LNG - Cheniere's Current Stock Price Does Not Factor In Potential External Risk Factors

2023-11-29 00:55:35 ET

Summary

- Cheniere's revenues plunged, even as profitability improved greatly, mostly on derivatives.

- Cheniere is set to double its LNG production capacity, with several new projects and expansions in the pipeline. Global LNG supply growth is set to grow by 25% by 2026.

- The growth of global LNG demand is expected to continue, but economic considerations may outweigh the safety of supply in some countries that could opt for pipeline gas instead.

- Ample storage supplies of gas, especially in Europe, may lead to a weak LNG market this winter, which may provide for a better entry point in Cheniere stock, which is currently trading at all-time highs.

- A better entry point is desirable, given a number of external potential risks to Cheniere's future outlook, so for now, I see it as a hold, despite growth prospects within a decent P/E context.

Investment thesis: With the chaos caused by several events this decade in the world's natural gas markets, LNG producers seemed like a sure bet to take advantage of the situation. Cheniere ( LNG ) is one of the most interesting pure LNG plays in this regard. It has been ramping up its export capacity in the past years and it is about to double its LNG production capacity in the next few years from current levels. This fall and winter might not present the ideal conditions for a bullish LNG market, which comes on top of the first three quarters of this year being already weak in many respects compared with the previous year, mostly on ample storage levels in key markets such as Europe. The longer-term picture in my view continues to be bullish for the global LNG market. The next few months might be a good time to keep an eye on Cheniere as a buying opportunity based on potential short-term weakness that could push its stock price down, even as the longer-term LNG market prospects still look potentially solid. There are also potential risks to the bullish LNG thesis, therefore more risk needs to be priced into Cheniere's stock price. For now, it remains a hold, given the external potential risk/reward picture.

Declining revenues & improving profits so far in 2023. Cheniere's LNG production stagnated but more capacity is on the way.

For the first nine months of 2023 , Cheniere saw a dramatic decline in revenues, of 36%, from $24.34 billion in the first nine months of 2022, to $15.57 billion for the first nine months of the current year. The actual volume of LNG sold was down 1% for the corresponding periods. Net income increased from -$2.51 billion for the first nine months of 2022, to $8.5 billion for the same period of this year. The main stated factor that led to its losses and gains in earnings is its use of derivatives.

In terms of Cheniere's current LNG production volumes, it is currently on track to produce the equivalent of about 60-65 billion cubic meters of gas equivalent, assuming that the fourth quarter will be similar to the previous nine months. This volume is equivalent to about 3.7% of global LNG deliveries recorded in 2022. There are several new projects set to be completed as well as several expansion projects that will come online in the next few years. I will not mention them all specifically. The SPL project currently has 6 trains operational producing 30 mtpa of LNG/year, and it is set to add 3 more which will add 20 mpta more in capacity. That is equivalent to 69 billion cubic meters of natural gas in total current & future export capacity.

Other operational projects will provide a total of 53 mtpa in capacity once fully completed for the equivalent of another 73 billion cubic meters per year. All of them are set to be completed in the next few years. For reference, the total volume of LNG production capacity that Cheniere will have within a few years exceeds the total volumes of LNG that the US is set to sell to Europe this year, by a factor of roughly two. In other words, Cheniere is a globally significant factor within the global LNG industry.

{kind=link}

For Cheniere itself, building out capacity that is set to roughly double from current levels means that this continues to be a growth company, which is not easily found in the energy sector these days.

Other financial metrics of note for the period include the interest on debt, which came in at $871 million for the first nine months of the year. It comes out to about 5.6% of revenues. I tend to start to worry when this figure surpasses 5%, especially when it comes to mining or energy-related companies, where a great deal of volatility can occur, which can leave companies caught offside regarding debt servicing costs. On a positive note, interest on debt was just over $1 billion for the same period last year, so there is a seemingly improving trend. Long-term debt declined from $24.1 billion at the end of Q3, 2022, to $23.4 billion as of Q3 this year.

US natural gas supply outlook.

Building out LNG production capacity is all fine and well, but in the end, there has to be plentiful and affordable natural gas to fill the facilities with the gas that can be transformed into LNG for transport.

{kind=link}

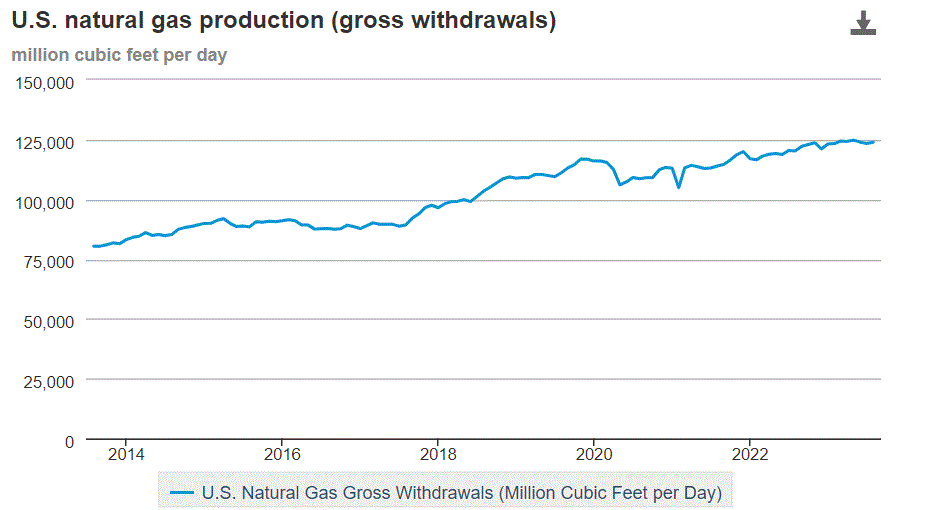

As we can see, US natural gas production has been trending up, which is mostly a reflection of the shale boom. Production reached a peak in May of just under 125 billion cubic feet/day, and it is currently down roughly 1% from those record levels as of August. The plateau in production we observe on the chart is most likely a reflection of the shale industry's reaction to lower natural gas prices this year. In other words, if the market price were to be right, the odds are that production could increase again, although it is not certain by what amount and how significant of an increase in prices it would take to make it happen.

This is a very important issue to ponder when considering one's investment prospects in Cheniere. Its LNG production capacity is set to more than double, in other words, increase by about 70 billion cubic meters (2,450 billion cubic feet) per year. In other words, US natural gas production will have to increase by around 5% in the next few years just to satisfy the expanded LNG production capacity that Cheniere is planning to bring online. That is in addition to any increase in LNG production capacity that other companies are adding as well as any increase in domestic demand that might occur. If by any chance US natural gas supplies do not increase to meet rising demand, there is a chance that Cheniere will find itself with excess LNG production capacity. If there are enough supplies, but it will come at the cost of much higher natural gas prices, Cheniere's profit margins could get squeezed. There is also a chance that political decisions will intervene to limit natural gas exports in response to high prices.

Global LNG demand trends & Cheniere's place within those trends.

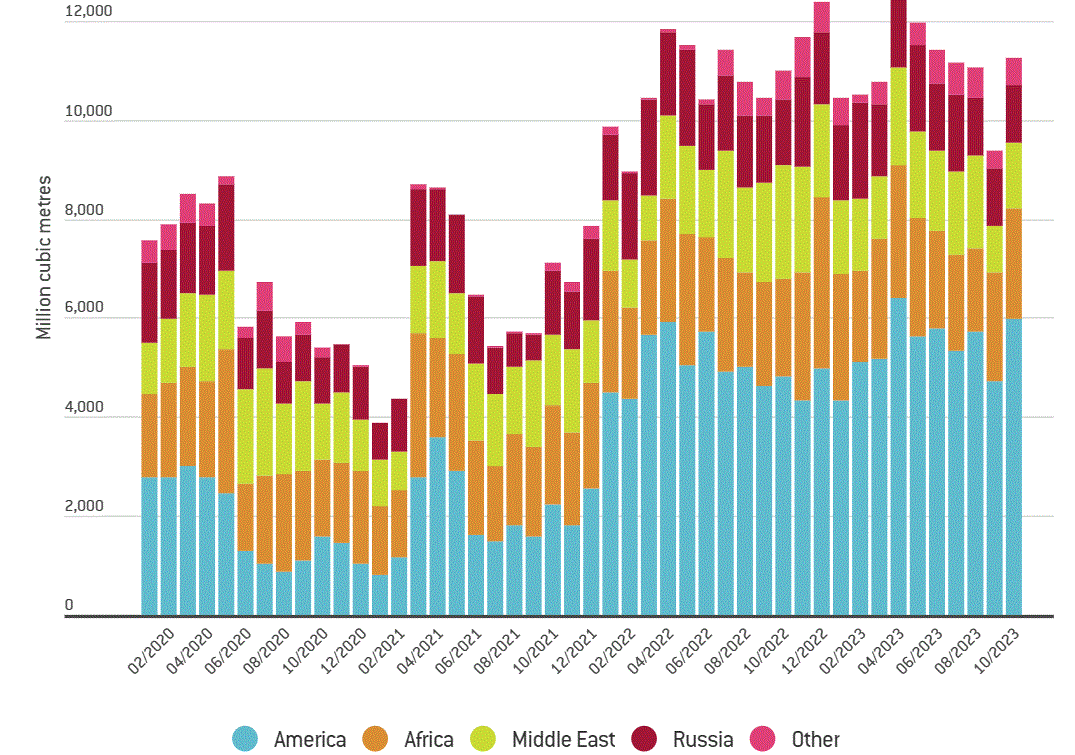

The massive disruption to the global natural gas market caused by the Ukraine war and the resulting sanctions on Russia was assumed to become a significant driver of global LNG demand growth this decade. Looking at the chart of monthly European LNG imports, it does seem to have had a significant impact on at least one market, with US LNG playing an outsized role in meeting the EU's natural gas needs, after imports from Russia were greatly reduced.

Russia was unable to immediately pivot to new markets since such a pivot requires years of investment in new infrastructure. New investment is taking place and most of it is now geared toward shifting exports to Asia. Some of it seems to be geared toward converting Russian natural gas domestically into other forms in the future such as fertilizers, plastics, and other petrochemicals. It already had a strategy to this effect in place before the 2022 war began, perhaps in anticipation of the economic conflict with the West. In other words, Russia's natural gas will gradually make it back into the global market, perhaps surpassing previous record years recorded before the COVID crisis.

In the meantime, companies like Cheniere can take market share in Europe, at least, while Russian and Central Asian natural gas supplies delivered via pipeline are set to arguably lessen China's dependence on LNG imports .

{kind=link}

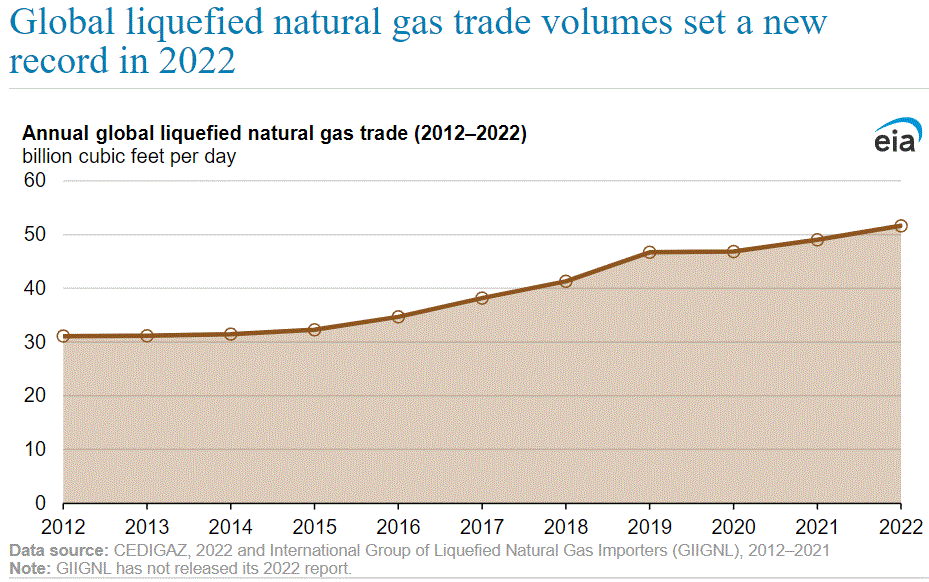

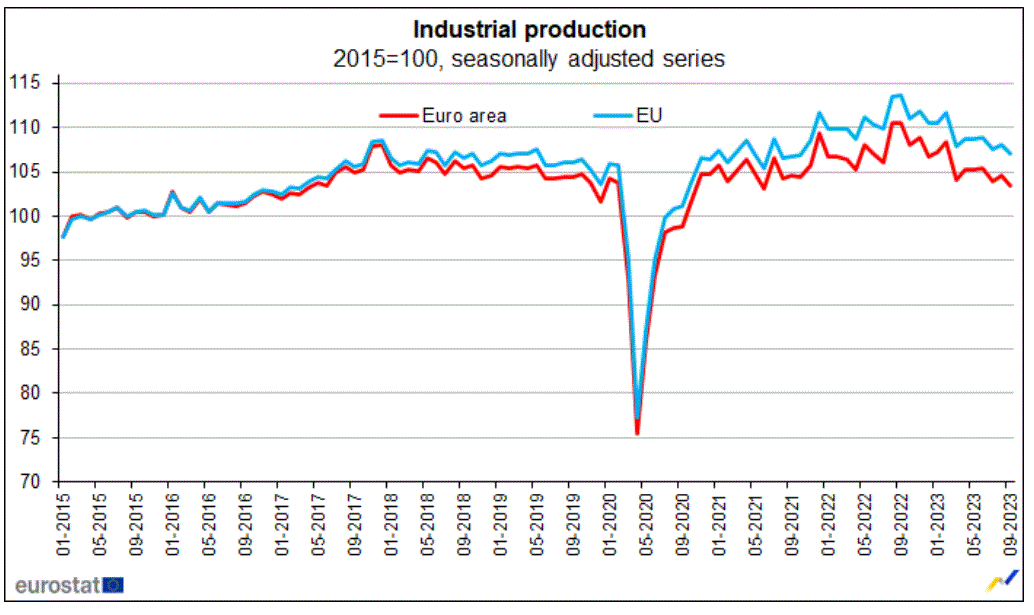

Overall global LNG demand has been on a steady path of growth and it is assumed that it will continue to grow as major natural gas importers will in theory seek to diversify natural gas supply sources for safety. It has been assumed that importers are willing to pay more to have a greater degree of safety. In my view, there may be a paradigm shift happening, as Europe's economy is increasingly struggling to compete, as it steadily pays many times more for natural gas than US consumers do. The value of cheaper natural gas for an economy is becoming increasingly clear through the European example, where the EU is losing ground fast in terms of industrial output due to higher energy prices since 2022.

{kind=link}

It remains to be seen whether economic considerations will prevail over the safety of supply, at least in countries that have a choice to make in this regard, like China. At the moment, it seems that China is choosing economic considerations, by dramatically increasing pipeline supplies from Russia and Central Asia, over having more supply flexibility through increasing reliance on LNG imports, as I already highlighted. This is an important aspect of recent developments that we need to consider in terms of future LNG market expectations. It may be that China may largely bow out of the LNG market, aside from its growing long-term deals with Qatar, which if anything, it may resell to others for a higher price on the spot markets.

If this is the case, the LNG market may lose a lot of pricing power. The EU, Japan, and South Korea, which are currently major importers, are mostly highly developed economies with a tendency toward deindustrializing and fast-shrinking demographics. Between stagnated economies and an aggressive push into green energy, these markets could shrink very fast. Developing nations such as China & India on the other hand seem more interested in getting cheap energy to fuel their continued economic expansion, therefore they are more likely to be interested in pipeline gas from Russia, Central Asia, and Iran than they might be in significantly increasing their reliance on LNG imports. Even if they buy LNG, they tend to seek imports from geographically more advantageous sources, which cost less to transport. Cheniere could therefore potentially be increasing its LNG production capacity, even as global demand growth may end up being less robust than it is currently assumed.

Investment implications:

On one hand, Cheniere, currently trading at a forward P/E ratio of just under 5, even as it is set to double its LNG production capacity compared with this year's estimated sales volume, makes it a very attractive potential investment opportunity. It is profitable, it is growing, and it is arguably not overpriced, even if we were to ignore it and not factor in its growth potential. On the other hand, it faces a dual potential external threat to its plans, as I stated in the article. There is a real risk that US natural gas production may stagnate or even start to decline as long as natural gas prices continue to stay low. Higher market prices for natural gas may stimulate more drilling, but higher natural gas prices can squeeze the profits of LNG producers, especially if the global LNG market does not see a corresponding increase in prices.

The assumed continued expansion of global LNG demand should not be taken for granted either. Cheniere is building out its LNG production capacity, and so are many other companies around the world. The IEA estimates a 25% increase in LNG supplies between 2022-2026. Given the factors I already mentioned, including expanding pipeline gas deliveries to major markets in Asia such as China & India as well as declining natural gas demand in several major developed world markets, it is entirely possible that global LNG demand will not come close to keeping pace with the flood of supply hitting the market in the next few years.

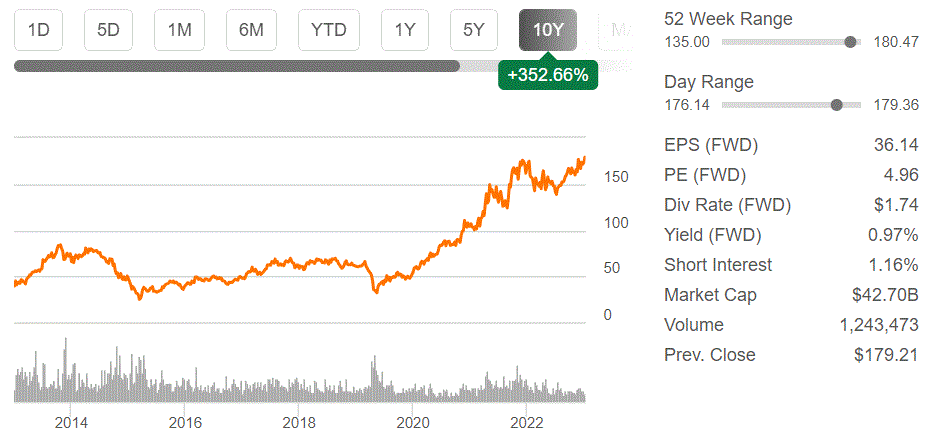

While Cheniere's current valuation and growth prospects make it an attractive investment opportunity, despite its stock price being at or near all-time highs, the potential external risk factors I highlighted should not be ignored.

{kind=link}

Depending on weather factors this winter, a potential buying opportunity may arise in the next few months, if Europe for instance will cut back on LNG imports on ample storage . A 20% decline in its stock price would provide a better entry point that would reduce the risk from the external factors I mentioned. It would also improve the dividend, which is currently at just under 1% correspondingly, making it a more attractive buy & hold. For now, however, with its stock price at or near its all-time high, it remains a hold for me.

For further details see:

Cheniere's Current Stock Price Does Not Factor In Potential External Risk Factors