CLDT - Chatham Lodging: The Dividend Is Back

Summary

- Chatham Lodging Trust is among the best-positioned hotel REITs for an economic comeback.

- It carries low operating costs and has seen significant improvements in operating fundamentals.

- Management recently reinstated the dividend and the stock appears to be in value territory.

It's important to set the right expectations when buying stocks, especially for income-generating ones like REITs. While this asset class is generally considered to behave like bond proxies, not all property types are the same.

For example, Hotel REITs are generally considered to be most vulnerable to a recession, and because of their cyclical nature, it's better to buy them during a down cycle.

This brings me to Chatham Lodging Trust ( CLDT ), which is among the best-positioned Hotel REITs for an economic comeback. This article highlights why CLDT presents a good long-term, albeit cyclical, opportunity for value investors.

Why CLDT?

Chatham Lodging Trust is a self-managed REIT that's focused on investing in upscale, extended-stay hotels and premium branded, select service hotels. At present, it owns 38 hotels totaling 5,900 rooms in 16 U.S. states and Washington, D.C.

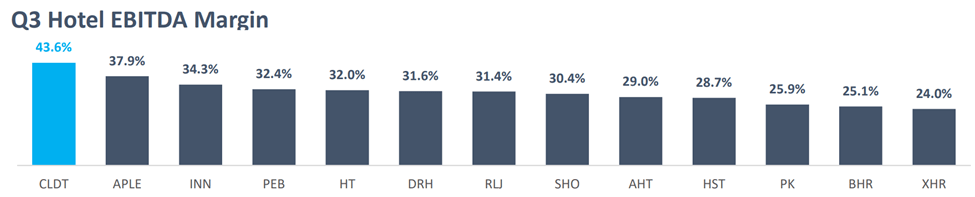

What sets CLDT apart from other hotel REITs is its focus of the aforementioned hotel property types, which come with lower operating costs than full-service hotels, resulting in higher margins and profitability. As shown below, CLDT has the best hotel EBITDA margin, at 43.6%, compared to its peer group.

CLDT Hotel Margin (Investor Presentation)

{kind=link}

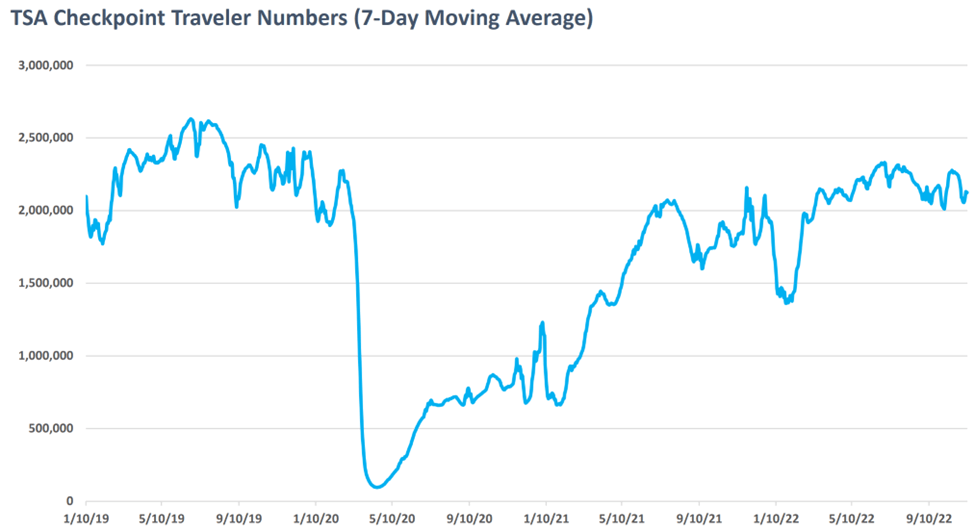

Meanwhile, CLDT's operating results have come a long way over the past year, with portfolio revenue per available room increasing by 34% YoY to $150 in the third quarter, and occupancy grew 10% to 80%. The story is even more pronounced compared to 2020. As shown below, travel has made a near full recovery to 94% pre-COVID times.

TSA Travel Numbers (Investor Presentation)

{kind=link}

The strong results gave a substantial boost to CLDT's AFFO per share, which improved to $0.50 in the latest reported quarter, up from $0.21 in the prior year period. Importantly, this gave management the confidence to resume the dividend at $0.07 per share per quarter. This equates to a 14% payout ratio based on third quarter results, and a 5% payout ratio based on the $1.38 FFO per share that analysts estimate for 2023. As such, I would expect for the dividend to be meaningfully raised in the near term.

Meanwhile, CLDT has made significant debt reductions since 2020, reducing its net debt balance by 42% since March 2020. This debt reduction percentage is second only to Hersha Hospitality Trust ( HT ) over the same timeframe. At present, CLDT carries a safe net debt to enterprise value of 37%.

This frees up substantial capital for management to pursue opportunistic acquisitions. Management expects 2023 to present a favorable deal environment driven by a narrowing bid/ask spread (i.e., falling asking prices to be more in line with buyer bids). This was highlighted during the last conference call :

Touching on external growth. As I stated, we have the capacity and desire to acquire hotels. But as I'm sure you've heard, the transaction market is essentially slower between the significant recent rise in interest rates combined with strong operating results. For the industry, there really is a pretty wide bid ask spread between buyers and sellers.

We are looking at deals, we don't expect to announce anything soon. However, we are certainly looking forward to 2023, because I really do believe that that bid ask spread will narrow, I believe that there will be some debt maturities that owners will have a difficulty dealing with and refinancing in this market. And I also think some of the pressures from the brands should be significant relative to CapEx and deferred CapEx that certainly has occurred over the last few years and during the pandemic.

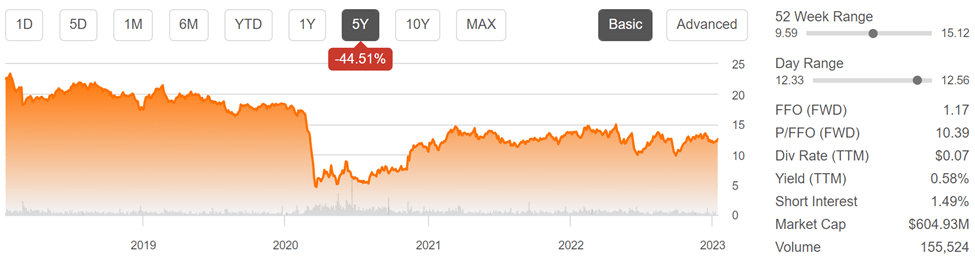

Turning to valuation, CLDT appears to be attractively priced at $12.54 with a forward P/FFO of 10.7. This is considering CLDT's competitive advantages due to lower operating costs and its continued rebound. Analysts expect to see a robust 18% FFO per share growth this year, which would bring the forward P/FFO down to 8.8.

They also have a consensus Buy rating with an average price target of $16.20 , equating to a potentially strong total upside from the current price. As a matter of reference, CLDT continues to trade well below its high-teens to low $20s level in pre-2020 times, as shown below.

{kind=link}

Investor Takeaway

In conclusion, CLDT is an attractive opportunity in the hotel REIT space. Its focus on select-service hotels ensures cost efficiencies and higher margins, and its fundamentals have dramatically improved. Plus, the company's debt reduction efforts have strengthened its financial position, allowing it to pursue opportunistic acquisitions. CLDT currently trades well below its pre-2020 levels and appears undervalued considering its FFO growth potential.

For further details see:

Chatham Lodging: The Dividend Is Back