CRK - Chesapeake And Southwestern Combination Presents Attractive Pairs Trade Opportunity

2023-10-23 01:17:10 ET

Summary

- Chesapeake Energy has approached Southwestern Energy about a potential merger in the natural gas space.

- The merger would create a company valued at $20.5 billion, equivalent to EQT Corporation.

- The combined company will have annual natural gas production of 3Tcf, making it the largest independent producer of natural gas in the US.

Reuters reported on October 17, 2023 , that Chesapeake Energy ( CHK ) has approached Southwestern Energy ( SWN ) about a potential merger. This is huge news given the fact that the two firms are some of the biggest players in the natural gas space in the Marcellus and Haynesville basins. Chesapeake currently trades at a market cap of $12,610mm and an enterprise value of $13,743mm at 2.14x EV/EBITDA, net of asset sales. SWN’s market cap is currently valued at $7,950mm for an enterprise value of $11,960mm and currently trades at 2.09x EV/EBITDA, a discount to CHK and the broader E&P market. The combination would create a company valued at $20,560mm by market cap, equivalent to EQT Corporation ( EQT ). Considering the fundamentals, I provide CHK shares a SELL rating for a price target of $86.94/share at 2.12x EV/EBITDA, net of asset sales, and SWN a BUY rating for a price target of $9.34/share for a target multiple of 2.5x EV/EBITDA, a 30% premium to the current price of SWN shares.

Please review my analysis on Southwestern Energy dated June 5, 2023.

I will do a brief analysis of Chesapeake independent of Southwestern followed by a business combination analysis with an analysis of firm valuation in the same format.

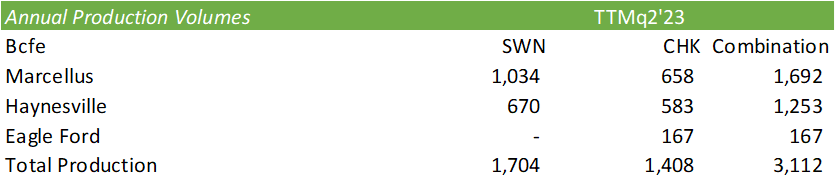

As of q2’23, Chesapeake Energy owned a total of 5,400 oil and dry gas wells across the Eagle Ford, Marcellus, and Haynesville/Bossier basins for total production volumes of 1,408Bcfe. Chesapeake announced the sale of the remaining Eagle Ford properties on August 14, 2023 for $700mm, bringing in a total of $3.5b from the complete sale of their Eagle Ford properties. Between the sale of the Eagle Ford and Powder River Basins, Chesapeake has completely refocused its resources to natural gas production in the Appalachia region and Haynesville/Bossier basin. Chesapeake announced a long-term, 15-year LNG supply agreement signed with Gunvor in March 2023 to supply up to 2mpta. This equates to roughly 98bcf/year, or 8% of Chesapeake’s total production between the Marcellus and Haynesville/Bossier as of q2’23. The agreement will index gas prices to the Japan Korea Market, which has a significant premium over Henry Hub prices. Comparing futures contracts , Japanese LNG December 2023 contracts are priced at $18.245 whereas Henry Hub futures are priced at $3.326. North West Europe’s market December 2023 contract is currently priced at $16.135. Assuming prices remain constant at $18/mcf, this should generate ballpark $1,764mm in revenue for Chesapeake, holding all else equal.

{kind=link}

Financials

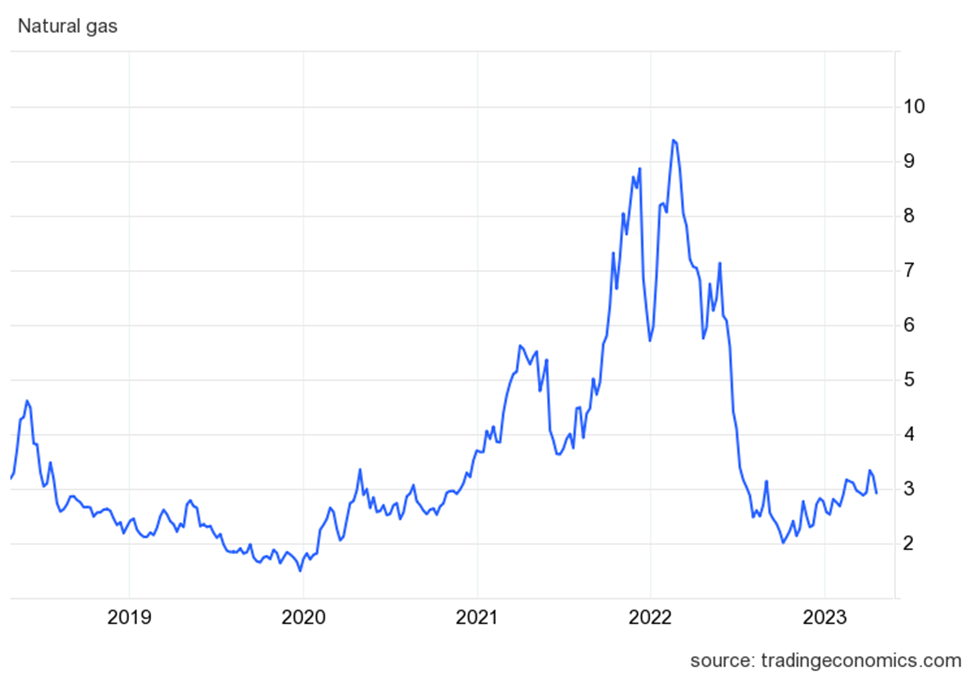

Like the rest of the industry, natural gas prices haven’t been on the side of the producers. Given the robust natural gas market in 2022 between the ongoing Russia/Ukraine war, Europe’s natural gas crisis as a result of Russia turning off Nord Stream I, and the mild winter weather experienced across Europe, natural gas prices have significantly fallen from their $9/mcf peak back down to historical norms between $2.02 in April 2023 to $3.30 in early October. CME Group is currently pricing natural gas futures between $3 and $3.77 through November 2024 before reaching $4.22 in December. Unless another exogenous event occurs, FY24 will still look significantly better than FY23 but remain suppressed compared to FY22.

{kind=link}

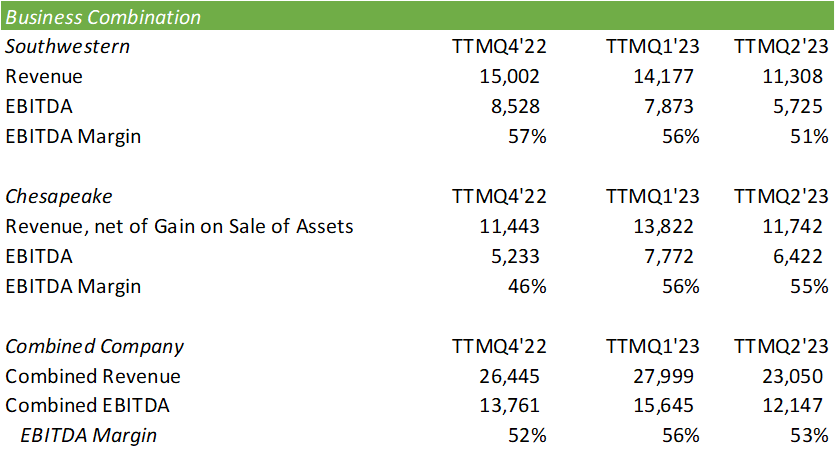

As of q2’23, Chesapeake has 65% of 2h23 natural gas hedged with a $3.45/Mcf and $3.55/Mcf floor in q3’23 and q4’23, respectively. On a TTM basis, revenue from natural gas, oil, and NGLs dropped by 23% from the previous year with their EBITDA margin net of asset sales compressing to 54.7% from 56% from the previous year. The decline in revenue was the result of a combination of reduced volumes and pricing per equivalent as total volumes dropped from 4,125MMcfe/day to 3,653MMcfe/day for realized prices dropping from $7.43/Mcfe to $1.97/Mcfe for q2’22 & q2’23, respectively. Strategically, reducing volumes at both the Haynesville/Bossier and Marcellus was an appropriate tactic as the Haynesville/Bossier assets hold significantly more value when LNG export is tied to the equation. This tactic was also employed by Southwestern Energy when comparing 1h23 to 1h22.

There is a huge opportunity coming in the back half of 2024 with Chesapeake’s 35% interest in the Momentum Sustainable Ventures natural gas gathering pipeline and CCUS project. The pipeline will provide Chesapeake an initial capacity of 1.7Bcf/d with an expansion to 2.2Bcf/d on natural gas transport from the Haynesville Shale to the Gulf Coast LNG export market. As the Exxon/QatarEnergy JV Golden Pass LNG export terminal is set to come online at the end of 2024, this should provide an ideal opportunity for Chesapeake as an excess of 3.20Bcf/day of free capacity will come online at around the same time the pipeline is complete. I highlighted some of the features of the Golden Pass terminal in my analysis of Comstock ( CRK ) dated October 5, 2023.

Chesapeake’s capital structure is relatively debt-light with $2,036mm of debt on books for a net debt/EBIDAX, net of asset sales of 0.175x. Management has made it clear that they will not be utilizing bond issuance to grow their asset base, but rather, rely on cash flow from operations, cash, and their revolving credit facility. Total liquidity sums to $2.9b as of q2’23. Given the latest Eagle Ford asset sale, their liquidity should be increased to $3.55b with an additional $50mm in one year post-sale. Chesapeake also has a contingency with SilverBow to receive an additional $25-50mm if the average price/bbl sustains between $75-80/bbl or above $80/bbl, respectively. This is certainly not your father’s Chesapeake Energy.

Shareholder Value

Chesapeake Energy certainly brings a lot of value to shareholders through both share buybacks and their use of the industry standard fixed plus variable dividend rate. Chesapeake currently has a $2b buyback program, representing 16% of their market cap, that expires 12/31/23 with $1,248mm shares repurchased as of q2’23. Their last dividend rate paid in August summed to $1.18/share with $0.63/share attributable to the variable portion of the dividend rate. Though the variable portion is 66% lower than that paid q2’22, there may be additional value to be seen in future dividend payments as Chesapeake focuses more on natural gas sales through LNG exports.

Business Combination

Considering the combination of Chesapeake Energy and Southwestern Energy, the combination will be more operationally accretive for Southwestern Energy.

{kind=link}

The combined company will have a book value of $49,561mm in proved and unproved oil and natural gas properties, net of the announced sale of the Eagle Ford properties, assuming a 23% profit on the sale above book (based on historical Eagle Ford sale). The acquisition of Southwestern will nearly triple Chesapeake’s natural gas properties, providing Chesapeake with more assets to leverage for future operations. This can provide the combined firm a stronger competitive advantage to rig pricing and allow for more strategic drilling across their properties as natural gas prices remain suppressed.

Considering a trade, SWN shares trade at a small relative discount to CHK at 2.09x EV/EBITDA to CHK’s 2.14x net of asset sales. I believe the appropriate pair trade will be to SHORT CHK shares with a price target of $87.12/share and go LONG SWN shares with a price target of $9.34/share for a multiple of 2.5x EV/EBITDA, a 30% premium to Friday's closing price of $7.21/share, assuming this deal goes through.

The short position recommendation comes with two factors. The first is through multiple compression as a result of the acquisition and the second relates to the acquisition potentially being funded with both cash and equity, resulting in SWN shares being converted into CHK shares. This will in turn result in the converted shares covering the short position. This short position is a short-term merger arbitrage trade and should not be expected to see much further downside risk as a result of the acquisition. The borrowing cost to short CHK is 35bps. If you are not an active trader, I do not recommend the short leg of this trade and only recommend the long position in SWN. Long-term, after this price adjustment, I will be updating my recommendation for CHK to a BUY given their low valuation both independently and as a combined company.

For further details see:

Chesapeake And Southwestern Combination Presents Attractive Pairs Trade Opportunity