SWN - Chesapeake Energy And Southwestern Energy: A Big Bet On Big Savings

2024-01-14 22:29:03 ET

Summary

- Chesapeake Energy and Southwestern Energy have announced a merger in an all-stock transaction valued at $7.4 billion for the latter.

- The combined company will be the third-largest publicly traded gas producer, with significant gas production in the regions in which it operates.

- The merger aims to create significant synergies, with expected annual cost savings of $400 million, and plans to build a global marketing and trading presence in Houston.

The past 12 months have seen a number of massive transactions announced in the energy space, particularly related to the fossil fuel market. Mergers and acquisitions open up many interesting doors for shareholder value creation. Significant synergies can arise from companies combining together, especially when they have complementary or overlapping assets. The latest such move was announced by the management teams of Chesapeake Energy Corporation ( CHK ) and Southwestern Energy Company ( SWN ) on January 11th. This did not come as a major surprise, however. I say this because rumors began circulating the week prior that a deal between the two companies was in the works. On top of this, the other major transactions in the space leading up to this point made it unlikely that these two sizable players would just sit idly by and do nothing.

For my own Marketplace service on Seeking Alpha, Crude Value Insights, I cover 36 companies whose operations are largely focused on the exploration and production niche in the oil and gas industry. Both of these are companies that I have covered before. My most recent conclusion about each is that they are not all that appealing on their own. However, this particular transaction is interesting because of the potential for additional value creation from some rather large synergies. At the end of the day, I would say that the deal is quite balanced. But if there was one winner from this transaction, it would likely be Chesapeake Energy.

An interesting transaction

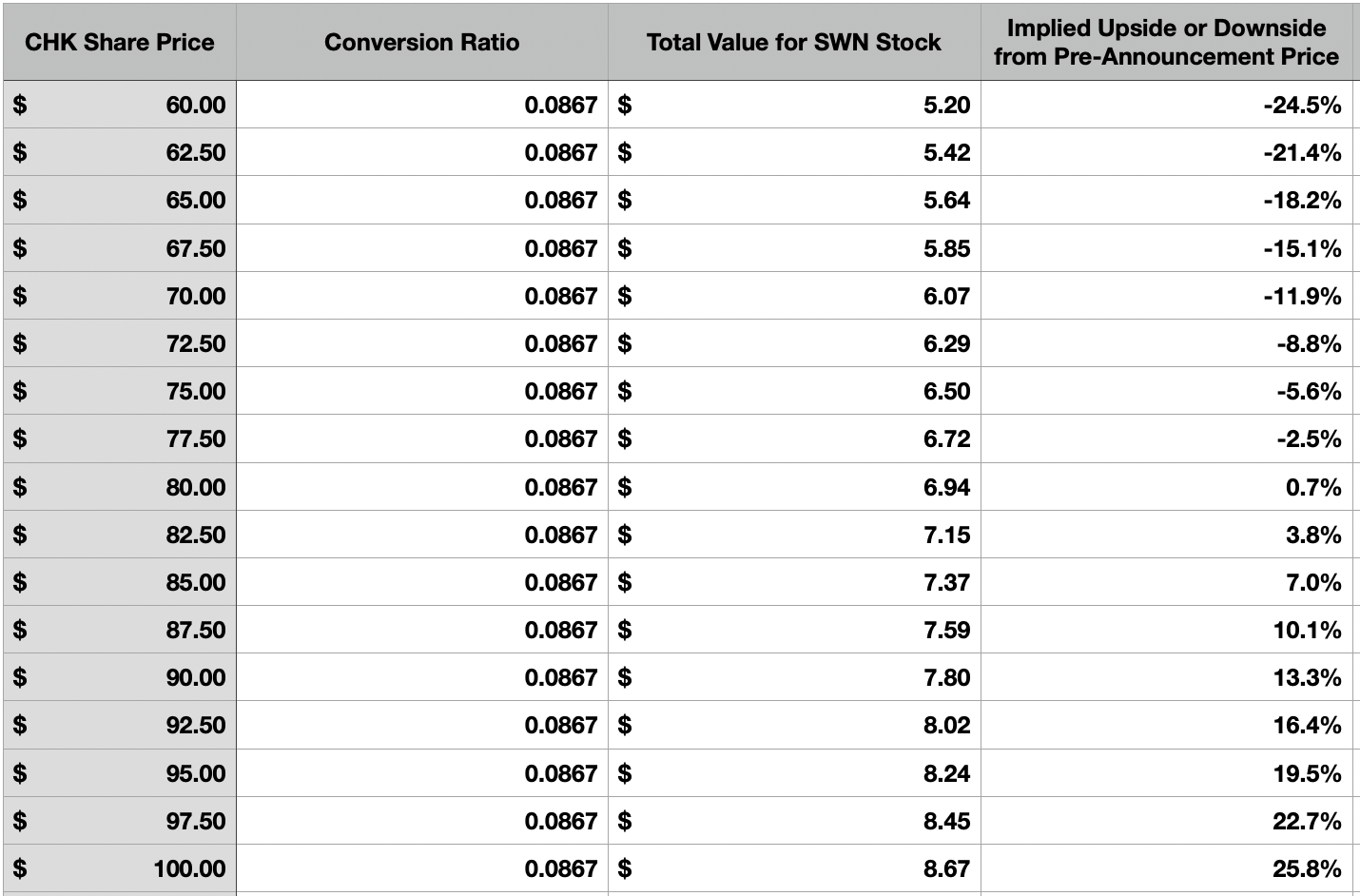

On the morning of January 11th, the management teams at Chesapeake Energy and Southwestern Energy announced that the two companies would be merging in an all-stock transaction valuing the latter at about $7.4 billion, or $6.69 per share. According to the terms of the agreement, Chesapeake Energy will essentially absorb Southwestern Energy by issuing 0.0867 of a share for each unit that shareholders of Southwestern Energy hold at the time of the closing of the transaction. Even though this may not seem like much, the end result will be a rather large combined company that will have an enterprise value of more than $23 billion. Based on my own math, shareholders of Chesapeake Energy today will end up owning 59.8% of the combined firm, with the remaining 40.2% owned by shareholders of Southwestern Energy.

{kind=link}

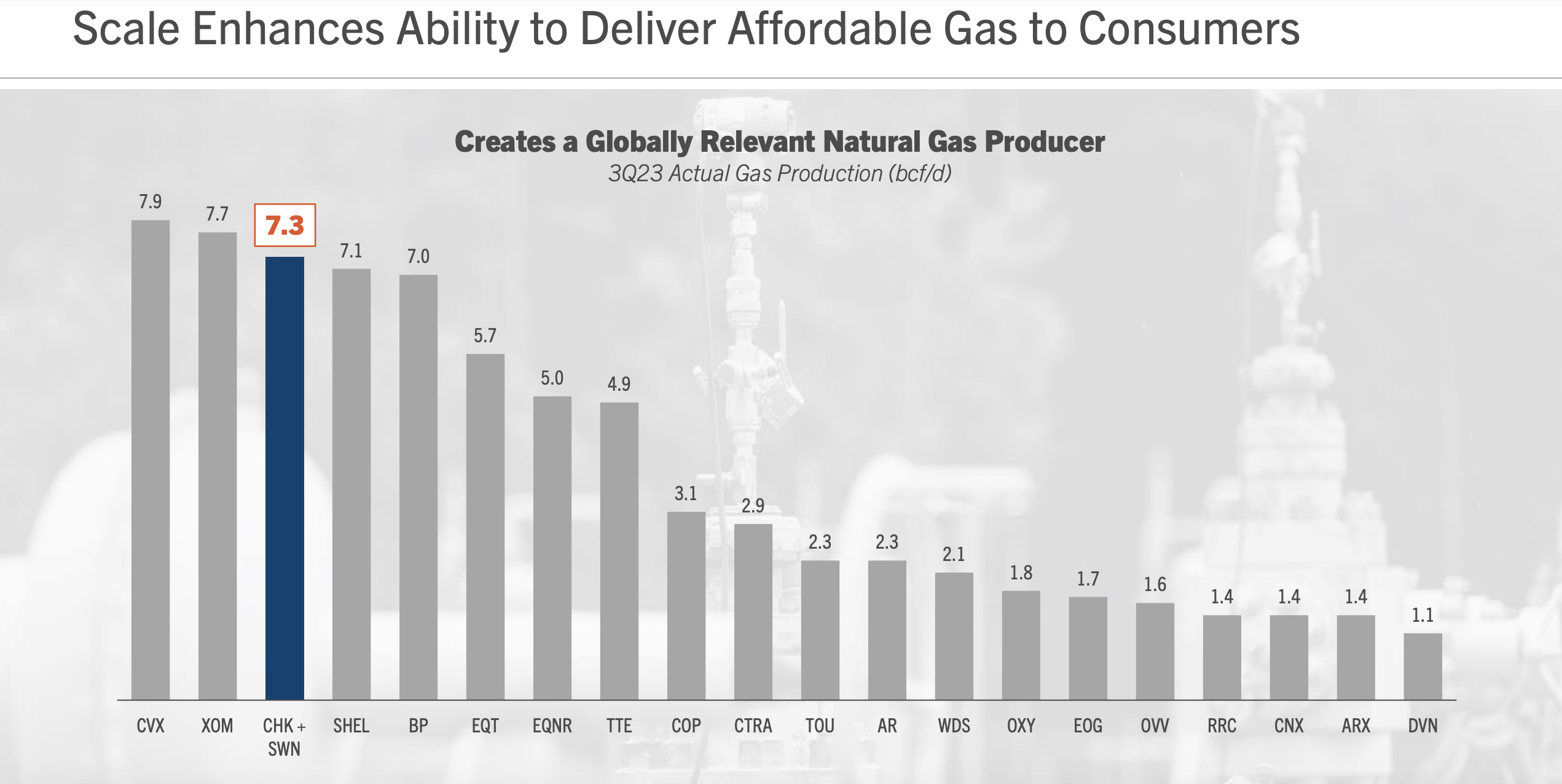

In the oil and gas exploration and production market, size can yield many benefits. And few companies will be larger than this combined firm. According to management, using data from the third quarter of the 2023 fiscal year, Chesapeake Energy and Southwestern, on a combined basis , will be responsible for approximately 7.3 bcf per day worth of gas production. This will make it the third largest publicly traded gas producer, not far behind Chevron ( CVX ) and Exxon Mobil ( XOM ). The combined company will have over 5,000 gross extraction locations across Appalachia and Haynesville, both of which are major natural gas producing regions.

{kind=link}

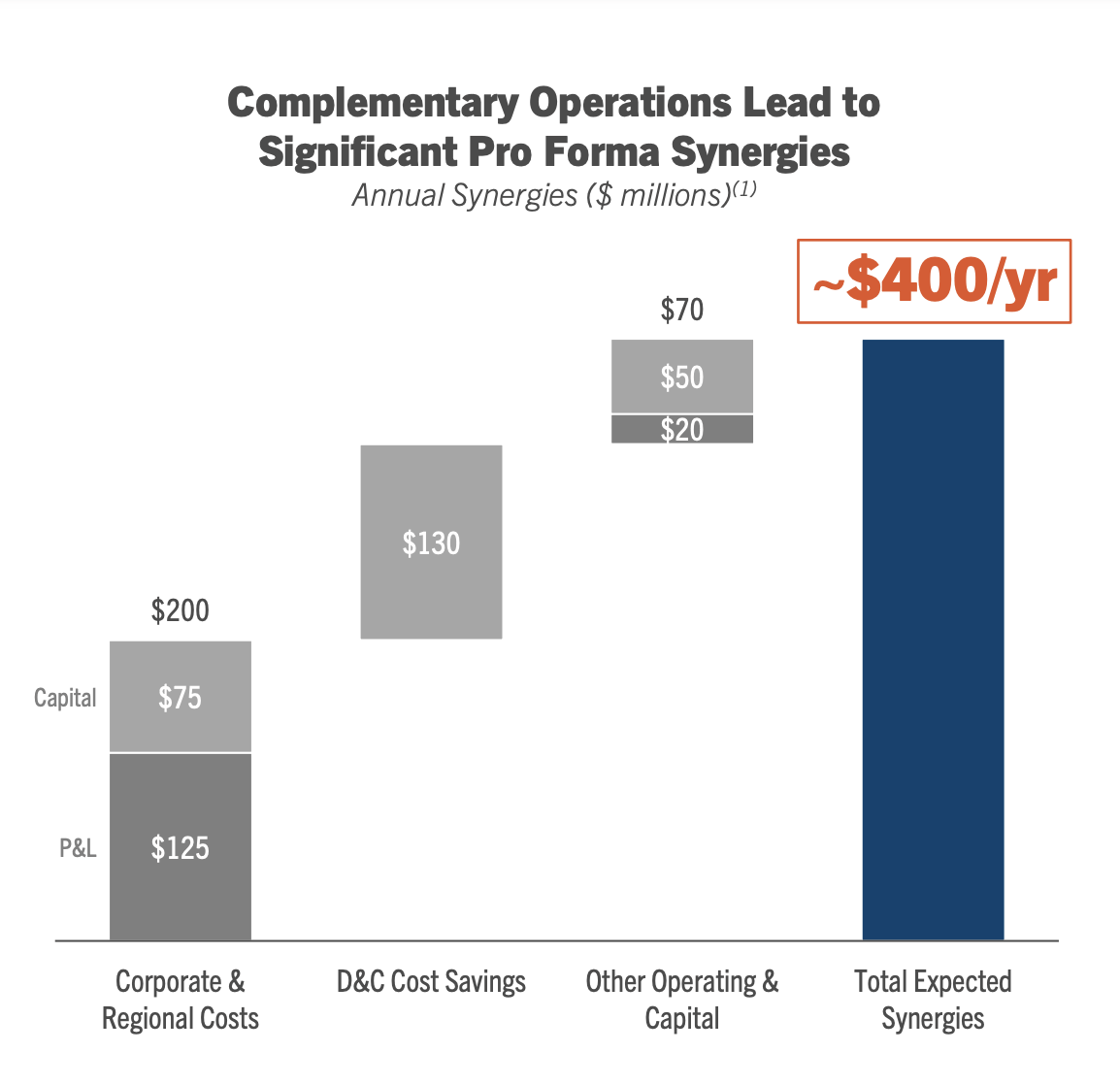

Management's goal from this combination is to create significant synergies for the combined company. The expectation is for annual run rate synergies to come in at around $400 million. Approximately $200 million of this will come from corporate and regional cost cutting. Much of that would be reduced regulatory fees, combined with the cutting of duplicative staff and processes. After all, you now need only one investor relations department and one accounting department, not two separate ones. But there are other cost savings plans included in this as well. Management believes that it can cut about $130 million per annum worth of drilling and completion costs. And on top of this, the company is targeting $70 million of other operating and capital cost cuts.

When you look at the map of resources that these two companies have, it becomes clear how some of this cost cutting will be possible. As you can see in the image below, there is significant overlap for the two companies throughout the Haynesville region, with almost all of that overlap occurring in Louisiana. There's also some overlap in Pennsylvania, though not nearly as much as when it comes to Haynesville. Geographic proximity can be incredibly important when it comes to cost cutting initiatives because it allows not only for the companies in question to exercise buying power when it comes to service providers, but also because it allows the clustering of resources that results in quick and easy cost reductions.

{kind=link}

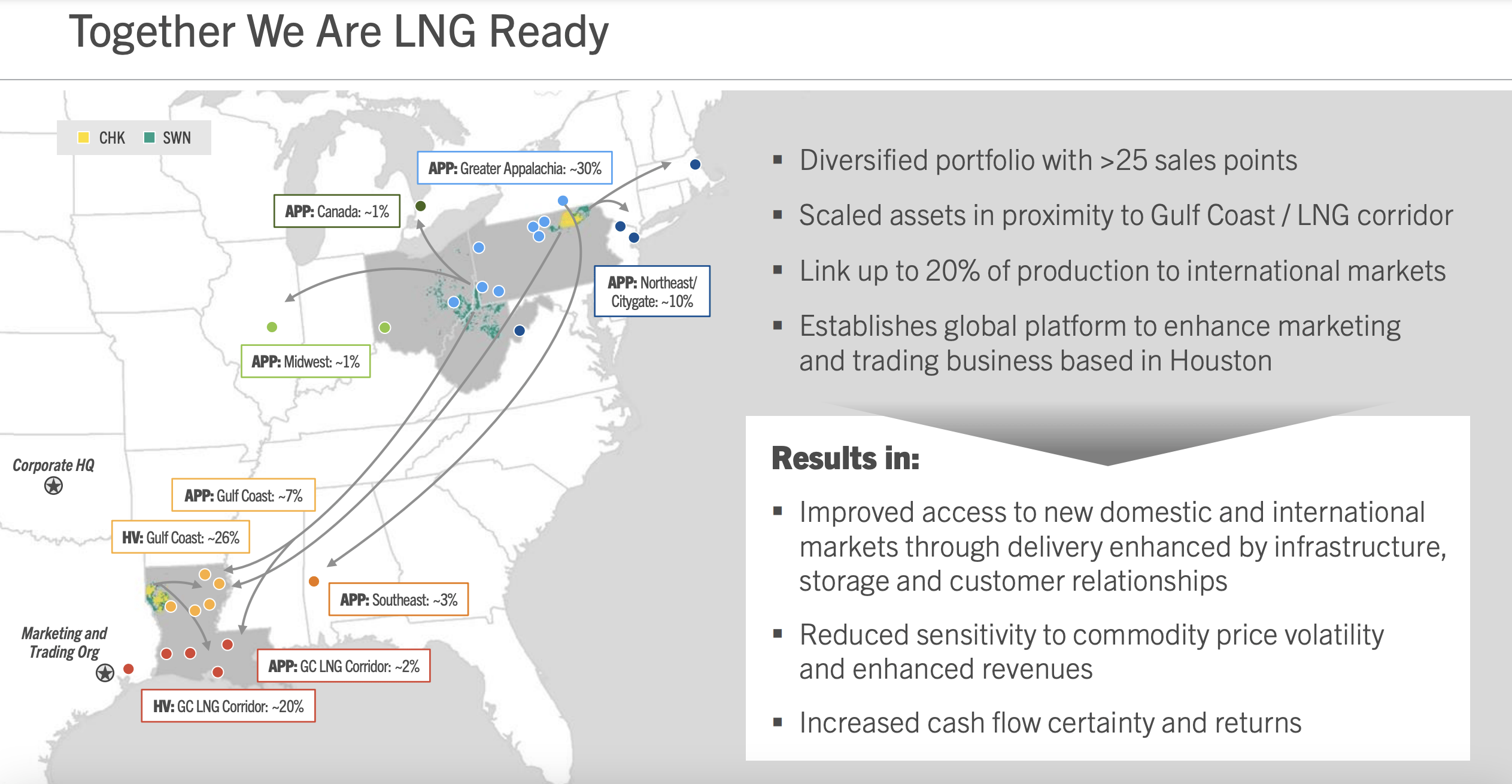

Outside of the cost side of things, there are some other reasons for such a transaction. For starters, LNG (liquified natural gas) is becoming a big thing. As you can see in the image below, the combined firm would be well positioned from a geographical perspective to cater to this growing trend. Management's goal is to ultimately use the resources at their disposal to build a 'global marketing and trading presence in Houston to supply lower cost, lower carbon energy to meet increasing domestic and international LNG demand'. The firm plans to even use what it believes will be improved credit metrics to open the door to additional opportunities in this space and to optimize returns through lower borrowing costs and a greater ability to pay down debt.

{kind=link}

After declaring bankruptcy in 2020, Chesapeake Energy was able to shed a tremendous amount of its debt. Today, the company has net debt of only $1.25 billion. Unfortunately, Southwestern Energy is a bit more heavily leveraged than that, with net debt of $4.09 billion as of the end of the most recent quarter for which data is available. However, assuming that energy prices don't tank, management intends to target about $1.1 billion of debt retirement by the end of 2025. The combined company does not have any debt coming due until 2025 when it has to repay $389 million. So in all likelihood, the firm will make a tender offer for some chunks of its debt between now and the end of that year.

For those worried about the distribution, my answer would be that you should not be. For starters, if management can achieve the debt reduction target that they are looking at, it would mean a net leverage ratio lower than 1. That's quite attractive in the space. In addition to that, management reiterated their commitment to paying out distributions to shareholders. Actual amounts will vary based on energy prices and overall financial performance. But management believes that annual distributions of between $1 billion and $1.5 billion would be realistic moving forward, with an initial goal of $1.4 billion annually. This would make the business the 5th largest exploration and production player as measured by total cash outlays for shareholders. However, investors should be prepared for the nature of the distribution to be a bit different. Management intends to have a base distribution of about $2.30 per annum. After that, they would take free cash flow, strip out amounts allocated for distribution, and take 50% of what's left for what they are calling a variable dividend.

{kind=link}

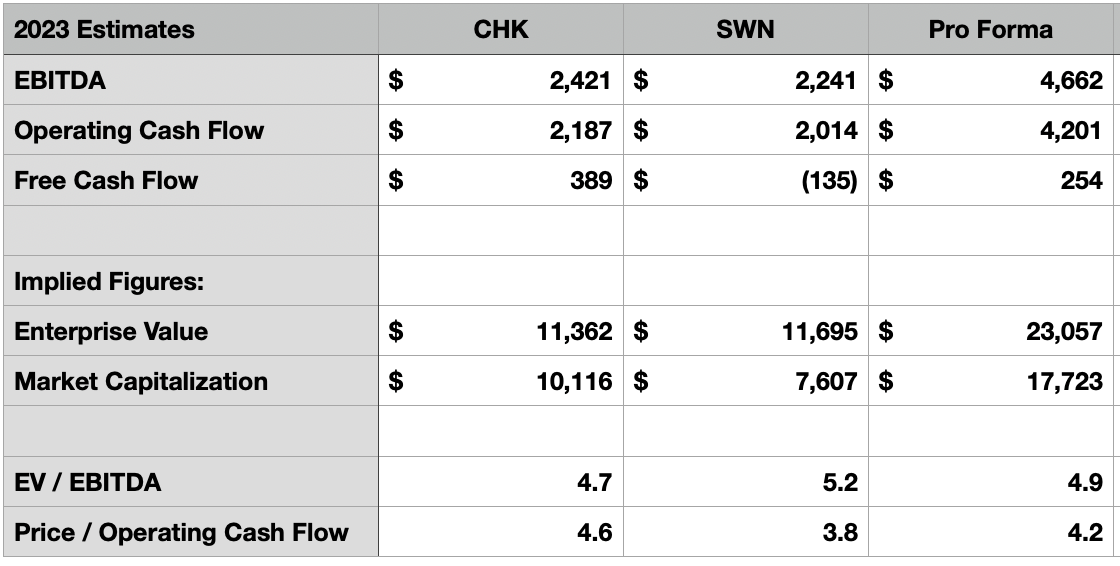

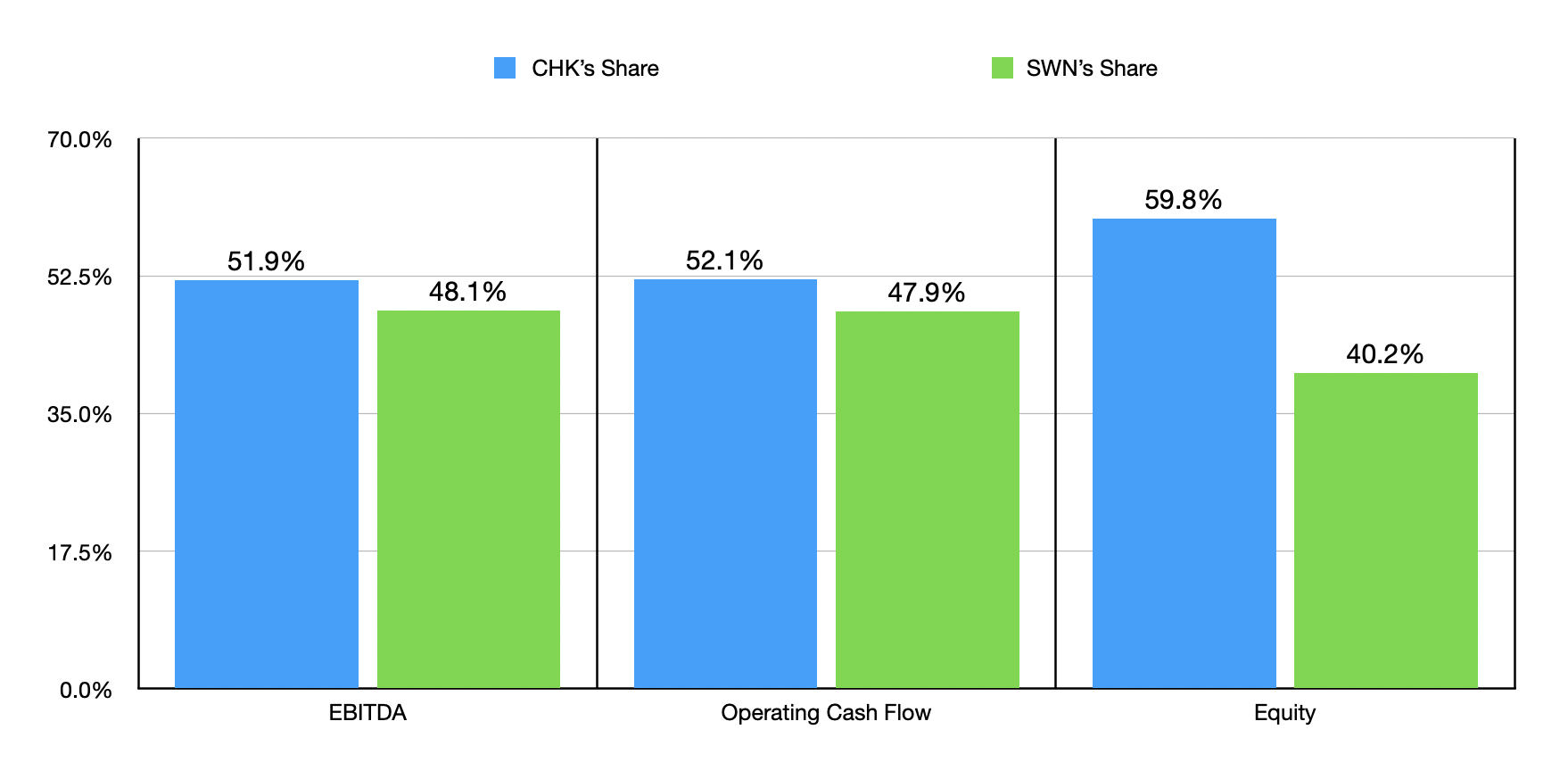

Now, in terms of whether or not this transaction makes sense, there are a couple of different ways that we can evaluate the picture. For starters, in the table above, you can see some cash flow metrics that I calculated for each of the companies based on the models, here and here , in my Marketplace service and the most recent guidance, here and here , and updated energy prices provided by management for the 2023 fiscal year. As you can see, the companies produce a similar amount of EBITDA and operating cash flow. The acquirer, Chesapeake Energy, is ultimately responsible for 51.9% of EBITDA but its shareholders are getting an outsized portion of the company, with total ownership amounting to 59.8%. When it comes to operating cash flow, Chesapeake Energy is contributing about 52% to the combined firm.

{kind=link}

What this initially tells us is that Chesapeake Energy is getting a larger share of the pie relative to the cash flows it generates. But there are a couple of other caveats here. For starters, Southwestern Energy should actually generate negative free cash flow in the current environment. That compares to slightly positive free cash flow for Chesapeake Energy. On the other hand, Southwestern Energy has more to show for that extra spending. I say this because, from 2022 to 2023, Southwestern Energy has seen its total production drop by 3.7%. But for Chesapeake Energy, the year over year production decline should be about 8.3%. So if anything, it should be spending more in order to keep output at a level more in line with Southwestern Energy. Though it's hard to tell, it is possible that difference might push the company into a position of being free cash flow neutral or negative.

Another way to evaluate this is to look at the trading multiples at the implied merger prices. On a price to operating cash flow basis, Chesapeake Energy is the more expensive of the two companies with a multiple of 4.6. That compares to the 3.8 reading that we get for Southwestern Energy. But when we switch over to the EV to EBITDA approach, the picture is different. In this case, Chesapeake Energy is trading at a multiple of 4.7 compared to the 5.2 for Southwestern Energy. Both of these are more or less in line for what I have seen over the past year or so in the space. But the argument that I would make is that Chesapeake Energy is getting a larger chunk of the pie because it is inheriting a rather sizable chunk of debt that it otherwise wouldn't have.

Takeaway

As things stand, I still do not find myself all that drawn to either of these companies. Combined, the extra cash flows they might generate because of synergies could make them more interesting. But investors should always be worried about relying too much on forecasts of cost savings because, from my experience, they don't always pan out. Because of the higher leverage, Southwestern Energy is the less appealing of the two prospects. This makes it justifiable for its counterpart, Chesapeake Energy to get a larger chunk of the pie. If synergies do come to fruition, I could become a bit more bullish on either firm. But for now, I believe that a 'hold' rating for each makes sense.

{kind=link}

It is entirely possible that I would turn out to be wrong and that both companies could appreciate nicely. The market did push shares of Chesapeake Energy higher by the amount of 3.2% in response to this development. So there clearly is some optimism there, but how much upside exists for either firm will depend on the other. More likely than not, Southwestern Energy will move more in line with Chesapeake Energy now as the image above illustrates. On the other hand, I would like to point to my own track record with Chesapeake Energy. I first became bearish on the company in August of 2019. And by November of that year, I downgraded the company to a 'strong sell', even going so far as to saying that, 'the end is fast approaching' for the business. I was probably one of the first analysts to predict bankruptcy for the company. So while I fully embrace the possibility of being wrong this time around, I think that my neutral stance on the company as it stands today is perfectly appropriate.

For further details see:

Chesapeake Energy And Southwestern Energy: A Big Bet On Big Savings