CQP - Cheniere Energy Partners: Structure Is Unattractive

2023-07-27 19:15:41 ET

Summary

- Cheniere Energy Partners owns and operates the Sabine Pass LNG Terminal, one of the world's largest LNG production facilities.

- Despite a nice yield, CQP is not associated with all of Cheniere’s growth projects, its distribution coverage is light, and its incentive distribution rights are a burden.

- In my view, the stock is not as attractive as its parent company, Cheniere Energy.

While Cheniere Energy Partners ( CQP ) offers a nice yield, the stock is not anywhere near as attractive as its parent.

Company Profile

CQP is part of the Cheniere Energy ( LNG ) family. It owns and operates the Sabine Pass LNG Terminal in Cameron Parish, Louisiana, which is one of the largest LNG production facilities in the world. The facility has approximately 30 mtpa of LNG capacity through its six operational trains. The facility is also able to store approximately 17 Bcfe of LNG with its five LNG storage tanks.

Sabine Pass also has three marine berths. Two of the berths handle ships with capacity of up to 266,000 cubic meters, while the third can accommodate 200,000 cubic meters. The company also has a 94-mile pipeline, the Creole Trail Pipeline, that connects to several interstate and intrastate pipelines, as well as plant that can handle 4 Bcf/d of regasification capacity.

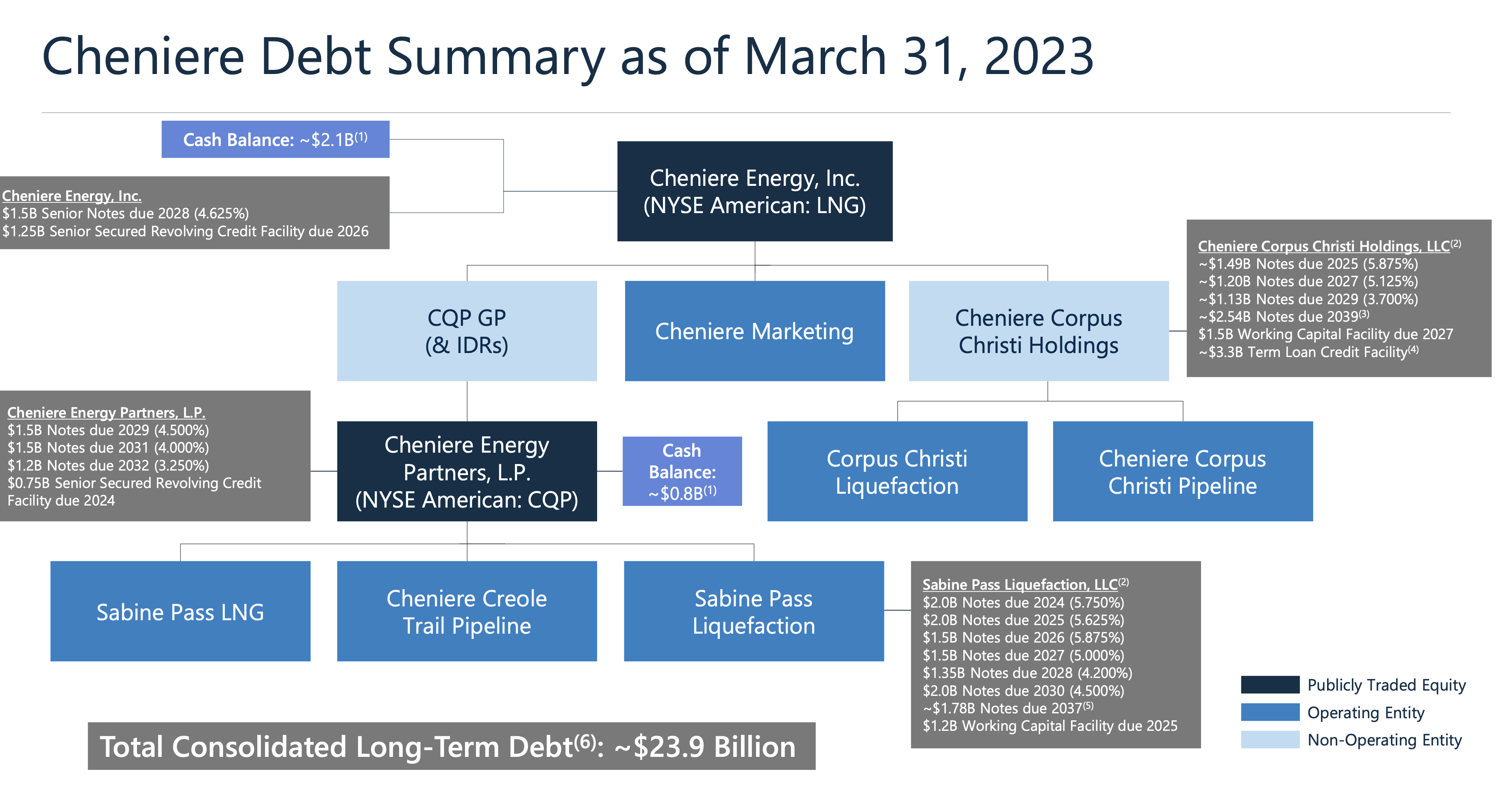

Cheniere Energy owns 48.6% of CQP, as well as its general partner and incentive distribution rights (IDRs).

Opportunities and Risks

Similar to Cheniere Energy, CQP has a pretty steady business, as about 85% of its total product capacity is contracted out through SPA or IPM agreements. These contracts have about a 15-year remaining life. Under its SPAs, CQP’s customers must pay a fixed fee on contracted volumes even if they decide to cancel or suspend deliveries of LNG cargoes. Meanwhile, under its IPM agreements, gas producers sell it natural gas based on a global LNG index price, less a fixed liquefaction fee, shipping and other costs.

CQP’s top-5 customers representing 77% of its 2022 revenue are all on SPAs. That does add some concentration risk if one were to unexpectedly go under, but that is unlikely.

{kind=link}

The IPM agreements come with commodity price exposure, which the company somewhat hedges out. While the Cheniere Marketing unit isn’t under the CQP umbrella, CQP also benefited from higher LNG prices and increased margins on its unsold production, just not to the extent of its parent company. CQP saw 2022 EBITDA jump 65% to $5.1 billion, versus a 138% increase in EBITDA for Cheniere Energy to $11.6 billion. Much of the difference on a percentage basis can be attributed to Cheniere Energy's marketing unit.

Similar to Cheniere Energy, expansion to meet increasing global LNG demand will be a growth driver for the CQP. However, Cheniere Energy’s Corpus Christie facility is not under CQP’s umbrella, which will be the first of the expansion projects. The company has only started to have FEED work done at Sabine Pass, so the project won’t be coming online anytime soon. The company is looking to eventually add an additional three trains with over 20mpta in capacity combined, as well as 2 additional LNG storage tanks.

Discussing the Sabine Pass expansion project on its Q1 earnings call , Cheniere CEO Jack Fusco said.

“Moving on to the Sabine Pass expansion project, which we revealed on our call back in February. I'm extremely excited about developing this major 20 million-tonne expansion, which has the ability to leverage our massive infrastructure position at Sabine Pass for economically advantaged incremental capacity. We have submitted the prefiling documents to FERC. We recently signed a contract with Bechtel for the FEED work related to this large-scale project, including for the carbon capture component. Commercially, the project is already gaining traction. As I highlighted earlier, last week, we're executing SPA of approximately 0.4 million tonnes per annum for over 20 years with an investment-grade Asian end user for LNG volumes delivered through 2047. Most of the volumes associated with the SPA are subject to FID of Train 1 of the Sabine Pass expansion project. We are excited to have already signed an SPA linked to the project and to be building commercial momentum as we progress development. We progressed these project developments in an environment marked by cost inflation, rising interest rates and extremely competitive LNG markets. These realities not only underscore the importance of Cheniere's competitive advantages but also our resolute commitment to the investment parameters that guide our disciplined approach to capital investment.”

Notably, Cheniere Energy has already started selling more potential production for an expanded Sabine Pass since its announcement. The company recently announced two deals where half the agreement volumes would be dependent on a 7 th train coming online. The deals are with ENN for 1.8 million tonne a year in total and Equinor for 1.75 million tonnes a year in total.

The company is also looking into possibly build a new pipeline to bring more natural gas to Sabine Pass. This would presumably be done under the CQP umbrella.

When it comes to risks, one thing to note with CQP is that it is one of the few MLPs that still are burdened by IDRs. The company is also in the dreaded high splits, whereby with every quarterly distribution increase, an equal amount will go to its GP Cheniere Energy.

This is the equivalent of a huge tax on the firm every time it increases its distribution, and thus there is a huge 50% transfer of value on every quarterly distribution amount over 63.8 cents. Most MLPs eliminated their IDRs several years ago by buying them out from their parents.

CQP currently pays a base distribution of 77.5 cents, along with a variable distribution. It is expecting to pay out a distribution of $4.00-4.25 in 2023.

CQP also faces construction risks. With its project further out, inflation costs are a real risk and could lessen the attractiveness of the expansion project. Regulatory risks are also present when building LNG facilities, but hopefully with expansion it should be easier to get approvals. Then CQP also runs the risks of delays and overruns once construction on these projects begin.

Cheniere also carries a lot of debt, much of with is at the CQP level or below.

{kind=link}

Valuation

CQP trades at 10x the 2023 EBITDA consensus of $3.93 billion. For 2024, it trades at 10.1x the 2024 EBITDA consensus of $3.87 billion.

It trades at about 9.2x P/DCF of $2.73 billion (my estimate), and has a 2023 DCF yield of nearly 11%.

The stock currently yields 8.2% with about a 1.1x coverage ratio.

Conclusion

If you want exposure to the growing LNG market, stick to Cheniere Energy, which I wrote up here . CQP gives you a nice yield, but it’s not associated with all of Cheniere’s growth projects, its distribution coverage is light, and its IDRs are a burden. The fact that CQP did not eliminate its IDRs when most MLPs did is a disappointment in my view, and having them remain in place is not unitholder friendly. In addition, with expansion projects further out, CQP looks relatively expensive compared to other midstream stocks.

If you want yield from the energy or midstream space, there are just better options. I like Cheniere Energy and the LNG export story, I just don’t like CQP. As such, I’m largely neutral on the name and would be a buyer of the parent instead.

For further details see:

Cheniere Energy Partners: Structure Is Unattractive