CLDT - Chatham Lodging Trust: Well-Managed REIT But Expensive With A Low Yield

2023-10-03 06:28:22 ET

Summary

- Chatham Lodging Trust is a real estate investment trust specializing in upscale, extended-stay hotels.

- The company has shown resilience and adaptability in industry challenges and has prudent financial management.

- The U.S. hotel, resort, and cruise line industry is undergoing transformation, with CLDT consistently surpassing industry RevPAR growth for five consecutive quarters.

- Based on my valuation analysis, CLDT stock might be slightly overvalued, leading to a neutral rating recommendation.

Chatham Lodging Trust ( CLDT ) has carved a niche in the upscale, extended-stay hotel sector with a diverse portfolio of 39 hotels. The company's financial performance and strategic choices underscore its resilience against industry headwinds and adaptability to market shifts. While CLDT has leveraged debt to fuel its growth and acquisitions, I believe its financial management has been prudent. Based on my valuation model, the company might be slightly overvalued. This perception, combined with its moderate debt-adjusted growth and modest dividend yield, leads me to think there needs to be more potential for significant price movement in either direction. In my view, a neutral rating for CLDT seems appropriate, given these factors.

Business Overview

CLDT is a self-managed real estate investment trust [REIT]A primarily investing in upscale, extended-stay, premium-branded, select-service hotels. It owns 39 hotels, encompassing 5,915 rooms/suites across 16 states and the District of Columbia, operating under 11 brands. Institutions own over half of CLDT, with the largest shareholder being BlackRock, Inc., holding 17%. The next two largest shareholders hold about 12% and 7% of the stock, respectively. The CEO, Jeffrey Fisher, also has 1.9% of the shares. Overall, 8 of the top shareholders hold around 52% of the company's stock. The company, originating as a Maryland real estate investment trust in 2009, has significantly evolved over the years, with its investment focus being primarily on upscale extended-stay and premium-branded select-service hotels. The movement of funds from share offerings to its operating partnership, Chatham Lodging, L.P., adheres to the tax advantages accorded by its REIT status.

Various factors influence its market prospects, including travel trends, economic recovery, and consumer spending habits on accommodations. Through smart asset management and brand collaborations , CLDT finds avenues for growth and stability in its market segment. The analysis of CLDT unveils a well-structured yet complex operational framework. This framework, underscored by its REIT status and Operating Partnership, showcases a significant alignment between strategic asset management and operational flexibility. The intricate interplay of asset ownership, managerial contracts, and brand diversification delineates the operating ethos of CLDT and its strategic foresight in navigating the dynamic hospitality industry landscape.

CLDT investor presentation, August 2023

Since its 2010 IPO, CLDT has leveraged debt and strategic acquisitions to fuel growth. A significant move was its joint ventures, particularly with Colony Capital, Inc. affiliates, which broadened its reach. However, selling its interests in these ventures in 2021 suggests a shift, possibly to concentrate on core operations. This decision might be to reallocate resources or reduce risks from shared control, perhaps based on market insights or financial evaluations. To maintain its REIT status, CLDT can't directly operate its hotels. Instead, it leases them to its TRS Lessees, who partner with third-party managers. This approach removes operational challenges while ensuring revenue, but it also entrusts much control to third parties. As of 2022's end, Island Hospitality Management Inc. managed all CLDT hotels. This model demands strong trust and alignment between CLDT and its partners to achieve brand and financial goals.

CLDT's diverse brand portfolio, including extended-stay hotels like Residence Inn and select-service hotels like Courtyard, both managed by Marriott, showcases a strategy to tap into varied market segments. While treating all hotels as one industry segment streamlines financial reporting, it might miss subtle performance differences among hotel brands. A detailed financial analysis could reveal insights into the performance and potential risks of CLDT's varied brands. This could guide strategic investments and operational adjustments to boost overall performance. I believe CLDT's approach, marked by strategic shifts and a broad hotel brand portfolio, reflects a comprehensive strategy to navigate the hospitality sector's complexities and enhance shareholder value.

CLDT’s Strategic Real Estate Acquisitions

During 1H2023 , CLDT's strategy appears focused on operational efficiency and prudent debt management. The company reduced its mortgage debt and eliminated a $39.3 million construction loan, resulting in a leaner debt profile. In my opinion, this move showcases sound financial management and enhances CLDT's attractiveness to potential investors. While Q2 2023 revenue underscores room revenue as a primary income driver, the stable net income suggests operational adeptness despite a modest rise in operating income. The increase in net cash from operating activities points to a robust operational foundation.

Meanwhile, in my view, the company's decision to allocate cash towards debt reduction is a strategic step to minimize financial risks associated with high debt levels. The negative investing cash flows, mainly from hotel property enhancements, hint at a growth strategy through strategic acquisitions. I believe these investments' effectiveness will be gauged by their impact on future revenue and net income. The slight equity dip between December 2022 and June 2023, coupled with dividend declarations, reflects a balanced approach to shareholder value.

{kind=link}

Recent transactions by CLDT, such as hotel property divestitures, suggest a prudent financial approach in a volatile market. Their October 2022 debt strategy, which transitioned to a $215.0 million unsecured credit facility, a $90.0 million term loan facility, and a $45.0 million credit increment, showcases proactive financial management. However, the upcoming " cash trap " provisions by June 2023 hint at potential financial challenges, warranting closer examination. While their modest hotel investments show dedication to asset enhancement, some property sales might reflect a cautious growth perspective due to market uncertainties. Using derivative instruments, like interest rate cap agreements for the Home2 Woodland Hills hotel loan, indicates a risk-mitigation approach. Yet, terminating certain loan agreements suggests a possible shift in risk management strategy.

Valuation Analysis

The U.S. hotel, resort, and cruise line industry is in a transformative phase, with the market size reaching a notable USD 218.50 billion in 2021. The projected CAGR of 9.3% from 2022 to 2030 underscores the industry's potential, largely driven by the rebound of the U.S. tourism and travel sector after the challenges of 2020. The industry's recovery trajectory is evident, with predictions suggesting a return to pre-pandemic hotel occupancy levels. Florida's hotel occupancy surpassing the national average in 2021 is a testament to this resilience. However, while leisure travel is up, business travel remains subdued. I believe this shift will compel hotels to reorient their services to cater more to leisure travelers, at least in the short term.

Grand View Research

CLDT's recent quarterly performance provides a nuanced glimpse into the prevailing industry trend. The company has consistently surpassed industry RevPAR growth for five straight quarters, which speaks to its resilience and adaptability. This growth, driven by increased occupancy and ADR, suggests a steady recovery path. Notably, even with setbacks like the loss of intern business in crucial tech areas, the company has managed to maintain its revenue momentum . The company's ability to navigate such challenges is a testament to its strategic foresight and operational efficiency.

CLDT's management is optimistic about the upcoming year, expecting a larger intern presence from tech firms. Given the significance of intern business in tech hubs, I believe this bodes well for the company. Financially, CLDT's 5% RevPAR growth has translated into a notable FFO per share of $0.43, outpacing consensus estimates. In my view, this showcases their financial acumen. Operationally, their ability to stabilize hourly wages demonstrates strategic foresight. The net debt-to-LTM EBITDA ratio, at 4.1 times, is commendably lower than pre-pandemic levels. I infer that their Q3 plans for the CMBS market signal a commitment to enduring financial stability.

{kind=link}

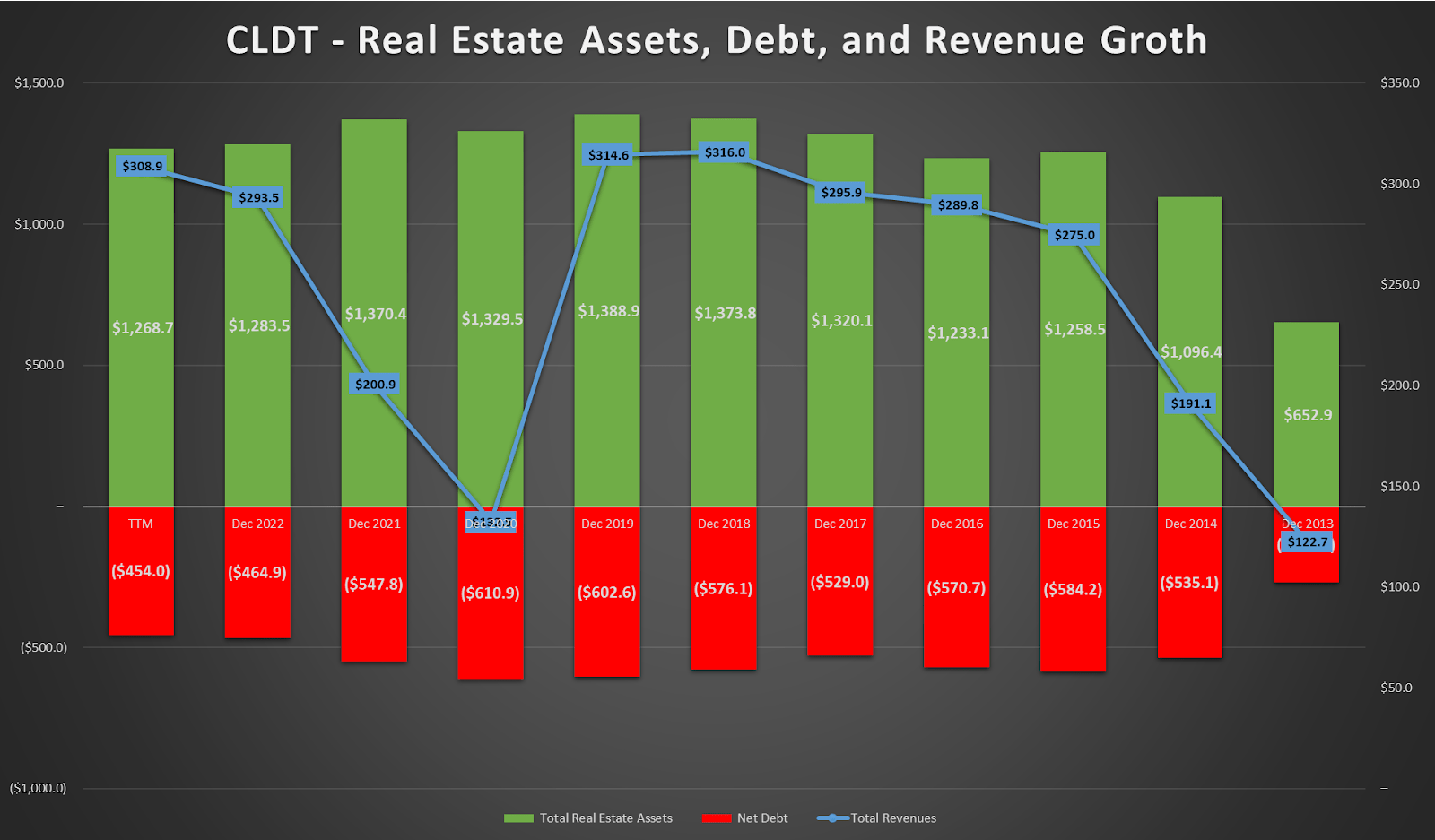

From the data, CLDT's revenue CAGR since 2013 stands at 10.2%. While impressive, seeing its debt grow at a 6.3% CAGR is concerning. I infer that this rising debt can offset the positive revenue trajectory, potentially impacting the company's financial health. Consequently, I've adjusted CLDT’s revenue projections by accounting for its debt growth, leading to a conservative estimate of 2.0% growth post-2027. I believe this is a prudent approach, especially when considering the company's historical trends. Using past EBIT, D&A, and acquisitions, I derived CLDT’s implied FCFs. Considering the company's financial position, these were discounted at a CAPM rate of 13.4%.

Author's elaboration.

Upon analyzing the data, CLDT might be overvalued, indicating a potential decrease of 18.7% from its current value. This suggests a more prudent entry point for investors when CLDT is priced below $7.78 per share. This observation aligns with the current dividend yield of 2.93%, which is relatively low, especially compared to the returns from bonds, including treasury yields. If CLDT were to trade at $7.78, the implied dividend yield would be around 3.60%. While this is still on the lower side, I believe it reflects the company's potential and underlying real estate assets better. Given the current circumstances, there seems to be limited room for significant price movement in either direction for CLDT, leading me to assign a neutral rating.

Conclusion

CLDT has effectively positioned itself in the upscale, extended-stay hotel sector, demonstrating strategic insight and financial prudence. Its ability to navigate industry challenges and adapt to market changes is commendable. While CLDT utilizes debt to drive growth, its financial decisions appear well-considered. I believe, however, that there are signs of potential overvaluation for CLDT. This perspective, coupled with its conservative growth strategy and modest dividend yield, leads me to infer that CLDT may not present an optimal investment opportunity at its current valuation. The resurgence of leisure travel boosts the U.S. hotel sector, but the lag in business travel's return is a concern. I believe the industry's future largely depends on its adaptability and innovation. While CLDT's performance is noteworthy, it must maintain its agility to thrive. Given these factors, I've assigned a neutral rating to CLDT.

For further details see:

Chatham Lodging Trust: Well-Managed REIT, But Expensive With A Low Yield