CRHCF - Checking In On CRH plc Post The 26 April Trading Update

2023-04-29 05:41:48 ET

Summary

- Operationally things are chugging along swimmingly, and the company has guided to better sales, EBITDA and margins for the first half of the year.

- The company plans to host an extraordinary general meeting on the 8th of June to see shareholder approval for a change in primary listing to the USA from the UK.

- This remains a catalyst for a significant potential rerating as CRH trades at a meaningful discount to US peers.

- Patience is required as there are many moving parts involved but the reward could be substantial.

Checking in on CRH

In a follow up to my article published on 9 March 2023 , CRH plc (CRH) released a trading update on the 26th of April 2023 . Let's jump in and check how things are going.

Operationally things are chugging along quite nicely.

Firstly, in North America which accounts for about 75% of Group EBITDA the report card reads like this.

Materials solutions

This business delivered sales that was 10% ahead of the same period last year. Sub divisionally performance was as follows:

Essential Materials Q1 sales were up 15%, this was bolstered by solid double digit price growth in both aggregates and cement. Q1 is usually a dull quarter for the company as winter weather tends to impact activity levels in certain markets. So this number is quite robust.

Road solutions saw sales jump 7% over the corresponding period once again strong pricing and demand helped boost performance. Special mention was made that backlogs and bidding activity has picked up considerably underpinned by US infrastructure funding at both the federal and state level. This particular point is quite heartening as it clearly means that money is starting to flow into projects as both Infrastructure Investment and Jobs Act ((IIJA)) and the Inflation Reduction Act ((IRA)) commitments begin to see some traction.

Building solutions

Another solid print, up 22% on the corresponding period in 2022. A nice cocktail of strong pricing, resilient demand, and positive contributions from last year's acquisitions were behind the numbers. The strategy of providing a full turnkey solution also picked up momentum. Sub divisionally,

Outdoor Living solutions saw a significant boost to numbers after integrating the acquisition of Barrette Outdoor living. This culminated in a 30% jump on a comparable basis.

Building & Infrastructure solutions grew 9% despite lapping a strong prior year comparison. Also boosted by 2022 acquisitions contributing. Mention was made there that adverse weather did hold things back somewhat.

Secondly looking to Europe which is the remainder of the business results were a little more subdued. With Q1 sales 1% lower than the prior year period. Tough comps and bad weather were the main culprit.

Outdoor living solutions

This was the major drag with sales 6% lower, price increases did offset some of the pain but the extended winter in the region kept things on 'ice' for the most part in first quarter.

Building & Infrastructure solutions

This division delivered a flat performance. My sense was that the slowdown in residential construction in the region (UK in particular) was mostly behind this flattish performance.

The line of sight for the next three months however is strong and overall sales, EBITDA and margins are expected to improve vs the comparable period for the first half of the fiscal year.

Update on the US listing

There has been overwhelming support for the shift in primary listing from the UK to the USA and an extraordinary general meeting has been scheduled for the 8th of June to seek formal approval for this process.

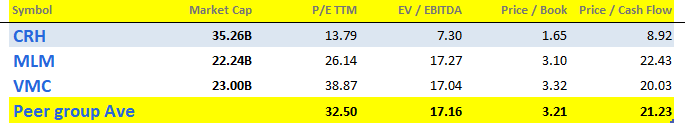

As mentioned in my first article on the company this is a key catalyst for a major potential rerating in the CRH share price. US peers, Vulcan Materials ( VMC ) and Martin Marietta Materials (MLM), continue to trade as significant premiums to CRH and by allowing the market to compare apples with apples the potential upside to CRH is significant. It doesn't matter how you cut it, but CRH is cheap.

CRH peer group valuations (Seeking Alpha)

{kind=link}

On top of this its screening well against these peers on other metrics too

Seeking Alpha screens (Seeking Alpha)

{kind=link}

Valuation

Looking the valuation once again the discount to peers remains compelling.

PE comparison (current price = $48.60)

{kind=link}

EV/EBITDA comparison (current price = $48.60)

EV/EBITDA vs Peers (Analyst)

DCF valuation (current price = $48.60)

My assumptions laid out in the first note are unchanged. That is 12% growth for the next 5 years (vs 14% last year) supported by IIJA, IRA, and the equivalent program in Europe ( NextGenerationEU recovery funding program ). Dropping down to 0.5% thereafter. The discount rate is the long-term average market return of the S&P500 which also happens to be their weighted average cost of capital.

DCF valuation (Analyst)

As per my last note I suggested that it may be of course that the CRH is 'cheap' BUT that the peer group is also 'expensive'. To compensate for that we'll push a discount of 20% on both the PE and EV/EBITDA valuation relative to peers on the basis that if peers are indeed expensive, they may fall by 20% at which point what would the value vs peers look like then. Using the DCF which is company specific we then get the following average value for the company.

Average of the various valuations (Analyst)

There we have it. With an 'average' target price of $83.14 vs a current price of $48.60 it sure looks like there is a lot of potential value unlock to come when the company moves its listing to the USA from the UK.

What's the catch?

You'd be right to ask well if it's so cheap why hasn't the market responded yet? I'd retort with the following.

Firstly, there are very few US analysts covering CRH, its viewed as a European business and as such is covered in that region more extensively. I'd expect that to slowly change over time.

Secondly CRH is part of the mega cap FTSE100 index in the UK and the Eurostoxx50 in Europe. Leaving the Euro and UK arena would require substantial rejigging of portfolios by both tracker funds and long only managers. This could result in chunky outflows and selling pressure which could drive the price lower. The market is smart and has likely picked up on this already.

Lastly inclusions into the S&P500 and the Russell will take some time as liquidity hurdles need to be measured and met before they can be included. This time lag before US trackers are able to buy means that selling from the Euro/UK funds will not be absorbed smoothly.

I'd suggest that markets are aware of this and that smart bankers are already figuring out ways to 'resolve' this problem for both sides of the equation.

Ultimately though it does mean that some patience is required. Personally, I've acquired a position that I plan to add to as I see what may look like some 'odd' or 'irregular' share price moves.

Risks

Since my last article on CRH dated 9 March 2023 which you can find here , the risks haven't changed materially. Please see the note for more detail.

Concisely put however they include the cyclicity of the industry, recession risk, cost control, inflation risks, interest rate risk, leverage, and risks that the integration of any acquisitions made don't happen as efficiently as expected.

One of the big benefits of investing in the company now is its valuation relative to US peers. If the listing is moved to the US as expected there is of course no guarantee that the rerating will occur.

Conclusion

The trading update released on the 26th of April shows that the company is chugging along quite nicely. The discount to peers remains large and on both a relative and absolute basis the business seems quite undervalued for what the IRA, IIJA and euro equivalent promise to bring over the next decade or more.

Management is using the share price disconnect to buy back shares with the company on track to buy back $1bn worth of shares in the first half of the year. This is part of a total buyback program worth $3bn. Dividends are flowing too and the current yield of 3% is attractive and growing.

Patience is required and dripping the investment in over time is a prudent strategy but the upside potential here is certainly worth it.

I maintain my strong buy rating on CRH.

For further details see:

Checking In On CRH plc Post The 26 April Trading Update