GPRE - Checking On Alto Ingredients After Brutal 2022

2023-04-13 02:09:42 ET

Summary

- After I pitched Alto Ingredients in 2021, shares subsequently have declined ~80%.

- The story is largely unchanged, with future capital expenditures expected to help the business diversify away from fuel ethanol.

- I underestimated the depth of pain shareholders could experience in 2022, which raised liquidity fears progressively higher.

- I provide key drivers to watch as Alto continues to pursue their transformation.

In 2021, I wrote two pieces highlighting the investment opportunity at Alto Ingredients ( ALTO ), with the stock trading around $5/share. I argued the company had significant value-add projects in the works that were under-appreciated by the market. I believed the projects could lead to $100m of sustainable EBITDA, disparate from the manic fluctuations of the fuel ethanol market. With the stock down over 70% in two years, and FY22 negative adjusted EBITDA (even including a one-time USDA grant), this is among my worst calls on Seeking Alpha. Today, let’s review the story and discuss if hope remains for deeply underwater shareholders.

The Results

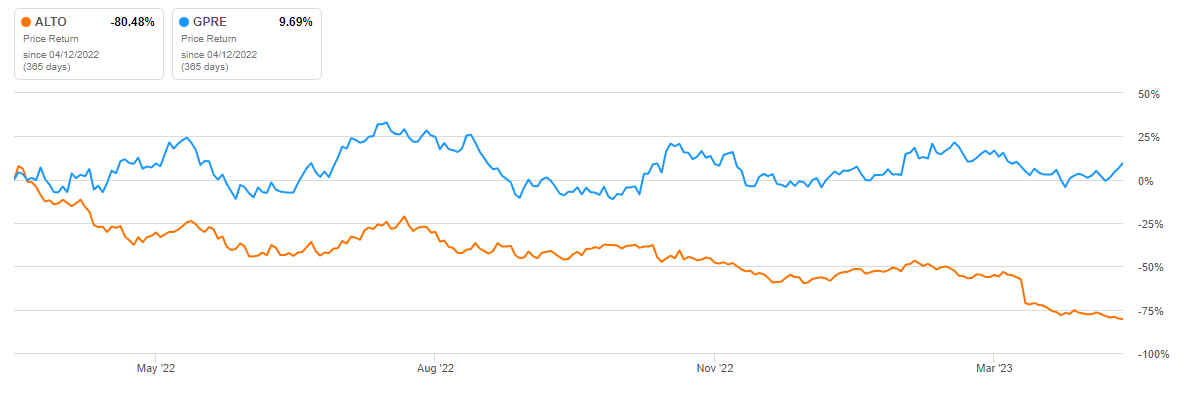

To support my thesis, I highlighted ALTO’s valuation relative to peer Green Plains ( GPRE ), and concluded ALTO appeared cheap by comparison (GPRE was attempting a similar pivot from fuel ethanol) . For FY21 and FY22 combined, ALTO earned positive net income, versus GPRE losing almost $200m, showing ALTO managed through tough industry crush margins respectably. On a cash flow basis, GPRE generated $70m from operations in the past two years, while spending a whopping $400m on CapEx for growth. ALTO produced $33m cash from operations and spent $50m on CapEx.

Shareholders felt otherwise, as you can see for the past year:

{kind=link}

Even though GPRE is outpacing ALTO on their corn oil and protein initiatives, the market response seems overdone. A bull case exists for GPRE, and it was certainly the better performing stock over the past two years.

ALTO has announced numerous capital initiatives, most of which have yet to begin:

{kind=link}

On the last ALTO earnings call , I asked for clarity on which projects have been funded so far with their new $120m credit line from Orion: Specialty upgrades, the corn oil and protein at Magic Valley, and larger corn storage. On the other hand, Carbon Capture, Cogeneration, RNG, Yeast, and corn oil/protein at other campuses all remain to be funded. How?

-

“As of December 31, 2022, we had $36.5 million in cash and cash equivalents and $57.9 million available for borrowing under Kinergy’s operating line of credit. In addition, we have $40.0 million available for capital improvement projects under our term loan." (Alto 10-K)

So, liquidity is just shy of $140m (plus a $25m option to expand the Orion loan), and total capital requirements will be ~$100m for carbon capture, ~$10m each for remaining protein and corn oil at each location (3 of each), before getting to the RNG (est. $10m), Yeast (est. $50m), or Cogeneration (est. $25m). I’m assuming a ~2 year payback period on each given they are all being considered with other ~2 year payback programs. The capital is not needed tomorrow, but expecting ALTO to fund these initiatives requires optimistic assumptions regarding the fuel ethanol market.

What I Got Wrong

In my last article, my assumptions for ALTO’s earnings power were too optimistic, namely $0.66-1.00 of Specialty revenue per gallon and 40-42% of coproduct revenue as a percentage of corn cost.

-

Specialty : Actual corn cost of $7.77/bushel and blended sale price of $2.64/gallon shows ALTO ended up with a negative crush margin in 2022 [7.77/2.8 - 2.64 = (0.14)] including Specialty gallons. The company discloses their average sale price per gallon produced in Pekin was $2.59 in 2022, where all their Specialty is manufactured. Of the 201.1 gallons produced at Pekin, 92.5m were Specialty. The average sale price for ethanol in Illinois for 2022 was $2.49/gallon . Solving for X in 92.5(x)+(201.1-92.5)(2.49) = 2.59*201.1 implies ALTO got an average price for their Specialty of $2.71, 22 cents above fuel grade. Assuming $0.66-$1.00 resulted in overestimating EBITDA by $44-78m, even before my overly optimistic production estimate of 110m gallons versus the 92.5m actual.

-

Coproduct : ALTO’s coproduct revenue was almost unchanged from 2021 as a % of corn cost (33.8%) despite my expectation this would improve. ALTO’s average sale prices per ton were $265.26 at Pekin and $114.78 at their Western campuses. These were up 23% and 34% over 2021, but essentially flat once accounting for the change in corn price. Actual realization of 33.8% for FY22 reduced EBITDA by about $50m versus my expectations.

These two drivers accounted for most of the gap between the “pro-forma 2022” I compiled and actual FY22 results. It’s also important to note that ALTO received $22.7m from the USDA in 2022 and left this amount in their adjusted EBITDA. So, the full year $9.8m EBITDA loss was actually over $30m, absent this one-time grant. The remaining difference is primarily the negative crush margins realized by ALTO in 2022.

For coproducts, GPRE sold 2.28m tons of grains and 282m lbs of corn oil in 2022. So “essential ingredient” revenue was $717m from 2.42m tons, which is $296/ton and significantly ahead of the prices ALTO realized. This appears to be driven by GPRE’s calculation of “equivalent dried tons,” making their result incomparable to ALTO’s by under-reporting actual tons sold via adjusting moisture weight. GPRE averaged $234/ton in FY21, so FY22 showed a 26% improvement like ALTO.

For now, it appears essential ingredient realization remains a function of external factors – corn and soybean prices, transportation, renewable diesel demand for corn oil, seasonality, etc. ALTO and GPRE will continue working to enter the high-end protein market, which will provide more attractive fixed price contracts with less sensitive to commodity inputs. Decoupling from inputs will lead to higher valuation multiples and stabilized earnings.

FY23 Outlook

Crush margins remained poor in Q1-23, and ALTO is poised to post a loss for the quarter. There were some sequential improvements and margins finally flipped positive in March. Management indicated Specialty pricing would be “better” in 2023 on the Q4 call, but I couldn’t imagine it getting “worse” given FY22’s thin margins over fuel. Magic Valley is idled until protein upgrades are completed in Q2-23, so overall production volumes are likely down versus 2022. The protein and corn oil benefits should add approximately $0.20/gallon to EBITDA at Magic Valley, though perhaps not immediately as sales contracts for protein may take time.

For now, I’m going to illustrate FY23 earnings (using rough market prices) when ALTO produces about 180m fuel gallons (lower due to Magic Valley idling), 100m Specialty gallons, $200m of third-party sales (1.5% margin), and attains 35% for essential ingredient sales. I will assume $0.30 cents margin for Specialty gallons. Using rough market prices of $6.75 average corn cost and $2.45 average fuel prices we are assuming crush margins are slightly above breakeven:

-

$441m fuel revenue

-

$275m Specialty revenue

-

$200m third party

-

$236m essential ingredient revenue

-

$1,152m total revenue

-

($197m) third party expense

-

($675m) cost of corn

-

($35m) SG&A

-

($10m) interest expense

-

($255m) labor, natural gas, fixed costs, -15% vs FY22 for Magic Valley idle and lower natural gas prices

-

$1,172 total expenses

-

Net $20m loss ($0.27/share)

-

Add back $10m interest expense

-

Add back $25m D&A

-

Add back $2m taxes

-

$17m EBITDA

This isn’t terribly exciting, but these numbers will vary dramatically as commodity prices swing during 2023. Natural gas is normally ~10% of total COGs by my math, so if prices stay low in 2022, ALTO may receive greater benefit. You can adjust the numbers above to see the impacts of improved crush margin, decreases in $/ton of essential ingredients, inflation impacts, etc. This is not my estimate for ALTO’s 2023 results , merely an illustration for anyone seeking to understand key drivers.

The issue is that, in the scenario above, the growth CapEx spend will outpace EBITDA and further deplete ALTO’s liquidity. Speculation will center on which projects come online before they run out of cash. Perhaps 35% doesn’t adequately reflect the benefits ALTO receives in the second half of 2023, as protein improvements take hold and corn oil yield increases. Perhaps I have underestimated the benefits corn storage provides to help level out the pain caused by basis in 2022. Regardless, 2022 showed the floor for ALTO is lower than I envisioned, and that has cast doubt on their ability to execute this transformation.

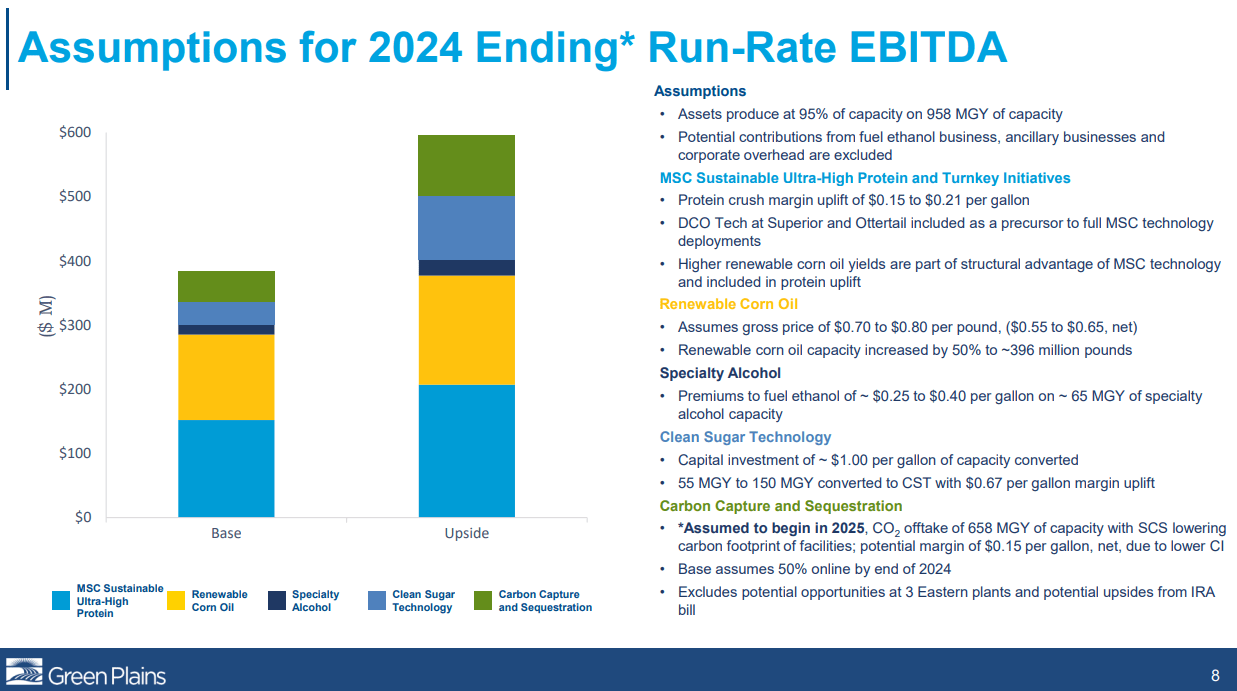

The Future

{kind=link}

G PRE continues to model what ALTO seeks to achieve, and you may recognize the format of the slide. Estimates for specialty used to be $0.66-1.00 and have been dialed back to $0.25-0.40, which hurts the ALTO story more than GPRE.

ALTO should see significant upside from their carbon capture project , where they can negotiate with the Inflation Reduction Act benefits in their back pocket. As we saw above, the greatest fear for investors is whether or not ALTO has sufficient liquidity to bring this project to completion. ALTO could sign a deal to surrender some of the benefits to lower the cost, but this would impair what would otherwise be one of their future sources of earnings. They also face potential regulatory challenges , and nearby states like Iowa have sought to effectively ban the practice .

If ALTO’s average margin for essential ingredients returned to 40% of corn cost, they could add over $30m to EBITDA from my illustration above. It seems likely they can meet or exceed this number once corn oil and protein upgrades mature, but they will need sufficiently supportive ethanol markets to get there. Corn oil benefits should materialize more quickly than protein and are expected to be $4.5m+ per location, annually.

The main challenge when forecasting ALTO’s improvements is establishing baseline EBITDA – is it negative $30m from last year, or positive $60m from prior years? If the former, ALTO may only achieve $30-40m of EBITDA by 2025, or it could be over $100m and 1x their current market cap. The answer depends on factors outside of their control in price-taking commodity markets. If ALTO survives to 2026, they should be able to profit even in terrible fuel markets like Q3/Q4-22. Investors buying the stock today are making a bet that the answer is yes, ALTO has the liquidity to get these projects online and survive.

Conclusion

Investing in Alto Ingredients represents a bet that they can deliver on significant CapEx projects and further insulate themselves from a volatile fuel ethanol market. For jaded investors down 80% in the past two years, this may be a tough sell. Did 2022 represent a one-off confluence of negative factors, or will tough commodity conditions persist? Time will tell, and successful execution should significantly benefit patient shareholders.

For further details see:

Checking On Alto Ingredients After Brutal 2022