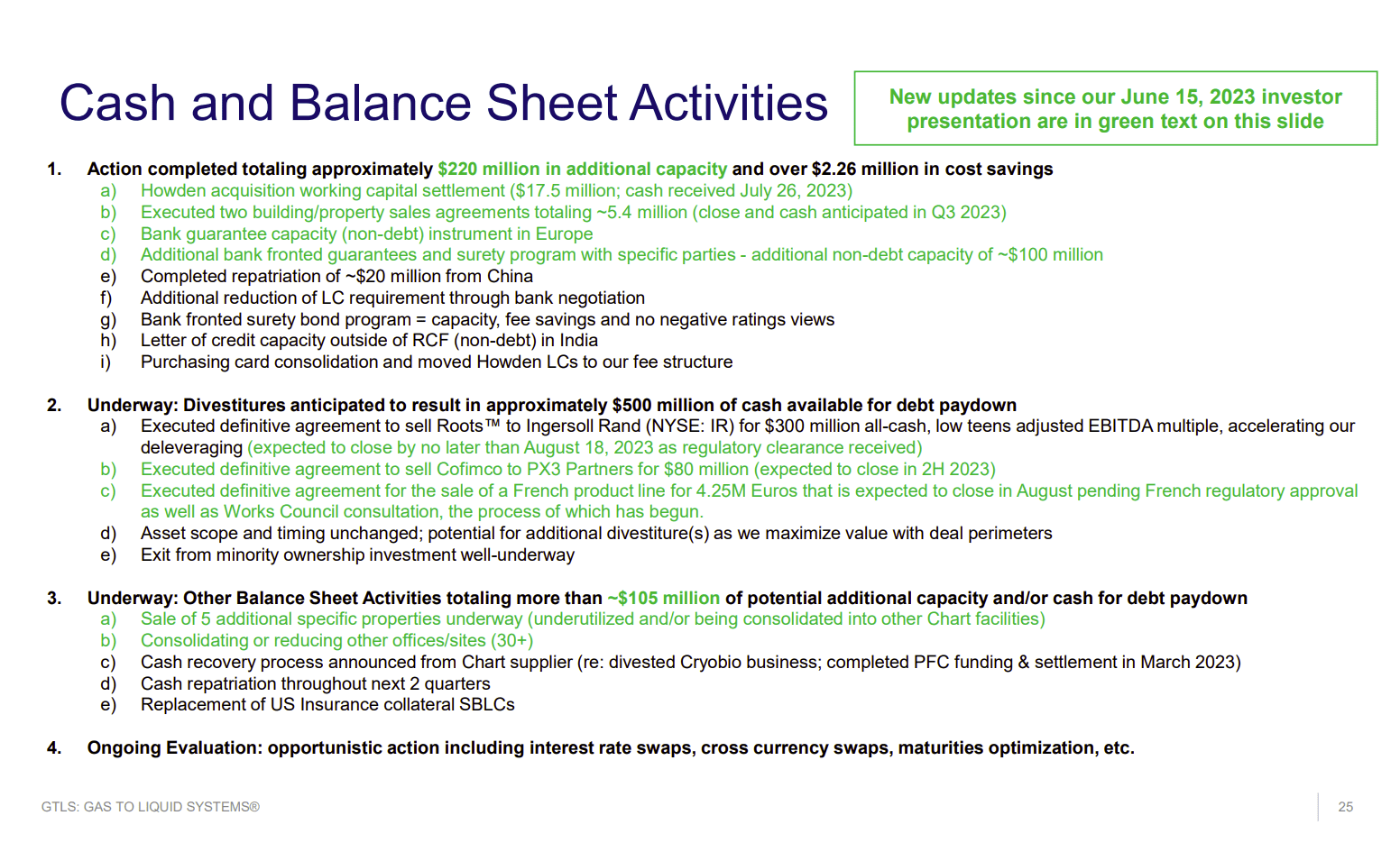

Deleveraging

Chart has a very long and successful history of acquisitions. The market concern this time around was the relatively high leverage that was a departure from the typical company strategy of relatively small acquisitions and a strong balance sheet. So far, management has been successful putting those concerns to rest. But there is clearly more to go.

Chart Industries Summary Of Deleveraging Activities (Chart Industries Second Quarter 2023, Earnings Conference Call Slides)

{kind=link}

Management clearly left themselves some upside leeway from the original guidance. The main focus at the time was raising about $500 million through noncore sales. Now a lot of smaller projects are coming into view that should allow management to exceed their own timelines.

Since the market is laser focused on the leverage ratio, every single tenth of an improvement in that leverage ratio is good news to the market and better for the stock price.

When the original acquisition was announced, the market clearly hated the leverage and the deleveraging guidance (because the stock price quickly collapsed). But now, the market loves that management is beating their own guidance. So, the stock price appears to be recovering.

Chart Industries Deleveraging Guidance (Chart Industries Earnings Conference Call Slides Second Quarter 2023)

{kind=link}

This guidance is probably conservative as well (meaning that there is probably still more acceleration potential). This management is not about to "box themselves into a corner" on something this important.

There are other acceleration tools available in that the company has convertible debt on the balance sheet and convertible preferred stock. Both of these are ahead of the common stock in terms of priority. The conversion of the debt will aid in the deleveraging process. Elimination of the preferred also helps the common but does not count for debt leverage purposes.

The latest 10-Q shows about $258.8 million of convertible notes that are eligible to convert (and mature in November of 2024). They are listed in current liabilities because the holders have the right to convert at any time.

In the past, this company replaced debt with convertible debt and then hedged against the dilution. That might happen again in the future. One of the biggest differences between this acquisition and the small ones of the past, was the company regularly used convertible debt to avoid repaying the debt and retaining the ability to do more deals. This time around there is likely to be a significant amount of debt repaid.

Summary

The Howden acquisition announcement cratered the common stock. This was largely due to a miscalculation by management about the financing part of the announcement.

Now that the market is seeing the execution of the acquisition assimilation, there has been a lot of upside announcements from what now can be clearly seen as very conservative guidance. The result is that the stock price is recovering.

Leading that stock price recovery has to be the growing backlog. This stock has long traded based upon the status of the backlog. So, it is no surprise that positive announcements about the backlog have allowed the stock price to recover a fair amount of the initial losses.

Fast growth has risks in and of itself because management can lose control of costs and quality if they are not careful. Chart protects against this by keeping the original management after the acquisition. There is further protection in that the company is decentralized so that a problem in one division will not necessarily affect other divisions.

Furthermore, most plant sizes are relatively small by industry standards. This company does not combine small plants into large ones that have a lot of the cost and quality control issues. Smaller plants can handle fast growth much more easily than a larger plant as the logistics are much less challenging.

The main market concern was the financial leverage. But this is being dealt with promptly and ahead of schedule. A downturn that would really make the debt levels "hurt" is unlikely in many of the markets the company has entered. This company has a presence in the fast-growing hydrogen and carbon capture markets (and a lot more). This is very different from when the whole business depended upon the very cyclical oil and gas business.

The stock remains a speculative strong buy consideration due to the high financial leverage and fast growth. Offsetting this is a management with a darn good track record so far. Still, investors that cannot withstand considerable stock price volatility need to look elsewhere. The preferred stock may be a consideration for those that are looking for income and do not mind the stock price volatility.

For further details see:

Chart Industries: Climbing Backlog Is Undoing The Debt Disaster