CHEF - Chefs' Warehouse: Upside From Wholesale Food Supply - But I Say 'Hold'

2023-09-04 05:16:06 ET

Summary

- Chefs' Warehouse is a specialized distributor of specialty food products to the restaurant, hotel, and catering industry.

- The company has seen significant growth in sales, with over 30% of transactions now placed online.

- Despite being profitable, the company's low margins and potential cost challenges raise concerns about its long-term potential, in keeping this over 1-2% net.

Dear readers/followers,

I'm happy at times to take requests from subscribers to review companies I find interesting. when I got a request a few weeks back to take a look at Chefs' Warehouse ( CHEF ) to see if I could consider the company undervalued here, I was curious. I'd never heard of the business before, but the name alone implied an interesting business model - so I started digging.

This is in no way a "new" company. Chefs' Warehouse has been around for over 30 years and is established not only in the USA but in Canada as well. I like the idea of owning wholesale businesses in this sector because of their link to industries like restaurants, hotels, and catering. This makes for relatively good earnings trends, outside of environments like COVID.

What I mean to do in this article is to offer you a comprehensive presentation of CHEF, its business model, and whether you could or should consider investing in the business from a dividend or valuation standpoint - in short, do I think that you can make money from a conservative basis by investing in CHEF, or should you invest your hard-earned capital elsewhere?

Chefs' Warehouse - Restaurant and Catering Wholesale with an upside

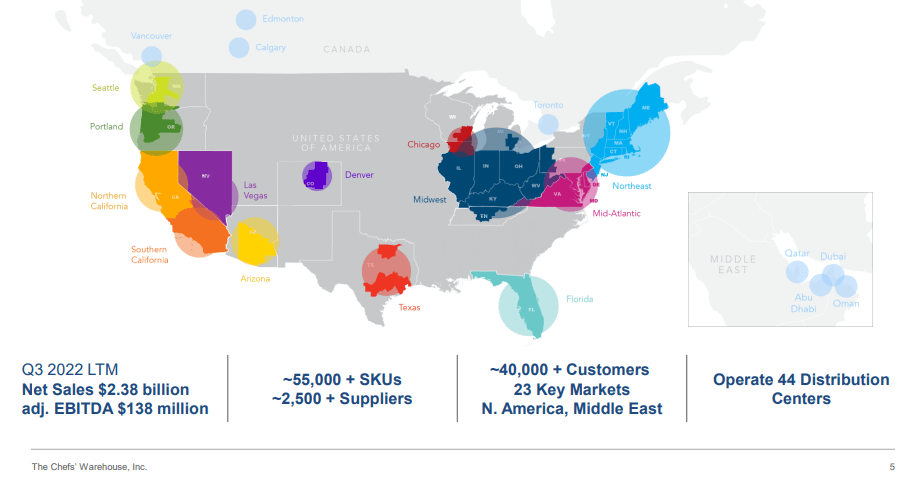

CHEF is a middleman between food production and the restaurant/hotel/catering industry. It's a distributor of specialty food products, serving specific needs of fine dining, restaurants, country clubs, hotels, caterers, specialty bakeries, cruise lines, and some food retailers.

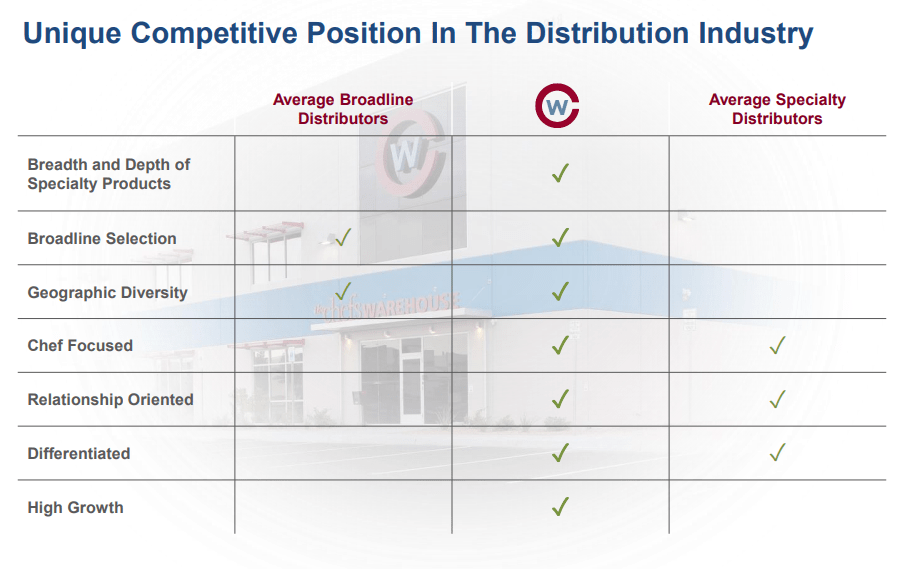

This is far more specialized than your typical food distributor. The company might offer "standard" items, but it works more in the specialty sectors, as can be seen, both in terms of SKUs, suppliers, and geographical coverage, where you find little in areas that do not offer the "finer dining" experience side of things.

{kind=link}

CHEF IR (CHEF IR)

Usually, companies like this have far more SKUs and far fewer suppliers. The indication from its SKU and supplier-number relationship is that the company works with far more suppliers to deliver far less numerous, but specialized goods - and this is the company's business idea.

At the same time, it compares itself to the ~$300B US food service distribution industry - but quickly points out that specialized distribution is even more fragmented than typical food distribution. CHEF as a business represents a leading national competitor in this field, and through its mix, manages to get synergies and advantages from both your standard and highly specialized distribution players.

{kind=link}

CHEF IR (CHEF IR)

To manage this sort of mix, the company needs to be good at a multitude of different things - both managing the macro, but also managing deep and individual customer relationships. Doing so requires resources/capital.

{kind=link}

CHEF IR (CHEF IR)

Personnel and HR for this company are more important than in your typical food distributor. The company also supplies other specialty suppliers and acts as a critical point for many of these, sourcing some of the world's best gourmet brands and products. Combining this with E-commerce can unlock some incredible potential, and the company is already seeing significant growth from an omnichannel/hybrid sales model, offering a comprehensive mobile app. In last year, the company's sales were up significantly and over 30% of transactions are now placed online, which compares to 17% in 2019.

Some basics to consider.

Chefs' Warehouse Incorporated is a B-rated, $1.1B market cap no-dividend growth company.

You'd think that this would make the company uninteresting to a value-oriented dividend investor such as myself. It doesn't. It just makes it crucial that the company manages to "grow" enough to interest me, on a conservative basis, where I feel that I am getting bang for my buck if I do put money into the company's pockets.

What I am about is profit.

And Chefs' Warehouse is profitable.

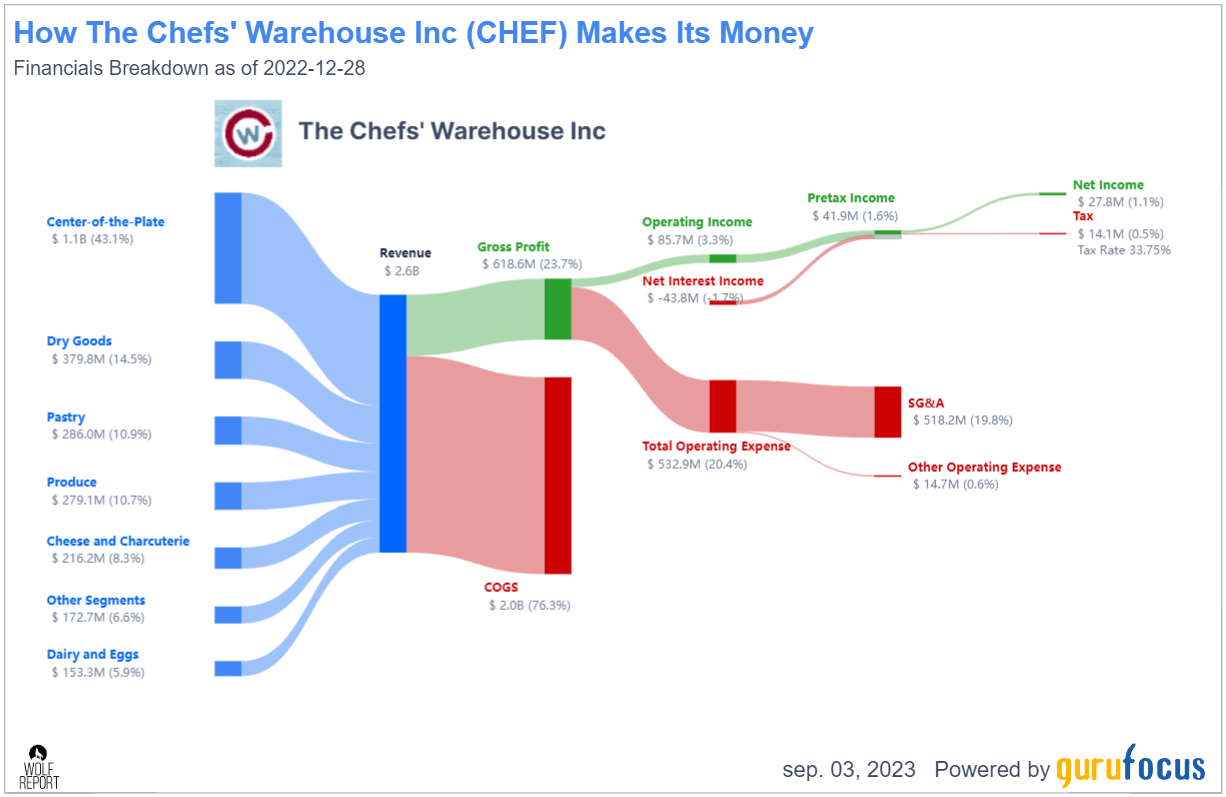

Oh, it's not superbly profitable. The company manages a gross margin of 23.6% and an EBIT margin of 2.92%, making it around 3% on average. That leaves a net margin of less than 1% for the latest numbers (Source: GuruFocus), which means that the company actually manages lower margins than your typical Fast-moving consumer goods company, or FMCG, which I review frequently.

That's a high hill to climb.

We're always putting companies in the context of the larger market, and while CHEF has probably the most interesting business model and business I've reviewed in over 2 months, the business model profitability leaves some things to be desired.

The company actually has lower SG&A than I expected.

{kind=link}

Chefs' Warehouse revenue/Net (GuruFocus)

Instead, which isn't surprising really when you think about it, most of it is COGS. I expect that the shift to e-commerce has also enabled CHEF to dial down its SG&A - but given its specialized focus, the company can't give up - ever - individual client relationships or their work in this area.

Growth can be said to come from a number of factors. You can grow through technology, which the company is doing. You can grow categories organically, try to grow the receipt size, grow organically, find more exclusive/specialized partnerships, and try to leverage sales through better customer relationships. None of this is unusual, and the company is doing all of it.

Its latest move involves a shift to the Middle East, which opens up some of the world's major delicacies market, as well as customer markets. Note the operating areas of UAE, Qatar, and Oman, some of the richest areas on the planet.

{kind=link}

CHEF IR (CHEF IR)

The company highlights continued revenue growth, at a CAGR of 16.7% since 2019. This is a total revenue growth of 59%, out of which more than half was organic. Adj. EBITDA is up 71% to $63M. The fact that the company is indeed profitable on every metric that matters is good - but not "enough", per se.

For any business, but especially for a business like this, what matters are margins. The amount of gross profit or EBITDA growth does not matter as much to me as the growth on a relational basis.

Positives for CHEF do include a significant reduction in leverage. Back in 2019, the company was at 4.1x but is now down to 3.1x with a total net debt of about half a billion here.

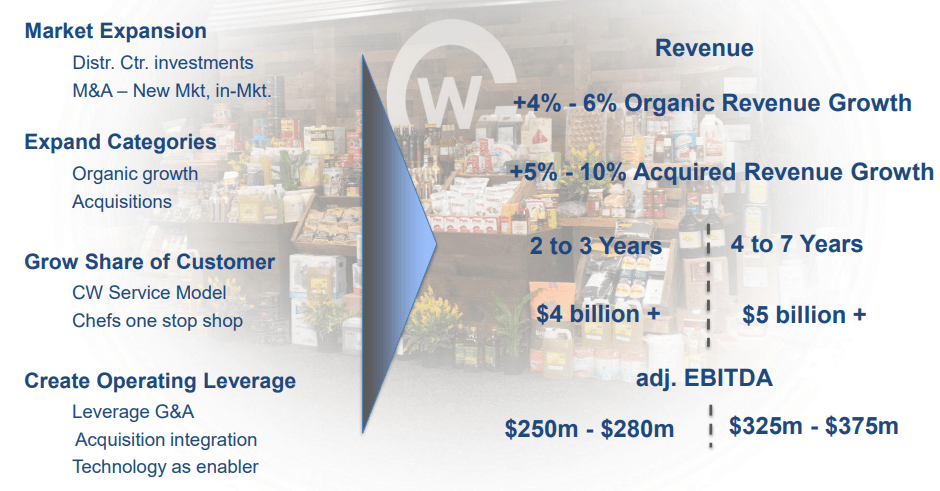

Here are the company's longer-term goals.

{kind=link}

CHEF IR (CHEF IR)

Growing in this market is a rough venture. The company does have some of the size, expertise, and age required to be a potential market leader not only in the USA, but the world, but the journey to growing elsewhere is far more difficult than growing in the home market.

The company expects to hit about $3B, or just below it, in 2023E net sales, with adjusted EBITDA of $190M for the full year. Current estimates from analysts put the company around $ 40M-$50M in normalized net income, which would represent a doubling of the net margin (source: S&P Global). I would say that my expectations lie somewhere around the $ 30M-$33M in net profit, representing that 1.1% net margin, with the possibility of going lower due to cost challenges.

These trends are confirmed by the latest quarterly results. EPS missed targets for 2Q23, but revenue saw a beat. The top line is growing, but the ongoing investments and costs are consuming what the company makes either through increased CapEx or other costs.

Other analysts on Seeking Alpha focus on the understandably undervalued business (because it is undervalued from certain perspectives, more on that in a bit). But in my view, this is a razor-thin margin sort of business, with the potential of going net-negative rather easily for a full year. The fact that it lacks any sort of dividend payout means that you can only invest here if you believe the company is going up.

CHEF is in the midst of scaling, which means that CapEx is up to around 1.5-2% of current revenue (I estimate as high as 2.5%, taking into account spillage and potential unforeseen consequences), and as you know from the short business model review, the company does not have 50 bps to easily take from anywhere - not with a ~1% net margin.

All you need to do is what other analysts are focusing on, and you'll find that for the most part, it's a margin game. The company manages 5-6% EBITDA margin but guides for almost 150 bps above that on the high end. Just where is this growth going to come from, especially with the different characteristics and seasonalities of the Middle Eastern market compared to the US market, which could work against some of the synergies we see in the company?

According to management, M&As and cadence should bring things up to that level. Color me dubious as to that. The company already admitted to unforeseen overhead expenses, and with the recent set of M&A's, it's completely understandable that the visibility for the next half of the year, maybe even longer, is somewhat murky.

When it comes to a company with as low margins as this one, the company has very little room for error. A 50-100 bps variance somewhere, which is not unrealistic, has the potential to drive profitability for CHEF into the ground. The current estimate is for 2023 to be significantly below 2022 due to the outsized strength of 2022, but for 2024 and beyond to go higher due to inorganic growth.

On the high level, I don't have an issue with this forecast, but there are some things to consider in terms of the valuation.

Chefs' Warehouse - The valuation is so-so.

Even my analyst colleagues here SA makes a point to say that margins are terrible in the foodservice industry, but then go ahead to rather generally compare the company to very broadline distributors. What you should not fail to realize is that your typical broadline distributors like SpartanNash ( SPTN ) or US Foods work with completely different cadences and often distribution and customers than does Chefs' warehouse. The expansion into EMEA is also often viewed as a boon - and it is - but it comes, as I see it with monumental challenges that need to be addressed.

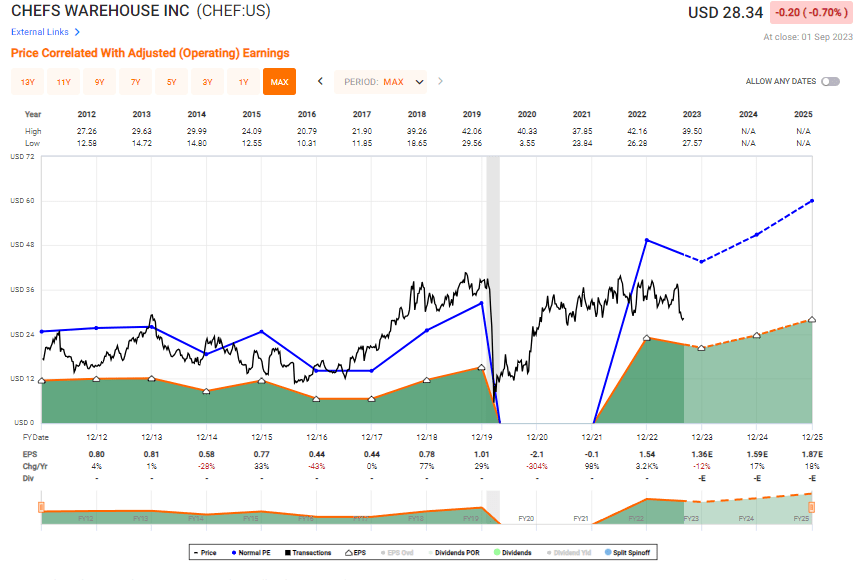

CHEF is a company that's trading at a 19.9x P/E despite coming out of 2 consecutive years of negative adjusted EPS during COVID-19 - understandable, given the state of the industry at that time.

{kind=link}

CHEF valuation (F.A.S.T Graphs)

However, the time to pick this company up on the dirt cheap is over. Now we're back within what I would consider a "normalized" valuation cadence for the business. The market applies a high premium to this business, typically allowing it to trade around 30x P/E, which I would not grant any company in this sector, but certainly not a B-rated, no dividend, 1%-net margin business with low visibility and what I consider to be a sub-par earnings forecast accuracy.

{kind=link}

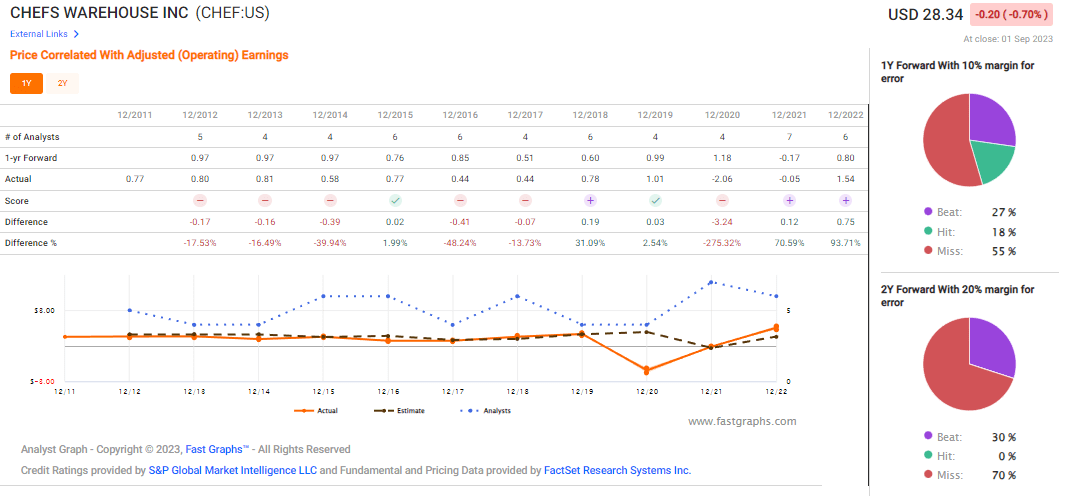

CHEF earnings accuracy (F.A.S.T graphs)

On a 15x normalized P/E, there is nothing to like about this investment. The company has negative RoR at this juncture if you forecast it there, even with a 17-18% Growth rate in terms of EPS for the 2024E-2025E period. In order for the company to have any chance of giving you positive growth, premiumization is required.

That's okay - I have nothing against assigning a bit of a premium to a company in this segment and with these specifics, and despite what I said, this is not a bad company, it's a good/interesting one.

But, that doesn't make it worth 30x P/E. The upside to a 25-30x P/E is as high as 32% per year. But given the earnings accuracy (or inaccuracy) and the challenges presented in terms of expansion CapEx, rising costs, inflation, labor, and different seasonalities, I would be careful entering the company at this time. As I view it, the market is discounting the company heavily until we can see with higher clarity where things are likely to "go".

Investing at this time is the same, to me, as taking an outsized risk, given the lack of a dividend and the fact there's an abundance of investment-graded, dividend-paying larger companies out here to invest in. This is an investment where I would say a double-digit upside is likely. On the basis of this, it can be investable.

But I don't view it as investable in this context compared to what else is available.

S&P Global gives the company an average PT of $46.7, with 5 out of 7 analysts being at "BUY". There's a high conviction here, but it's important to remember that these analysts have been holding $45-$50/share PTs for this company for over 2 years at this point -- and the company has rarely if ever during that time managed to come close to this.

A more conservative approach is suitable here.

I value the company at around 18-20x P/E, which caps to me the PT at around $33/share, which is more than $10/share below the other analyst targets. I justify these with the growth challenges and the fact that CHEF is not that conservatively leveraged. Above 3x for an FMCG or food distribution company is not that great.

I don't give PTs specific to market situations unless it's a long-lasting one. But I do give ratings specific to market situations. This can create situations where the essence of my rating is that "I acknowledge that this company is worth X, but I would still wait and rate this as a "HOLD" here.

That's the case with CHEF.

Here is my thesis for the business.

Thesis

- Chefs' Warehouse is an interesting business with a working business model, but an overall very low margin of below 1.5% net. This necessitates conservative estimates when investing in the business to not risk negative development in a downturn through investing in over-premiumized equity - as we've seen in the last few months.

- I would be interested in buying Chefs' Warehouse when we get more visibility from the EMEA sector and a clearer view of costs for this year.

- I give Chefs' Warehouse a PT of $33/share but still rate the company a "HOLD in the next few months for the reasons mentioned here and in the article.

Remember, I'm all about : 1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company has no dividend and I would not consider it cheap in this context. You could "BUY" it, but that would be risk, as I see it. For that reason, I give the company a "HOLD" here.

For further details see:

Chefs' Warehouse: Upside From Wholesale Food Supply - But I Say 'Hold'