GTLS - Chart Industries: Ghosts Of Issues Past

2023-12-18 07:48:53 ET

Summary

- Howden's acquisition by Chart Industries with debt was unexpected, and the accompanying financing caused a crash in the stock price.

- The market is concerned about the slowing pace of orders, even though it is only for one quarter. The next quarter will likely resume the growth pace.

- The market is also questioning the achieved synergies and margin volatility.

- The company is diversified enough that should the worst happen to the hydrogen market, the outlook for the company is still excellent.

- The hydrogen industry is very likely to qualify for some expected tax credits, despite current worries.

The acquisition of Howden by Chart Industries ( GTLS ) was a surprise to the market. The accompanying financing was a mistake (as I noted in past issues ) that crashed the market price of the stock. Ever since then, the market has been a jittery nervous wreck about the prospects of the stock. The initial cause was the leverage. But once that issue was resolved, the fight began about "green revolution" credits which may have helped slow the blistering pace of order growth. Usually, all of this normally gets resolved by a management that was careful to diversify into a large number of markets so that any setback would be temporary.

The Issues

The Slowing Pace Of Orders

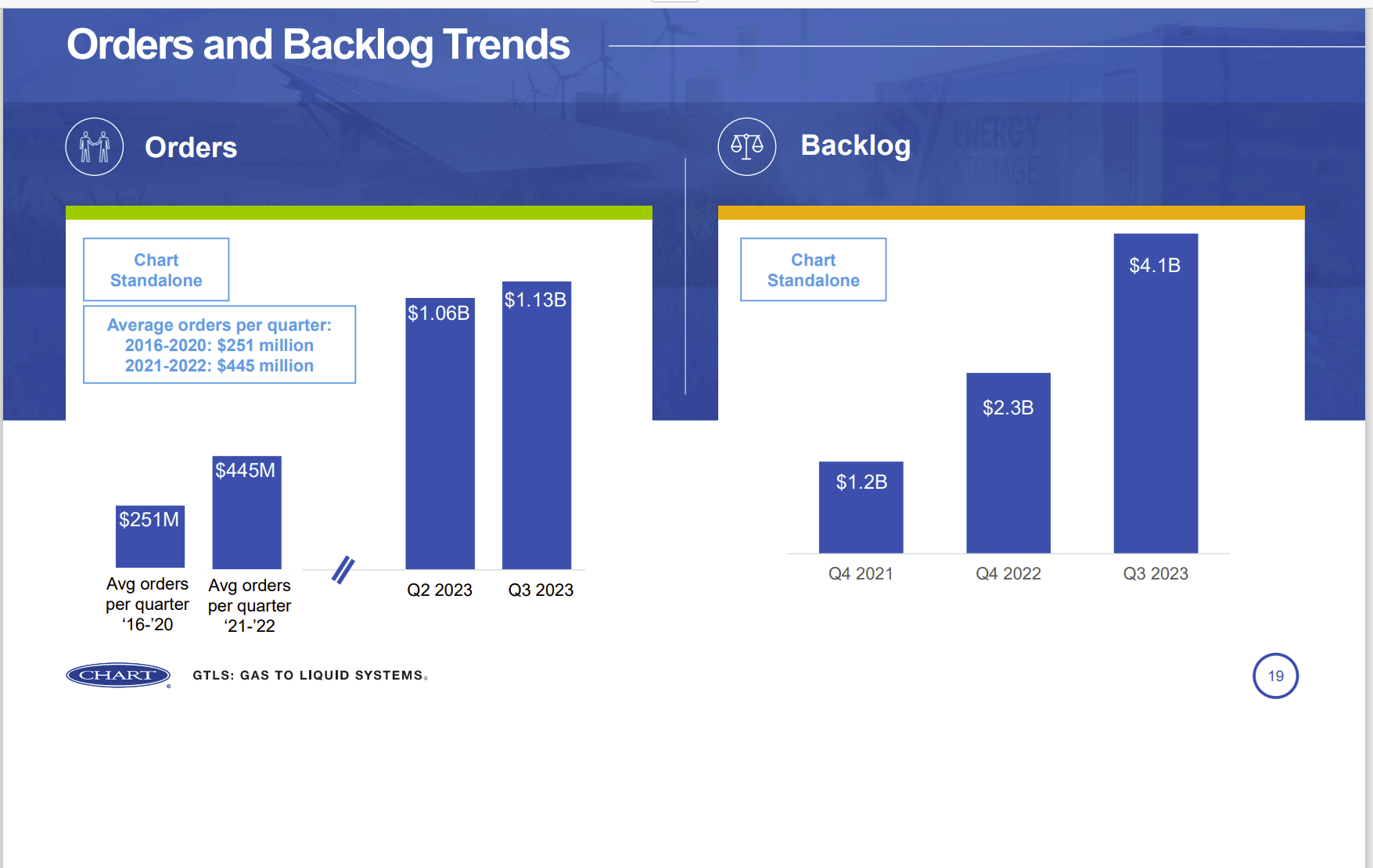

The company is a relatively small player in a large industry. Therefore, large orders are likely to cause a lumpy growth rate as management mentioned in the latest quarter. Orders still grew from the past, but the market was not satisfied by the pace.

Chart Industries Order Backlog Growth (Chart Industries Investor Day Presentation November 28, 2023)

{kind=link}

The first worry was that the pace of order growth had slowed down quarter to quarter. Yet management explained where the large orders were depending upon the comparison chosen. The company can now grow without large orders as shown above, but large orders do affect the rate of order growth in some comparisons. Investors should continue to expect the order growth rate to vary due to large orders.

The market is also wondering about synergies despite management representing the synergies achieved. This company has long had some big quarterly swings because it is a relatively small player that sells to large projects. The product mix can vary widely which causes margin, sales, and backlog swings. The market has long reacted to those swings which makes the stock one of the most volatile that I follow.

Oftentimes, the following quarter shows a return to what the market expects. Investors should expect the fourth quarter to reduce some of the fears introduced by the latest quarterly report. The stock price volatility often represents a trading opportunity for those experienced with this company and the stock price volatility.

A Complicating Factor

In addition to the slow order growth, a congressional fight also put an unfavorable light on the issues confronting the company. The Hydrogen industry was alarmed at the leaked tax credit rules because it could potentially cost jobs or even kill the industry. A significant part of Chart sells products to the rapidly growing industry.

The problem with this is that the environmental crowd wants the source for hydrogen to be water. Meanwhile, the industry has begun by using natural gas as the source for hydrogen because doing so is far cheaper and uses less energy.

Using "clean" energy sources like wind, solar, and similar sources, and then combining that with insisting upon using water as the source makes hydrogen an untenable processing idea at a commercial scale compared to what is happening now. As the industry itself notes, "we will probably get there" at some point in the future. But the hydrogen industry is definitely not there now.

Any industry needs to start somewhere and that somewhere is with natural gas as the sourced gas. Of course, the environmental crowd has issues with the power source to make hydrogen as well. It must have finally dawned on that group that this will not be clean energy at the start for sure.

But killing off the hydrogen industry is not politically feasible as the industry is now too large and too significant. More than likely there will be some sort of reasonable agreement to allow the industry to proceed while keeping in mind the long-term goal. Nonetheless, Mr. Market typically assumes the worst when it comes to the stock price.

Now, even if the worst happens and the industry is lost, Chart is well diversified. A loss like that would set the company back for a quarter or maybe two quarters. But the company services a lot of markets. The mainstay oil and gas industry, for example, is far larger and where the company began. Therefore, it will not be the end of the company by any stretch.

Leverage

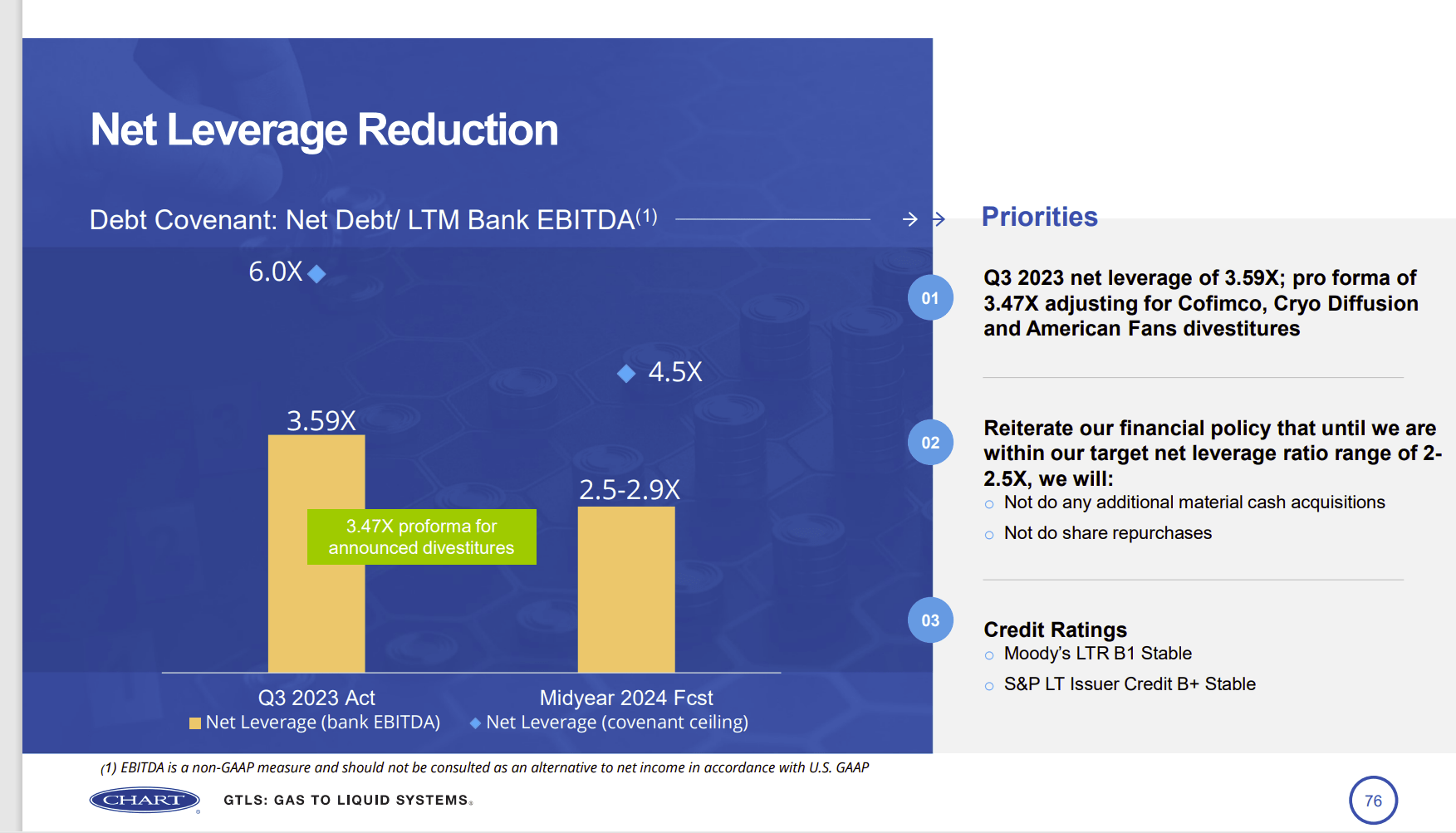

The financial leverage is a worry that the market just cannot get over despite the progress of management. Any other problems like the ones shown above and someone influential will just harp in the newspapers about the leverage despite the progress made.

Chart Industries Leverage Progress And Guidance (Chart Industries Investor Day Presentation November 2023)

{kind=link}

As shown above, this management is way ahead of the limits allowed for leverage. The biggest reason is that any divestments were not part of the deleveraging guidance strategy. Repatriating overseas cash was likewise not a part of the deleveraging strategy. Nonetheless, the company has sold some subsidiaries and brought home cash to get that leverage down as shown above.

The fourth quarter is normally the company's most important quarter. Therefore, more progress is likely to be made in the fourth quarter. Management likewise anticipates a significant growth in earnings to over $6 per share next year. That guidance has been continually reaffirmed the whole fiscal year.

The rapid growth of the backlog, even if that was not the case for one quarter, allows the company to pay down debt while growing EBITDA. The result of this has been a much more rapid decline in debt than the original guidance suggested. Investors should expect that to continue.

Even though Mr. Market just hates financial leverage, the issue is on course to become moot at a rapid pace. Then the stock price is going to respond to the usual rapid growth without the leverage worries.

Non-issue Of Order Delays

In the forty years since I have followed this company, it has yet to lose a material order from the backlog. Instead, what happened in the last quarter was the delay of delivery of some orders which were pushed into the fourth and possibly the first quarter.

Since those orders were large enough to mention to shareholders in the quarterly report, they are likely large enough to raise earnings expectations in those two quarters. That likely means a more favorable than expected quarterly comparison for the next six months after the third quarter.

That means that despite market fears, those orders are still going to be part of sales. It is just the "when" that changed. Large projects that Chart sells to have all kinds of challenges when underway. Therefore, the delay of an order is actually fairly common here.

Of course, so is the reaction of Mr. Market. One would think that after all this time, the market would learn that those orders are still ok.

The other thing that the market did not like was the guidance narrowing for the year on the lower side. But that is usually due to trying to forecast some smaller orders that can come to the backlog and be filled faster. That, likewise, is not a significant problem.

Key Takeaways

Probably the biggest issue for the whole fiscal year continues to be to never again make an acquisition like Howden using all that debt. That acquisition really tanked the stock.

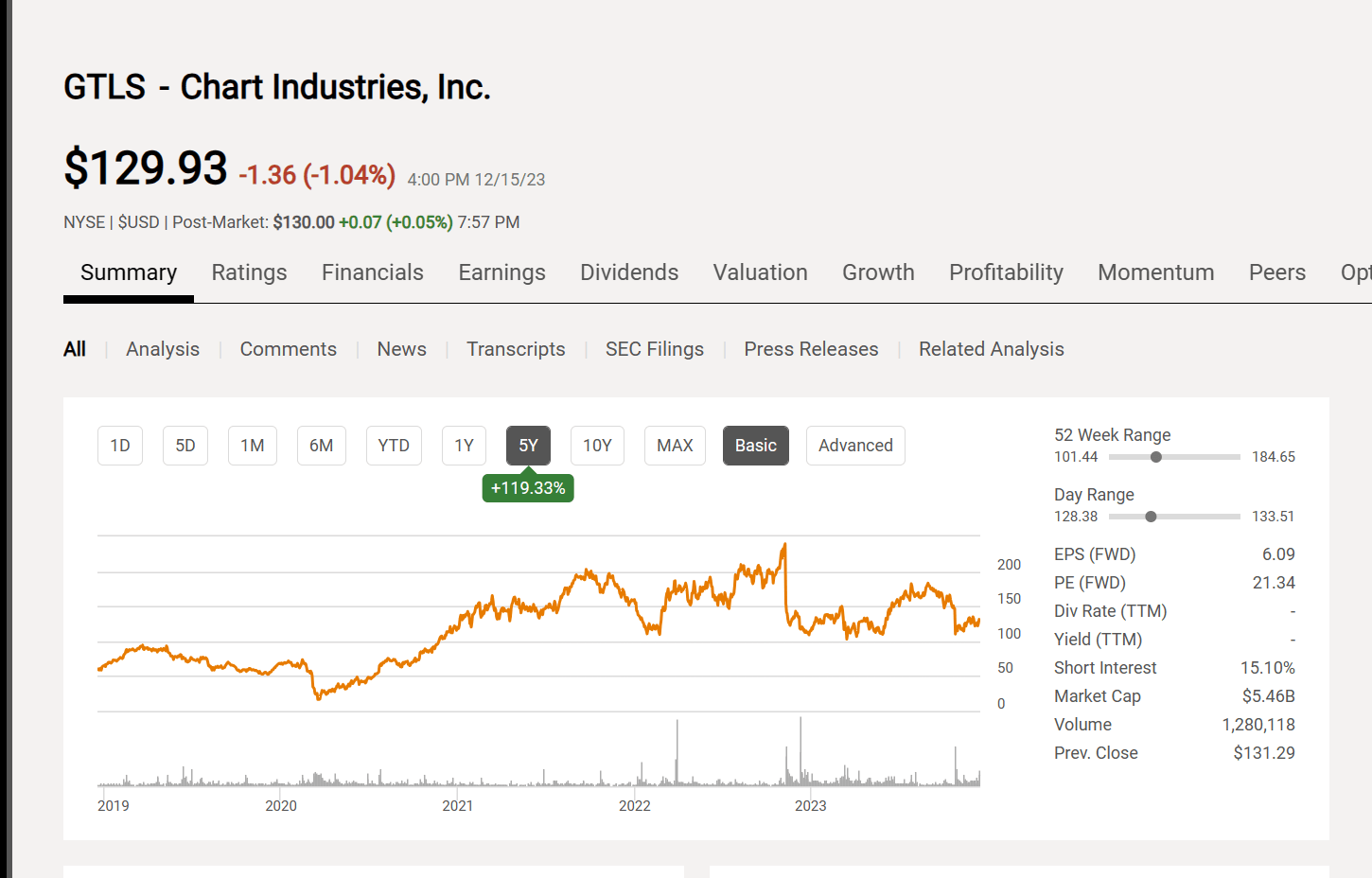

Chart Industries Common Stock Price History And Key Valuation Measures (Seeking Alpha Website December 16, 2023)

{kind=link}

It is very easy to see when the Howden announcement was made as the stock price plummeted from over $200 per share and never recovered. Nonetheless, the acquisition is proceeding as planned even if Mr. Market is still grouchy about the situation.

The latest headlines have introduced a "piling on" situation of more perceived problems that will likely pass quickly. This includes the very important (to the hydrogen industry) battle over tax credits that will likely be suitably resolved (but currently is not yet) as well as the slowed backlog growth. The hydrogen tax credits may have slowed the backlog growth somewhat as well. The industry tends to not spend money during uncertainty. In any event, these issues tend not to last long.

It needs to be considered that management has emphasized the smoothness and reliability of government projects. They also skipped the possibility of the political fight now underway on tax credits that adds to stock price volatility. Mr. Market fears the worst outcome but that rarely happens in politics where compromise is far more likely. The result will probably be something reasonable and viable (as usual in the past) without everyone getting what they wanted.

What needs to be the focus for investors is:

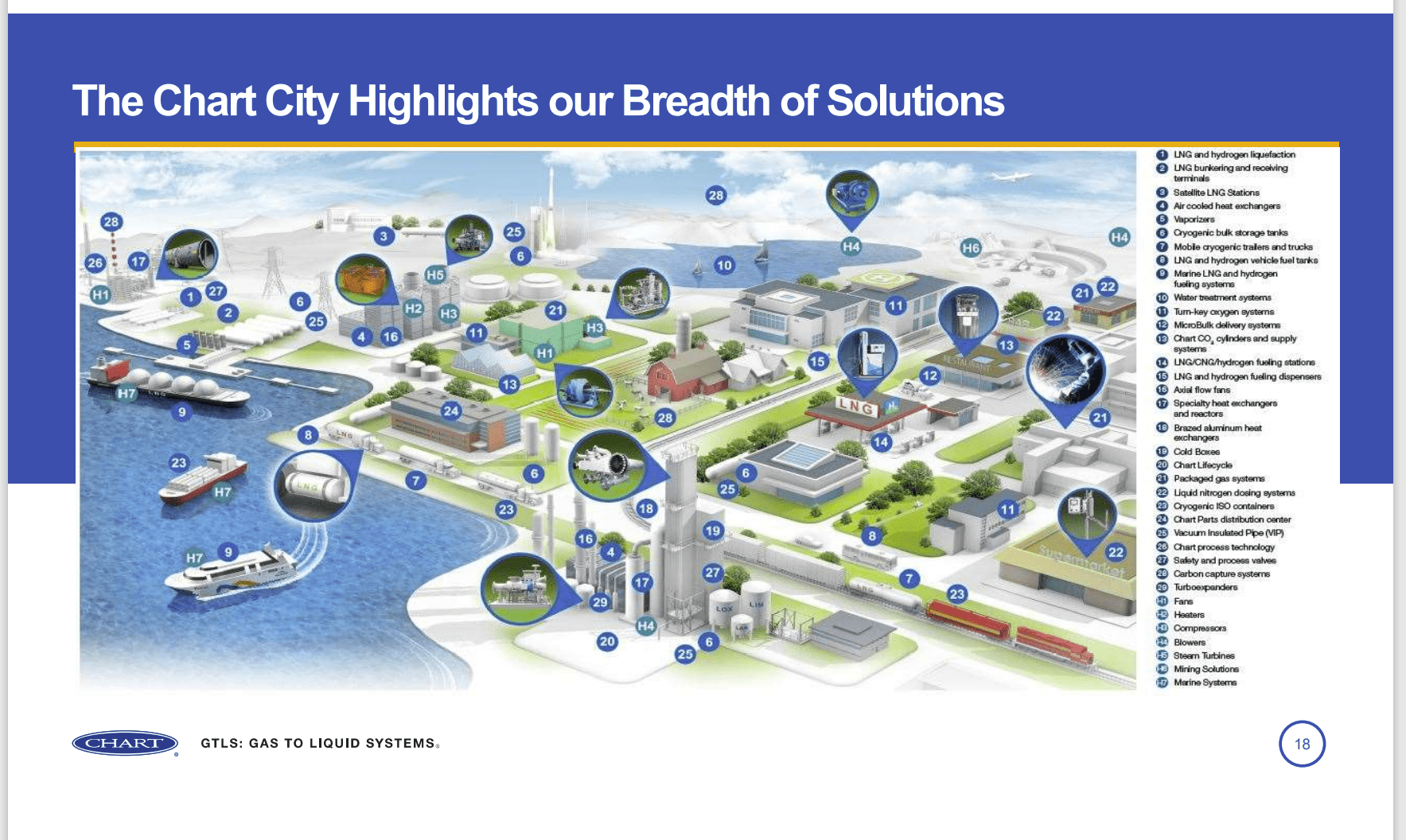

Chart Industries City Of Chart Solutions (Chart Industries Investor Day Presentation November 2023)

{kind=link}

Chart is a diversified company with addressable markets in the tens of billions of dollars (depending upon the market). Many of these markets are rapidly growing.

Like any supplier, management was smart enough to not "bet the company" upon any one outcome. That means that if one market "flops" or disappears, the company has many other markets to sell to as shown above. This company actually produces for several large "hot" markets. The outlook for further rapid growth is excellent despite some scary headlines and some worries about leverage.

The company remains a strong buy because there is nothing facing the company that management cannot handle. The biggest part of the company likely remains oil and gas. But it is not the "begin all" and "end all" that it was when I first began following the company decades ago. It is, however, the most cyclical. A cyclical downturn in oil and gas would likely materially slow growth. But it will not result in a cycle following oil and gas as it has in the past.

The diversification away from dependence upon oil and gas will likely continue. But as the latest news has shown, even the new markets have some risk of neutral to bad news.

This company has the advantage of long lead times. Therefore, the first six months of earnings for fiscal year 2024 are likely fixed (with only the potential for small orders to change the outcome a little). The second half of fiscal year 2024 is likely 70% known already. That means management guidance has a lot more visibility to it than is the case with many industries. Even though the market rarely acts on that visibility (rather than current headlines), investors can. All management has to do is ship out that backlog without cost overruns to make the market happy. That is far less risk than is the case with many investments.

For further details see:

Chart Industries: Ghosts Of Issues Past