PLNHF - Cheap Cannabis Stock Planet 13 Has Gotten Even Cheaper

2023-08-20 02:43:58 ET

Summary

- Planet 13 Holdings stock has declined since June and hit an all-time low, down 20.5% in 2023.

- Q2 results showed revenue of $25.8 million, down 9% from last year, but adjusted EBITDA exceeded expectations at $3.0 million.

- Analysts expect revenue to slip 3% in 2023 but increase 41% in 2024.

- The stock is debt-free and cash-rich, and it trades at its tangible book value.

I last wrote about Planet 13 Holdings ( OTCQX:PLNHF ) near the end of June when the stock was trading at $0.58, and I called it a great cannabis investment . Like almost all cannabis stocks, though, it has declined since then. The stock, now $0.485, set an all-time low this past week and is now down 20.5% in 2023, slightly worse than the New Cannabis Ventures Global Cannabis Stock Index, which has dropped 20.2%.

Since I wrote the last piece, the company reported its Q2 . The large decline in price since then might lead one to assume it was a bad quarter, but I don't think that was the case at all. I am a bit underwater in my model portfolios at the investment group that I run, but I used the decline to add to my position, now 12% of my Beat the Global Cannabis Stock Index model portfolio. It's not in the index, so this is a very large holding.

In this follow-up piece, I discuss Q2, the outlook, the valuation and the chart.

Q2 2023

In the last piece, I wrote about Q1, which saw revenue of $24.9 million, in line with analyst expectations but down slightly from a year ago. The adjusted EBITDA of $680K was ahead of expectations.

For Q2, a single analyst was expecting revenue of $25 million with adjusted EBITDA of $1 million, according to Sentieo. The company reported revenue of $25.8 million, down 9% from a year ago. The adjusted EBITDA was above expectations, rising slightly from a year ago to $3.0 million.

Planet 13 ended the quarter with a strong balance sheet that is unique among American cannabis companies, with cash of $40.5 million and debt of less than $1 million. Cash flow from operations improved from Q1, but the company's operations did use $1.5 million during Q2.

The Outlook

Ahead of the Q2 report, the analyst was looking for revenue of $112 million in 2023 and $151 million in 2024. His outlook for adjusted EBITDA was $8 million in 2023 and $20 million in 2024. Now the analyst expects revenue to slip 3% in 2023 to $102 million and to increase 41% in 2024 to $144 million. Adjusted EBITDA is still expected to be $8 million this year and now $18 million next year, a margin of 12.5% in 2024.

So, 2023 is not a year of much progress, but 2024 is expected to be very strong. Many companies are seeing pressure on their adjusted EBITDA margins, but the margin at Planet 13 remains relatively low with room to continue improving. Again, the Florida stores still aren't open yet, and they will contribute to the growth next year, and the Illinois store near the border of Wisconsin is on track to open later this year.

Valuation

I was excited by the valuation two months ago, and it is now even more compelling. The market cap, then $130 million, is now $107 million. Subtracting cash net of debt leaves an enterprise value of $68 million. That's just 3.8X the expected adjusted EBITDA for 2024. This is the metric I use for my year-end targets. For Planet 13, my target multiple is 8X now rather than 10X, which would suggest a stock price of $0.83, which is 71% higher.

My target may not be reached, as cannabis stocks continue to slump. I am very cautious on the sector. One thing, though, that could help is that the stock is trading at 1X tangible book value. Of course, some cash-rich debt free companies in Canada that are licensed producers trade at a discount, so perhaps this protection isn't as strong as I might hope, but Planet 13 stands out compared to other MSOs in this regard. Most MSOs have negative tangible book value. The best-capitalized large MSO, Green Thumb Industries ( OTCQX:GTBIF ), trades at 3X tangible book value.

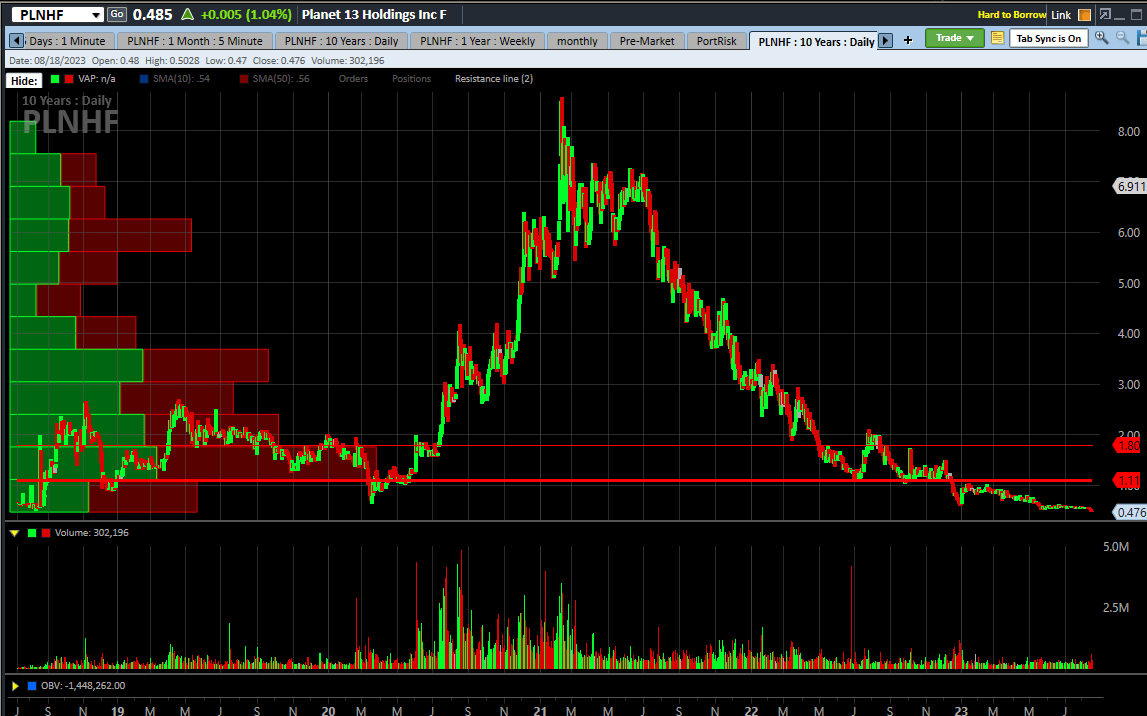

The Chart

The company finally took out its low from late 2018:

{kind=link}

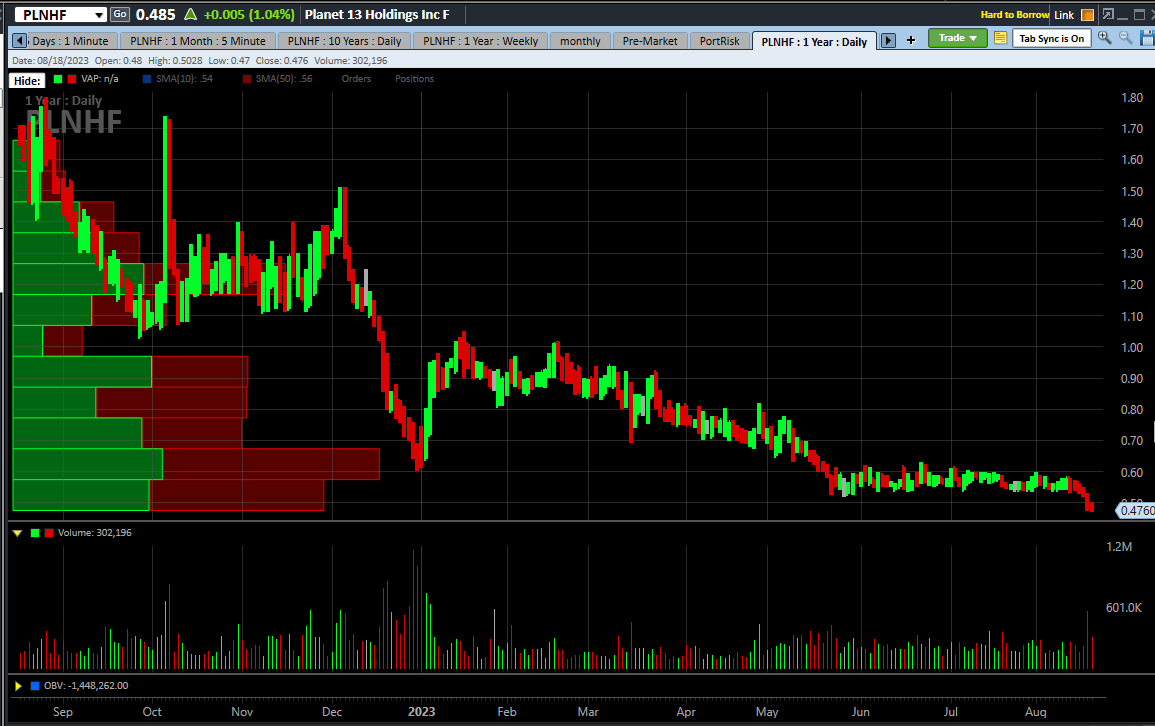

The stock is currently down almost 95% since its peak in early 2021. Looking at the action over the past year, the stock is clearly in a downtrend:

{kind=link}

Conclusion

For a company that has been trading publicly since 2018 with operations in four states, Planet 13 isn't widely followed. Investors used to get overly excited by their strong balance sheet, but these days, when it is the most relevant factor, they no longer seem to care about it as much.

I find the risk quite low given the strong balance sheet, and the growth likely very strong with the recovery in Nevada, its largest market, potentially, perhaps better traction in the tough California market and the addition of revenue from two states, Florida and Illinois. This stock is a big bargain, in my view, and hopefully investors appreciate it more next year as the growth kicks in.

For further details see:

Cheap Cannabis Stock Planet 13 Has Gotten Even Cheaper