CYH - Checking In On Community Health Systems

2023-12-19 13:32:48 ET

Summary

- Community Health Systems, Inc. shares have been performing poorly due to high debt and declining occupancy rates.

- The company owns 76 hospitals and operates over 1,000 sites of care.

- However, Community Health Systems stock has seen some recent insider buying and decent same-store gains.

- A full investment analysis and recommendation follows in the paragraphs below.

Let food be thy medicine and medicine be thy food ."? Hippocrates.

Shares of hospital operator Community Health Systems, Inc. ( CYH ) have been mired in the low single-digits as poor performance impels management to sell properties to pay down debt. The community's net leverage of 8.0 (based on FY23E Adj. EBITDA) doesn't look likely to drop significantly as operating margins are squeezed by inflationary expenses while occupancy declines. However, with decent same-store gains in FY23, and some recent insider buying, the company merited a deeper dive. An analysis follows below.

{kind=link}

Company Overview:

Community Health Systems, Inc. is a Franklin, Tennessee-based provider of healthcare services through its operation of hospitals and sites of care in primarily large non-urban areas. As of September 30, 2023, the company owned or leased 76 hospitals with approximately 12,500 licensed beds and operated over 1,000 sites of care, including physician practices, freestanding emergency departments, urgent care centers, occupational medicine clinics, imaging centers, cancer centers, and ambulatory surgery facilities. Community was formed in 1985 and went public in 2000, raising net proceeds of $245.7 million at $10.74 per share, after giving effect to its spinoff of Quorum Health in 2016. Its stock trades right at three bucks a share, translating to an approximate market cap of $400 million.

The Healthcare and Hospital Industry

The hospitals under the Community's auspices are 76 of 6,129 populating the U.S., according to 2021 data from the American Hospital Association. That number includes 5,157 not-for-profit, investor-owned, state or local government-owned (collectively 'community') facilities, as well as 972 federal, psychiatric, and other (e.g., prison) infirmaries. A total of 31.97 million patients were admitted to community hospitals with 787,987 staffed beds in 2021, for an average of 40.6 patients per bed annually.

As can be gleaned from the prior sentence, Americans are a sick bunch, with national healthcare outlays totaling a gob-smacking $4.3 trillion in 2021, up 2.7% over the pandemic-stained 2020, equaling $13,162 per American citizen. Hospital services - The community's subgroup - comprises the largest portion of healthcare spending, reaching north of $1.3 trillion in 2021, up 4.4% over 2020.

Metrics That Matter

Hospitals' top lines are a function of several factors, including number of beds available, occupancy rates, and outpatient admissions. Occupancy rates are influenced not only by the number of inpatients, but also by the average length of stay. During FY22, the Community had 10,936 beds in service, 434,765 inpatient admissions, 975,737 adjusted (inpatient and outpatient) admissions, and an average stay of 4.7 days, which translated to an occupancy rate of 49.2%. On a same-hospital basis versus FY21, inpatient admissions were up 0.5% and adjusted admissions were up 5.0%, while the average length of stay fell 4% to 4.8 days, causing the occupancy rate to drop from 51.7% in FY21 to 50.0% in FY22. Also on a same-store basis, FY22 net operating revenue was essentially flat (down 0.2%) at $12.0 billion. That top line was provided by third-party payers (47%), Medicare (21%), Medicare Managed Care (16%), Medicaid (15%), and self-pay (1%).

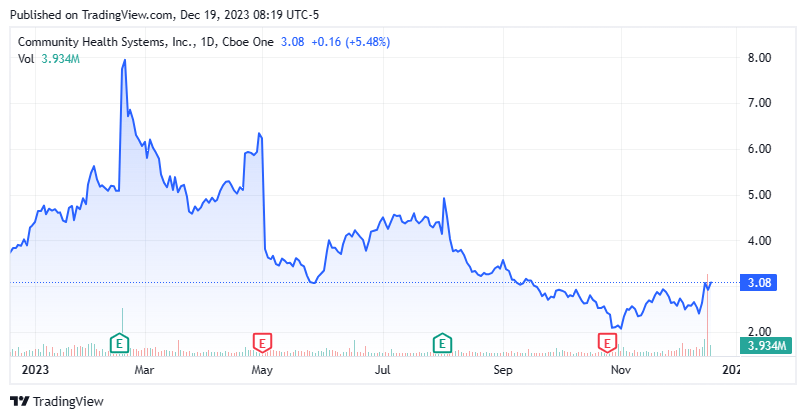

Share Price Performance

After rallying to an all-time high of $53.72 in June 2015 - buoyed by initial (and misplaced) optimism regarding its 2014 buyout of Health Management, which made it the largest for-profit hospital operator at that time, and a favorable Supreme Court ruling on Obamacare - shares of CYH cratered 92% to $4.15 in the subsequent two and a half years as high debt levels and poor operational performance had it seeking "strategic alternatives" that resulted in a survival strategy of selling off hospitals to reduce debt. The facility count dropped from 194 (2015) to 102 (2019) (38 from the spinoff of Quorum), and Community's stock remained primarily below $5 until investors began to speculate on the post-Covid hospital environment in 2H20.

And, for a brief period, the Community's financial performance, aided by occupancy rates above 50% and federal pandemic assistance, somewhat justified the market's optimism, although it continued to sell off hospitals to reduce its still very elevated debt. Adj. EBITDA margin improved from low double digits to over 15% in FY20 and FY21 and Community's stock rallied to $17.04 in June 2021. But higher labor costs, reimbursement challenges, and falling occupancy sent FY22 Adj. EBITDA margins back to the low double digits, with the company generating a FY22 loss of $1.38 per share (non-GAAP) and Adj. EBITDA of $1.47 billion on revenue of $12.2 billion versus a gain of $2.45 per share (non-GAAP) and Adj. EBITDA of $1.97 billion on revenue of $12.4 billion in FY21. As a result, shares of CYH have been stuck in the low-to-mid-single-digits since May 2022 save some brief unfounded optimism regarding an operational turnaround after an outlier 4Q22 financial report in 1Q23.

Q3 2023 Financials & Outlook

And for shareholders, 2023 has been more of the same, punctuated by a dismal Q3 2023 reported on October 25, 2023. The company posted a loss of $0.33 per share (non-GAAP) and Adj. EBITDA of $360 million on net operating revenue of $3.09 billion as compared to a loss of $0.52 per share (non-GAAP) and Adj. EBITDA of $400 million on net operating revenue of $3.03 billion. On a positive note, same-store net operating revenue grew 5.1% year-over-year on a 4.2% increase in adjusted admissions. However, Adj. operating expenses continued to outpace top line growth, up to 89.5% of net operating revenue in Q3 2023 versus 87.2% in the prior year period.

As such, management guided FY23 Adj. EBITDA of $1.475 billion, down slightly from a previous outlook of $1.5 billion, based on range midpoints.

Balance Sheet & Analyst Commentary:

Although its hospital count has more than halved since 2016 (even after not giving effect to the Quorum spinoff), the Community's debt level has only dropped 23% from $15.2 billion to $11.8 billion over the same period as of the end of the third quarter. With cash and equivalents of $91 million, its net leverage on FY23E Adj. EBITDA is a disconcerting 8.0. That said, the company still has $860 million of borrowing capacity on its asset-back facility.

May Company Presentation

On December 11th, the company announced it would raise $750 million in senior secured notes due 2032. Community Health Systems said it intends to offer $750 million aggregate principal amount of senior secured notes due 2032. The company said the issuer intends to use the net proceeds to refinance a portion of its outstanding 8% senior secured notes due 2026.

With its wobbly balance sheet, the Street is split on the Community's prospects. Since the third quarter results were posted, three analyst firms including UBS and Wells Fargo have reissued Hold ratings on the stock. Price targets proffered range from $2.75 to $3.10 a share. Oppenheimer ($6.50 price target), RBC Capital ($6 price target), and Citigroup ($6 price target) have maintained Buy ratings on the stock. On average, they expect the company to lose $.93 a share (non-GAAP) on net operating revenue of $12.46 billion in FY23, followed by a gain of $0.04 a share (non-GAAP) on net operating revenue of $12.68 billion in FY24.

Director Wayne Smith is certainly of the opinion that the low $2 area represents a bottom for Community's stock, buttressed by his one million share purchase at $2.11 on October 31, 2023, upping his direct ownership to 5.1 million shares.

Verdict

Mr. Smith's optimism notwithstanding, Community has a structural flaw: its properties ($9.4 billion before depreciation and amortization) are worth significantly less than its debt ($11.8 billion). The answer to this issue is for it to earn its way out of its obligations, and with some same-store gains in 2023, it would appear that management is shedding the right assets and retaining the growing ones.

However, with its margins very low and getting lower due to rising expenses, the Community is going to have a challenging time accomplishing that end. It may look marginally compelling on an EV/FY23E Adj. EBITDA basis of just over 9 and a microscopic price-to-sales ratio of 0.04, but Adj. EBITDA of $1.475 billion is not going to provide any meaningful dent in its debt, given the $800 million of annual interest payments and close to $500 million in capex. As such, even though shares of Community Health Systems, Inc. could spasm higher in an above-expectations quarter, the long-term recommendation is to avoid it.

When health is absent, wisdom cannot reveal itself, art cannot manifest, strength cannot fight, wealth becomes useless, and intelligence cannot be applied ."? Herophilus.

For further details see:

Checking In On Community Health Systems