NRDY - Chegg: Bullish With A Tailwind For Earnings In 2023

Summary

- Chegg, Inc. has rallied sharply from its 2022 lows with positive momentum entering the new year.

- Chegg is transitioning away from its legacy textbook rental business to focus more on high-growth services that can add to profitability.

- We like Chegg, Inc. stock as it benefits from solid fundamentals and a positive long-term outlook.

Chegg, Inc. ( CHGG ) has moved beyond its pioneering college textbook rental model with growth in recent years driven by an expansion into services including targeted study materials and step-by-step homework solutions. The attraction here is strong demand from University and high school students looking to learn through a technology platform and save time in the academic process.

Indeed, 2022 was marked by Chegg's transition away from handling physical book sales and rentals, while adding a new language learning segment through " Busuu ," and skills courses on topics like computer programming. The result is a more targeted business that is set to generate higher margins by focusing on high-growth opportunities. That being said, shares have been volatile amid the broader market selloff, with growth moderating against pandemic-skewed benchmarks.

We like Chegg stock into 2023 as it benefits from several underlying tailwinds with room for earnings to accelerate. We are bullish on CHGG as a high-quality free cash flow profile supports a positive long-term outlook.

CHGG Key Metrics

Chegg, Inc. last reported its Q3 earnings in November with a non-GAAP EPS of $0.21, which beat expectations by $0.07. While revenue at $167 million was down -4% from an exceptionally strong 2021, the figure also beat the consensus estimate by $6 million. Management notes that a $1.00 increase to the "Chegg Study" package drove an increase in the average revenue per user, with total subscribers reaching 4.8 million, up 8% year-over-year. Adjusted EBITDA at $50 million was also up 8% from $46 million in the period last year.

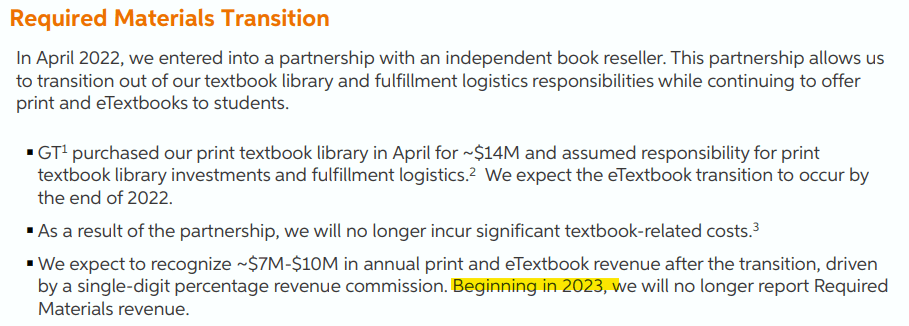

Reconciling the net revenue decline, keep in mind that the company has exited the "required materials" segment by essentially outsourcing its textbooks business. The announcement came back in Q2 with Chegg partnering with " GoTextbooks " GT Marketplace LLC to completely manage the textbook side of the business with control of fulfillment and logistics.

In other words, students can still make the orders on Chegg while the company is simply recognizing a marginal commission which is expected to generate upwards of $10 million in revenue per year. More favorable is the impact on margins, as the company no longer needs to deal with the publisher content fees, print textbook depreciation, and related customer support.

{kind=link}

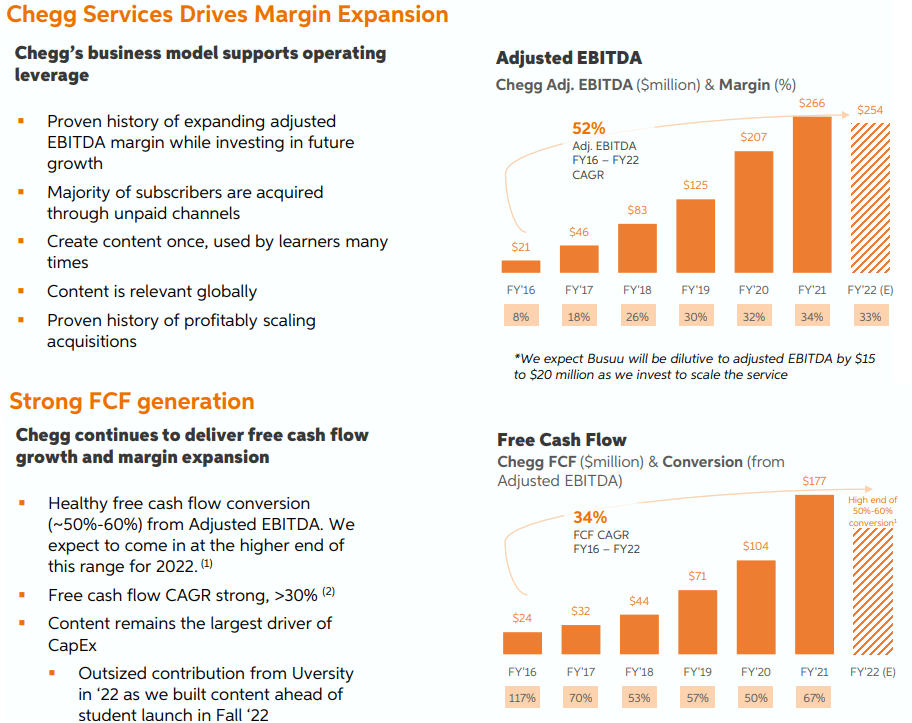

The result is a boost to overall profitability expected going forward. For context, the adjusted EBITDA margin is on track to end 2022 at just around 33%, which is up from 30% back in 2019 as a pre-pandemic benchmark. An interpretation here is that Chegg is moving more towards "tech" and relying less on the more capital and logistically-intensive side of academia.

{kind=link}

We mentioned Chegg's impressive free-cash-flow generation. On this point, the conversion from EBITDA averaging 55% over the last five years highlights a good balance between ongoing investment spending towards content while delivering an ongoing balance sheet deleveraging. The company creates study modules which have a long useful lifespan with students around the world reusing the same materials.

Chegg ended the last quarter with $1.2 billion in cash and investments against $1.2 billion in long-term senior notes, down from $1.7 billion at the end of 2021. The company has also been active with buybacks, repurchasing $324 million in common stock year-to-date through Q3, within an expanded $1 billion repurchase authorization.

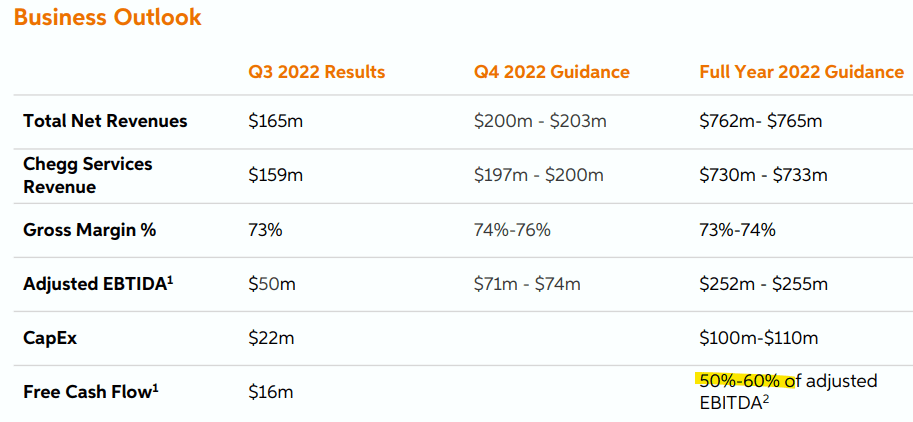

With the yet-to-be-reported Q4 results, management is targeting full-year 2022 revenue between $762 million and $765 million, representing a -1.5% decrease from 2021. Again, the context here is the volatility from the transition away from the textbook business, although the 8% increase in "Chegg Services" revenue is likely a better representation of the underlying momentum. Also, keep in mind that 2021 was exceptionally strong, leaving some tough comparables.

{kind=link}

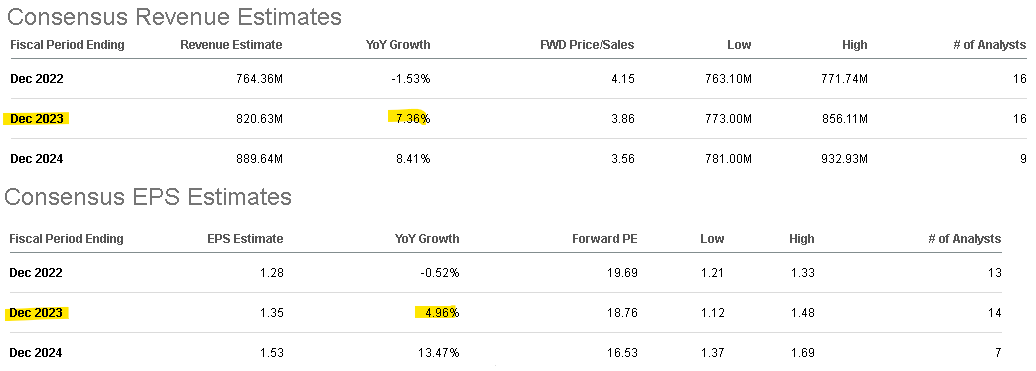

The consensus EPS estimate for 2022 at $1.28 is nearly flat year-over-year. For 2023, the market sees a rebound in earnings towards $1.35, up 5% year-over-year and above $1.34 in 2020. Looking ahead, annual earnings growth can trend above double-digits by 2024 with a sense that international expansion begins to deliver a positive contribution at scale.

{kind=link}

What's Next For Chegg?

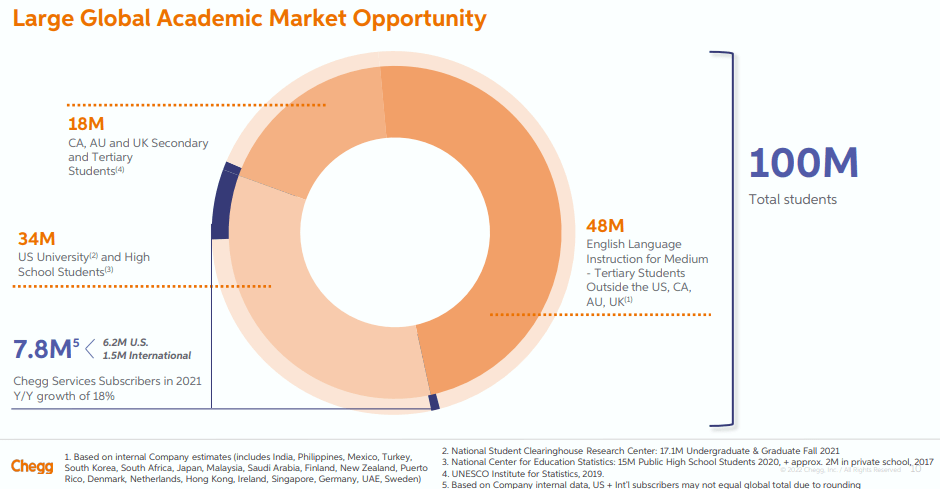

Chegg sees a large global academic addressable market of 100 million students as English speakers both in the U.S. and international regions outside North America, U.K., and Australia. Compared to 4.8 million "services" subscribers at the end of last quarter, the potential to incrementally add just a few percentage points in an expanding market highlights the growth opportunity. Over time, there is also an effort to launch tools in foreign languages like Spanish.

The idea here is that there is an entirely new generation of learners that are most comfortable with the type of tools on the Chegg platform that leverages personalized, adaptive, and mobile technology. The data the company shares suggest students on the platform are both finding value in the service while also helping to deliver higher grades.

{kind=link}

When looking at the universe of online education companies, what stands out to us is the wide range of diversity with different companies focusing on various segments and learning models. By this measure, while Chegg has several peers and rivals, the company's value proposition of direct-to-student "study guides", homework help, and problem-solving tutorials are relatively unique.

This is in contrast to Udemy, Inc. ( UDMY ), which is set up more like a marketplace for independent teachers to publish courses and learning videos. Similarly, Nerdy, Inc. ( NRDY ) through its "VarsityTutors" platform is structured as a one-one tutoring service that may not appeal to all learners. Duolingo, Inc. ( DUOL ) specializes in language learning, which is just one part of Chegg's offering. There is also a larger group of online dedication providers among private schools and those working directly with educators as part of the standard learning tools, such as Stride, Inc. ( LRN ).

The way we see it is that the strength of Chegg is that its curriculum is developed directly, corresponding to the textbooks students are working with daily. They may need help solving "problem number 17 in chapter 5," and Chegg has that answer. That connection with the official course material is a major selling point that keeps subscribers coming back.

As it relates to valuation, Chegg is among the few profitable tech-focused online education platforms. The combination of recurring earnings and positive growth gives it a good backdrop of value. Longer term, there is always the risk that different players in the segment begin to offer similar or alternative solutions, but the strong point here is Chegg's brand awareness and reputation of authority in its subjects.

CHGG Stock Price Forecast

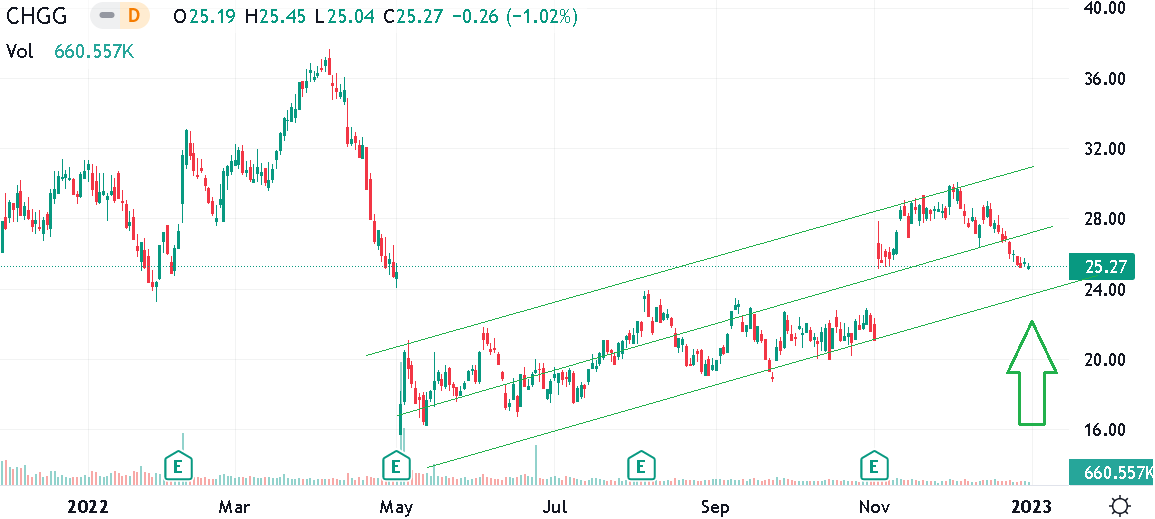

CHGG ended the year 2022 down 18%, although investors should be more encouraged by the more recent positive trend with shares up 60% from its Q2 low when it briefly traded under $16.00. We believe the relative strength here has room to continue through 2023 which is set up to be a year we believe earnings can outperform.

The combination of margins getting a boost since exiting the course materials textbook business while adding more value-added skills and learning features including foreign languages make Chegg well-positioned to see a resurgence of growth. Separately, the opportunity to expand into international markets is still in the early stages.

We rate CHGG as a buy with a price target for the year ahead at $32.50, representing a 23x multiple on the current 2023 consensus EPS of $1.35. In our view, this type of multiple is justified for a segment leader supported by strong fundamentals. The potential that earnings outperform will narrow the valuation spread and make shares appear even more compelling. The rock-solid balance sheet and recurring positive free cash flow make CHGG a high-quality tech name in our book.

In terms of risks, the downside to CHGG would come down to a deterioration of the broader economic outlook with an implied impact on demand for these types of academic services. A scenario where unemployment rises sharply or consumer spending faces a significant drop beyond the current baseline would undermine the operating environment and force a reassessment of the earnings trajectory.

While a date has not yet been confirmed, expect the Q4 earnings to be released in early February. Over the next few quarters, the key monitoring points for the stock will be strength in core services, the adjusted EBITDA margin, and high-level subscriber trends.

{kind=link}

For further details see:

Chegg: Bullish With A Tailwind For Earnings In 2023