CQP - Cheniere Energy Partners: Buy This Stock For Solid Dividend Yield

2023-05-09 18:56:46 ET

Summary

- The company has reported a revenue of $2.91 billion, decrease of 12.34% compared to $3.32 billion in Q1FY22.

- The company can distribute an annual dividend of $4.125, representing a dividend yield of 9.12%.

- After comparing the company's forward P/E ratio of 10.26x with its 5-year average P/E ratio 13.34x, I think the company is undervalued.

Investment Thesis

Cheniere Energy Partners ( CQP ) is an energy firm that deals in liquified natural gas. It has recently reported its quarterly results for the first quarter. I believe it can experience solid growth in the coming quarters due to the strong tailwinds in the natural gas industry. This growth can help the company to sustain its high dividend payout, which makes it an attractive opportunity.

About CQP

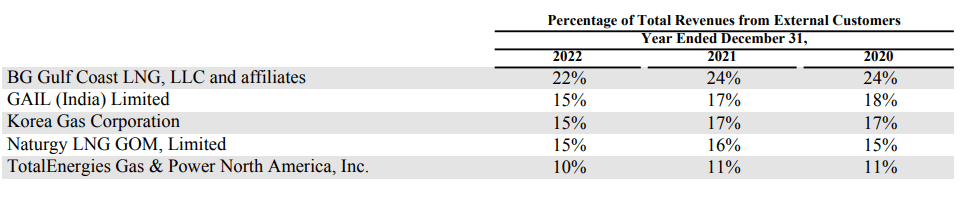

CQP provides liquified natural gas to utilities, integrated energy companies, and energy trading companies around the globe. Its major customers include BG Gulf Coast LNG, GAIL (India) Limited, Naturgy LNG GOM, TotalEnergies Gas, Power North America, and Korea Gas Corporation. The LNG produced by the company gets shipped worldwide, converted back into natural gas with a regasification process, and then transferred via pipeline to homes and companies, where it is used as an energy source for heating, cooking, and other industrial purposes. The business owns the Sabine Pass LNG terminal in Cameron Parish, Louisiana, which has six liquefication Trains with a total production capacity of roughly 30 Mtpa of LNG. The Sabine Pass LNG terminal also contains operational regasification facilities, which comprise five LNG storage tanks, vaporizers, and three maritime berths. It also owns the Creole Trail Pipeline, which connects the Sabine Pass LNG plant to several major interstate pipelines. The Sabine Pass LNG Terminal's liquefication and regasification operations constitute a single reportable segment. The company generates 93.42% of revenues from the sale of LNG, 6.21% from regasification, and 0.37% from other sources.

Revenue from External Customers (10K of Cheniere Energy Partners)

{kind=link}

Financials

In 2022, the LNG market experienced unprecedented price volatility across all natural gas and LNG benchmarks. Global gas market fundamentals were tight, which was compounded by Russia/Ukraine war concerns, and later by a substantial decline in Russian natural gas exports to the European Union ((EU)). Europe had to compete for LNG cargoes, resulting in unprecedented price increases. These conditions were exacerbated by high coal costs, low nuclear production output, and low hydro levels in Europe, which constrained the operations in the industry and worsened Europe's energy crisis. Kpler reported that despite tight supply scenarios, global LNG demand has grown by approximately 5% from 2021, adding 19.5 million tonnes more to the market. I believe the worldwide demand for the industry can further increase as LNG plays a prominent role in the clean energy transition, which has forced the majority of nations to adopt cleaner fuel alternatives. In addition, supportive policies, high government investment in clean energy, and strict regulations on hydrocarbons can also contribute to future growth.

Between 2020 and 2022, the United States passed the Infrastructure Investment & Jobs Act and the Inflation Reduction Act, which funds around $450 billion in sustainable energy and related investments. This heavy investment in clean energy signals the potential growth in the LNG industry. In the last quarter of 2022, Wood Mackenzie Limited (Woodmac) forecasted that global LNG demand can increase by 53%, from 388.5 million tons per annum to 595.7 million tons per annum by 2030 and 677.8 million tons per annum by 2040. As per my analysis, these positive growth factors can accelerate the company's future growth and help it capture additional market share as it plans to significantly expand its Sabine Pass LNG capacity , which can strengthen its capabilities and increase its operational efficiency leading to higher profit margins.

CQP has reported its mixed first-quarter results . It has reported a revenue of $2.91 billion, a decrease of 12.34% compared to $3.32 billion in Q1FY22. The decrease was mainly driven by a decline in regasification revenues by 50%. It reported an adjusted EBITDA of $1.02 billion, a decrease of 0.48% compared to $1.03 billion in the same period last year. Net income saw an astonishing 1117% YoY growth from $0.15 billion to $1.93 billion in Q1FY2022. Non-cash favorable changes in the fair value of commodity derivatives and increased LNG deliveries primarily contributed to the net income growth. Improved net income resulted in an earning per unit of $3.50 compared to the net loss per unit of $0.11 in Q1FY22. The company ended its first quarter with $0.83 billion in cash and cash equivalents. The company expects FY2023's full-year distribution per unit between the range of $4.00-$4.25. After analyzing the company's current demand scenario and expansion plans, I believe these estimates are correct. I think as the focus is turning toward clean energy, the company can sustain its growth for a longer period. In addition, the company has contracted approximately 85% of its anticipated production capacity, which can help it to stabilize its growth.

According to data found on Seeking Alpha, the company's revenue for FY2023 might be in the range of $9.47 billion to $13.12 billion. I think the revenue estimate of $10.66 billion perfectly captures the impact of current demand in the market and low prices. The company's 5-year average net income margin is 18%. However, after considering the demand in the market and the net income margin of Q1FY23, I think the company can exceed the 5-year average net income margin. That is why I am estimating a net income margin of 20%, which gives me an estimated $4.41 earnings per unit.

Dividend Yield

The company has a long and impressive track record of dividend payouts which signals its good positioning in the market. In the previous year, it distributed a cash dividend of $0.7 in the first quarter, $1.05 in the second quarter, $1.06 in the third quarter, and $1.07 in the last quarter, which makes the total annual dividend $3.88 per share, representing a dividend yield of 8.63% compared to the current share price. In the current year, the company distributed a cash dividend of $1.07 in the first quarter and $0.775 in the second quarter. The management has reconfirmed their distribution guidance of $4.00 - $4.25 per common unit in the Q1FY23 result. Observing the current high growth potentials of the company due to the rising demand scenarios, solid quarterly performance, and its expansion activities, I believe that it can sustain this dividend growth in the next quarters as well. I am taking an average of the upper and lower limits of the distribution guidance of the company to keep my estimate conservative. I estimate that it can distribute an annual dividend of $4.125, representing a dividend yield of 9.12% compared to the current share price of $45.24. The company's forward dividend yield of 9.12% is significantly higher than the 4-year average dividend yield of 6.75% and sector median dividend yield of 4.48%. This high dividend yield makes CQP an attractive investment opportunity for risk-averse investors looking for passive income and capital appreciation.

What is the Main Risk Faced by CQP?

The company relies on third-party pipelines and other facilities to transfer gas to its liquefaction facility as well as to and from the Creole Trail Pipeline. Suppose the supply of natural gas from the third party disrupts due to reasons such as lack of capacity, damage to the facility, or weather events. In that case, it can negatively impact the company's operations by further contracting its profit margins.

Valuation

The company has recently reported its mixed first-quarter results and outperformed the market expectation in terms of net profit. The high global demand for LNG mainly drove this growth, and I believe the company can sustain this growth as LNG demand can continue to rise in the future due to the adoption of cleaner energy alternatives. In addition, the company is expanding its capacities at Sabine Pass, which can strengthen its position in the competitive market. These growth factors can push the stock upwards, and we can expect a long-term upside. After considering all the above factors, I am estimating revenue of $10.66 billion and a 20% net profit margin, which gives a $4.41 earnings per unit for FY2023. The earning per unit of $4.41 gives the forward P/E ratio of 10.26x. After comparing the forward P/E ratio of 10.26x with the sector median of 8.33x, the company seems overvalued at its current share price. However, the company has a tendency to trade above its sector median, as its 5-year average P/E ratio is 13.34x. Therefore, after comparing the company's forward P/E ratio with its 5-year average P/E ratio, I think the company is undervalued. In my opinion, the company might gain significant momentum due to the rapidly rising demand for LNG and its recent expansion activities, which can help it to increase its capabilities and help it to trade at its 5-year average P/E Ratio. Therefore, I estimate the company might trade at a P/E ratio of 13.34x, giving the target price of $58.83, a 30.03% upside compared to the current share price of $45.24.

Conclusion

The company has recently reported mixed first-quarter results and delivered a solid performance, outperforming market expectations. This growth was mainly driven by increasing demand for LNG on a global level. I believe the company can sustain this growth in the future as LNG demand is expected to grow exponentially due to its increasing need to reduce carbon emissions. It is exposed to the risk of supply disruptions which can contract its profit margins. As the company is growing financially, it can significantly increase its dividend payout in the future, making it an attractive opportunity for risk-averse investors. The stock is currently undervalued, and I believe we can expect a healthy 30.03% growth from current price levels due to the strong tailwinds in the industry and expansion activities of the company. After analyzing all the above factors, I assign a buy rating to CQP.

For further details see:

Cheniere Energy Partners: Buy This Stock For Solid Dividend Yield