LNG - Cheniere Energy: The King Of LNG - Why It Remains Undervalued

2023-08-08 07:28:43 ET

Summary

- Cheniere Energy is benefiting from rising demand and favorable pricing in the LNG market, with LNG replacing Russian gas as Europe's baseload supply.

- The company has secured record levels of long-term contracts, particularly for US volumes, and is expanding its facilities to meet growing demand.

- Cheniere has raised its guidance for 2023 and plans to increase shareholder distributions through dividends and share buybacks. Valuation is estimated to be between $200 and $220.

Introduction

This morning, I briefly considered wearing a hoodie. I cannot remember the last time I wore one - let alone in early August.

As I doubt that anyone cares what I wear, let me quickly explain that it's cold and rainy in Western Europe right now. While this is great news for farmers who finally enjoy a year without severe droughts, it's bad news if below-average temperatures continue in the winter. After all, since the invasion of Ukraine, Europe has relied on liquid natural gas ("LNG") imports to offset the massive supply gap from Russian gas cuts.

That's where Cheniere Energy (LNG) comes in. This giant doesn't produce natural gas. It produces LNG and ships this to customers all over the world.

In May, I wrote an article titled Cheniere Energy Saves The World , which was aimed at assessing the risk/reward after the stock had declined for almost six consecutive months.

The company is set to benefit from decades of rising demand and favorable pricing, and investors can benefit through distributions. LNG has replaced Russian state-owned Gazprom as Europe's new baseload supply, with LNG accounting for two-thirds of the region's imports through the 2022-2023 winter season.

Now, the stock is gaining upside momentum again, as the bull case is unfolding nicely, backed by strong demand, new long-term contracts, and favorable developments putting a bigger emphasis on LNG exports.

In this article, we'll discuss all of this and assess the risk/reward in light of the new uptrend.

Even if investors don't own Cheniere, I believe we'll discuss developments that are important in any major macro outlook.

So, let's get to it!

The World Needs LNG, Cheniere Has It

The US is the largest producer of natural gas in the world, which puts it in a terrific spot to export it to European nations that used to rely on Russian gas, Asian nations trying to decarbonize a very dirty energy mix, and African nations in the early stages of explosive middle-class growth.

However, in order to export natural gas, it needs to be liquified. After all, building pipelines from the US to Europe and Asia is a total no-go.

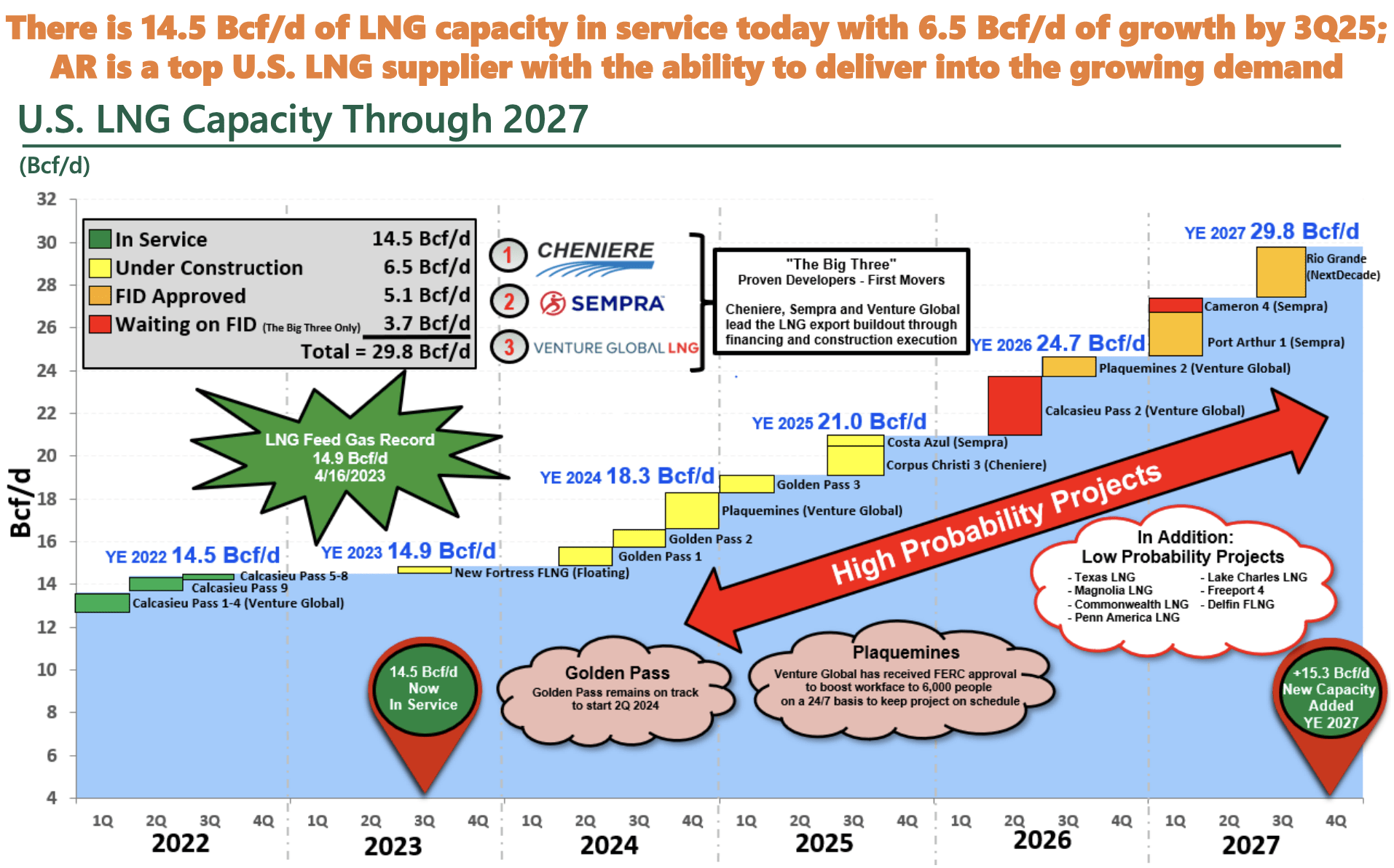

Antero Resources ( AR ), an upstream natural gas producer, estimates that LNG export capacity through 2027 is likely to more than double compared to current levels, led by the Big Three , which includes Cheniere Energy.

{kind=link}

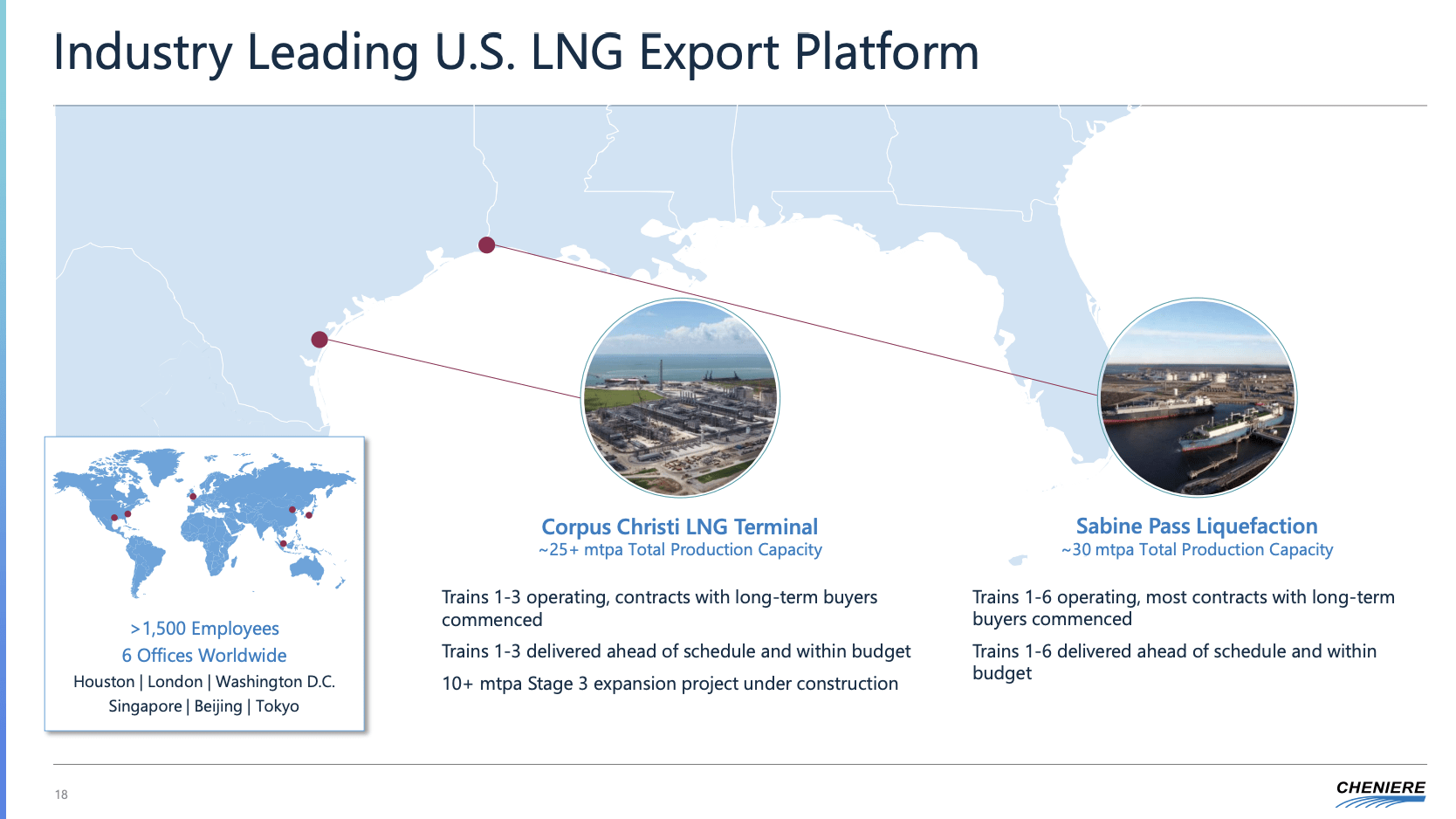

Cheniere is one of the few global LNG export companies with a mature business model and free cash flow.

After many years of aggressive investments, the company is now the biggest US LNG exporter. Founded in 1996, it operates the Sabine Pass and Corpus Christi terminals, which were the first major terminals to allow for global natural gas exports.

Energy Information Administration

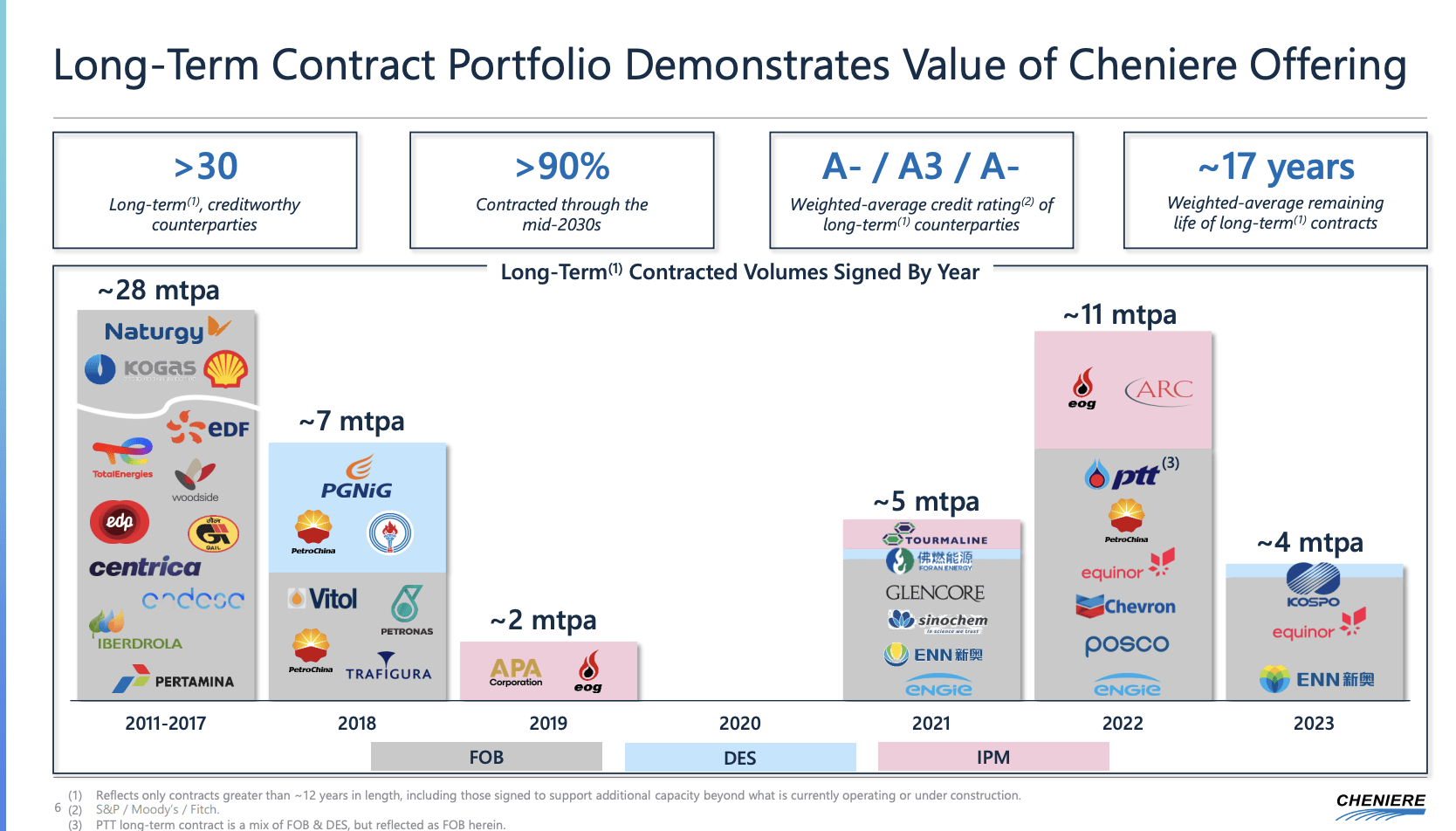

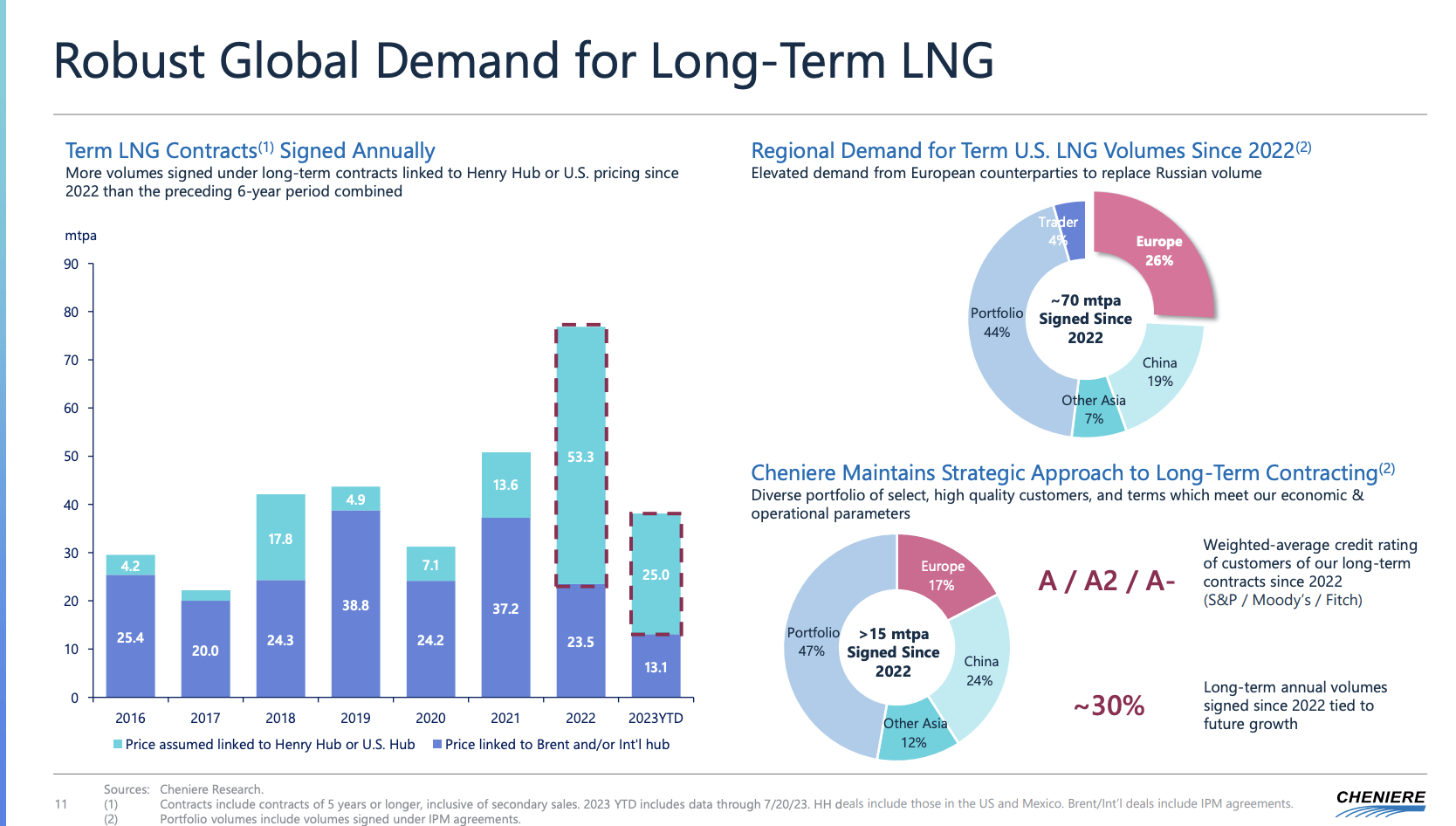

In light of these developments, Cheniere is in a terrific spot. During the Q2'23 earnings call, the company discussed record levels of long-term contracting over the past 12 to 18 months, particularly for US volumes.

Despite potentially softened near-term demand, strong trade outlooks, especially from fast-growing Asian economies like China, are expected to drive LNG supply growth.

For example, European and Asian buyers engaged in long-term contracts, with Cheniere signing over 15 million tons of contracts in the last 18 months.

The second quarter alone saw three new long-term Sales and Purchase Agreements (SPAs) in support of the SPL (Sabine Pass Liquefaction) expansion project.

The SPAs were signed with Korea Southern Power, Equinor, and ENN, totaling just under four million tons per year. Also, the weighted average credit rating of its contract counterparties is A-, which shows that it tends to do only business with the strongest players in the room.

{kind=link}

The company is also expanding its Corpus Christi (Stage 3) facility.

During the Q2'23 earnings call, the progress of the Corpus Christi Stage-3 project was highlighted, with construction ahead of schedule and positive expectations for LNG volume delivery in 2025, and potential completion of the entire Seven Train project by the end of 2026.

{kind=link}

The company invested roughly $200 million during the quarter and over $2 billion to date in the Stage-3 project, which also shows how expensive building a solid energy infrastructure is.

With this in mind, thanks to the company's footprint, it has a very good idea of what is happening in its industry around the globe.

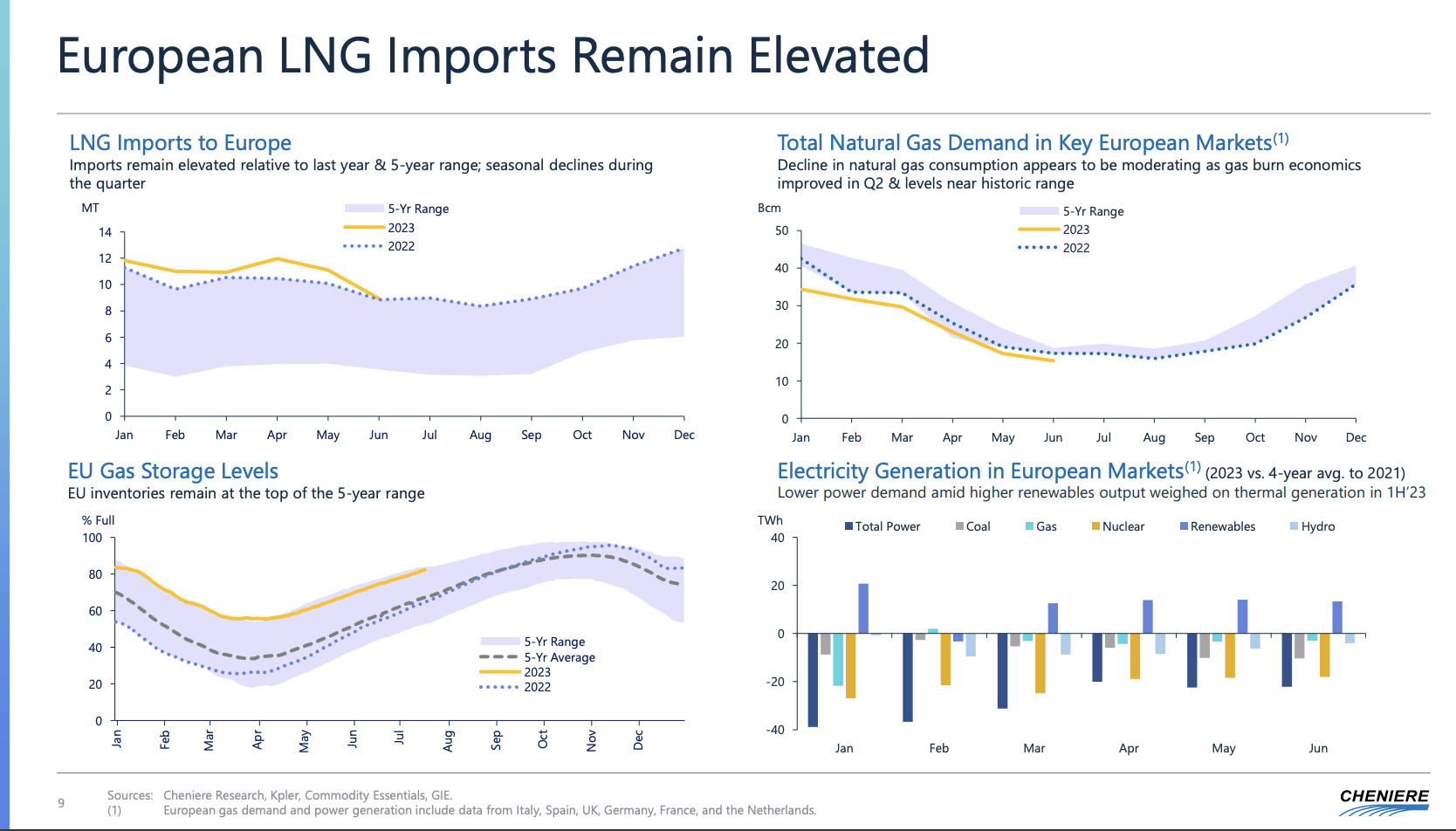

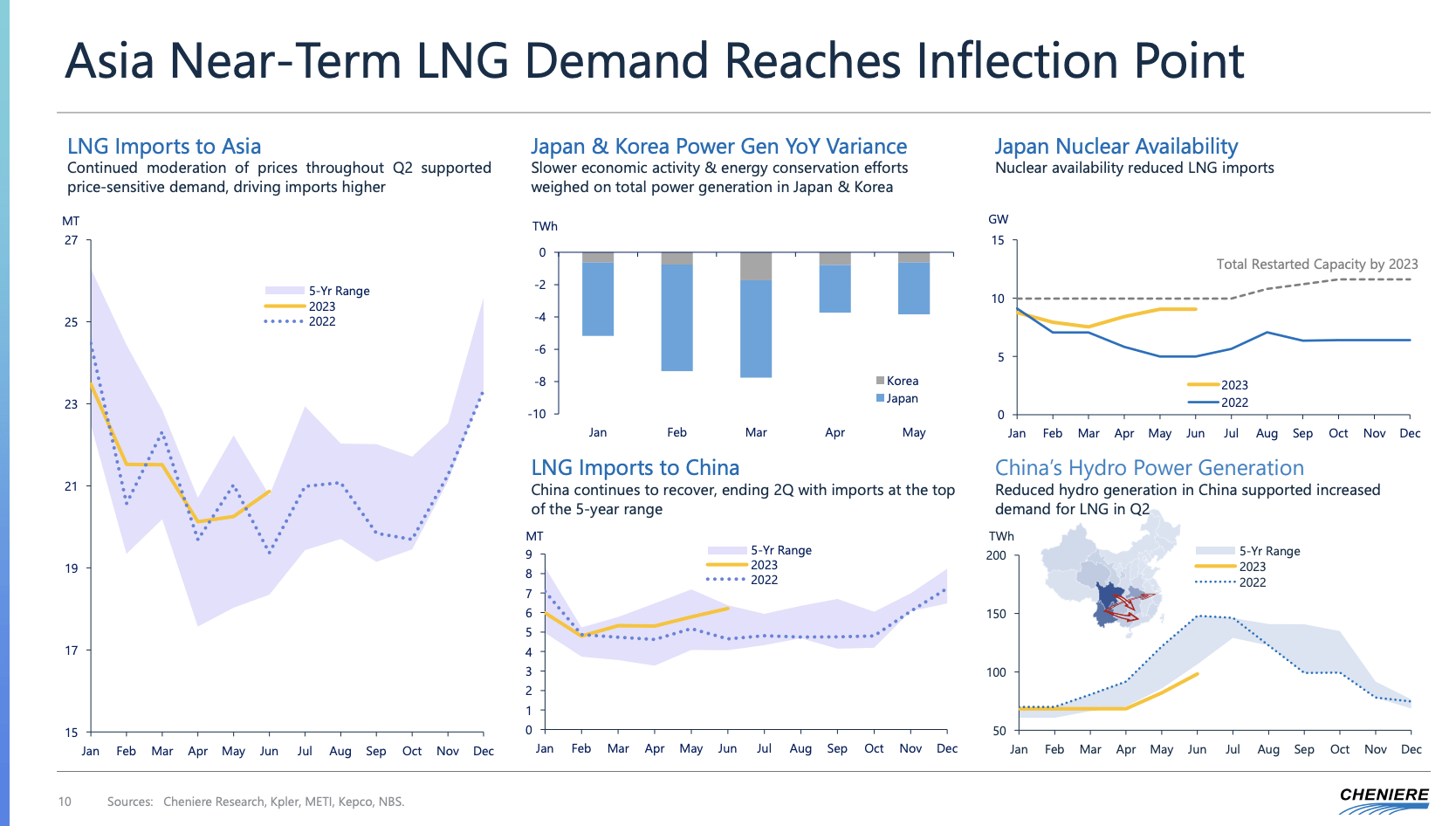

For example, despite efforts to reduce gas consumption, LNG imports to Europe grew by 9% year-on-year in the second quarter, driven by strong US growth in April and May.

However, reduced gas consumption, elevated storage levels, and decreased electricity generation caused by factors like the Russia-Ukraine conflict and slower economic growth led to challenges.

The (German) chart below shows German chemical production as of 1Q23. Demand destruction was, and still is, a major issue, which is hurting natural gas demand (to protect inventories) and wealth, as it destroys jobs, supply chain resilience, and so much more. It's also why I cannot stop tweeting about deindustrialization in Germany.

DeStatis, VCI

Despite this, natural gas was expected to regain its role in Europe's power mix as energy demand levels gradually restored, particularly with ongoing coal, lignite, and nuclear capacity retirements, which would increase demand for gas capacity.

{kind=link}

China saw increased LNG imports due to warm and dry summer conditions, resulting in a 20% year-on-year increase in the second quarter.

Essentially, reduced nuclear availability and electricity demand growth led to higher gas demand despite macroeconomic headwinds.

In contrast, Japan experienced an 18% decline in LNG demand, driven by lower imports and energy conservation measures amid electricity rate hikes.

Southeast Asian countries demonstrated mixed trends, with notable growth in Thailand due to a heatwave but challenges in Japan and Korea due to nuclear plant restarts.

{kind=link}

However, despite these challenges, the situation remains rosy. As we already discussed, Cheniere is benefiting from a lot of new long-term deals, while most of its headwinds appear to be of temporary nature (macroeconomic and weather-related headwinds).

According to the company (emphasis added):

Despite some of the near-term market dynamics discussed earlier, pointing to potentially softened demand for LNG in the front of the curve, which as Jack noted, we are largely insulated from, over the last 12-months to 18-months, we have witnessed record levels of long-term contracting, particularly for U.S. volumes as the long-term trade outlook continues to call for further growth in LNG supply .

In aggregate, the level of long-term Henry Hub linked contract signed in 2022 alone far exceeded the total signed over the six preceding years combined and the market looks to be on track to potentially repeat this level of contract activity this year.

As we previously discussed, we expect demand from China and other fast-growing Asian economies to underpin the next LNG supply wave, representing over 70% of the LNG demand growth through 2040. Asian demand, coupled with Europe's desire to replace Russian supply has driven recent commercial activity.

{kind=link}

As a result of strong tailwinds, the company also hiked its guidance.

Better Guidance & Shareholder Distributions

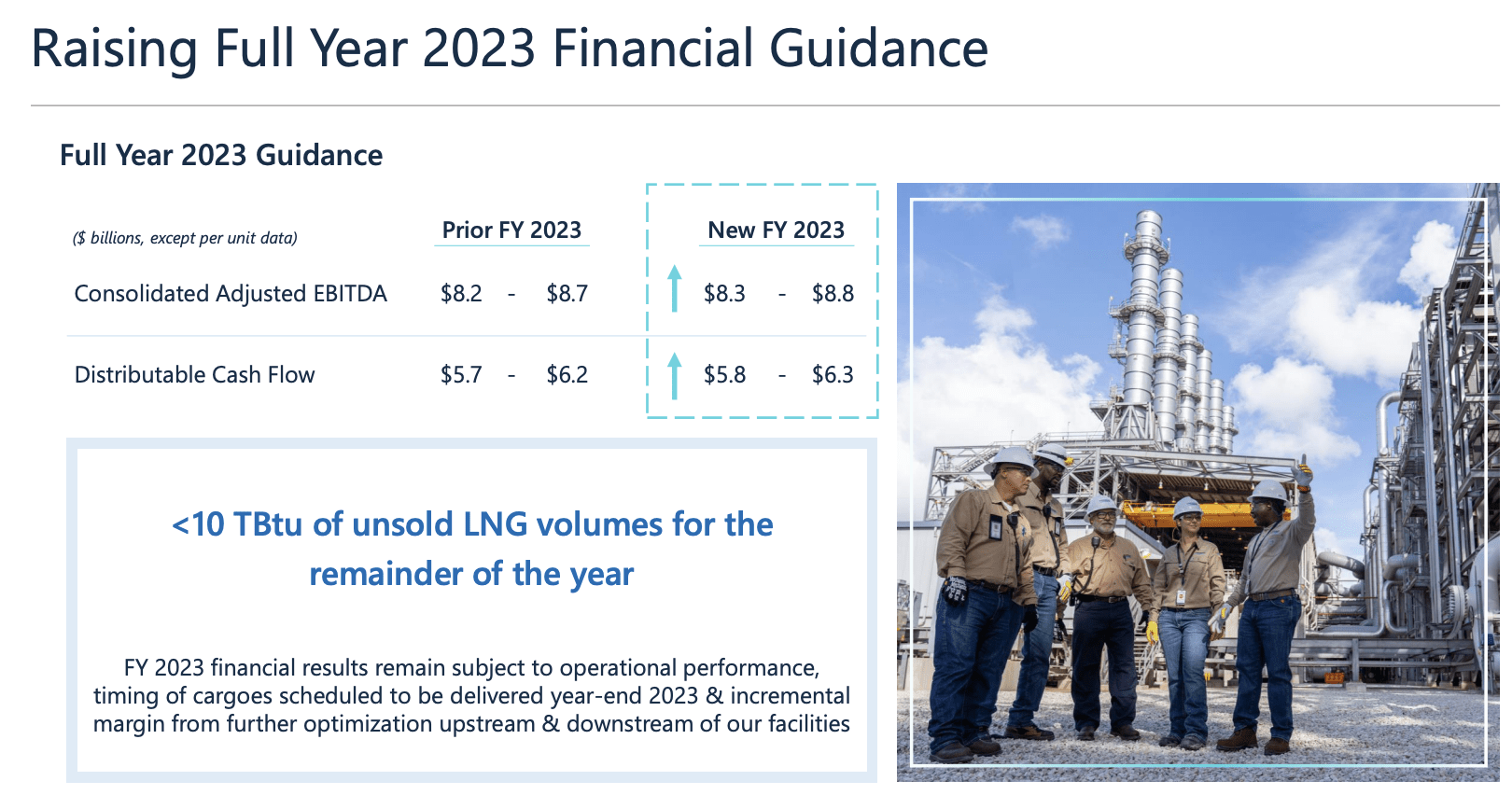

Thanks to strong numbers and a good outlook, Cheniere raised its full-year guidance ranges for 2023.

- The consolidated adjusted EBITDA guidance was increased to a range of $8.3 to $8.8 billion.

- The distributable cash flow guidance was raised to a range of $5.8 to $6.3 billion.

{kind=link}

These improvements were attributed to the release of reserved cargoes, optimization, and subchartering activities.

Also, the company's financial flexibility was further enhanced through debt reduction, share buybacks, and successful refinancing of debt maturities.

Speaking of shareholder distributions and debt, the company has declared its eighth quarterly dividend and made clear that it sticks to its plans to grow dividends in line with prior guidance, which is 10% annual dividend growth per year through the construction of Stage 3, which should be finished in 2026.

The current dividend yield is 0.9%.

Furthermore, the company has the intent to repurchase around 10% of its shares as part of a $4 billion plan.

Because the company has a healthy balance sheet with a BBB- credit rating and an expected net leverage ratio of 3x (EBITDA) if EBITDA normalizes, it has a one-to-one approach, where every dollar in debt reduction is matched by a dollar spent on stock buybacks.

Given that the company is expected to generate $2.5 billion in average annual free cash flow in the 2023-2025 period, it has plenty of cash to reward shareholders while reducing debt. After all, $2.5 billion in average FCF implies a 6.3% free cash flow.

It's also why I expect dividend growth to accelerate after 2026.

Valuation

Putting a valuation on Cheniere isn't easy. After all, it recently became free cash flow positive and is subject to a somewhat volatile market environment.

Currently, LNG is trading at just 7.3x NTM EBITDA.

The consensus price target is $200, which is 22% above the current price.

I believe that LNG's fair value is somewhere between $200 and $220, depending on the severity of the next winter and the development of macroeconomic factors influencing natural gas demand.

Takeaway

Cheniere Energy stands at the forefront of the global LNG export market, benefiting from surging demand and new long-term contracts.

As the US's largest exporter of LNG, it holds a prime position to supply Europe, Asia, and Africa with LNG.

Despite near-term challenges like softened demand and macroeconomic headwinds, the company's mature business model and strong cash flow allow it to weather these storms.

Cheniere's expanding facilities and strategic position underscores its potential for significant growth.

With an optimistic outlook and enhanced shareholder distributions, Cheniere demonstrates its commitment to rewarding investors while reducing debt.

Though valuing Cheniere proves challenging given market volatility, a consensus price target around $200 - $220 suggests substantial upside potential.

As we brace for the next winter and closely monitor macroeconomic factors, Cheniere's ability to meet growing global demand reaffirms its position as a key player in the LNG market and a promising investment opportunity.

For further details see:

Cheniere Energy: The King Of LNG - Why It Remains Undervalued