CLDT - Chatham Lodging Trust: I Will Be Buying The 8.2% Yielding Preferred Shares

2023-11-27 10:30:00 ET

Summary

- Chatham Lodging Trust's financial performance in Q3 was as expected, with a decline due to tech companies cutting expenses.

- The company's adjusted FFO and AFFO calculations show that the preferred dividends are well covered.

- Chatham's balance sheet is healthy, with a low net debt ratio and a cushion of common equity to absorb any shocks.

Introduction

I don’t really like hotel REITs as they are quite exposed to fluctuations in travel patterns, but some of the REITs in that sector have issued preferred shares at pretty interesting terms. In July, I had a closer look at Chatham Lodging Trust ( CLDT ) as I thought its preferred shares were getting increasingly attractive . As it has been a while, I wanted to follow up on that article to see if I should finally initiate a long position in the preferred shares.

The FFO performance was as expected: pretty soft

While the financial results of the hotel REIT in the third quarter showed a pretty substantial decline on a YoY basis (while its H1 performance was stronger than in the first half of last year), this was not entirely unexpected. In his comments, the CEO mentioned the impact of tech companies cutting their expenses which reduced the intern related room demand and negatively impacted the revenue by $8M and the operating profit by approximately $5M.

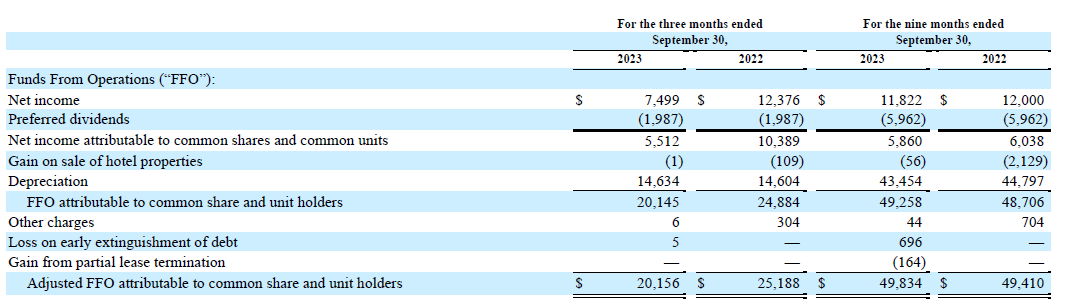

Looking at the actual FFO and AFFO calculation, you see the starting point was the $7.5M net profit generated during the third quarter, of which $5.5M was attributable to the common shares and common units. After adding back the $14.6M in depreciation and amortization , the attributable FFO was $20.1M and the attributable AFFO was $20.2M.

{kind=link}

This means the AFFO was approximately $0.40 per share, and looking at the 9M 2023 results, the adjusted FFO of $49.8M represented $0.99 per share. That’s indeed not bad but keep in mind this calculation of the Adjusted FFO does not take capital expenditures into account. The company spent about $21.4M on capital improvements to the hotel portfolio in the first nine months of the year and is guiding for a $9.2M commitment in Q4 bringing the full-year capex to $30.6M. If I would deduct the $21.4M in capex from the $49.8M in adjusted FFO as reported for 9M 2023, the underlying AFFO post improvement capex was $28.4M or $0.56 per share.

Due to the volatility and uncertainty in the sector, the REIT is not providing any guidance for the final quarter of the year.

Even if I would use the AFFO which includes the capital expenditures, the preferred dividends are very well covered. As the table earlier in this article shows, the $49.8M in adjusted FFO already includes almost $6M in preferred dividend payments. So if we would use the $28.4M in AFFO including capex, the total generated AFFO was approximately $35.4M which means the $5.96M in preferred dividends is still very well covered as the REIT needed approximately 17% of its underlying AFFO to cover its preferred dividend commitments.

So from an operating perspective, I’m quite confident in Chatham’s ability to continue to make the preferred dividends. The next element I always want to check is the balance sheet and access to liquidity. Not in the least because the REIT will have to refinance almost $300M in existing debt in 2024.

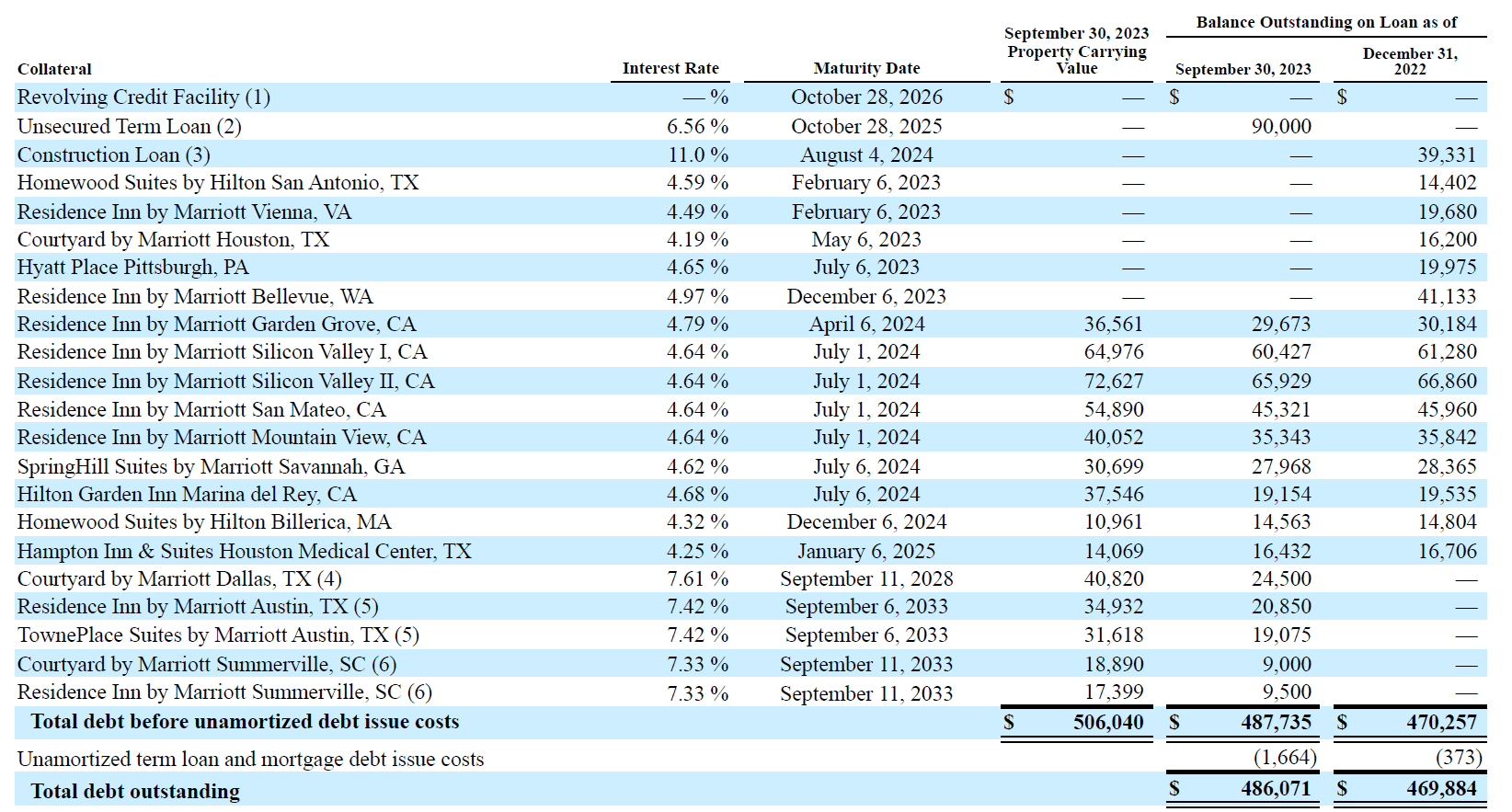

During the third quarter of this year, the REIT took care of $60M in loan repayments and issued $83M in fixed rate debt. The refinancings indicate Chatham had to pay 7.6% for a 5-year loan, and 7.3-7.4% for 10-year loans. That’s pretty high but still manageable from a preferred shareholder perspective. As of the end of September, the average cost of debt was 5.5%. Should this increase to 7% on average, the total amount of interest expenses would increase by $1.9M per quarter. Difficult but still manageable and the preferred dividends would still be very well covered. It would definitely bad news for the common shareholders but I am looking at Chatham from the perspective of a preferred shareholder.

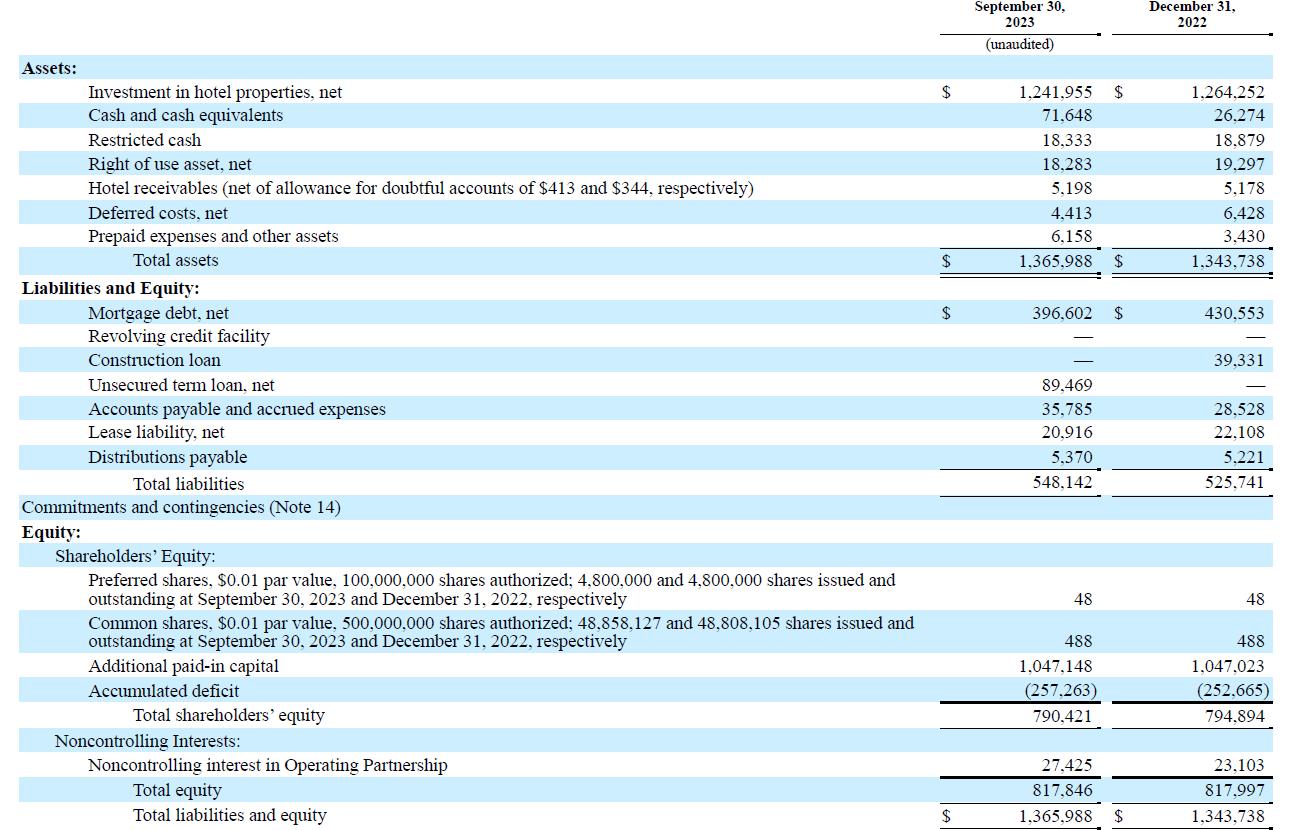

Looking at the balance sheet, there is just under $490M with a net debt of around $420M (excluding the restricted cash). Considering the book value of the hotel assets is $1.24B, the debt ratio is actually pretty healthy. And as you can see below, the balance sheet contains approximately $790M in equity.

{kind=link}

As there are 4.8M preferred shares outstanding, the preferred equity accounts for $120M of that, which means there’s approximately $670M in common equity, which ranks junior to the preferred shares. And that is a very nice cushion to absorb any adverse shocks.

There is one additional interesting element I’d like to highlight: some of the hotel properties have a carrying value that is lower than the remaining mortgage on the property. As you can see below, the Homewood Suites by Billerica has a $14.6M mortgage but only has a book value of $11M while the Hampton Inn & Suites Houston Medical Center has a $16.4M mortgage against a property with a carried value of $14.1M.

{kind=link}

While the carried value may not necessarily represent the market value, it will be interesting to see if Chatham decides to surrender the properties.

The details of the preferred shares

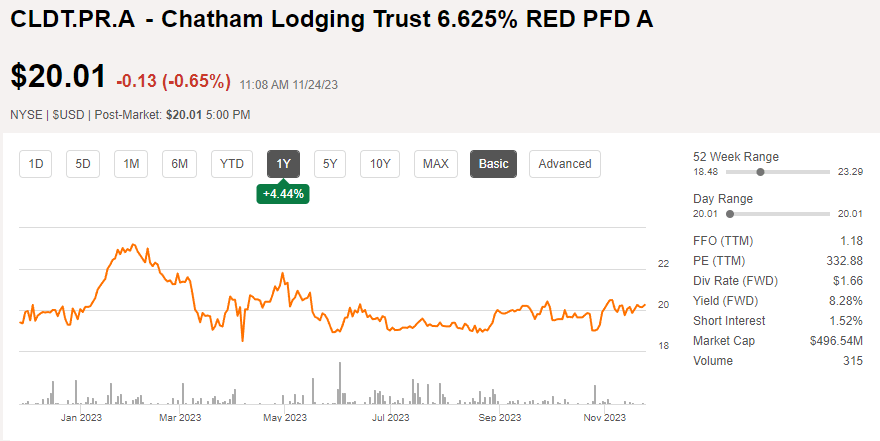

Chatham Lodging Trust only has one series of preferred shares outstanding, the Series A cumulative preferred shares ( CLDT.PR.A ). I like the fact this series of preferred shares offers a cumulative dividend, as it means the REIT will have to cover all unpaid preferred dividends before making any payments on the common units. And perhaps also important: although Chatham suspended making distributions on its common units (until it reinstated a quarterly dividend of $0.07 per share), it continued to make the preferred dividend payments.

{kind=link}

The Series A preferred shares have a fixed annual preferred dividend of $1.65625 per share, which is payable in four equal quarterly installments of $0.414 per share. As the prefs are currently trading at just over $20/share, the current yield is approximately 8.2%.

Investment thesis

As I do believe we have seen peak interest rates and I am looking for some last minute additions to my fixed income portfolio, the preferred shares issued by Chatham Lodging Trust meet my criteria. The preferred dividends are well covered and even in a stress test wherein the average cost of debt increases to 7% (or even 8% for that matter), the preferred dividends remain covered. Meanwhile, with a net debt ratio in the low thirties, Chatham’s balance sheet looks robust as well.

In my previous article I was also considering a long position in the common shares but now I am no longer interested in the common shares at the current share price. However, I will likely buy a starter position in the preferred shares in the next few days.

For further details see:

Chatham Lodging Trust: I Will Be Buying The 8.2% Yielding Preferred Shares